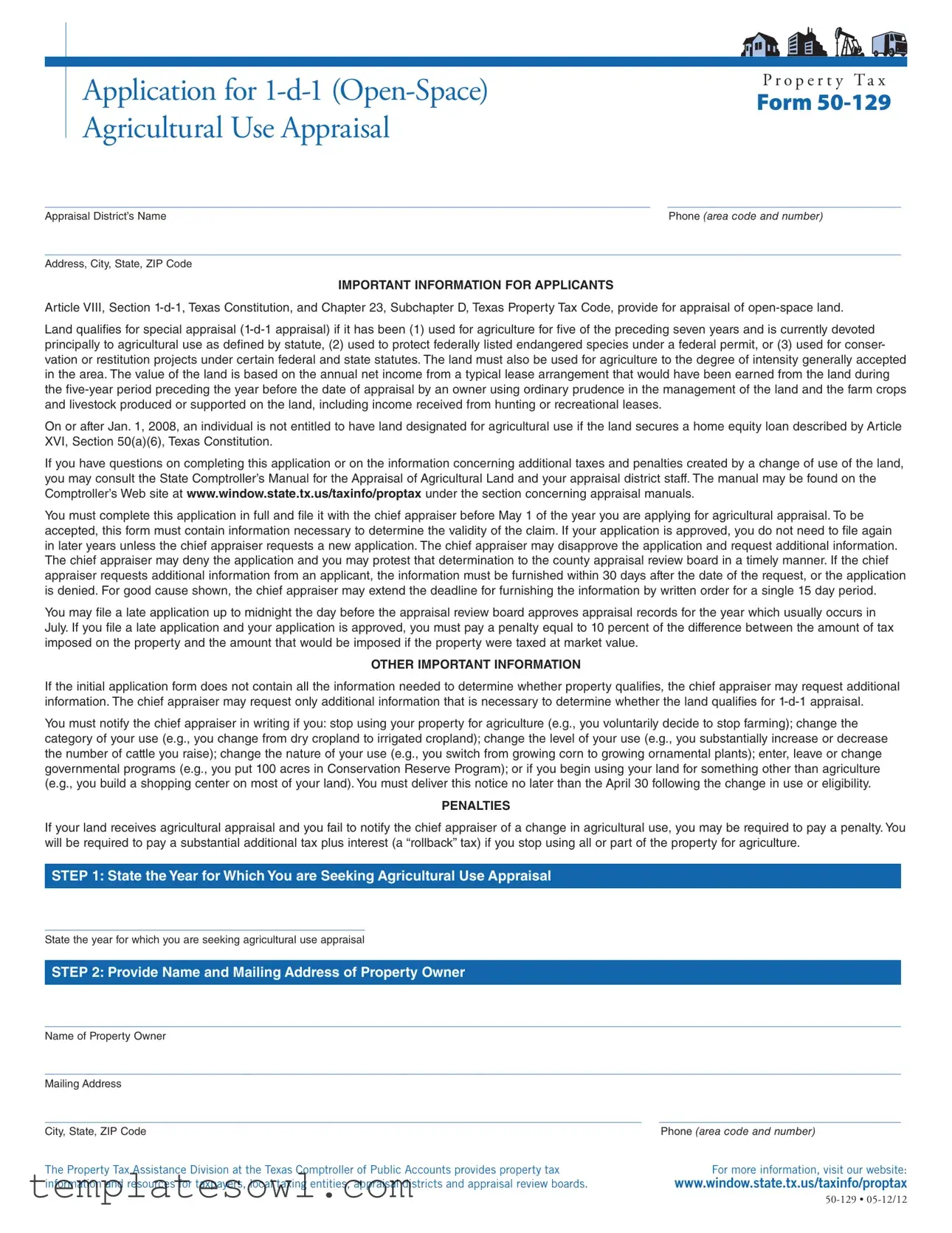

Fill Out Your 1 D 1 Open Space Agricultural Valuation Form

The 1 D 1 Open Space Agricultural Valuation Form is a vital tool for landowners looking to benefit from special property tax appraisals in Texas. This form allows property owners to apply for agricultural use appraisal based on specific criteria outlined in the Texas Constitution and Property Tax Code. To qualify for this designation, property must have been used primarily for agricultural purposes for five out of the last seven years and must adhere to certain guidelines regarding use intensity and type. Eligible uses include traditional agriculture, wildlife management, and conservation efforts for endangered species. The valuation for the land is determined by assessing its net income potential from average lease agreements in the area over the previous five years. Applicants must submit the completed form to the chief appraiser by May 1 of the application year, including comprehensive information about the property's agricultural use, ownership status, and any recent changes in land utilization. Failure to comply with these requirements may lead to penalties, including additional taxes. Understanding these requirements and accurately completing the form can facilitate a smoother application process while ensuring compliance with state laws.

1 D 1 Open Space Agricultural Valuation Example

Application for

P r o p e r t y T a x

Form

______________________________________________________________________ |

_ ___________________________ |

Appraisal District’s Name |

Phone (area code and number) |

___________________________________________________________________________________________________

Address, City, State, ZIP Code

IMPORTANT INFORMATION FOR APPLICANTS

Article VIII, Section

Land qualifies for special appraisal

On or after Jan. 1, 2008, an individual is not entitled to have land designated for agricultural use if the land secures a home equity loan described by Article XVI, Section 50(a)(6), Texas Constitution.

If you have questions on completing this application or on the information concerning additional taxes and penalties created by a change of use of the land, you may consult the State Comptroller’s Manual for the Appraisal of Agricultural Land and your appraisal district staff. The manual may be found on the Comptroller’s Web site at www.window.state.tx.us/taxinfo/proptax under the section concerning appraisal manuals.

You must complete this application in full and file it with the chief appraiser before May 1 of the year you are applying for agricultural appraisal. To be accepted, this form must contain information necessary to determine the validity of the claim. If your application is approved, you do not need to file again in later years unless the chief appraiser requests a new application. The chief appraiser may disapprove the application and request additional information. The chief appraiser may deny the application and you may protest that determination to the county appraisal review board in a timely manner. If the chief appraiser requests additional information from an applicant, the information must be furnished within 30 days after the date of the request, or the application is denied. For good cause shown, the chief appraiser may extend the deadline for furnishing the information by written order for a single 15 day period.

You may file a late application up to midnight the day before the appraisal review board approves appraisal records for the year which usually occurs in July. If you file a late application and your application is approved, you must pay a penalty equal to 10 percent of the difference between the amount of tax imposed on the property and the amount that would be imposed if the property were taxed at market value.

OTHER IMPORTANT INFORMATION

If the initial application form does not contain all the information needed to determine whether property qualifies, the chief appraiser may request additional information. The chief appraiser may request only additional information that is necessary to determine whether the land qualifies for

You must notify the chief appraiser in writing if you: stop using your property for agriculture (e.g., you voluntarily decide to stop farming); change the category of your use (e.g., you change from dry cropland to irrigated cropland); change the level of your use (e.g., you substantially increase or decrease the number of cattle you raise); change the nature of your use (e.g., you switch from growing corn to growing ornamental plants); enter, leave or change governmental programs (e.g., you put 100 acres in Conservation Reserve Program); or if you begin using your land for something other than agriculture (e.g., you build a shopping center on most of your land). You must deliver this notice no later than the April 30 following the change in use or eligibility.

PENALTIES

If your land receives agricultural appraisal and you fail to notify the chief appraiser of a change in agricultural use, you may be required to pay a penalty. You will be required to pay a substantial additional tax plus interest (a “rollback” tax) if you stop using all or part of the property for agriculture.

STEP 1: State the Year for Which You are Seeking Agricultural Use Appraisal

_____________________________________

State the year for which you are seeking agricultural use appraisal

STEP 2: Provide Name and Mailing Address of Property Owner

___________________________________________________________________________________________________

Name of Property Owner

___________________________________________________________________________________________________

Mailing Address

_____________________________________________________________________ |

____________________________ |

City, State, ZIP Code |

Phone (area code and number) |

The Property Tax Assistance Division at the Texas Comptroller of Public Accounts provides property tax |

For more information, visit our website: |

information and resources for taxpayers, local taxing entities, appraisal districts and appraisal review boards. |

www.window.state.tx.us/taxinfo/proptax |

P r o p e r t y T a x |

A p p l i c a t i o n f o r 1 - d - 1 ( O p e n - S p a c e ) A g r i c u l t u r a l U s e A p p r a i s a l |

Form |

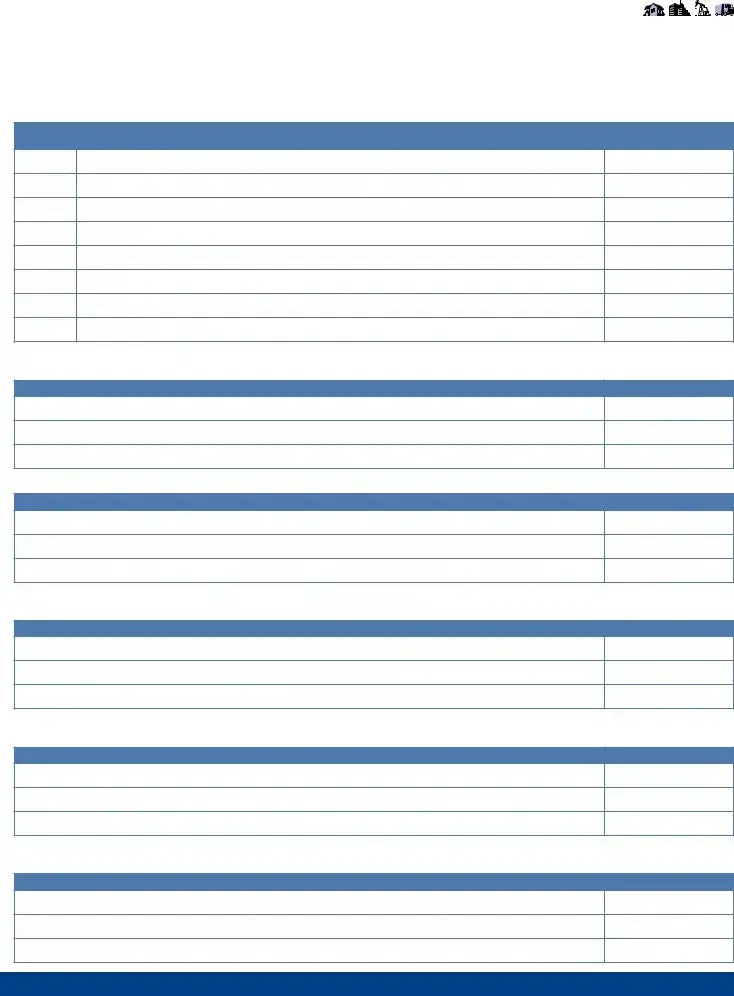

STEP 3: Describe the Property for Which you are Seeking Agricultural Use Appraisal

Give legal description, abstract numbers, field numbers or plat numbers. You may attach last year’s tax statement, notice of appraised value or other corre- spondence identifying the property, rather than completing this section.

________________________________ |

___________________________ |

|

|

|

Appraisal District Account Number (if known) |

Number of Acres for Which Application is Made |

|

|

|

|

|

|

|

|

|

|

|

|

|

Please check the appropriate box for “Yes” or “No” |

|

|

|

|

1. |

Has the ownership of the property changed since January 1 of last year or since the last application was submitted? . . . . |

Yes |

No |

|

|

If yes, the new owner must complete all applicable questions, including Step 4 and Step 5, if the land is |

|

|

|

|

used to manage wildlife. |

|

|

|

2. |

Last year, were you allowed |

Yes |

No |

|

|

If no, you must complete all applicable questions, including Step 4 and Step 5, if the land is used to manage wildlife. |

|

|

|

|

If yes, you need only complete those parts of Steps 4 and 5 that have changed since your earlier application or any |

|

|

|

|

information in Steps 4 and 5 requested by the chief appraiser. |

|

|

|

3. |

Is this property located within the corporate limits of a city or town? . . . . . . . . . . . . . . . . . 對 |

Yes |

No |

|

STEP 4: Describe the Property’s Use

Agricultural use includes, but is not limited to, the following activities: (1) cultivating the soil; (2) producing crops for human food, animal feed, or planting seed or for the production of fibers; (3) floriculture, viticulture and horticulture; (4) raising or keeping livestock; (5) raising or keeping exotic animals or fowl for the production of human food or fiber, leather, pelts or other tangible products having a commercial value; (6) planting cover crops or leaving land idle for the purpose of participating in a governmental program provided the land is not used for residential purposes or a purpose inconsistent with agricultural use or leaving the land idle in conjunction with normal crop or livestock rotation procedures; (7) wildlife management; and (8) beekeeping.

Wildlife management is defined as actively using land that at the time the

for human use, including food, medicine, or recreation, in at least three of the following ways: (1) habitat control; (2) erosion control; (3) predator control;

(4)providing supplemental supplies of water; (5) providing supplement supplies of food; (6) providing shelters; and (7) making census counts to determine population.

Wildlife management is also actively using land to protect federally listed endangered species under a federal permit if the land is included in a habitat preserve subject to a conservation easement created under Chapter 183 Natural Resources Code or part of a conservation development under a federally approved habitat conservation plan restricting the use of the land to protect federally listed endangered species or actively using land for a conservation or restoration project under certain federal and state statutes is wildlife management. These two types of wildlife management uses do not require showing a history of agricultural use but do require evidence identified in Step 4, Questions 4 and 5.

Agricultural land use categories include: (1) irrigated cropland, (2) dry cropland, (3) improved pastureland, (4) native pastureland, (5) orchard, (6) wasteland,

(7) timber production, (8) wildlife management, and (9) other categories of land that are typical in your area.

For more information, visit our website: www.window.state.tx.us/taxinfo/proptax

Page 2 •

A p p l i c a t i o n f o r 1 - d - 1 ( O p e n - S p a c e ) A g r i c u l t u r a l U s e A p p r a i s a l |

P r o p e r t y T a x |

Form |

Please answer the following questions fully. You may list the agricultural use of your property according to the agricultural land categories listed in the preceding paragraph. You may divide the total acreage according to individual uses to which the land is principally devoted.

1.Describe the current and past agricultural uses of this property as described above, starting with the current year and working back 5 years or until you have shown 5 out of 7 years of agricultural use.

Year

Current

1

2

3

4

5

6

7

Agricultural Use Category of Land (list all that apply)

Acres Principally Devoted

to Agricultural Use

2.(a) If you raise livestock, exotic animals, exotic fowl or manage wildlife on the property, list the livestock or exotics raised or the type of wildlife managed and the number of acres used for this activity. You may attach a list if the space is not sufficient.

Livestock/Exotics/Wildlife

Number of Acres

(b) If you raise livestock or exotic animals, how many head (average per year) do you raise?

Livestock/Exotics

Number of Head

3.If you grow crops (including ornamental plants, flowers or grapevines), list the crops grown and the number of acres devoted to each crop. You may attach a list if the space is not sufficient.

Type of Crop

Number of Acres

4.If you have planted cover crops or your land is lying idle because you are participating in a governmental program, please list these programs and the number of acres devoted to each program. You may attach a list if the space is not sufficient.

Program Name

Number of Acres

5.Is this property now used for any

Number of Acres

For more information, visit our website: www.window.state.tx.us/taxinfo/proptax

P r o p e r t y T a x |

A p p l i c a t i o n f o r 1 - d - 1 ( O p e n - S p a c e ) A g r i c u l t u r a l U s e A p p r a i s a l |

Form |

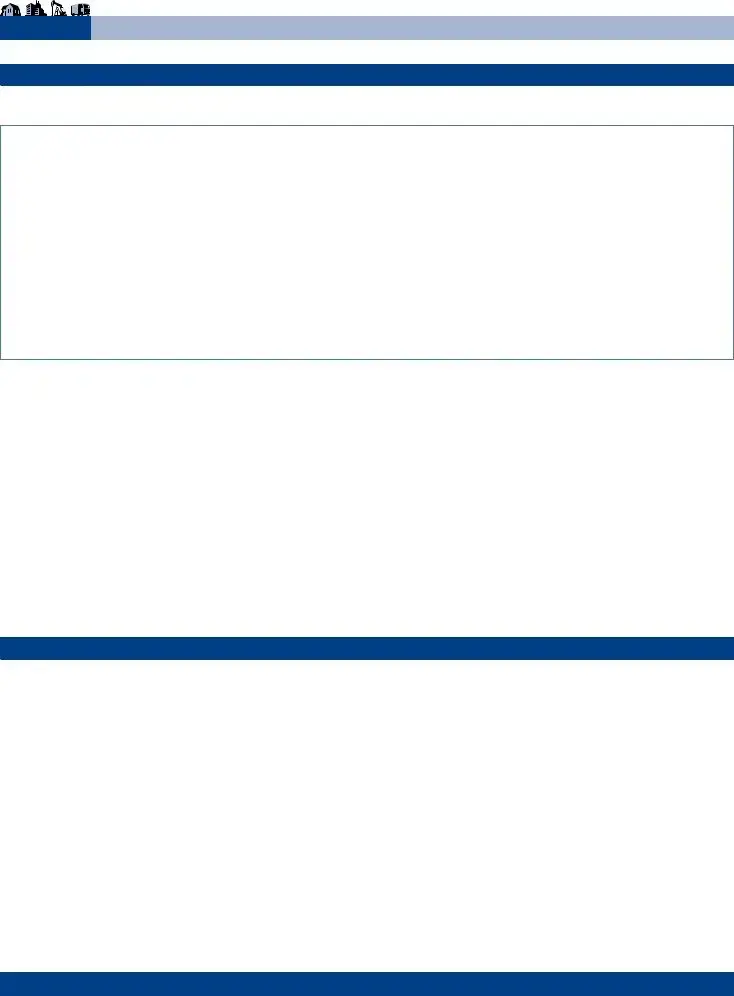

STEP 5: Describe Wildlife Management Use

Do not complete this step if you are not using the land to manage wildlife as permitted by law.

If you are using the land to manage wildlife, list at least three of the wildlife management practices listed in the description found in Step 4 above in which you manage wildlife.

A.__________________________________________________________________________________________________

B.__________________________________________________________________________________________________

C.__________________________________________________________________________________________________

Please indicate the property’s agricultural land use category, as described in Step 4, for the tax year preceding the land’s conversion to wildlife management use. An example is that the land was categorized as native pasture before conversion to wildlife management. It is necessary that the category of use prior to conversion be identified in response to this request.

___________________________________________________________________________________________________

Please attach a wildlife management plan completed on a form prescribed by the Texas Parks and Wildlife Department for the property described in Step 3. A form may be obtained at http://www.tpwd.state.tx.us/landwater/land/private/agricultural_land/.

1. (a) |

Was the land subject to wildlife management a part of a larger tract of land qualified for |

|||||

|

appraisal on January 1 of the previous year? |

. . . . . . . . . . . . . |

. . |

. |

. |

對 |

(b) |

Is the current ownership of the land subject to wildlife management different from the ownership on January 1 |

|||||

|

of the previous year? |

. . . . . . . 對 |

. . |

. |

. |

. . . . . . . . . 對 . . . . |

2.Is any part of the land subject to wildlife management managed through a wildlife management property association? . . .

If yes, please attach a written agreement obligating the owners in the association to perform wildlife management practices necessary to qualify wildlife management land for

Yes No

Yes No

Yes No

3. Is any part of the land that is the subject of this application located in an area designated by the Texas Parks and Wildlife Department as a habitat for an endangered species, a threatened species, or a candidate species for

listing by Texas Parks and Wildlife Department as threatened or endangered? . . . . . . . . . . . . . . . . . 對 . .

4. Is the land that is the subject of this application subject to a permit issued under Section 7 or 10(a) of the

Federal Endangered Species Act? . . . . . . . . . . . . . . . . . 對 . . . . . . . . . . . . . . . . . . 對 .

If yes, is the land included in a habitat preserve and subject to a conservation easement created under Chapter 183, Texas Natural Resources Code or part of a conservation development under a federally

approved habitat conservation plan? . . . . . . . . . . . . . . . . . 對 . . . . . . . . . . . . . . . . . .

If you answer yes to Questions 4(a) and (b), provide evidence of the permit and of the conservation easement or habitat conservation plan. Your application cannot be approved without this evidence.

5.Is the land that is the subject of this application actively used for a conservation or restoration project providing compensation for natural resources damage under one or more of the following laws:

Comprehensive Environmental Response, Compensation, and Liability Act (42 U.S.C. Section 9601 et seq.) . . . . . . .

Oil Pollution Act (33 U.S.C. Section 2701 et seq.) |

. . |

. . |

對 |

Federal Water Pollution Control Act (33 U.S.C. Section 1251 et seq.) |

. . |

. . . |

. . . . . . . 對 |

Chapter 40, Texas Natural Resources Code |

. . |

對 |

|

If yes to any of the above, provide evidence of the conservation easement, deed restriction, or settlement agreement with the Texas Commission on Environmental Quality. Your application cannot be approved without this evidence.

Yes No

Yes No

Yes No

Yes No

Yes No

Yes No

Yes No

For more information, visit our website: www.window.state.tx.us/taxinfo/proptax

Page 4 •

|

A p p l i c a t i o n f o r 1 - d - 1 ( O p e n - S p a c e ) A g r i c u l t u r a l U s e A p p r a i s a l |

|

P r o p e r t y T a x |

|

|

|

Form |

||

|

|

|

|

|

STEP 6: Conversion to Timber Production |

|

|

|

|

1. |

Did you convert the land subject to this application to timber production after September 1, 1997? |

Yes |

No |

|

|

If yes, on what date did you convert to timber production? _____________________________ |

|

|

|

2. |

Do you wish to have the land subject to this application continue to be appraised as |

Yes |

No |

|

|

If yes, complete Question 1 in Step 4 and all other questions in that step that describe the previous agricultural use of this land. |

|

|

|

STEP 7: Read, Sign, and Date

By signing this application, you certify that the information provided in this application is true and correct to the best of your knowledge and belief.

|

|

________________________________________________________________ |

________________________________ |

|

|||

|

|

Authorized Signature |

Title |

________________________________________________________________ |

________________________________ |

||

Printed Name |

Date |

||

If you make a false statement on this application, you could be found guilty of a Class A misdemeanor or a state jail felony under Section 37.10, Penal Code.

For more information, visit our website: www.window.state.tx.us/taxinfo/proptax

Form Characteristics

| Fact Name | Details |

|---|---|

| Governing Laws | The 1-d-1 Open Space Agricultural Valuation form is governed by Article VIII, Section 1-d-1 of the Texas Constitution and Chapter 23, Subchapter D of the Texas Property Tax Code. |

| Eligibility Criteria | Land qualifies for 1-d-1 appraisal if used for agriculture for at least five of the preceding seven years and is currently devoted to agricultural use as defined by law. |

| Additional Uses | Land also qualifies if used for protecting federally listed endangered species or for specific conservation projects under federal and state statutes. |

| Valuation Basis | The value of the land is determined by the average annual net income from typical lease arrangements over the preceding five years, reflecting ordinary land management practices. |

| Deadline for Application | Applications must be completed and submitted to the chief appraiser by May 1 of the year for which agricultural appraisal is requested. |

| Penalties for Non-Compliance | Failure to notify the chief appraiser of changes in land use may result in significant back taxes and penalties, often termed rollback taxes. |

| Late Application Acceptance | Late applications can be filed until just before the appraisal review board approves records, typically occurring in July. |

| Approval Process | Once approved, applicants do not need to reapply annually unless requested by the chief appraiser for additional information. |

| Wildlife Management Use | If the land is used for wildlife management, at least three management practices must be identified to qualify under this category. |

Guidelines on Utilizing 1 D 1 Open Space Agricultural Valuation

Completing the 1 D 1 Open Space Agricultural Valuation form requires careful attention to detail and a clear understanding of the requirements for agricultural appraisal in Texas. Following the outlined steps systematically will ensure that your application is filled out correctly and submitted on time.

- State the Year for Which You are Seeking Agricultural Use Appraisal: Enter the specific year you are applying for appraisal.

- Provide Name and Mailing Address of Property Owner: Fill in the name and full mailing address, including city, state, and ZIP code, as well as the phone number of the property owner.

- Describe the Property for Which You are Seeking Agricultural Use Appraisal: Provide legal descriptions, abstract numbers, field numbers, or plat numbers. You may attach last year’s tax statement or other relevant documentation if easier. Include the appraisal district account number (if known) and the total number of acres for which the application is made. Then answer the three follow-up questions about ownership changes, past appraisals, and city limits status.

- Describe the Property’s Use: List current and past agricultural uses over the last five years, breaking down the types of crops, livestock, and any government programs involved. Also, identify any non-agricultural uses and their acreage.

- Describe Wildlife Management Use: If applicable, outline at least three of the wildlife management practices you actively engage in. Mention the property’s land use category prior to conversion to wildlife management and attach a wildlife management plan if one exists.

- Conversion to Timber Production: Indicate whether the property has been converted to timber production after September 1, 1997. If yes, state the conversion date and confirm if you wish to continue appraisal as 1-d-1 land.

- Read, Sign, and Date: The final step involves reading through the application, signing it to certify the information is true, and providing the date of the signature. Provide the name and title of the authorized individual.

Once the application is filled out completely, it should be submitted to the appropriate appraisal district by the May 1 deadline. Be prepared to respond to any additional information requests from the chief appraiser within the stipulated timeframe to avoid application denial.

What You Should Know About This Form

What is the 1-D-1 Open Space Agricultural Valuation form?

The 1-D-1 Open Space Agricultural Valuation form is an application that allows landowners in Texas to apply for a special appraisal on their property to receive agricultural property tax rates. This form is intended for properties that have been actively used for agricultural purposes or conservation efforts. It must be submitted to the chief appraiser by May 1 each year to qualify for the reduced tax valuation.

What are the eligibility requirements for 1-D-1 appraisal?

To qualify for 1-D-1 appraisal, the land must meet at least one of the following criteria: It has been used for agricultural purposes for five of the preceding seven years, is actively protecting federally listed endangered species, or is involved in specific conservation projects. Additionally, the agricultural use must align with accepted practices in the local area.

What happens if I do not submit my application by the deadline?

If the application is submitted late, you may still file it up until the appraisal review board approves appraisal records, usually in July. However, a penalty will apply. You will be charged 10% of the difference between the tax at market value and the tax at the agricultural valuation if your application is approved.

Can I use the land for non-agricultural purposes and still qualify for the agricultural appraisal?

Using the land for non-agricultural purposes can disqualify it from receiving the 1-D-1 appraisal. If you stop using any part of your property for agriculture, you are required to notify the chief appraiser by April 30 of the following year. Failure to do so could result in penalties and additional taxes.

How is the value of the land assessed under the 1-D-1 program?

The land value is determined based on the income generated from a standard lease arrangement over the five years prior to the appraisal date. This includes income from agricultural operations, hunting leases, and any additional agricultural activities conducted on the property that adhere to the local industry standards.

What should I do if I receive a request for additional information after submitting my application?

If the chief appraiser requests additional information, it is crucial to provide that information within 30 days. If you are unable to meet this deadline, you may request a one-time extension of 15 days. If you do not respond within the set time, your application may be denied.

What if my land use changes after I’ve applied for the 1-D-1 appraisal?

Any change in land use must be reported to the chief appraiser by April 30 of the following year. Whether you switch from agricultural use to residential or commercial activities, or even change the agricultural practices, notification is essential to ensure compliance with the terms of the 1-D-1 program.

Will I need to reapply for the 1-D-1 appraisal every year?

Once your application is approved, you generally do not need to reapply unless requested by the chief appraiser. Should there be any changes to your land’s use or ownership, however, a new application or update may be necessary to maintain your appraisal status.

Common mistakes

Completing the 1-D-1 Open Space Agricultural Valuation form can be a crucial step for property owners seeking special tax treatment for agricultural land. However, there are common mistakes that applicants often make, which can lead to complications or outright denial of their applications.

First, many people fail to provide comprehensive agricultural use information. The form asks for a detailed account of agricultural activities conducted over the past five years. Neglecting to detail all agricultural uses may cause the chief appraiser to question the validity of the application. Providing clear and consistent data is essential. Applicants should double-check that they've captured all agricultural activities, such as growing crops or raising livestock.

Another frequent mistake is missing the submission deadline. The form must be filed by May 1 of the year the appraisal is sought. Missing this deadline can result in disqualification for that tax year. Some applicants mistakenly believe they can submit forms later, but late applications incur penalties and do not guarantee acceptance. Staying organized and setting reminders can help avoid this pitfall.

Inadequate descriptions of property use also pose a significant issue. The form requires a clear and thorough description of both current and past agricultural uses. If the property is also used for non-agricultural purposes, this must be stated. Omitting this information can lead to complications and potential penalties. Clarity and completeness are vital, as the chief appraiser relies on this information to make informed decisions.

Misunderstanding property ownership changes is another common concern. If ownership has changed since the last application was submitted, the new owner must complete all relevant sections of the form. Some applicants mistakenly skip this requirement, thinking it's not necessary if they filled it out in prior years. However, every change in ownership or use needs to be clearly stated to avoid automatic disqualification.

Additionally, many individuals overlook the importance of properly documenting wildlife management practices. For those who manage wildlife, it’s required to list specific practices being implemented. Inadequate documentation can result in the loss of eligibility for wildlife management appraisal. Clear evidence supporting the management practices must be included for the application to be fully considered.

Lastly, many applicants fail to understand the implications of changes in land use. If land changes from agricultural use to another purpose or retains dual use, this must be reported in writing to the chief appraiser no later than April 30 of the year following the change. Ignoring this obligation can lead to significant penalties, including rollback taxes. Understanding these requirements can prevent costly mistakes and keep property owners compliant.

Documents used along the form

The 1 D 1 Open Space Agricultural Valuation form is essential for landowners seeking special appraisal for their agricultural properties under Texas law. Alongside this form, several other documents play a crucial role in the application process. Here’s a list of those commonly used documents, each accompanied by a brief description.

- Ownership Documentation: This includes records such as a deed or title that verify the applicant's ownership of the property. It is critical to confirm legal ownership before proceeding with the application.

- Prior Year’s Tax Statement: A copy of the previous year’s tax statement helps identify the property and its valuation. This documentation can simplify the application process by confirming past agricultural use.

- Legal Description of Property: This document includes details like abstract numbers and field numbers. A precise legal description is necessary to accurately assess the land being claimed for agricultural valuation.

- Wildlife Management Plan: If the land includes wildlife management practices, an approved plan from the Texas Parks and Wildlife Department must accompany the application. This plan outlines how the property will be managed for wildlife purposes.

- State Comptroller’s Manual: Although not a submission document, referencing this manual is useful for understanding guidelines and calculations involved in agricultural valuation. It serves as a comprehensive resource.

- Conservation Easement Documents: When applicable, these documents detail any restrictions on the property related to conservation efforts, which could impact its agricultural status.

- Change of Use Notification: This is a written notice to the chief appraiser if there’s a change in the agricultural use of the property. Timely notification helps avoid penalties or tax implications.

- Application for Agricultural Use Appraisal: In cases of late submissions, this additional application form is necessary to establish eligibility for agricultural appraisal after the standard deadline.

- Agreement for Wildlife Management Property Associations: If the property is part of an association for wildlife management practices, an agreement outlining the responsibilities of the property owners is required for qualification.

Understanding and gathering these documents enhances the chances of a successful application for agricultural valuation. Each piece of information is significant in establishing eligibility under the law. Ensure all forms are correctly filled out and submitted on time to avoid delays or denials.

Similar forms

The 1 D 1 Open Space Agricultural Valuation form is crucial for property owners seeking agricultural appraisal benefits. It shares similarities with several other documents that also relate to property usage and valuation. Here are four such forms that resemble the 1 D 1 form:

- Form 50-129-A (Application for 1-d-1 Open-Space Agricultural Use Appraisal for Wildlife Management): Like the 1 D 1 form, this application focuses on property that is used for agricultural purposes or wildlife management. It requires documentation of use and compliance with state regulations, maintaining an emphasis on the agricultural intent of the land.

- Form 50-144 (Application for Agricultural and Timber Appraisal): This form shares the objective of determining appropriate appraisals for agricultural land. It requires property owners to verify the land's usage for agriculture or timber production, paralleling the conditions outlined in the 1 D 1 application.

- Form 50-157 (Application for Special Valuation for Open-Space Land): This document is similar in that it also assesses land designated for agricultural or open-space use but may focus on different aspects of valuation. Both forms require evidence of land use over a specified period and detail the agricultural practices involved.

- Form 50-166 (Affidavit of Ownership for the Property Tax Exemption): While this affidavit primarily serves to confirm ownership for property tax exemption eligibility, it often accompanies applications like the 1 D 1. It requires details that affirm the property meets necessary qualifications for special appraisal based on its usage.

Understanding these forms can help property owners navigate the complexities of property valuation and ensure they are benefiting from available agricultural use appraisals.

Dos and Don'ts

Your application for the 1-d-1 Open Space Agricultural Valuation form plays a crucial role in determining your property’s eligibility for agricultural appraisal. Here are five important dos and don’ts to keep in mind while filling out the application:

- Do fill out the application completely. Incomplete applications may be disqualified.

- Do ensure that your information is accurate and current, especially concerning property ownership and agricultural use.

- Do submit your application by the deadline of May 1 to avoid penalties.

- Do keep records of your agricultural activities for at least five years, as past use must be demonstrated.

- Do communicate in writing any changes in land use to the chief appraiser before April 30 of the following year.

- Don’t leave any sections blank; every part of the application includes vital information.

- Don’t ignore the request for additional information from the chief appraiser, as failing to respond may lead to denial of your application.

- Don’t forget to attach supplementary documents, such as last year’s tax statement if applicable.

- Don’t delay in notifying the chief appraiser if your property stops being used for agricultural purposes

- Don’t assume that prior approvals mean you don’t have to file again; always check if updates are needed.

Misconceptions

Below are common misconceptions about the 1-d-1 Open Space Agricultural Valuation form, along with explanations for each.

- Misconception 1: Only large farms can qualify for the 1-d-1 appraisal.

- Misconception 2: Once approved, the 1-d-1 designation is permanent.

- Misconception 3: The form does not need to be filed every year.

- Misconception 4: The 1-d-1 appraisal is based solely on property size.

This is not true. Any land that has been used for agriculture for five of the preceding seven years may qualify, regardless of the farm's size. Small plots dedicated to agricultural activities can also benefit from this appraisal.

Approval is not indefinite. If land use changes or if the applicant fails to notify the chief appraiser of such changes, the appraisal may be revoked. Regular updates and notifications are essential to maintain the status.

While it is true that applicants may not need to refile in subsequent years, they must submit a new application if requested by the chief appraiser. Additionally, any changes that affect the agricultural use must be reported.

This is incorrect. The appraisal value is actually based on annual net income from typical lease arrangements during the preceding five years. Other factors, including the intensity of agricultural use, also play a role in determining value.

Key takeaways

Complete the 1-d-1 Open Space Agricultural Valuation form entirely before submitting it to the chief appraiser. Ensure that all required information is included to determine eligibility.

The land must be specifically used for agricultural purposes for at least five out of the past seven years. Acceptable uses include crop production, livestock raising, and wildlife management.

Provide accurate details about the property, including its legal description, acreage, and past agricultural activities. Attach any previous tax statements if necessary to clarify your claims.

Submit the application by May 1 of the year you seek appraisal. If the application is late, a penalty may apply, so file as early as possible.

If there's a change in the agricultural use of the property, notify the chief appraiser in writing by April 30 of the following year. This includes stopping agricultural use or switching to non-agricultural activities.

Be aware that if the land's use changes without notifying the chief appraiser, you may face a rollback tax, which can be substantial.

If approved for agricultural appraisal, you do not need to reapply annually unless requested by the chief appraiser. Keep records and documentation ready in case of future audits.

Browse Other Templates

Sales Tax Exemption Form,Resale Exemption Certificate,Multistate Resale Certificate,California Tax Exemption Document,Wholesale Purchase Certificate,Retail Sales Certificate,Sales Tax Resale Affidavit,Tax Exempt Purchase Authorization,Sales Tax Compl - The certificate can be revoked at any time by the buyer through written notice.

Injury/Incident Report Form Daycare - Learn from past incidents to avoid future occurrences.