Fill Out Your Circle K W2 Form

The Circle K W-2 form serves as an essential document for both employers and employees, providing crucial information regarding wage and tax reporting. Employers use this form to report an employee's annual wages and the amount of taxes withheld for federal, state, and local obligations. It includes various fields that detail wages, tips, and other compensation, as well as social security and Medicare tax information. Each employee receives multiple copies of the W-2 form, including those for their personal records, state tax filing, and federal tax return. Employers must ensure accurate completion to avoid penalties, particularly when filing with the Social Security Administration (SSA). The form has specific instructions regarding the submission of the scannable Copy A, and it distinguishes between printable copies that serve informative purposes. Additionally, the W-2 form accommodates various tax credits and benefits, which may affect an employee’s eligibility for refunds. By understanding the critical components of the Circle K W-2 form, employees can navigate their tax responsibilities with greater clarity.

Circle K W2 Example

Attention:

You may file Forms

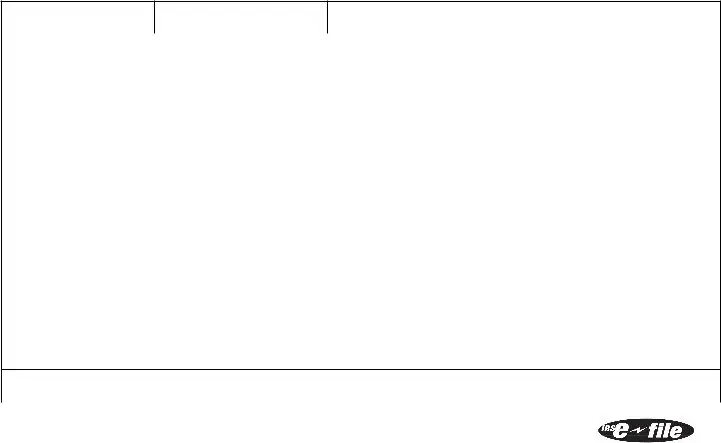

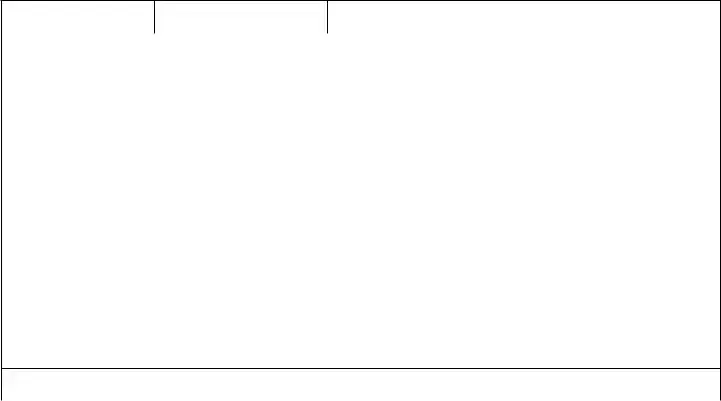

Note: Copy A of this form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. The official printed version of this IRS form is scannable, but the online version of it, printed from this website, is not. Do not print and file Copy A downloaded from this website with the SSA; a penalty may be imposed for filing forms that can’t be scanned. See the penalties section in the current General Instructions for Forms

Please note that Copy B and other copies of this form, which appear in black, may be downloaded, filled in, and printed and used to satisfy the requirement to provide the information to the recipient.

To order official IRS information returns such as Forms

See IRS Publications 1141, 1167, and 1179 for more information about printing these tax forms.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

22222 |

Void |

|

|

|

a |

Employee’s social security number |

For Official Use Only ▶ |

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

OMB No. |

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

b Employer identification number (EIN) |

|

|

|

|

|

1 Wages, tips, other compensation |

|

2 Federal income tax withheld |

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

c Employer’s name, address, and ZIP code |

|

3 |

Social security wages |

|

|

|

4 Social security tax withheld |

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 Medicare wages and tips |

|

6 |

Medicare tax withheld |

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Social security tips |

|

|

|

8 |

Allocated tips |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d Control number |

|

|

|

|

|

|

|

|

|

9 |

|

|

|

|

|

|

|

10 |

Dependent care benefits |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e Employee’s first name and initial |

|

|

Last name |

|

Suff. |

11 |

Nonqualified plans |

|

|

|

12a See instructions for box 12 |

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13 |

Statutory |

Retirement |

|

12b |

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

employee |

plan |

sick pay |

|

C |

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14 Other |

|

|

|

|

|

12c |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

f Employee’s address and ZIP code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

15 STATE |

Employer’s state ID number |

|

|

16 State wages, tips, etc. |

17 State income tax |

|

18 Local wages, tips, etc. |

19 Local income tax |

20 Locality name |

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form |

2016 |

Copy A For Social Security Administration — Send this entire page with

Form

Department of the

For Privacy Act and Paperwork Reduction Act Notice, see the separate instructions.

Cat. No. 10134D

Do Not Cut, Fold, or Staple Forms on This Page

22222 |

a Employee’s social security number |

|

|

OMB No. |

|

|

|

|

|

|

|

b Employer identification number (EIN) |

|

|

1 |

Wages, tips, other compensation |

|

2 Federal income tax withheld |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

c Employer’s name, address, and ZIP code |

3 |

Social security wages |

|

|

|

4 Social security tax withheld |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 Medicare wages and tips |

6 |

Medicare tax withheld |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Social security tips |

|

|

8 |

Allocated tips |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d Control number |

|

|

9 |

|

|

|

|

|

|

|

10 |

Dependent care benefits |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e Employee’s first name and initial |

Last name |

Suff. 11 |

Nonqualified plans |

|

|

|

12a |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

13 |

Statutory |

Retirement |

|

12b |

|

|

|

|||||

|

|

|

|

|

|

employee |

plan |

sick pay |

|

C |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14 Other |

|

|

|

|

|

12c |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

f Employee’s address and ZIP code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

15 STATE |

Employer’s state ID number |

|

16 State wages, tips, etc. |

17 State income tax |

|

18 Local wages, tips, etc. |

19 Local income tax |

20 Locality name |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form |

Wage and Tax |

2016 |

Department of the |

Statement |

|

Copy

|

|

a |

Employee’s social security number |

|

|

|

Safe, accurate, |

|

|

|

|

|

Visit the IRS website at |

|

|||||

|

|

|

|

|

OMB No. |

FAST! Use |

|

|

|

|

|

www.irs.gov/efile |

|

||||||

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

b Employer identification number (EIN) |

|

|

|

1 |

Wages, tips, other compensation |

|

2 Federal income tax withheld |

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

c Employer’s name, address, and ZIP code |

|

3 |

Social security wages |

|

|

|

4 Social security tax withheld |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

5 Medicare wages and tips |

|

6 |

Medicare tax withheld |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Social security tips |

|

|

|

8 |

Allocated tips |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

d Control number |

|

|

|

9 |

|

|

|

|

|

|

|

10 |

Dependent care benefits |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e Employee’s first name and initial |

Last name |

Suff. |

11 |

Nonqualified plans |

|

|

|

12a See instructions for box 12 |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

13 |

Statutory |

Retirement |

|

12b |

|

|

|

|

|

||||

|

|

|

|

|

|

|

employee |

plan |

sick pay |

|

C |

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

14 Other |

|

|

|

|

|

12c |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

f Employee’s address and ZIP code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

15 STATE |

Employer’s state ID number |

|

16 State wages, tips, etc. |

17 State income tax |

|

18 Local wages, tips, etc. |

19 Local income tax |

20 Locality name |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form |

Wage and Tax |

2016 |

Department of the |

Statement |

|

Copy

This information is being furnished to the Internal Revenue Service.

Notice to Employee

Do you have to file? Refer to the Form 1040 instructions to determine if you are required to file a tax return. Even if you do not have to file a tax return, you may be eligible for a refund if box 2 shows an amount or if you are eligible for any credit.

Earned income credit (EIC). You may be able to take the EIC for 2016 if your adjusted gross income (AGI) is less than a certain amount. The amount of the credit is based on income and family size. Workers without children could qualify for a smaller credit. You and any qualifying children must have valid social security numbers (SSNs). You cannot take the EIC if your investment income is more than the specified amount for 2016 or if income is earned for services provided while you were an inmate at a penal institution. For 2016 income limits and more information, visit www.irs.gov/eitc. Also see Pub. 596, Earned Income Credit. Any EIC that is more than your tax liability is refunded to you, but only if you file a tax return.

Clergy and religious workers. If you are not subject to social security and Medicare taxes, see Pub. 517, Social Security and Other Information for Members of the Clergy and Religious Workers.

Corrections. If your name, SSN, or address is incorrect, correct Copies B, C, and 2 and ask your employer to correct your employment record. Be sure to ask the employer to file Form

to correct any name, SSN, or money amount error reported to the SSA on Form

Cost of

Credit for excess taxes. If you had more than one employer in 2016 and more than $7,347 in social security and/or Tier 1 railroad retirement (RRTA) taxes were withheld, you may be able to claim a credit for the excess against your federal income tax. If you had more than one railroad employer and more than $4,321.80 in Tier 2 RRTA tax was withheld, you also may be able to claim a credit. See your Form 1040 or Form 1040A instructions and Pub. 505, Tax Withholding and Estimated Tax.

(Also see Instructions for Employee on the back of Copy C.)

aEmployee’s social security number

This information is being furnished to the Internal Revenue Service. If you

OMB No.

b Employer identification number (EIN) |

|

|

|

1 |

Wages, tips, other compensation |

|

2 Federal income tax withheld |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

c Employer’s name, address, and ZIP code |

|

3 |

Social security wages |

|

|

|

4 Social security tax withheld |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 Medicare wages and tips |

|

6 |

Medicare tax withheld |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Social security tips |

|

|

|

8 |

Allocated tips |

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d Control number |

|

|

|

9 |

|

|

|

|

|

|

|

10 |

Dependent care benefits |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e Employee’s first name and initial |

Last name |

Suff. |

11 |

Nonqualified plans |

|

|

|

12a See instructions for box 12 |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

13 |

Statutory |

Retirement |

|

12b |

|

|

|

||||

|

|

|

|

|

|

employee |

plan |

sick pay |

|

C |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

14 Other |

|

|

|

|

|

12c |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

f Employee’s address and ZIP code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15 STATE |

Employer’s state ID number |

|

16 State wages, tips, etc. |

17 State income tax |

|

18 Local wages, tips, etc. |

19 Local income tax |

20 Locality name |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form |

Wage and Tax |

2016 |

Department of the |

|

|||

Statement |

Safe, accurate, |

||

|

|

|

FAST! Use |

Copy

Employee on the back of Copy B.)

Instructions for Employee (Also see Notice to Employee,

on the back of Copy B.)

Box 1. Enter this amount on the wages line of your tax return.

Box 2. Enter this amount on the federal income tax withheld line of your tax return.

Box 5. You may be required to report this amount on Form 8959, Additional Medicare Tax. See the Form 1040 instructions to determine if you are required to complete Form 8959.

Box 6. This amount includes the 1.45% Medicare Tax withheld on all Medicare wages and tips shown in box 5, as well as the 0.9% Additional Medicare Tax on any of those Medicare wages and tips above $200,000.

Box 8. This amount is not included in boxes 1, 3, 5, or 7. For information on how to report tips on your tax return, see your Form 1040 instructions.

You must file Form 4137, Social Security and Medicare Tax on Unreported Tip Income, with your income tax return to report at least the allocated tip amount unless you can prove that you received a smaller amount. If you have records that show the actual amount of tips you received, report that amount even if it is more or less than the allocated tips. On Form 4137 you will calculate the social security and Medicare tax owed on the allocated tips shown on your Form(s)

Box 10. This amount includes the total dependent care benefits that your employer paid to you or incurred on your behalf (including amounts from a section 125 (cafeteria) plan). Any amount over $5,000 is also included in box

1.Complete Form 2441, Child and Dependent Care Expenses, to compute any taxable and nontaxable amounts.

Box 11. This amount is (a) reported in box 1 if it is a distribution made to you from a nonqualified deferred compensation or nongovernmental section 457(b) plan or (b) included in box 3 and/or 5 if it is a prior year deferral under a nonqualified or section 457(b) plan that became taxable for social security and Medicare taxes this year because there is no longer a substantial risk of forfeiture of your right to the deferred amount. This box should not be used if you had a deferral and a distribution in the same calendar year. If you made a deferral and received a distribution in the same calendar year, and you are or will be age 62 by the end of the calendar year, your employer should file Form

Box 12. The following list explains the codes shown in box 12. You may need this information to complete your tax return. Elective deferrals (codes D, E, F, and S) and designated Roth contributions (codes AA, BB, and EE) under all plans are generally limited to a total of $18,000 ($12,500 if you only have SIMPLE plans; $21,000 for section 403(b) plans if you qualify for the

However, if you were at least age 50 in 2016, your employer may have allowed an additional deferral of up to $6,000 ($3,000 for section 401(k)(11) and 408(p) SIMPLE plans). This additional deferral amount is not subject to the overall limit on elective deferrals. For code G, the limit on elective deferrals may be higher for the last 3 years before you reach retirement age. Contact your plan administrator for more information. Amounts in excess of the overall elective deferral limit must be included in income. See the “Wages, Salaries, Tips, etc.” line instructions for Form 1040.

Note: If a year follows code D through H, S, Y, AA, BB, or EE, you made a

(continued on back of Copy 2)

aEmployee’s social security number

OMB No.

b Employer identification number (EIN) |

|

|

|

1 |

Wages, tips, other compensation |

|

2 Federal income tax withheld |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

c Employer’s name, address, and ZIP code |

|

3 |

Social security wages |

|

|

|

4 Social security tax withheld |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 Medicare wages and tips |

|

6 |

Medicare tax withheld |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Social security tips |

|

|

|

8 |

Allocated tips |

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d Control number |

|

|

|

9 |

|

|

|

|

|

|

|

10 |

Dependent care benefits |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e Employee’s first name and initial |

Last name |

Suff. |

11 |

Nonqualified plans |

|

|

|

12a |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

13 |

Statutory |

Retirement |

|

12b |

|

|

|

||||

|

|

|

|

|

|

employee |

plan |

sick pay |

|

C |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

14 Other |

|

|

|

|

|

12c |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

f Employee’s address and ZIP code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15 STATE |

Employer’s state ID number |

|

16 State wages, tips, etc. |

17 State income tax |

|

18 Local wages, tips, etc. |

19 Local income tax |

20 Locality name |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form |

Wage and Tax |

2016 |

Department of the |

Statement |

|

Copy

Income Tax Return

Instructions for Employee (continued from back of

Copy C)

Box 13. If the “Retirement plan” box is checked, special limits may apply to the amount of traditional IRA contributions you may deduct. See Pub.

Box 14. Employers may use this box to report information such as state disability insurance taxes withheld, union dues, uniform payments, health insurance premiums deducted, nontaxable income, educational assistance payments, or a member of the clergy's parsonage allowance and utilities. Railroad employers use this box to report railroad retirement (RRTA) compensation, Tier 1 tax, Tier 2 tax, Medicare tax and Additional Medicare Tax. Include tips reported by the employee to the employer in railroad retirement (RRTA) compensation.

Note: Keep Copy C of Form

Void |

a Employee’s social security number |

|

OMB No. |

||

|

b Employer identification number (EIN) |

|

|

|

1 |

Wages, tips, other compensation |

|

2 Federal income tax withheld |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

c Employer’s name, address, and ZIP code |

|

3 |

Social security wages |

|

|

|

4 Social security tax withheld |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 Medicare wages and tips |

|

6 |

Medicare tax withheld |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Social security tips |

|

|

|

8 |

Allocated tips |

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d Control number |

|

|

|

9 |

|

|

|

|

|

|

|

10 |

Dependent care benefits |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e Employee’s first name and initial |

Last name |

Suff. |

11 |

Nonqualified plans |

|

|

|

12a See instructions for box 12 |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

13 |

Statutory |

Retirement |

|

12b |

|

|

|

||||

|

|

|

|

|

|

employee |

plan |

sick pay |

|

C |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

14 Other |

|

|

|

|

|

12c |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

o |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

d |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

e |

|

|

|

f Employee’s address and ZIP code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15 STATE |

Employer’s state ID number |

|

16 State wages, tips, etc. |

17 State income tax |

|

18 Local wages, tips, etc. |

19 Local income tax |

20 Locality name |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form |

Wage and Tax |

2016 |

Department of the |

Statement |

For Privacy Act and Paperwork Reduction |

Act Notice, see separate instructions.

Copy D — For Employer

Form Characteristics

| Fact Name | Fact Description |

|---|---|

| Filing Options | Employers can file Forms W-2 and W-3 electronically through the SSA's website. |

| Copy A Purpose | Copy A serves informational purposes only and cannot be filed with the SSA if downloaded. |

| Penalties for Filing | Filing a non-scannable Copy A may lead to penalties according to IRS guidelines. |

| Copy B Usage | Copy B may be downloaded, filled in, and printed to provide information to employees. |

| IRS Ordering | Organizations can order official IRS forms, including scannable Copies A, through the IRS website. |

| Employer Identification | The W-2 form requires the employer's identification number (EIN) and state ID number. |

| Dependent Care Benefits | Employers report dependent care benefits in box 10 of the W-2 form. |

| State-Specific Requirements | State-specific regulations may apply. Always check your state's governing laws for compliance. |

Guidelines on Utilizing Circle K W2

After receiving your Circle K W-2 form, it's essential to fill it out correctly to ensure accurate reporting of your income to the Internal Revenue Service (IRS) and state tax authorities. Follow the steps outlined below to complete the form correctly.

- Locate your social security number: Write your social security number in box a. This number is essential for your tax records.

- Find your employer identification number (EIN): This number will be listed in box b. You can obtain it from your employer if necessary.

- Report your wages: Fill in box 1 to indicate your total wages, tips, and other compensation for the year.

- Document federal income tax withheld: Enter the amount withheld from your payments in box 2.

- Enter your employer’s information: In box c, write the name, address, and ZIP code of your employer.

- Complete social security wages: In box 3, provide the total of your social security wages.

- Note social security tax withheld: Enter the amount withheld for social security tax in box 4.

- Fill in Medicare wages and tips: Box 5 should show the total Medicare wages and tips received.

- Document Medicare tax withheld: The amount withheld for Medicare tax goes in box 6.

- Include tips: Fill in box 7 with any social security tips received.

- Indicate allocated tips: If applicable, write in box 8 the allocated tips.

- Complete control number: If your employer assigns a control number, enter it in box d.

- Report dependent care benefits: In box 10, provide any dependent care benefits received.

- Enter your name: Fill in box e with your first name, middle initial, last name, and suffix (if any).

- Provide your address: In box f, write your address and ZIP code.

- Insert state information: If applicable, fill in your employer’s state ID number in box 15.

- Report state wages and taxes: In boxes 16 and 17, enter your state wages and state income tax withheld, respectively.

- Document local wages and income tax: If applicable, fill in boxes 18 and 19 with local wages and local income tax, respectively, and specify the locality in box 20.

Once completed, ensure that you keep a copy for your records and provide copies as required for tax filing. If any mistakes are found after submission, a corrected W-2, known as Form W-2c, will need to be filed to rectify the errors.

What You Should Know About This Form

What is the Circle K W2 form?

The Circle K W2 form is a wage and tax statement that employers use to report an employee's annual wages and the taxes withheld from their paycheck. It is essential for employees to accurately file their income tax returns. The form includes various details such as the employer’s identification number, employee's social security number, wages earned, and the amount of federal, state, and local taxes withheld. Each employee typically receives a copy from their employer at the end of the tax year.

How can I file the Circle K W2 form electronically?

To file Forms W-2 and W-3 electronically, employers can visit the Social Security Administration’s (SSA) Employer W-2 Filing Instructions web page. Here, they can also create fill-in versions of Forms W-2 and W-3 to file with the SSA. This is a safe option that aids in ensuring compliance with federal requirements while avoiding common errors associated with paper filing.

What should I do if my W2 form contains incorrect information?

If there are any inaccuracies on your W2 form, such as incorrect name, social security number (SSN), or address, you should correct Copies B, C, and 2 of the form. Additionally, you must ask your employer to amend the records and file Form W-2c, which is the Corrected Wage and Tax Statement, with the SSA. Be sure to retain a copy of the corrected form to include with your tax return.

Is the online version of the W2 form scannable?

No, the online version of the W2 form, if printed directly from a website, is not scannable. Only the official printed version of the form provided by the IRS is scannable. If the online form is filed incorrectly, a penalty may be imposed. Therefore, it is advisable to order the official IRS forms for accurate filing.

What is reported in Box 12 of the W2?

Box 12 of the W2 form reports additional information such as the cost of employer-sponsored health coverage, nonqualified plans, and retirement plan contributions. This information is provided strictly for the employee's knowledge and is not taxable. Employees should review this box to understand their benefits better.

How can I obtain a copy of the official W2 form for filing?

To acquire an official W2 form, employers can visit the IRS's Online Ordering for Information Returns page. This allows them to order the necessary scannable forms for accurate filing. It is recommended that this process be completed well before tax season to ensure timely receipt of the documents needed for tax return preparation.

Common mistakes

Filling out the Circle K W2 form correctly is essential for accurate tax reporting. However, many individuals encounter common mistakes that can lead to complications. One common error involves incorrectly entering the Employee’s Social Security Number. This number should always be accurate, as it’s critical for the IRS to match the income reported with each employee properly. Double-checking this number can prevent delays in the processing of tax returns.

Another frequent mistake is failing to include the Employer Identification Number (EIN). This number uniquely identifies the employer and must be reported accurately on the form. If an employee tries to file with an incorrect EIN, it could result in significant confusion and potential issues with the IRS. The EIN can typically be found on other tax documents from the employer, so it’s important to cross-reference this information.

People also make the mistake of not reporting wages, tips, or other compensation accurately. This line captures all taxable income, including bonuses or any additional earnings from side jobs. Any discrepancies could lead to audits or fines. It's advisable to refer to pay stubs to ensure this information matches the reported earnings.

Additionally, the section for Federal income tax withheld is often filled out incorrectly. Misunderstandings about how much tax should have been withheld can result in an inaccurate tax return. Employees should consult their pay stubs and withholding documentation to confirm they are entering the correct amounts.

Another common issue is neglect in completing the state and local income tax sections. These segments are vital for individuals who live in states with income taxes. Failing to include or correctly report these amounts can alter the overall tax liability and lead to underpayment penalties.

Lastly, many individuals overlook the importance of correcting any errors. If any mistakes are identified after filing, failing to submit a corrected form can lead to complications. Employers should file a Form W-2c, Corrected Wage and Tax Statement, to resolve any discrepancies. This should be done as soon as the error is identified to prevent issues with the IRS or potential delays with tax refunds.

Documents used along the form

In addition to the Circle K W-2 form, various forms and documents are often utilized during tax preparation and reporting. Each of these documents serves a specific purpose, assisting individuals and businesses in fulfilling their tax obligations efficiently and accurately.

- Form 1040: This is the individual income tax return form used by taxpayers to report their annual income, claim deductions, and calculate taxes owed or refund due.

- Form W-3: This form is a summary of all W-2 forms issued by an employer. It is submitted to the Social Security Administration (SSA) along with the W-2 forms, providing a total for withheld taxes and earnings.

- Form 1099-MISC: Used to report payments made to contractors and freelancers. It includes details on income paid outside of regular employee wages.

- Form 945: This is the annual return used to report nonpayroll withholding, including backup withholding and withholding on certain payments made to non-employees.

- Form 1040-SR: This simplified version of Form 1040 is designed for senior taxpayers (aged 65 and older) and features larger type and a straightforward layout.

- Schedule C: This form details income and expenses for self-employed individuals, allowing them to report business earnings and expenses when filing their taxes.

- Form W-2c: The Corrected Wage and Tax Statement, used to correct errors made in a previously filed W-2 form, ensuring accurate reporting to the SSA and the employee.

- Form 8862: This form is required for taxpayers who have previously had their claim for the Earned Income Tax Credit (EITC) denied and wish to claim it again in a subsequent year.

These documents assist taxpayers in various aspects of income reporting and compliance with tax laws. Gather these forms promptly to ensure an efficient tax filing process.

Similar forms

- Form 1099-MISC: Similar to the W-2, this form reports income for non-employees. Businesses use it to report payments made to contractors, freelancers, and other non-employees. Both forms provide important tax information but cater to different types of income recipients.

- Form 1099-NEC: This form specifically reports non-employee compensation. It replaces the 1099-MISC for reporting payments to independent contractors. Like the W-2, it is used to report income but differs in the types of earnings reported.

- Form 1040: The individual tax return form that taxpayers file with the IRS. While the W-2 provides information about earned income, the 1040 is the form where individuals report total income and calculate their tax liability.

- Form W-3: This is a summary form that accompanies the W-2. Employers submit it to the Social Security Administration (SSA) alongside W-2 forms to confirm the total earnings and tax information reported for all employees.

- Form 941: The employer's quarterly tax return. This form reports the amounts withheld for Social Security, Medicare, and federal income tax for employees. It complements the W-2, which reports these amounts annually to employees and the IRS.

- Form W-4: This form informs your employer about how much federal income tax to withhold from your paycheck. While the W-2 shows the total tax withheld at year's end, the W-4 is filled out at the beginning of employment and can be adjusted as necessary.

Dos and Don'ts

When filling out the Circle K W2 form, it’s crucial to be mindful of certain best practices and potential pitfalls. Here’s a helpful guide to what you should and shouldn’t do:

- Do ensure that you accurately fill in your name, Social Security Number (SSN), and address as they appear on your documents.

- Don’t use the Copy A downloaded from the website for filing with the SSA, as it is not scannable and may lead to penalties.

- Do print and file the official W-2 form to avoid any issues with the IRS or SSA.

- Don’t forget to include all relevant wages, tips, and other compensation in the appropriate boxes.

- Do check the accuracy of your employer’s information, including the Employer Identification Number (EIN).

- Don’t leave any required fields blank; this may result in processing delays or errors.

- Do keep a copy of your completed form for your own records and potential future reference.

- Don’t hesitate to ask your employer for help if you encounter any discrepancies or questions during the completion process.

Following these guidelines will help ensure a smoother filing experience.

Misconceptions

Misconception 1: The W-2 form is only for federal tax purposes.

This is incorrect. While the W-2 form is essential for federal tax filings, it is also necessary for state and local tax reporting. Employees need various copies of the W-2, including those for state and local tax departments, to ensure compliance with tax laws.

Misconception 2: Copy A of the W-2 can be printed from any source for filing.

This statement is misleading. Copy A is specifically designed to be filed with the Social Security Administration (SSA) in its official printed version. The downloadable version from online sources is not scannable and should not be filed. Using this version can lead to penalties.

Misconception 3: Employees do not need to keep copies of their W-2 forms.

This is not true. Employees should retain copies of their W-2 forms for their personal records. Keeping copies can be beneficial for future tax filings, eligibility for claims, and resolving any discrepancies that may arise.

Misconception 4: The W-2 form does not influence tax refunds or credits.

This misconception overlooks the importance of the W-2 in tax calculations. The information reported on the W-2 can determine eligibility for various tax credits, such as the Earned Income Credit (EIC). Even if you do not have to file a tax return, you might still qualify for a refund based on the withholding shown on the W-2.

Key takeaways

Understanding the Circle K W2 form is essential for both employers and employees to manage tax obligations effectively. Here are six key takeaways to consider:

- Filing Options: Employers can file Forms W-2 and W-3 electronically through the Social Security Administration’s website. This option is efficient and helps ensure accuracy.

- Copy A Details: Copy A of the W2 is intended strictly for informational purposes. Do not file this copy with the SSA if downloaded; only use the official printed version, which is designed to be scannable.

- Distribution Requirements: Copies B and others may be downloaded, filled out, and provided to employees. These copies fulfill the requirement of giving recipients their wage and tax information.

- Correcting Errors: If there are mistakes in personal information or earnings, employees should correct Copies B, C, and 2 and request their employer file a Form W-2c to amend records with the SSA.

- EIC Eligibility: Employees may qualify for the Earned Income Credit (EIC) based on adjusted gross income. Those who are eligible might receive a refund even if they do not need to file a tax return.

- Health Coverage Reporting: Box 12 of the form can show the cost of employer-sponsored health coverage. This amount isn’t taxable, but it is important information for employees.

Being well-informed about the Circle K W2 form will help you navigate tax season with greater ease and confidence.

Browse Other Templates

How Much Does Altcs Pay for Assisted Living - Include contact information such as phone number and email address.

Stoichiometry Review Worksheet - The key provides immediate feedback, promoting learning through correction.