Fill Out Your Blamk Free Life Insurance List Form

The Blank Free Life Insurance List form serves as a comprehensive tool for individuals looking to use their life insurance policy as collateral for a loan. This form outlines essential details such as the policy number, insurer, and the parties involved, including the insured and the debtor. By signing this document, the undersigned assigns their life insurance policy to the assignee, granting them specific rights linked to the policy. Notably, these rights include the ability to collect the policy's net proceeds, surrender the policy for its cash value, and obtain loans against the policy itself. Importantly, the agreement specifies certain retained rights, such as the ability to change beneficiaries or collect disability benefits, ensuring the policyholder retains some control. The form also establishes that the policy will serve as collateral for any liabilities owed to the assignee, detailing how any funds received will be managed. Additional provisions stipulate how the assignee can operate with the policy and how they will handle any premiums or additional payments. The document requires notarization and may also include a corporate acknowledgment where applicable, thus ensuring the process is both legal and binding.

Blamk Free Life Insurance List Example

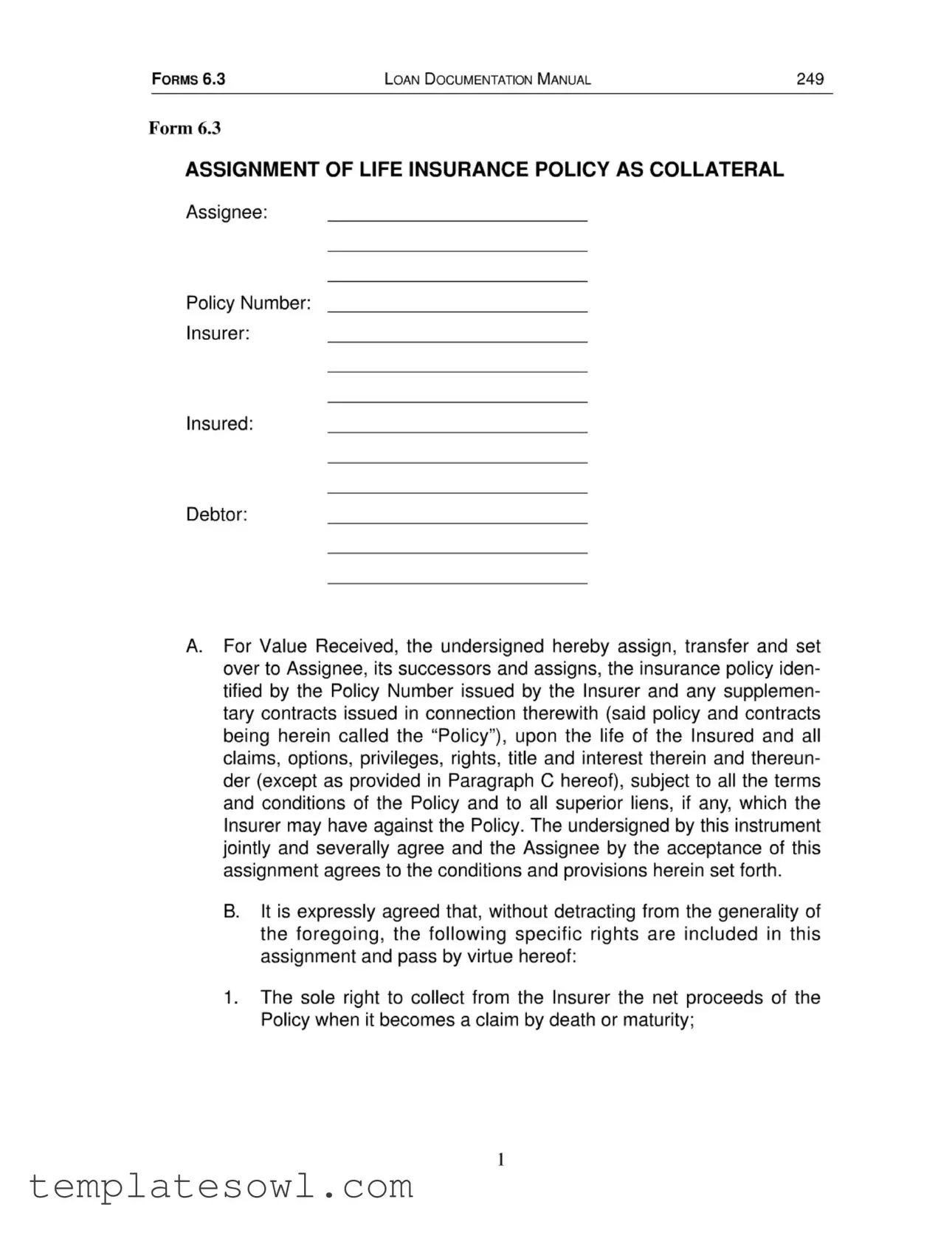

Forms 6.3 |

Loan Documentation Manual |

249 |

Form 6.3

ASSIGNMENT OF LIFE INSURANCE POLICY AS COLLATERAL

Assignee:

Policy Number:

Insurer:

Insured:

Debtor:

A.For Value Received, the undersigned hereby assign, transfer and set over to Assignee, its successors and assigns, the insurance policy iden tified by the Policy Number issued by the Insurer and any supplemen tary contracts issued in connection therewith (said policy and contracts being herein called the “Policy”), upon the life of the Insured and all claims, options, privileges, rights, title and interest therein and thereun der (except as provided in Paragraph C hereof), subject to all the terms and conditions of the Policy and to all superior liens, if any, which the Insurer may have against the Policy. The undersigned by this instrument jointly and severally agree and the Assignee by the acceptance of this assignment agrees to the conditions and provisions herein set forth.

B.It is expressly agreed that, without detracting from the generality of the foregoing, the following specific rights are included in this assignment and pass by virtue hereof:

1.The sole right to collect from the Insurer the net proceeds of the Policy when it becomes a claim by death or maturity;

1

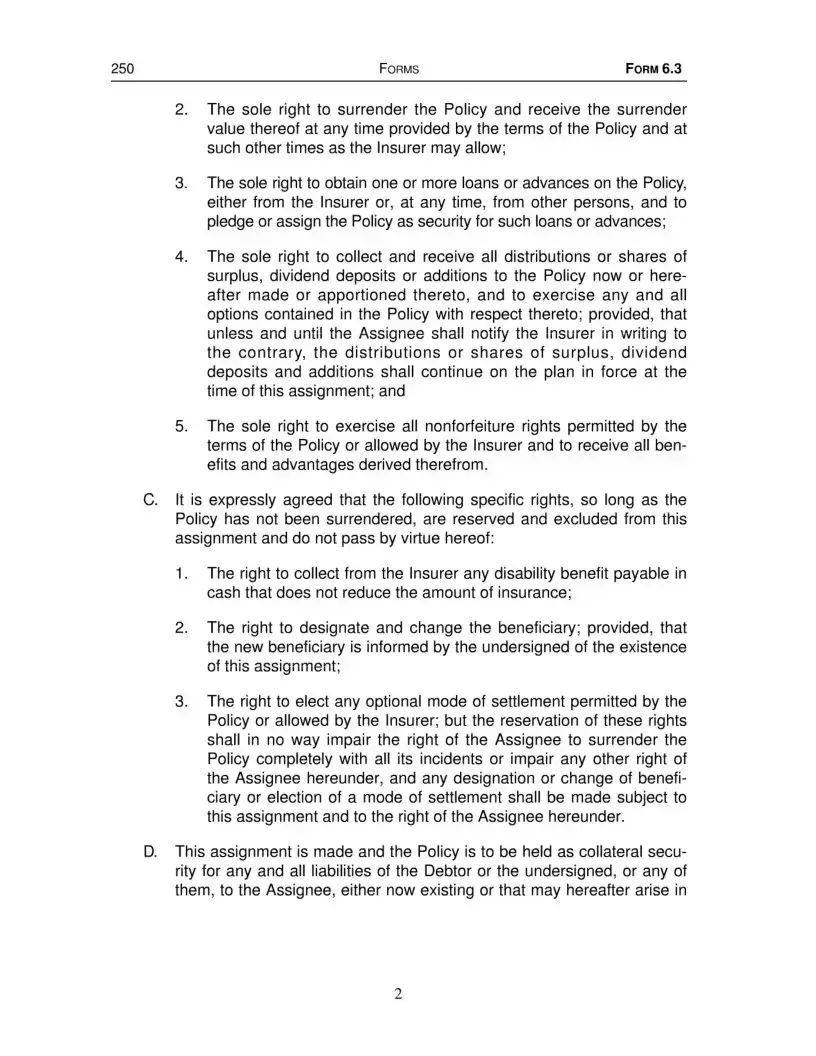

250 |

Forms |

Form 6.3 |

2.The sole right to surrender the Policy and receive the surrender value thereof at any time provided by the terms of the Policy and at such other times as the Insurer may allow;

3.The sole right to obtain one or more loans or advances on the Policy, either from the Insurer or, at any time, from other persons, and to pledge or assign the Policy as security for such loans or advances;

4.The sole right to collect and receive all distributions or shares of surplus, dividend deposits or additions to the Policy now or here after made or apportioned thereto, and to exercise any and all options contained in the Policy with respect thereto; provided, that unless and until the Assignee shall notify the Insurer in writing to the contrary, the distributions or shares of surplus, dividend deposits and additions shall continue on the plan in force at the time of this assignment; and

5.The sole right to exercise all nonforfeiture rights permitted by the terms of the Policy or allowed by the Insurer and to receive all ben efits and advantages derived therefrom.

C.It is expressly agreed that the following specific rights, so long as the Policy has not been surrendered, are reserved and excluded from this assignment and do not pass by virtue hereof:

1.The right to collect from the Insurer any disability benefit payable in cash that does not reduce the amount of insurance;

2.The right to designate and change the beneficiary; provided, that the new beneficiary is informed by the undersigned of the existence of this assignment;

3.The right to elect any optional mode of settlement permitted by the Policy or allowed by the Insurer; but the reservation of these rights shall in no way impair the right of the Assignee to surrender the Policy completely with all its incidents or impair any other right of the Assignee hereunder, and any designation or change of benefi ciary or election of a mode of settlement shall be made subject to this assignment and to the right of the Assignee hereunder.

D.This assignment is made and the Policy is to be held as collateral secu rity for any and all liabilities of the Debtor or the undersigned, or any of them, to the Assignee, either now existing or that may hereafter arise in

2

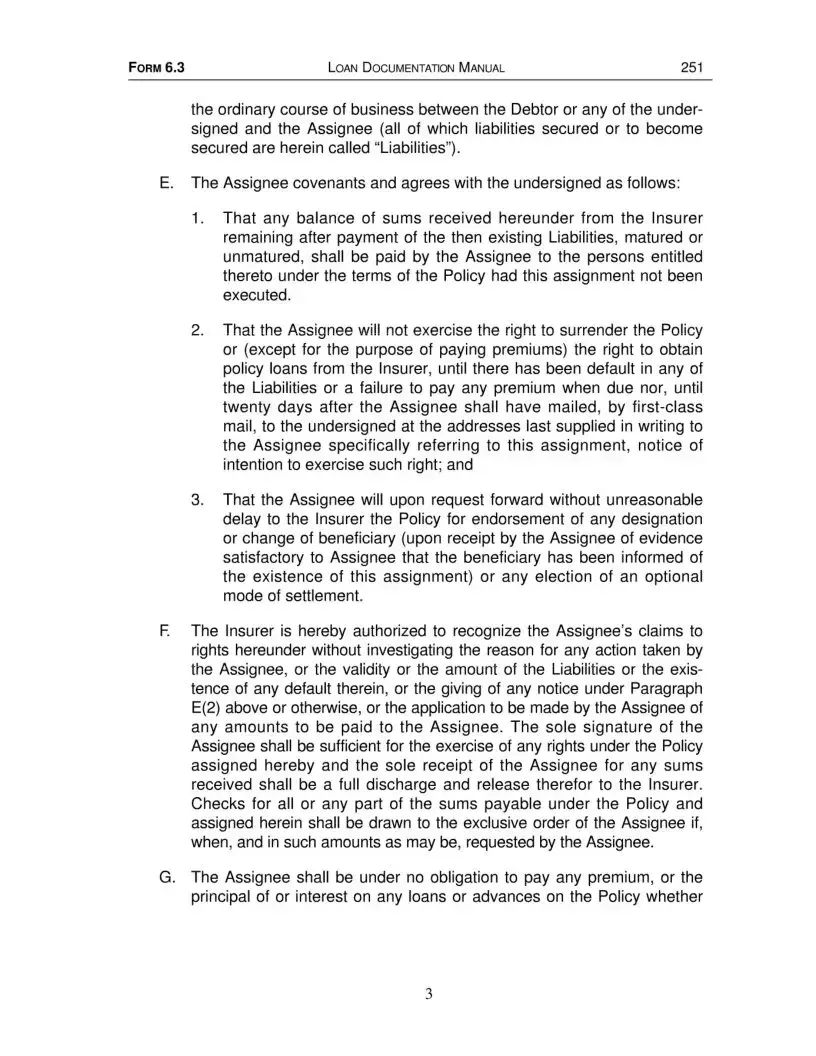

Form 6.3 |

Loan Documentation Manual |

251 |

the ordinary course of business between the Debtor or any of the under signed and the Assignee (all of which liabilities secured or to become secured are herein called “Liabilities”).

E.The Assignee covenants and agrees with the undersigned as follows:

1.That any balance of sums received hereunder from the Insurer remaining after payment of the then existing Liabilities, matured or unmatured, shall be paid by the Assignee to the persons entitled thereto under the terms of the Policy had this assignment not been executed.

2.That the Assignee will not exercise the right to surrender the Policy or (except for the purpose of paying premiums) the right to obtain policy loans from the Insurer, until there has been default in any of the Liabilities or a failure to pay any premium when due nor, until twenty days after the Assignee shall have mailed, by

3.That the Assignee will upon request forward without unreasonable delay to the Insurer the Policy for endorsement of any designation or change of beneficiary (upon receipt by the Assignee of evidence satisfactory to Assignee that the beneficiary has been informed of the existence of this assignment) or any election of an optional mode of settlement.

F.The Insurer is hereby authorized to recognize the Assignee’s claims to rights hereunder without investigating the reason for any action taken by the Assignee, or the validity or the amount of the Liabilities or the exis tence of any default therein, or the giving of any notice under Paragraph E(2) above or otherwise, or the application to be made by the Assignee of any amounts to be paid to the Assignee. The sole signature of the Assignee shall be sufficient for the exercise of any rights under the Policy assigned hereby and the sole receipt of the Assignee for any sums received shall be a full discharge and release therefor to the Insurer. Checks for all or any part of the sums payable under the Policy and assigned herein shall be drawn to the exclusive order of the Assignee if, when, and in such amounts as may be, requested by the Assignee.

G.The Assignee shall be under no obligation to pay any premium, or the principal of or interest on any loans or advances on the Policy whether

3

252 |

Forms |

Form 6.3 |

or not obtained by the Assignee, or any other charges on the Policy, but any such amounts so paid by the Assignee from its own funds, shall become a part of the Liabilities hereby secured, shall be due immediate ly, and shall draw interest at a rate fixed by the Assignee from time to time not exceeding 6% per annum.

H.The exercise of any right, option, privilege or power given herein to the Assignee shall be at the option of the Assignee, but (except as restricted by Paragraph E (2) above) the Assignee may exercise any such right, option, privilege or power without notice to, or assent by, or affecting the liability of, or releasing any interest hereby assigned by the Debtor, the undersigned, or any of them.

I.The Assignee may take or release other security, may release any party primarily or secondarily liable for any of the Liabilities, may grant exten sions, renewals or indulgences with respect to the Liabilities, or may apply to the Liabilities, in such order as the Assignee shall determine, the proceeds of the Policy hereby assigned or any amount received on account of the Policy by the exercise of any right permitted under this assignment, without resorting or regard to other security.

J.In the event of any conflict between the provisions of this assignment and provisions of the note or other evidence of any Liability, with respect to the Policy or rights of collateral security therein, the provisions of this assignment shall prevail.

K.Each of the undersigned declares that no proceedings in bankruptcy are pending against him or her and that his or her property is not subject to any assignment for the benefit of creditors.

Signed and sealed this |

day of |

, 20 |

|

|

|

____________________________(L.S.) |

|

Witness |

|

Insured or Owner |

|

Address |

|

|

|

Witness |

Beneficiary |

|

(L.S.) |

|

|

||

Address

Individual Acknowledgment

4

Form 6.3 |

|

Loan Documentation Manual |

253 |

State of |

|

) |

|

|

|

)ss |

|

County of |

|

) |

|

On the |

day of |

, 20 |

before me personal |

ly came |

|

|

, to me |

known to be the individual described in and who executed the foregoing assign ment and acknowledged to me that he or she executed the same.

Notary Public

My commissions expires |

. |

Corporate Acknowledgment

State of |

) |

|

)ss |

County of |

) |

On the |

day of |

, 20 |

before me personal |

ly came |

|

|

, who being |

by me duly sworn, did depose and |

say that he or she resides in |

|

, that he or she is |

the |

of |

,the corporation described in and which executed the foregoing assignment; that he knows the seal of said corporation; that the seal affixed to said assignment is such corporate seal; that it was so affixed by order of the Board of Directors of said corporation, and that he or she signed his or her name thereto by like order.

254 |

Forms |

Form 6.3 |

|

Notary Public |

|

My commissions expires |

|

. |

Duplicate received and filed at the home office of the Insurer in

, this |

day of |

, |

20 . |

|

|

By________________________________

Authorized Officer

NOTE: When executed by a corporation, the corporate seal should be affixed and there should be attached to the assignment a certified copy of the resolution of the Board of Directors authorizing the signing officer to execute and deliver the assignment in the name and on behalf of the corporation.

6

Form Characteristics

| Fact Name | Details |

|---|---|

| Document Type | This is the Assignment of Life Insurance Policy as Collateral form, referred to as Form 6.3. |

| Purpose | It allows the undersigned to assign a life insurance policy as collateral security for various liabilities. |

| Governing Laws | Each state may have specific laws governing the assignment of insurance policies; consult local statutes. |

| Assignee Rights | The assignee gains the right to collect, surrender the policy, and take loans against it. |

| Reserved Rights | The policyholder retains specific rights, like the ability to change beneficiaries and collect certain benefits. |

| Collateral Security | The assignment serves as collateral for any current or future liabilities to the assignee. |

| Insurance Company | The insurance company must recognize the assignee's claims without questioning the validity of the underlying liabilities. |

| Payment Responsibilities | The assignee is not obligated to pay premiums or loan amounts but can do so from its own funds. |

| Conflict Resolution | If there’s a conflict between this assignment and any other related documents, this assignment’s provisions take precedence. |

| Bankruptcy Declaration | The undersigned confirms that no bankruptcy proceedings are ongoing against them, ensuring their eligibility to assign the policy. |

Guidelines on Utilizing Blamk Free Life Insurance List

Completing the Blank Free Life Insurance List form involves carefully providing specific details related to the assignment of a life insurance policy. Follow the steps outlined below to ensure accurate and complete information is entered on the form.

- Begin by entering the Assignee's Name. This is the individual or entity receiving the assignment of the policy.

- Next, fill in the Policy Number. This identifier must match the number indicated on your life insurance policy.

- In the Insurer field, provide the name of the insurance company responsible for the policy.

- For the Insured section, input the name of the person whose life is covered by the insurance policy.

- In the Debtor field, enter the name of the individual or entity that owes a liability to the Assignee.

- Review the section labeled For Value Received to confirm a clear understanding of the terms being agreed upon. This section outlines the assignment of rights to the Assignee.

- In parts B and C, acknowledge and note the specific rights being assigned or retained. No entries are required here, but understanding these rights is essential.

- Proceed to complete the area labeled Signed and sealed. Fill in the date and signature of the Insured or Owner. Include their address for correspondence.

- Identify a witness who will also need to sign and provide their Address.

- If applicable, the Beneficiary section must also be completed with the necessary signature and address.

- In the Individual Acknowledgment section, date and sign the form in the specified fields. Ensure the notary public can identify each party involved. This will be filled out by the notary.

- If the assignment is made by a corporation, complete the Corporate Acknowledgment section with the appropriate corporate officer's name and title. The officer must also sign this section.

Once completed, the form should be reviewed for accuracy before submitting it to the relevant parties. Engaging a notary public for signatures will help with the formalization and recognition of this document.

What You Should Know About This Form

What is the purpose of the Blank Free Life Insurance List form?

This form serves as an assignment of a life insurance policy as collateral security. When someone has outstanding liabilities, they can assign their life insurance policy to a lender or assignee, ensuring that the insurer acknowledges this assignment. This gives the assignee certain rights related to the policy in case of default on the liabilities.

Who are the key parties involved in this assignment?

The main parties include the Assignee, who is the entity receiving the assignment (usually a lender), the Insured, who is the individual whose life is covered by the insurance policy, the Debtor, who is the borrower obligated to repay the liabilities, and the Insurer, the company providing the life insurance.

What rights does the Assignee obtain through this assignment?

Upon assignment, the Assignee gains specific rights including the ability to collect proceeds from the life insurance policy upon death or maturity, surrender the policy for its cash value, obtain loans against the policy, and receive distributions related to the policy. However, specific rights are reserved for the policy owner as outlined in the form.

Can the policyholder change the beneficiary after assigning the policy?

Yes, the policyholder can change the beneficiary, but it is required that any new beneficiary be informed of the assignment. Additionally, the right to change the beneficiary is still subjected to the conditions set forth in the assignment.

What happens if the Insured passes away before the debt is paid?

If the Insured passes away before the liabilities are settled, the Assignee is entitled to claim the death benefit from the life insurance policy. The proceeds will first be used to satisfy the outstanding debts and any remaining balance will be distributed according to the policy’s terms.

Are there any rights that the policyholder retains after the assignment?

Indeed, the policyholder retains specific rights after the assignment, such as the right to collect any disability benefits that do not reduce the total insurance amount, and the right to elect settlement options as outlined in the policy. These rights ensure that the policyholder has a degree of control over the policy even after it has been assigned.

What should the Assignee do if they wish to surrender the policy?

The Assignee must wait until there is a default on the liabilities or a failure to pay premiums before exercising the right to surrender the policy. Additionally, they must notify the policyholder in writing of their intention to do so, allowing a twenty-day grace period for compliance.

How does this form accommodate future liabilities?

This form is designed to cover any and all current and future liabilities that may arise in the ordinary course of business between the Debtor and Assignee. It acts as a security agreement that evolves with the financial situation of the parties involved, ensuring ongoing protection for the Assignee.

What is required for the assignment to be legally binding?

For the assignment to be legally binding, it must be signed by the relevant parties and properly acknowledged, often in the presence of witnesses or a notary. It ensures there is a clear record of the agreement and the associated rights without ambiguity.

Common mistakes

When filling out the Blamk Free Life Insurance List form, individuals often make common mistakes that can lead to complications. One major mistake is omitting essential information. Many applicants forget to include the assignee's name or policy number. Without these details, the form may be considered incomplete.

Another frequent issue is an incorrectly filled policy number. Even a single digit mistake can create significant problems in identifying the correct policy. Accuracy in this area is crucial to ensure that the assignment is valid and properly processed.

Some people misunderstand the role of the assignee and beneficiary. It is vital to clearly distinguish between these two roles. The assignee has rights to the policy as collateral, while the beneficiary receives the proceeds upon the insured's death. Confusing these roles can lead to disputes and unintended consequences.

A lack of proper signatures and dates also commonly occurs. Signatures must match those of the individuals listed on the form. Additionally, dating the document ensures that all parties are clear on when the assignment was made, which is important for legal and processing purposes.

Another mistake is neglecting to read the terms and conditions thoroughly. Many individuals check off boxes without understanding the implications. Ignoring the provisions can lead to significant issues down the line, especially regarding rights and responsibilities outlined in the document.

Some applicants also fail to provide a clear mailing address for correspondence. If the assignee's address is incorrect or not provided, communication may be hindered, resulting in delays or failures in processing important actions related to the policy.

Moreover, leaving out the witness signatures can invalidate the form. Each of the parties involved needs to have at least one witness to ensure that the assignment process is transparent and acknowledged by credible parties.

Lastly, individuals often skip the acknowledgment section, especially in corporate situations. This section is essential as it verifies the identity and authority of those signing on behalf of a corporation. Without this acknowledgment, the entire assignment could be challenged later on.

Documents used along the form

The Blank Free Life Insurance List form is a crucial document when dealing with life insurance policies. Along with this form, several other documents play significant roles in ensuring that all legal obligations and rights are adequately addressed. Here’s an overview of key forms that are often used together with the Blank Free Life Insurance List form.

- Assignment of Life Insurance Policy as Collateral: This document allows an insured person to assign their life insurance policy to another party as collateral for a debt. It outlines rights to the policy, including the ability to collect proceeds or surrender the policy if necessary.

- Life Insurance Policy Contract: This is the original policy document that details all the terms and conditions of the insurance coverage. It includes information such as coverage amounts, premium payments, and any exclusions.

- Change of Beneficiary Form: This form is used to officially change the designated beneficiary of the life insurance policy. It ensures that the new beneficiary is legally recognized in case of the insured’s passing.

- Loan Request Form: If the insured wishes to borrow against their life insurance policy, this form allows them to request a loan. It outlines the terms of the loan and any implications on the policy itself.

By keeping these documents in mind and utilizing them appropriately, individuals can navigate their life insurance matters with greater confidence and clarity. Each document serves a specific purpose, helping to safeguard rights and responsibilities in the realm of life insurance.

Similar forms

- Power of Attorney (POA): Similar to the Blamk Free Life Insurance List form, a POA grants authority to another person to act on behalf of the principal. This document specifies the powers assigned and can include financial and healthcare decisions.

- Loan Agreement: Just like the assignment form, a loan agreement outlines the terms of borrowing money. It includes details about collateral, repayment terms, and responsibilities of both parties.

- Collateral Agreement: This document secures an obligation with a specific asset, much like how the insurance policy is used as collateral. It delineates the rights and claims of the lender to the collateralized asset.

- Beneficiary Designation Form: This form outlines who will receive benefits from a policy or account when the insured individual or account holder passes away. The distinction lies in the fact that it focuses on the beneficiary's rights instead of the assignment of policy income.

- Insurance Policy Waiver: A waiver allows the policyholder to relinquish certain rights. Similar to the assignment document, it defines the specific rights retained and waived, including any effects on benefits.

- Mortgage Agreement: A mortgage agreement contains terms related to property loan security, identifying a property as collateral. It shares the concept of collateral used to guarantee fulfillment of financial obligations, akin to the insurance policy assignment.

- Release of Lien: Similar to the provisions in the assignment form, a release of lien is a document that verifies the cancellation of a lender’s claim on a secured asset after the debt has been fully satisfied.

- Trust Deed: This document serves as a type of security for a loan, where the property is held in trust to guarantee repayment. It parallels the assignment by designating what happens upon debt fulfillment.

- Divorce Settlement Agreement: This legal document settles the financial terms and issues arising from a divorce. It can similarly list rights and responsibilities for assets, echoing the assignment's detailed declaration of rights to the insurance policy.

- Release of Claims Form: This document confirms that one party is releasing the other from any further claims. Like the Blamk Free Life Insurance List form, it outlines conditions and rights related to liabilities and assets.

Dos and Don'ts

When filling out the Blamk Free Life Insurance List form, consider the following tips to ensure a smooth process. Here’s what to do and what to avoid:

- DO read the instructions carefully before starting. Understanding the requirements can save you time and frustration later.

- DO double-check all the information provided. Accurate details are crucial for the assignment to be valid.

- DO sign and date the form in the designated areas. This step is necessary to validate the document.

- DO keep a copy for your records. Having a backup is always a good idea for reference.

- DO consult a professional if you have questions. Sometimes, clarity is just a conversation away.

- DON'T rush through the form. Taking your time can help prevent mistakes that might delay processing.

- DON'T leave any fields blank unless specified. Missing information could lead to complications.

- DON'T use correction fluid or tape. It’s best to start fresh if a mistake is made.

- DON'T ignore the deadlines. Be aware of any timelines to ensure your assignment is timely.

- DON'T assume everything is fine without reviewing. Even small errors can cause big issues.

Misconceptions

Understanding life insurance assignments can be complex, and various misconceptions can lead to confusion. Here are five common misconceptions about the Blank Free Life Insurance List form:

- 1. Assigning a life insurance policy means giving up all rights to it. Many believe that once a life insurance policy is assigned, the original owner loses all rights. In reality, certain rights, such as designating a beneficiary and collecting disability benefits, can remain with the original owner if specifically reserved in the assignment.

- 2. The Assignee automatically takes control of the policy. While the assignee does gain certain rights, they cannot exercise these rights, such as surrendering the policy, without specific conditions being met, including a default on liabilities. This ensures that the original owner maintains some level of control over their policy until certain criteria are fulfilled.

- 3. All policies can be assigned without limitations. People often think any life insurance policy can be assigned with ease. However, some policies may have restrictions based on their terms or specific state laws, which could affect assignment options. It's essential to read the specific provisions of the policy in question.

- 4. The Insurer has to investigate all claims made by the Assignee. Many assume that the insurer must validate the legitimacy of each action taken by the assignee. On the contrary, the insurer is authorized to accept the assignee's claims without delving into the underlying facts of the assignment, provided proper procedures are followed.

- 5. Policy assignments are only useful for immediate loans. While these assignments can indeed facilitate loans, they can offer broader benefits as well, such as providing security for other financial liabilities. It’s a comprehensive tool that can be beneficial in various financial arrangements, not limited to just obtaining loans against the policy.

By understanding these misconceptions, individuals can gain a clearer insight into how life insurance assignments function and what implications they may carry.

Key takeaways

When filling out and using the Blank Free Life Insurance List form, keep these important points in mind:

- Understand the Purpose: This form is primarily used to assign a life insurance policy as collateral for loans. It allows the assignee to have rights over the policy.

- Gather Necessary Information: Before starting, collect all required details like the policy number, insurer, and information about the insured and debtor.

- Assign the Policy Properly: Ensure that the policy is correctly assigned to the assignee, along with a clear reference to the rights and interests being transferred.

- Know Your Rights: Familiarize yourself with the specific rights that are being passed to the assignee, such as the right to receive proceeds upon a claim.

- Retain Certain Rights: Remember that some rights, like changing the beneficiary or collecting certain benefits, are not transferred and remain with the policyholder.

- Understand the Conditions: Pay attention to the conditions under which the assignee can exercise their rights, including situations of default on liabilities.

- Obtain Required Signatures: The document must be signed by the insured or owner and witnessed to make it valid.

- Consider Notarization: For added security, consider having the document notarized to verify the authenticity of the signatures.

Being meticulous while completing this form can help ensure that the assignment process goes smoothly and that the rights of all parties are respected.

Browse Other Templates

Wedding Cake Contract - Provide a detailed description of your cake to help the bakery bring your vision to life.

Federal Habeas Corpus - Your narrative in the petition serves as a critical element in the court's review process.

Pregnancy Note From Doctor - Understanding the implications of signing this form is vital for parents.