Fill Out Your Addendum To Contract Form

The Addendum To Contract form plays a crucial role in real estate transactions involving FHA and VA financing. This addendum is inseparably linked to the Offer to Purchase and Contract between the seller and the buyer of a property. For those utilizing FHA financing, the form includes the FHA Amendatory Clause, which assures that buyers are not obligated to complete the purchase unless they receive a written statement from the Federal Housing Commissioner or a Direct Endorsement lender, confirming an appraised value that meets or exceeds a specified amount. Buyers can choose to continue the transaction regardless of the appraised value, but they should verify the property’s worth and condition. The VA section of the addendum addresses similar concerns. Buyers are protected from penalties if the contract price exceeds the property's reasonable value as determined by the Department of Veterans Affairs. Here, too, buyers retain the option to proceed, but if they decide to pay more than the authorized value, they must disclose how they will fund the excess. Furthermore, the seller may choose to adjust the sales price if it does not meet the DVA’s valuation. The form emphasizes the importance of inspections that may be required by the DVA and stipulates the responsibility for their costs. In case of conflict between the addendum and the original contract, the addendum takes precedence except in specific scenarios regarding property description or party identities. Ultimately, all parties involved must attest to the accuracy of the provided information, understanding the serious implications of any false statements.

Addendum To Contract Example

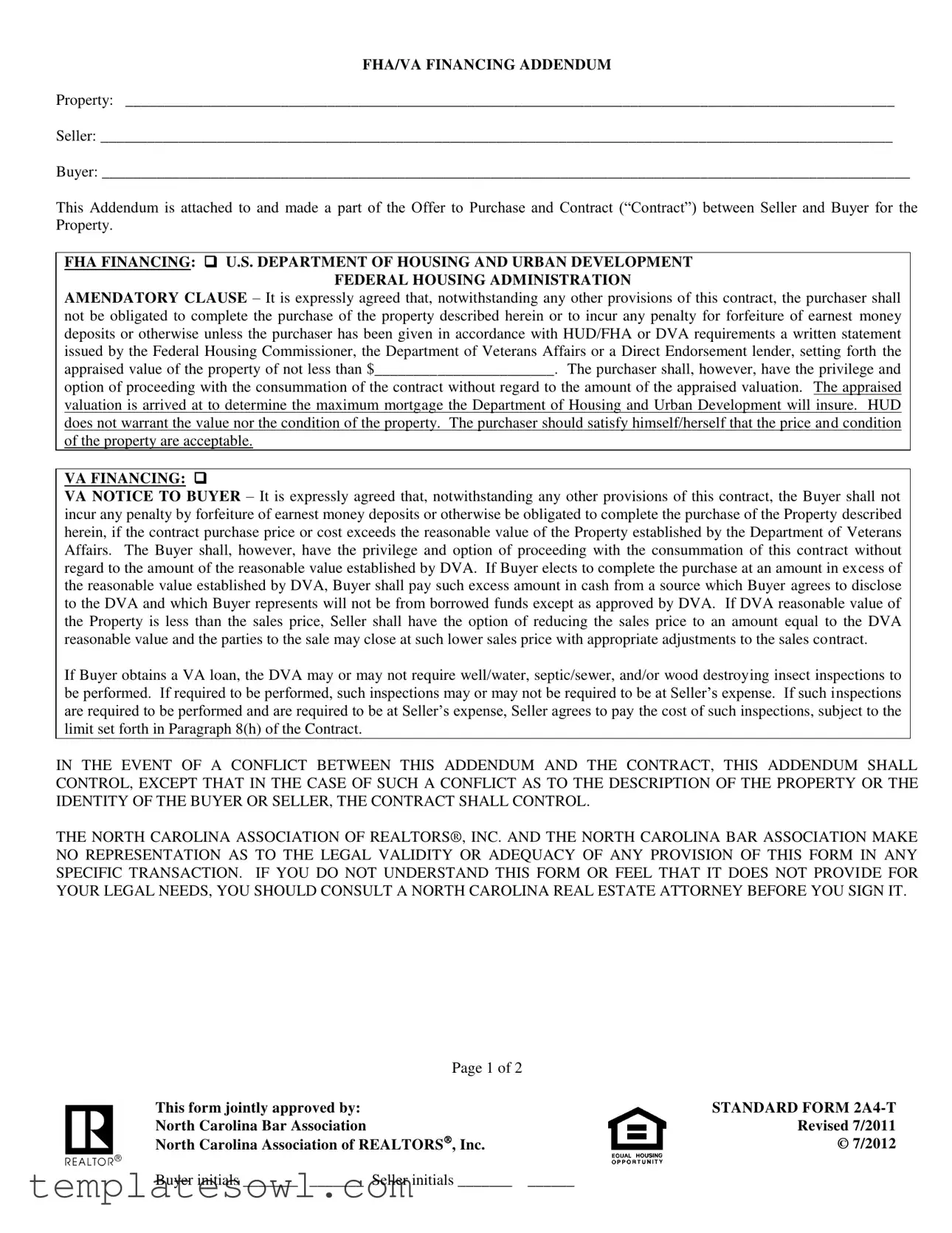

FHA/VA FINANCING ADDENDUM

Property: ___________________________________________________________________________________________________

Seller: ______________________________________________________________________________________________________

Buyer: ________________________________________________________________________________________________________

This Addendum is attached to and made a part of the Offer to Purchase and Contract (“Contract”) between Seller and Buyer for the Property.

FHA FINANCING: U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT

FEDERAL HOUSING ADMINISTRATION

AMENDATORY CLAUSE – It is expressly agreed that, notwithstanding any other provisions of this contract, the purchaser shall not be obligated to complete the purchase of the property described herein or to incur any penalty for forfeiture of earnest money deposits or otherwise unless the purchaser has been given in accordance with HUD/FHA or DVA requirements a written statement issued by the Federal Housing Commissioner, the Department of Veterans Affairs or a Direct Endorsement lender, setting forth the appraised value of the property of not less than $_______________________. The purchaser shall, however, have the privilege and

option of proceeding with the consummation of the contract without regard to the amount of the appraised valuation. The appraised valuation is arrived at to determine the maximum mortgage the Department of Housing and Urban Development will insure. HUD does not warrant the value nor the condition of the property. The purchaser should satisfy himself/herself that the price and condition of the property are acceptable.

VA FINANCING:

VA NOTICE TO BUYER – It is expressly agreed that, notwithstanding any other provisions of this contract, the Buyer shall not incur any penalty by forfeiture of earnest money deposits or otherwise be obligated to complete the purchase of the Property described herein, if the contract purchase price or cost exceeds the reasonable value of the Property established by the Department of Veterans Affairs. The Buyer shall, however, have the privilege and option of proceeding with the consummation of this contract without regard to the amount of the reasonable value established by DVA. If Buyer elects to complete the purchase at an amount in excess of the reasonable value established by DVA, Buyer shall pay such excess amount in cash from a source which Buyer agrees to disclose to the DVA and which Buyer represents will not be from borrowed funds except as approved by DVA. If DVA reasonable value of the Property is less than the sales price, Seller shall have the option of reducing the sales price to an amount equal to the DVA reasonable value and the parties to the sale may close at such lower sales price with appropriate adjustments to the sales contract.

If Buyer obtains a VA loan, the DVA may or may not require well/water, septic/sewer, and/or wood destroying insect inspections to be performed. If required to be performed, such inspections may or may not be required to be at Seller’s expense. If such inspections are required to be performed and are required to be at Seller’s expense, Seller agrees to pay the cost of such inspections, subject to the

limit set forth in Paragraph 8(h) of the Contract.

IN THE EVENT OF A CONFLICT BETWEEN THIS ADDENDUM AND THE CONTRACT, THIS ADDENDUM SHALL CONTROL, EXCEPT THAT IN THE CASE OF SUCH A CONFLICT AS TO THE DESCRIPTION OF THE PROPERTY OR THE IDENTITY OF THE BUYER OR SELLER, THE CONTRACT SHALL CONTROL.

THE NORTH CAROLINA ASSOCIATION OF REALTORS®, INC. AND THE NORTH CAROLINA BAR ASSOCIATION MAKE NO REPRESENTATION AS TO THE LEGAL VALIDITY OR ADEQUACY OF ANY PROVISION OF THIS FORM IN ANY SPECIFIC TRANSACTION. IF YOU DO NOT UNDERSTAND THIS FORM OR FEEL THAT IT DOES NOT PROVIDE FOR YOUR LEGAL NEEDS, YOU SHOULD CONSULT A NORTH CAROLINA REAL ESTATE ATTORNEY BEFORE YOU SIGN IT.

Page 1 of 2 |

|

This form jointly approved by: |

STANDARD FORM |

North Carolina Bar Association |

Revised 7/2011 |

North Carolina Association of REALTORS, Inc. |

© 7/2012 |

Buyer initials _______ _______ Seller initials _______ |

______ |

REAL ESTATE CERTIFICATION – The seller, the purchaser, and the broker hereby certify that the terms of the sales contract are true to the best of their knowledge and belief and it is agreed that any other agreement entered into by any of the parties is fully disclosed and attached to the sales contract. The seller, the purchaser, and the broker fully understand that it is a federal crime punishable by fine or imprisonment or both to knowingly make any false statement concerning any of the above facts as applicable under the provisions of Title 18, United States Code, Sections 1012 and 1014.

I CERTIFY I HAVE READ & UNDERSTAND THE ABOVE STATEMENTS: |

|

BUYER/BORROWER ________________________________________________(SEAL) |

DATE _________________________ |

DATE _________________________ |

|

DATE _________________________ |

|

SELLING FIRM ___________________________________________ BY: _____________________________________________ |

|

SELLER ____________________________________________________________(SEAL) |

DATE _________________________ |

SELLER ____________________________________________________________(SEAL) |

DATE _________________________ |

SELLER ____________________________________________________________(SEAL) |

DATE _________________________ |

LISTING FIRM ___________________________________________ BY: _____________________________________________

THE MORTGAGE LENDER MUST RECEIVE AN ORIGINAL SIGNATURE COPY

Page 2 of 2

STANDARD FORM

Form Characteristics

| Fact Name | Details |

|---|---|

| Purpose of the Addendum | The Addendum To Contract form is used to clarify terms related to FHA and VA financing in real estate transactions. |

| Parties Involved | This form is signed by both the seller and the buyer, making it a mutual agreement between the two parties. |

| FHA Financing Clause | The addendum contains a specific clause that protects buyers from being obligated to complete the purchase if they do not receive an acceptable appraisal from the Federal Housing Administration. |

| VA Financing Clause | Similar to FHA financing, the VA clause provides protections for buyers if the purchase price exceeds the property's reasonable value set by the Department of Veterans Affairs. |

| Appraisal Requirements | For both FHA and VA financing, an appraisal is required to ensure that property values meet the necessary standards for loan approval. |

| Legal Control | In case of any discrepancies, the addendum prevails over the main contract, except for issues related to property description or parties' identities. |

| Seller's Inspection Obligations | If inspections are mandated by the DVA, the seller may be responsible for covering the costs, within limits outlined in the sales contract. |

| Certification Requirement | All parties involved—the seller, buyer, and broker—must certify the truthfulness of the sale contract's terms, acknowledging the consequences of false statements. |

| Governing Laws in North Carolina | The form is governed by North Carolina real estate laws, reinforcing the need for clarity and compliance under state regulations. |

| Consultation Recommendation | The form advises individuals to consult a real estate attorney if they do not understand the document or if it does not meet their legal requirements. |

Guidelines on Utilizing Addendum To Contract

When preparing to fill out the Addendum To Contract form, it's important to ensure that you have all necessary information at hand. This form needs to be filled out carefully and accurately in order to reflect the agreement between the seller and buyer in relation to FHA or VA financing. The following steps outline how to complete the form properly.

- Write the property address in the space provided at the top of the form.

- Enter the names of the seller and buyer in the designated areas.

- Review the FHA Financing section. If applicable, check the box indicating this financing option is chosen.

- In the FHA Financing section, input the appraised value of the property where indicated.

- Review the VA Financing section. If applicable, check the box indicating this financing option is chosen.

- Understand the implications of the paragraphs under both financing options. Ensure you are aware of the conditions and responsibilities stated.

- Both the buyer and seller need to initial beside their names as indicated on the form.

- If there are any additional agreements, they should be disclosed and attached to the contract.

- After reviewing the entire form for accuracy, both parties must sign the appropriate lines, ensuring all signatures are accompanied by the date.

- Make sure the original signed copy is sent to the mortgage lender.

What You Should Know About This Form

What is an Addendum to Contract?

An Addendum to Contract is a document that adds specific provisions or amends certain terms of an existing contract. In the context of real estate transactions, this addendum often outlines financing details, such as FHA or VA loan requirements. It becomes part of the main contract and helps clarify obligations and protections for both the buyer and the seller.

When should I use an Addendum to Contract?

An Addendum is recommended when you need to adjust the terms of an existing real estate contract. For instance, if either party requires specific financing conditions, such as those associated with FHA or VA loans, then an addendum clarifies these terms. Using an addendum ensures that all parties are aware of and agree to the updated conditions.

What is FHA Financing, and why is it included in this addendum?

FHA Financing refers to loans backed by the Federal Housing Administration, designed to help lower-income buyers afford homes. This addendum includes provisions from the FHA that protect buyers by allowing them to back out of a contract if the appraised value of the home is below a specified amount. By incorporating this clause, the addendum ensures that the buyer isn’t obligated to proceed with a purchase that’s potentially overvalued.

What should I know about VA Financing in the Addendum?

VA Financing is available for veterans and active-duty service members, allowing them to purchase homes with favorable loan terms. This addendum specifies that buyers are not penalized for failing to complete a purchase if the property appraises for less than the sales price. It protects buyers from overpaying and gives them options if the appraised value turns out to be lower than expected.

Does the Addendum override the original contract?

In cases where there is a conflict, the addendum will take precedence, except when it comes to the property description or the identities of the buyer and seller. In those instances, the original contract will govern. This ensures clarity and coherence in the documentation of the transaction.

What should I do if I don't understand the Addendum?

If you find yourself uncertain about any aspects of the Addendum or believe it does not fit your legal needs, seeking advice from a real estate attorney is wise. They can provide clarification and help you make informed decisions about proceeding with the contract. This is especially important since misunderstandings can lead to legal issues later on.

Who is responsible for inspection costs mentioned in the Addendum?

The responsibility for paying for inspections can vary. If a VA loan requires certain inspections, the addendum may stipulate that the seller covers these costs. However, this is contingent on the regulations set by the DVA and the specifics outlined in the contract. Clarity on this matter can prevent confusion and disputes later.

What penalties apply for providing false information in this Addendum?

Providing false statements in this document can result in serious legal consequences. Federal law considers knowingly making false statements a crime punishable by fines or imprisonment. All parties involved—buyers, sellers, and brokers—must ensure the accuracy of the information disclosed in the document to avoid severe penalties.

Common mistakes

When filling out the Addendum To Contract form, many individuals unknowingly make mistakes that can complicate their home buying process. Here are seven common pitfalls to avoid.

One frequent error is failing to provide the appraised value of the property in the designated space. This section is crucial because it determines the maximum mortgage the Department of Housing and Urban Development (HUD) will insure. Leaving this blank can create confusion and potentially jeopardize financing options.

Another mistake occurs when buyers or sellers omit their initials on the form. Each party must initial specific sections to confirm their understanding and agreement. Forgetting these initials might lead to disputes later, as one party might claim they were unaware of certain terms.

People also tend to overlook the importance of disclosing all agreements involved in the sale. If there are additional agreements outside the sales contract, failure to attach these documents can create legal issues. Transparency is key; disclosure fosters trust and clarity.

Inadequate knowledge about the implications of VA financing leads to mistakes as well. Many buyers do not realize they have the option to proceed with the sale despite differences between the contract price and the Department of Veterans Affairs (DVA) assessment. It's essential to understand these nuances to avoid unnecessary financial strain or penalties.

Misunderstanding who is responsible for inspections is another common error. Buyers often assume all costs related to inspections fall on the seller. However, it's critical to know that some inspections might be the buyer's responsibility, depending on the terms agreed upon. The details matter in these situations.

The failure to complete the certification section can create serious issues. This section certifies that all information is accurate and full disclosure has been made. Not signing this part undermines the validity of the entire document, inviting potential legal consequences.

Lastly, neglecting to consult a legal advisor when unsure can be a costly oversight. The form includes a clause advising parties to seek legal assistance if they have questions. Not doing so can lead to misunderstandings and possibly compromise the transaction.

By being aware of these common mistakes, parties can navigate the Addendum To Contract form more effectively, ensuring a smoother real estate transaction.

Documents used along the form

The Addendum to Contract form is often accompanied by several other important documents that help clarify and support the terms of the agreement between the buyer and the seller. These documents provide detailed information about financing, rights, and responsibilities that both parties must be aware of during the transaction. Below is a list of key forms you may encounter alongside the Addendum to Contract.

- Purchase Agreement: This foundational document outlines the specific terms and conditions of the sale, including the purchase price, contingencies, and timelines. It serves as the main agreement between the buyer and seller.

- Financing Contingency Addendum: This addendum specifies the buyer’s financing requirements, ensuring that the purchase is contingent upon obtaining a loan. It protects the buyer in case financing falls through.

- Disclosure Documents: These documents inform the buyer about the property's condition, including any known issues or hazards. Common disclosures include lead paint, mold, and radon disclosures.

- Home Inspection Report: Conducted by a qualified inspector, this report details the property's condition. It allows buyers to negotiate repairs or request concessions based on findings.

- Lead-Based Paint Disclosure: Required for homes built before 1978, this document informs buyers about the potential presence of lead-based paint and its risks.

- Appraisal Report: An independent appraiser assesses the property's value, which is crucial for securing financing. This document verifies whether the property's value meets or exceeds the sale price.

- Real Estate Settlement Statement (HUD-1): This document provides a detailed breakdown of all costs associated with the transaction. It is reviewed at closing to ensure both parties understand their financial responsibilities.

Understanding these additional forms and documents helps both buyers and sellers navigate the real estate process more effectively. Being familiar with these papers creates a smoother transition and ensures that all parties are informed of their rights and obligations.

Similar forms

- Addendum to Lease – This document similarly modifies the terms of an existing lease agreement. Like the addendum to a contract, it can clarify responsibilities or adjust conditions while ensuring all parties agree to the changes.

- Contract Modification Agreement – A contract modification agreement serves to alter specific terms within an original contract. Just as the addendum allows amendments without rescinding the entire contract, this document can be used to make necessary adjustments while retaining the core agreement.

- Memorandum of Understanding (MOU) – An MOU outlines the intentions of both parties and is often used in place of a formal contract. It resembles the addendum in that it provides clarity on agreed terms but lacks the legally binding nature typically found in contracts.

- Side Agreement – This is an informal document created alongside a main contract to address additional terms or conditions. Much like an addendum, it supplements the original document without overshadowing its primary provisions.

- Amendment – An amendment is a legal alteration to an existing contract or agreement. Similar to an addendum, it modifies specific clauses, but it may typically require more formal language and signatures for legal effect.

- Waiver – A waiver relinquishes a right or privilege outlined in a contract. This document, akin to an addendum, acknowledges specific conditions have changed, although it is typically more limited in scope than a comprehensive addendum.

- Disclosure Statement – A disclosure statement provides crucial information to one or more parties, much like the addendum ensures all parties have a mutual understanding of modifications. It aims to clarify expectations and responsibilities.

- Seller's Disclosure Form – This form is designed to inform buyers about the condition of a property. While more focused on property details, it works in conjunction with an addendum to reduce misunderstandings before finalizing a sale.

- Termination Agreement – A termination agreement formally dissolves a contract's terms, much like how an addendum can change them. Though the purposes differ, both documents require mutual consent to alter or end commitments.

Dos and Don'ts

When filling out the Addendum To Contract form, certain practices can help ensure the process goes smoothly. Below is a list of important do's and don'ts to consider.

- Do carefully read each section before making any entries.

- Do ensure that all names and property details are filled out accurately.

- Do communicate openly with both the seller and buyer regarding any terms of the addendum.

- Do provide clear written statements regarding appraisals and financing to avoid misunderstandings.

- Do seek clarification from a real estate attorney if any part of the form is confusing.

- Don’t leave any sections blank; incomplete forms may cause issues later.

- Don’t overlook the importance of signatures; ensure all necessary parties sign where required.

- Don’t fabricate or falsely represent any information, as it could lead to serious legal consequences.

- Don’t assume that verbal agreements are sufficient; all agreements should be documented in the addendum.

- Don’t rush through the process; take time to review and verify all information added to the form.

Adhering to these guidelines not only helps maintain the integrity of the contract but also fosters trust and communication among all parties involved.

Misconceptions

Misconceptions about the Addendum To Contract form can lead to confusion for both buyers and sellers. Here are seven common misconceptions:

- This form guarantees financing. Many believe that signing the addendum ensures financial backing. In reality, it only outlines conditions under which financing can be pursued, not a guarantee.

- The buyer is always obligated to complete the purchase. Some assume the buyer must follow through on the contract regardless of appraisal outcomes. The addendum clearly states the buyer can choose not to proceed if the property appraises below the agreed price.

- The seller has no responsibilities. Many sellers think the addendum frees them from all obligations. However, sellers may need to accommodate inspection requirements and adjust sale prices based on appraisals.

- It applies only to FHA and VA loans. A common belief is that the addendum is exclusive to FHA and VA financing. Instead, it can also address conventional loans but must specify those terms separately.

- The appraised value is the same as market value. Buyers often confuse these terms. The appraised value is determined for loan purposes, whereas market value reflects what the property can realistically sell for in the current market.

- Inspection costs are always borne by the seller. Some assume that if inspections are required, sellers are always responsible for the costs. The addendum specifies that these costs may vary and could be negotiated.

- The addendum overrides all other agreement terms. Buyers and sellers may think the addendum's terms reign supreme over the entire contract. The addendum states explicitly that it only controls in conflicts regarding specific details and not overarching contract terms.

Understanding these misconceptions helps both buyers and sellers navigate the complexities of real estate transactions more effectively.

Key takeaways

When it comes to filling out the Addendum To Contract form, keeping a few key points in mind will help ensure a smoother transaction. Here are some important takeaways:

- Understand its Purpose: This addendum is an essential part of the contract. It addresses financing options, specifically FHA and VA loans, which are crucial for many buyers.

- Identifying the Right Parties: Clearly list the seller and buyer names. Accurate identification is vital for legal purposes and prevents any confusion.

- Appraised Value Importance: For FHA financing, make sure to fill in the appraised value of the property. This value determines the maximum insured mortgage amount.

- Be Aware of Financing Contingencies: Both FHA and VA financing come with conditions regarding the appraised value. Knowing these can help protect the buyer's interests.

- Seller's Responsibilities: Understand that if inspections are required, the seller may bear the cost, specifically for VA loans. This needs to be clearly stipulated in the contract.

- Conflict Resolution: If any conflicts arise between the addendum and the main contract, remember that this addendum generally prevails unless it concerns the property description or the parties involved.

- Legal Validity Disclaimer: Understand that the form does not guarantee legal sufficiency. Seek advice from a real estate attorney if unsure about its compliance with your needs.

- Certification Acknowledgment: Signatures from all parties are necessary, highlighting their understanding and acceptance of the terms outlined in the contract.

Approaching this form with clarity and attention to detail will not only protect your interests but also facilitate a more transparent transaction.

Browse Other Templates

Cdph 612 - It must be submitted within ten days after completing each training quarter.

Special Interrogatories Examples - Specific sections of the form address various topics relating to personal injury, property damage, and loss of income, reflecting the diverse aspects of civil claims.

Return Authorization Request,Exchange and Return Form,UrbanOG Product Return Sheet,Customer Return Submission,Refund and Exchange Application,UrbanOG Return & Exchange Request,Merchandise Return Form,UrbanOG Return Processing Form,Return and Refund F - Follow the exchange policy carefully to ensure a smooth process.