Fill Out Your 203 Form

Form 203 serves as a critical document in the establishment of a professional corporation. It functions as the Certificate of Formation for entities seeking to provide professional services, which legally require a specific license. This form is designed to adhere to minimum filing requirements set forth by the Texas Business Organizations Code. It addresses various aspects that are essential for compliance, such as entity name requirements, the designation of a registered agent, and the identification of directors. Specifically, Article 1 mandates that the chosen name must reflect the nature of the professional service being offered and must not be misleading or similar to any existing entities. The registered agent, detailed in Article 2, plays a significant role in receiving official documents on behalf of the corporation, and their consent is necessary for this appointment. Furthermore, Article 3 specifies that directors must be licensed professionals in the same field as the corporation's purpose. The form also touches upon matters of ownership structure, taxation, and filing processes, ensuring that all participants in the professional corporation meet requisite legal standards. By following the instructions provided, individuals can navigate the complexities of formation and set a solid foundation for their professional practice.

203 Example

Form

(Certificate of Formation – Professional Corporation)

The attached form is drafted to meet minimal statutory filing requirements pursuant to the relevant code provisions. This form and the information provided are not substitutes for the advice and services of an attorney and tax specialist.

Commentary

A professional corporation is a corporation that is formed for the purpose of providing a professional service that by law a

Title 7, chapter 301 establishes certain restrictions and requirements regarding ownership and management of a professional corporation. Only a professional individual licensed to practice the same professional service as the professional corporation may be a governing person or managerial official of a professional corporation. Also note that a professional corporation cannot be formed for the practice of medicine (BOC § 301.003(3)). If the purpose of the entity is to provide medical services, the professional may form either a professional association or a professional limited liability company.

Taxes: Professional corporations are subject to a state franchise tax. Contact the Texas Comptroller of Public Accounts, Tax Assistance Section, Austin, Texas,

Instructions for Form

Article

The administrative rules adopted for determining entity name availability (Texas Administrative Code, title 1, part 4, chapter 79, subchapter C) may be viewed at www.sos.state.tx.us/tac/index.shtml. If you wish the secretary of state to provide a preliminary determination on name availability, you may call (512)

Form 203 |

Instruction Page 1 – Do not submit with filing. |

will not be filed. A final determination cannot be made until the document is received and processed by the secretary of state. Do not make financial expenditures or execute documents based on a preliminary clearance. Also note that the preclearance of a name or the issuance of a certificate of formation under a name does not authorize the use of a name in violation of another person’s rights to the name.

Pursuant to section 5.060 of the BOC, the name of a professional entity must not be contrary to a statute or regulation that governs a person who provides a professional service through the professional entity, including a rule of professional ethics. Contact the state agency or examining board exercising control over the profession to determine whether the name chosen complies with statutory and regulatory requirements governing the profession.

Article

Consent: A person designated as the registered agent of an entity must have consented, either in a written or electronic form, to serve as the registered agent of the entity. Although consent is required, a copy of the person’s written or electronic consent need not be submitted with the certificate of formation. The liabilities and penalties imposed by sections 4.007 and 4.008 of the BOC apply with respect to a false statement in a filing instrument that names a person as the registered agent of an entity without that person’s consent. (BOC § 5.207)

Office Address Requirements: The registered office address must be located at a street address where service of process may be personally served on the entity’s registered agent during normal business hours. Although the registered office is not required to be the entity’s principal place of business, the registered office may not be solely a mailbox service or telephone answering service (BOC § 5.201).

Article

Set forth the name of the individual in the format specified. Do not use prefixes (e.g., Mr., Mrs., Ms.). Use the suffix box only for titles of lineage (e.g., Jr., Sr., III) and not for other suffixes or titles (e.g., JD, RN, Ph.D.).

Please note that a document on file with the secretary of state is a public record that is subject to public access and disclosure. When providing address information for directors, use a business or post office box address rather than a residence address if privacy concerns are an issue.

Article

Form 203 |

Instruction Page 2 – Do not submit with filing. |

Option

Option

Article

Joint Practice by Certain Professionals: Pursuant to section 301.012 of the BOC, professionals, other than physicians, engaged in related mental health fields such as psychology, clinical social work, licensed professional counseling, and licensed marriage and family therapy may form a professional corporation that is jointly owned by those practitioners to perform professional services that fall within the scope of practice of those practitioners.

The state agencies exercising regulatory control over professions to which the joint practice provisions apply continue to exercise regulatory authority over their respective licenses.

Initial Mailing Address: Effective January 1, 2022, the certificate of formation of a filing entity must provide the initial mailing address for the entity. The initial mailing address is the address that will be used by the Comptroller of Public Accounts for sending tax information and correspondence to the entity. The initial mailing address may be a post office box or street address.

Supplemental Provisions/Information: Additional space has been provided for additional text to an article within this form or to provide for additional articles to contain optional provisions.

Duration: Pursuant to section 3.003 of the BOC, a Texas professional corporation exists perpetually unless provided otherwise in the certificate of formation. If formation of a corporation with a stated period of duration is desired, use the “Supplemental Provisions/Information” section of this form to provide for a limited duration.

Organizer: Only one organizer is required for the formation of a professional corporation. An organizer may be any person having the capacity to contract for the person or for another; that is, a natural person 18 years of age or older, or a corporation or other legal entity. There are no residency requirements for an organizer. The organizer is not required to be licensed to perform the professional service for which the entity is formed.

Effectiveness of Filing: A certificate of formation becomes effective when filed by the secretary of state (option A). However, pursuant to sections 4.052 and 4.053 of the BOC the effectiveness of the instrument may be delayed to a date not more than ninety (90) days from the date the instrument is signed (option B). The effectiveness of the instrument also may be delayed on the occurrence of a future event or fact, other than the passage of time (option C). If option C is selected, you must state

Form 203 |

Instruction Page 3 – Do not submit with filing. |

the manner in which the event or fact will cause the instrument to take effect and the date of the 90th day after the date the instrument is signed. In order for the certificate to take effect under option C, the entity must, within ninety (90) days of the filing of the certificate, file with the secretary of state a statement regarding the event or fact pursuant to section 4.055 of the BOC.

On the filing of a document with a delayed effective date or condition, the computer records of the secretary of state will be changed to show the filing of the document, the date of the filing, and the future date on which the document will be effective or evidence that the effectiveness was conditioned on the occurrence of a future event or fact. In addition, at the time of such filing, the status of the entity will be shown as “in existence” on the records of the secretary of state.

Execution: The organizer must sign the certificate of formation, but it does not need to be notarized. However, before signing, please read the statements on this form carefully. The designation or appointment of a person as registered agent by an organizer is an affirmation that the person named in the certificate of formation has consented to serve in that capacity. (BOC § 5.2011)

A person commits an offense under section 4.008 of the BOC if the person signs or directs the filing of a filing instrument the person knows is materially false with the intent that the instrument be delivered to the secretary of state for filing. The offense is a Class A misdemeanor unless the person’s intent is to harm or defraud another, in which case the offense is a state jail felony.

Payment and Delivery Instructions: The filing fee for a certificate of formation for a professional corporation is $300. Fees may be paid by personal checks, money orders, LegalEase debit cards, or American Express, Discover, MasterCard, and Visa credit cards. Checks or money orders must be payable through a U.S. bank or financial institution and made payable to the secretary of state. Fees paid by credit card are subject to a statutorily authorized convenience fee of 2.7 percent of the total fees.

Submit the completed form in duplicate along with the filing fee if submitting the document by mail or by courier delivery. The form may be mailed to P.O. Box 13697, Austin, Texas

Need Faster Delivery and Processing? Use our SOSUpload system to electronically submit a PDF copy of the completed and executed document. When submitting a document through SOSUpload, do not include a copy of these instructions, a duplicate copy of the document, payment information, or personal identifying information (PII). Inclusion of this information may lead to a rejection of the document. For more information on SOSUpload, please call (512)

FYI: A corporation is required to maintain a registered agent and a registered office address in Texas. If the registered agent or registered office address changes, it is important to file a statement with the secretary of state to effect a change to the certificate of formation. Failure to maintain a registered agent and registered office may result in the involuntary termination of the corporation. In addition, section 21.802 of the BOC provides a penalty for the failure to timely file a statement of change of registered office or registered agent with the secretary of state. To be timely, the filing must be made by the corporation before the 30th day after the change.

Revised 12/21

Form 203 |

Instruction Page 4 – Do not submit with filing. |

Form 203 |

This space reserved for office use. |

(Revised 12/21) |

|

Submit in duplicate to: |

|

Secretary of State |

|

P.O. Box 13697 |

Certificate of Formation |

Austin, TX |

|

512 |

Professional Corporation |

Filing Fee: $300 |

|

Article 1 – Entity Name and Type

The filing entity being formed is a professional corporation. The name of the entity is:

The name must contain the word “corporation,” “company,” “incorporated,” “limited,” “professional corporation” or an abbreviation of one of these terms.

Article 2 – Registered Agent and Registered Office

(See instructions. Select and complete either A or B and complete C.)

A. The initial registered agent is an organization (cannot be entity named above) by the name of:

OR

B. The initial registered agent is an individual resident of the state whose name is set forth below:

First Name |

M.I. |

Last Name |

Suffix |

C. The business address of the registered agent and the registered office address is:

|

|

TX |

|

Street Address |

City |

State |

Zip Code |

|

Article 3 – Directors |

|

|

|

(A minimum of 1 director is required.) |

|

|

The number of directors constituting the initial board of directors and the names and addresses of the person or persons who are to serve as directors until the first annual meeting of shareholders’ or until their successors are elected and qualified are as follows:

Director 1

First Name |

M.I. |

Last Name |

|

|

Suffix |

|

|

|

|

|

|

Street or Mailing Address |

City |

|

State |

Zip Code |

Country |

Form 203 |

1 |

Director 2

First Name |

M.I. |

Last Name |

|

|

Suffix |

Street or Mailing Address |

City |

|

State |

Zip Code |

Country |

Director 3 |

|

|

|

|

|

First Name |

M.I. |

Last Name |

|

|

Suffix |

Street or Mailing Address |

City |

|

State |

Zip Code |

Country |

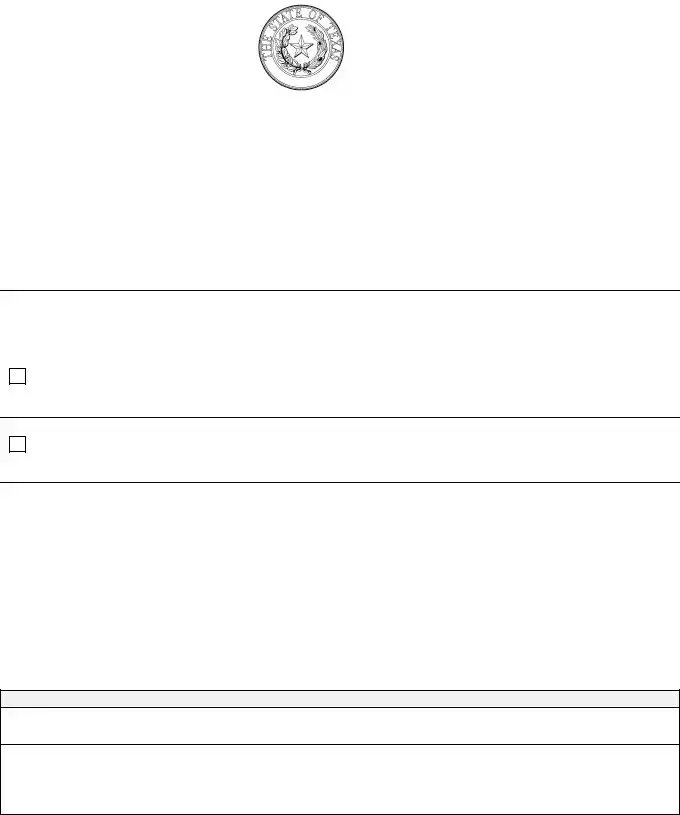

Article 4 – Authorized Shares

(Provide the number of shares in the space below, then select option A or option B, do not select both.)

The total number of shares the corporation is authorized to issue is

A. The par value of each of the authorized shares is

OR

B. The shares shall have no par value

If the shares are to be divided into classes, you must set forth the designation of each class, the number of shares of each class, the par value (or statement of no par value), and the preferences, limitations, and relative rights of each class in the space provided for supplemental information on this form.

Article 5 – Purpose

(Certain restrictions and limitations apply. See instructions.)

The type of professional service to be provided by the professional entity is:

Initial Mailing Address

(Provide the mailing address to which state franchise tax correspondence should be sent.)

Mailing Address |

City |

State |

Zip Code Country |

Supplemental Provisions/Information

Text Area: [The attached addendum, if any, is incorporated herein by reference.]

Form 203 |

2 |

Organizer

The name and address of the organizer:

Name

Street or Mailing Address |

City |

State |

Zip Code |

Effectiveness of Filing (Select either A, B, or C.)

A.

This document becomes effective when the document is filed by the secretary of state.

This document becomes effective when the document is filed by the secretary of state.

B.  This document becomes effective at a later date, which is not more than ninety (90) days from the date of signing. The delayed effective date is:

This document becomes effective at a later date, which is not more than ninety (90) days from the date of signing. The delayed effective date is:

C.  This document takes effect upon the occurrence of a future event or fact, other than the passage of time. The 90th day after the date of signing is:

This document takes effect upon the occurrence of a future event or fact, other than the passage of time. The 90th day after the date of signing is:

The following event or fact will cause the document to take effect in the manner described below:

Execution

The undersigned affirms that the person designated as registered agent has consented to the appointment. The undersigned also affirms that, to the best knowledge of the undersigned, the name provided as the name of the filing entity does not falsely imply an affiliation with a governmental entity. The undersigned signs this document subject to the penalties imposed by law for the submission of a materially false or fraudulent instrument and certifies under penalty of perjury that the undersigned is authorized to execute the filing instrument.

Date:

Signature of organizer

Printed or typed name of organizer

Reset

Form 203 |

3 |

Form Characteristics

| Fact Name | Description |

|---|---|

| Form Purpose | Form 203 is a Certificate of Formation for a Professional Corporation in Texas, designed to fulfill statutory filing requirements. |

| Governing Laws | The formation of a professional corporation is governed by the Texas Business Organizations Code, specifically Title 1, Chapters 20 and 21, and Title 7, Chapters 301 and 303. |

| Professional Services | A professional corporation can only be formed to provide services that require a state license, such as law, accounting, or engineering. |

| Restrictions | Medical services cannot be provided through a professional corporation, which must be organized as a professional association or limited liability company instead. |

| Director Requirements | At least one director is required, and the director must be a licensed professional in the field the corporation is providing services for. |

| Registered Agent | The registered agent can be a domestic or foreign entity, or an individual resident of Texas, and must consent to serve in that capacity. |

| Filing Fee | A fee of $300 is required to submit Form 203. Various payment methods are accepted, including personal checks and credit cards. |

Guidelines on Utilizing 203

Completing Form 203 is a crucial step in establishing a professional corporation. Each section of the form requires attention to detail to ensure compliance with state laws. Below are the steps to properly fill out the form.

- Article 1 – Entity Name and Type: Write a name for the corporation, including “Corporation,” “Company,” “Incorporated,” “Limited,” or “Professional Corporation.” Ensure it is distinguishable from existing entities and does not imply unauthorized affiliations.

- Article 2 – Registered Agent and Registered Office: Choose either an organization or an individual as the registered agent. If selecting an organization, do not use the entity’s name. Then provide the registered office address, which must be a physical location in Texas, not a mailbox service.

- Article 3 – Directors: Indicate the number of directors and list at least one individual. The director must be a natural person and licensed to provide the same service as the corporation. Use their full name and address, avoiding prefixes.

- Article 4 – Authorized Shares: Select whether shares will have par value or no par value. If choosing par value, provide the amount. If opting for no par value, you may issue shares for a price determined by the board.

- Article 5 – Purpose: Clearly state the type of professional service the corporation will provide. The entity may only engage in one type of professional service unless otherwise authorized under state law.

- Initial Mailing Address: Provide an address where the Texas Comptroller will send all tax-related correspondence. This can be a street address or a P.O. Box.

- Supplemental Provisions/Information: Use this section for any additional information. You can include a limited duration for the corporation if desired.

- Organizer: Include the name of at least one organizer. The organizer does not need to be licensed in the professional service but must be at least 18 years old.

- Effectiveness of Filing: Decide if the certificate will take effect immediately or if there needs to be a delay, and specify the conditions if applicable.

- Execution: The organizer must sign the certificate of formation. Ensure that the signer understands the responsibilities associated with being the registered agent.

- Payment: Submit the filing fee of $300 via acceptable payment methods. Make sure to send the completed form in duplicate, either by mail or in person.

Each step must be followed accurately to ensure the form is processed without delays. After submission, you will receive confirmation and a copy for your records. It's important to maintain compliance and keep the registered agent and address updated to avoid penalties.

What You Should Know About This Form

What is Form 203?

Form 203 is the Certificate of Formation for a Professional Corporation in Texas. This form is essential for individuals looking to establish a corporation that provides professional services, which require a state license. The document outlines the company’s name, structure, registered agent, directors, and other key details necessary for formation. It meets the minimum statutory requirements set forth by the Texas Business Organizations Code.

Who can form a professional corporation using Form 203?

Only individuals licensed to practice the same professional service can form a professional corporation using Form 203. This means that if you are a licensed professional, such as an attorney, accountant, or architect, you may establish a professional corporation dedicated to your field. However, it is important to note that professional corporations cannot be formed for the practice of medicine in Texas, which requires forming either a professional association or a professional limited liability company instead.

What information is required on Form 203?

Form 203 requires several pieces of information, including the entity name, registered agent, registered office address, names of directors, authorized shares, and the purpose of the corporation. The entity name must comply with specific guidelines to ensure it is distinguishable from existing corporations. Additionally, you will need to provide the details of one or more directors who are licensed professionals. Clarity about the professional service being offered and compliance with all applicable regulations is also necessary.

What are the filing and fee requirements for Form 203?

The filing fee for Form 203 is $300. This fee can be paid via personal checks, money orders, or credit cards. When submitting the form, you must include it in duplicate for processing. You can mail your completed form to the Texas Secretary of State or use electronic submission through the SOSUpload system for faster processing. It's essential to follow all submission guidelines to avoid rejection of your filing.

What happens after Form 203 is filed?

Once Form 203 is filed with the Texas Secretary of State, it becomes effective immediately unless a delayed effective date is specified. The secretary's office will provide you with evidence of filing, including a file-stamped copy of the document, which serves as proof that the corporation has been formed. It is crucial to maintain ongoing compliance, such as having a registered agent and updating the registered office address when necessary, to prevent the involuntary termination of the corporation.

Common mistakes

Filling out Form 203 can be a straightforward process, but many people inadvertently make mistakes that can delay or complicate their application. One common error occurs in the entity name. Applicants often neglect to ensure that the name is distinguishable from existing entities. The chosen name must comply with specific provisions in the Texas Business Organizations Code. If the name does not meet these criteria, it cannot be filed, wasting valuable time and resources.

Another mistake often seen involves the designation of a registered agent. Individuals sometimes mistakenly name the corporation itself as the registered agent, which is prohibited. The law requires that the registered agent be an individual resident of Texas or a registered foreign entity. This misstep can lead to significant delays in processing the certificate of formation.

Many applicants also misinterpret the directors' requirements. A director must be a licensed individual capable of providing the same professional service as that rendered by the corporation. Omitting essential details or using incorrect titles may result in the rejection of the application. Remember to list only the necessary information without prefixes or improper suffixes.

In the section for authorized shares, errors often arise concerning stating par values. Some individuals confuse options A and B, leading them to incorrectly declare $0 par value when shares should indeed have a stated par amount. Such errors can complicate the approval process and require re-filing.

Additionally, applicants frequently miscalculate the purpose of their corporation. The certificate must specify the exact professional service to be provided. If the description is vague or incorrect, or if it encompasses multiple services when only one is allowed, the filing may be rejected outright.

Another common error occurs in providing an initial mailing address. Some individuals fail to recognize that this address is critical for tax correspondence. Without a correct address, important communications may be missed, resulting in compliance issues down the line.

Moreover, many fail to adequately address the execution requirements. Although notarization is not necessary, the organizer must sign the form correctly. If this signature is missing or not executed properly, the entire document could be deemed invalid, necessitating another attempt to file.

Lastly, payment mistakes can hinder the process. Applicants sometimes choose incorrect payment methods or fail to include the total necessary fees. The filing fee for Form 203 is $300, and any oversight here can lead to an incomplete application, resulting in delays.

Documents used along the form

Submitting a Form 203 for a professional corporation is an essential step in establishing your business entity. However, there are various other forms and documents frequently associated with this process to ensure legality and compliance. Below is a list of five commonly used documents that often accompany the 203 form, each serving a distinct purpose.

- Certificate of Authority: This document allows a foreign (out-of-state) professional corporation to operate within Texas. It grants permission to engage in business activities in the state while ensuring compliance with Texas laws.

- Initial Board of Directors Minutes: These minutes document the initial meeting of the board of directors, outlining key decisions such as the adoption of bylaws, appointment of officers, and decisions related to banking authorizations.

- Bylaws: Bylaws serve as the internal governance rules of the corporation. They detail how the corporation will operate, including procedures for meetings, voting rights, and the duties of directors and officers.

- Registered Agent Consent Form: This form is signed by the registered agent, confirming their agreement to act on behalf of the corporation for service of process and official correspondence within Texas.

- Form 05-102 (Texas Franchise Tax Application): This form is required for registering the corporation for state franchise taxes. It informs the Texas Comptroller that the corporation is legally formed and responsible for tax obligations.

Having these documents prepared and filed correctly is vital for the successful formation and operation of a professional corporation in Texas. Each document contributes to establishing a clear structure and ensuring compliance with state regulations, setting a solid foundation for the future of your business.

Similar forms

- Form 201—Certificate of Formation: Similar to Form 203, Form 201 is used to establish a corporation in Texas. It covers the basic information required for filing, including the entity's name and type. However, Form 201 is for general corporations, while Form 203 is specifically for professional corporations.

- Form 202—Certificate of Formation for Limited Liability Company (LLC): This document serves a similar purpose as Form 203, but for LLCs. Both forms require information about the entity’s name, registered agent, and management structure, though Form 202 includes information specific to LLCs.

- Form 205—Application for Certificate of Authority: Like Form 203, Form 205 is necessary for entities seeking to conduct business in Texas. Whereas Form 203 focuses on forming a professional corporation, Form 205 provides the requirements for out-of-state entities to operate legally within Texas.

- Form 214—Certificate of Formation for a Nonprofit Corporation: While both Form 203 and Form 214 list foundational information needed for formation, Form 214 applies to nonprofit organizations. Each form has distinct requirements based on the purpose of the corporation.

- Form 300—Certificate of Formation for Foreign Entities: This form allows foreign entities to register in Texas. Similar to Form 203, it requires basic details about the entity, such as its name and registered agent, but it is tailored to existing entities formed outside Texas.

Dos and Don'ts

When filling out the 203 form, there are important actions to take and common pitfalls to avoid. Consider the following list:

- Do ensure that the entity name complies with state regulations and is distinguishable from existing entities.

- Do include a corporate name and organizational designation that reflects the professional service you are authorized to provide.

- Do specify the registered agent clearly, and remember that either an individual or a registered domestic entity can serve in this role.

- Do confirm that the registered agent has consented to serve in this capacity; this step is essential for compliance.

- Do provide a valid registered office address where official documents can be served during business hours.

- Do include a statement of the professional service to be provided; this must be precise and in line with legal requirements.

- Don’t use your corporate name as the name of the registered agent; each must be distinct.

- Don’t use prefixes or unnecessary suffixes when identifying directors, as this can lead to confusion.

- Don’t disregard the need for effective communication regarding any name availability checks; waiting for a preliminary determination is crucial.

- Don’t forget to include an initial mailing address for tax correspondence; this is now a required part of the filing process.

By following these guidelines, you can help ensure a smoother experience when submitting your 203 form.

Misconceptions

MISCONCEPTION 1: The 203 form can be filed without any legal guidance.

This is incorrect. While the form meets basic statutory requirements, it is crucial to seek advice from an attorney or tax specialist to ensure compliance with all regulations.

MISCONCEPTION 2: Any individual or entity can serve as a registered agent for the corporation.

This is not true. The registered agent must either be a licensed individual resident of Texas or a domestic or foreign entity registered to do business in Texas. The corporation itself cannot serve as its own registered agent.

MISCONCEPTION 3: A professional corporation can offer multiple types of professional services under one formation.

This is misleading. A professional entity is generally restricted to providing only one type of professional service unless specifically authorized otherwise under state law.

MISCONCEPTION 4: The filing fee is optional and can be waived.

This is incorrect. The filing fee of $300 is mandatory for submitting the certificate of formation. Payment must be made through accepted methods without exception.

MISCONCEPTION 5: Once the 203 form is filed, the corporation’s status is permanent.

This is not the case. A professional corporation must maintain a registered agent and address in Texas. If these change without notification to the secretary of state, the corporation may be involuntarily terminated.

MISCONCEPTION 6: The name of the professional corporation is automatically approved upon submission.

This is incorrect. The name must comply with specific state regulations. If it does not meet the required standards for availability, the form cannot be filed until the name is acceptable.

Key takeaways

1. Understanding the Purpose: Form 203 is used to create a professional corporation in Texas. This type of corporation is for individuals providing licensed professional services, which cannot be offered by other types of business organizations.

2. Entity Name Requirements: When filling out Form 203, the entity name must comply with Texas law. It needs to be unique and should not indicate activities that aren't authorized by law. Failure to meet these naming criteria will result in the inability to file the document.

3. Registered Agent Considerations: The registered agent can be either a Texas resident or a registered entity. This agent must consent to serve in this role, but written consent does not need to be submitted with the filing. The registered office cannot be just a mailbox or answering service.

4. Filing Fees and Payment: The fee for submitting Form 203 is $300. Payment options include checks, money orders, and credit cards. Be aware that credit card payments incur a convenience fee. Timely submission is essential for processing, and one should consider electronic filing for faster results.

Browse Other Templates

Blumberg Lease - It states that any illegal part of the lease does not affect the rest of the document.

Spangler Elementary - Engage children with fun promotional items featuring their favorite candy.