Fill Out Your Dwp Budgeting Loan Application Form

Applying for a Budgeting Loan can be a vital step for those requiring financial support in managing essential expenses. This loan can help individuals cover costs such as furniture, household equipment, clothing, or even rent in advance. Understanding the application process is essential, and it starts with the DWP Budgeting Loan Application form. Each applicant must be receiving certain benefits for at least 26 weeks to qualify, such as Income Support or Pension Credit. Within the form, you will specify your personal information, including your living situation and any dependents. It’s crucial to note that the maximum loan varies based on whether you are single or a parent, with set limits: up to £348 for singles, £464 for couples without children, and £812 for families with children. Importantly, you must not have existing debts exceeding £1,500 with the Social Fund to qualify for a new loan. Another key factor is savings; having over £1,000 can affect your loan amount if you are under 63 years old. The form also outlines how to repay the loan through small weekly deductions from your benefit payments, ensuring that repayments are manageable. By thoroughly understanding and filling out this application correctly, you can secure the financial assistance you need to relieve some of the burdens of daily living.

Dwp Budgeting Loan Application Example

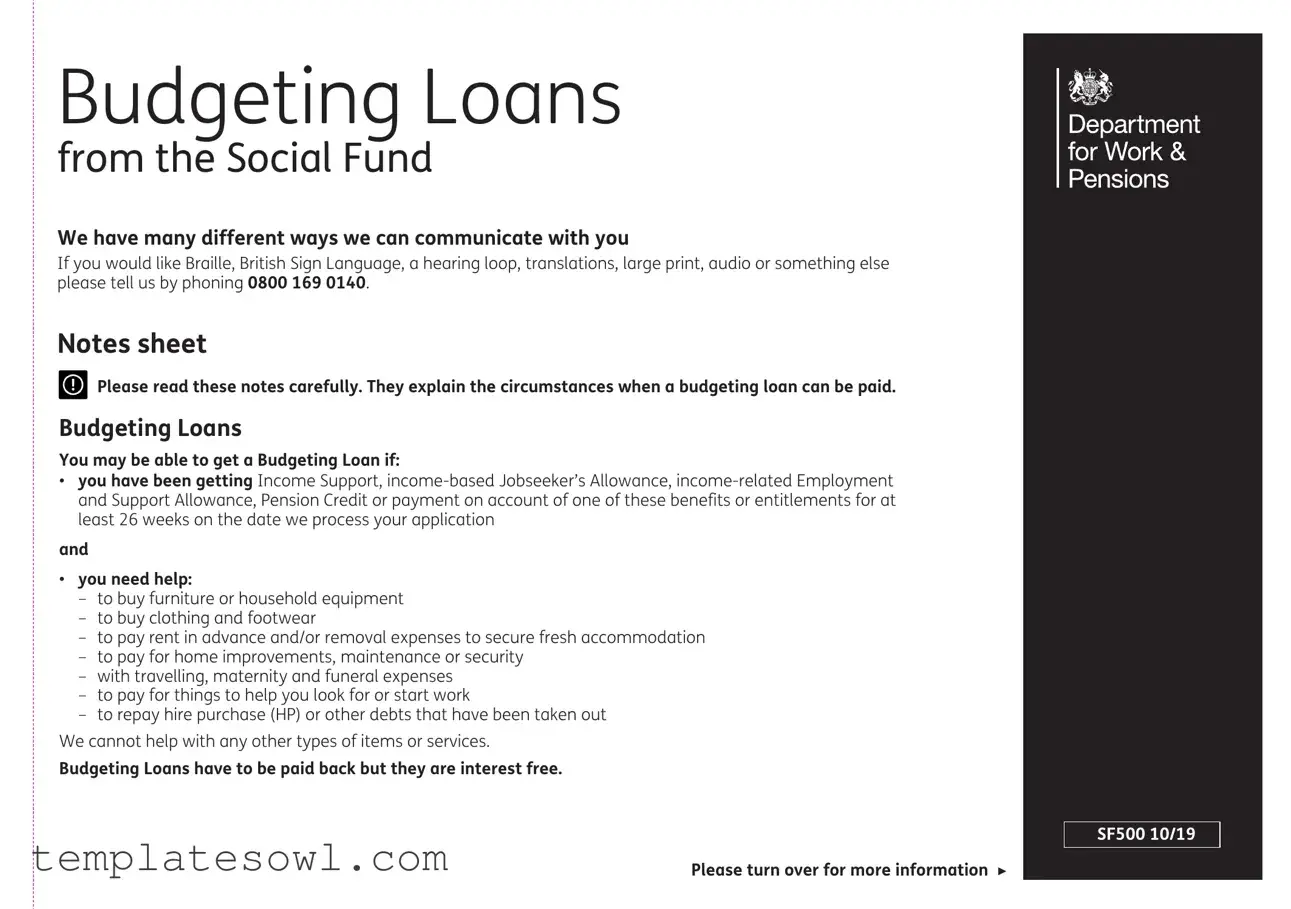

Budgeting Loans

from the Social Fund

We have many different ways we can communicate with you

If you would like Braille, British Sign Language, a hearing loop, translations, large print, audio or something else please tell us by phoning 0800 169 0140.

Notes sheet

Please read these notes carefully. They explain the circumstances when a budgeting loan can be paid.

Please read these notes carefully. They explain the circumstances when a budgeting loan can be paid.

Budgeting Loans

You may be able to get a Budgeting Loan if:

•you have been getting Income Support,

and

•you need help:

–to buy furniture or household equipment

–to buy clothing and footwear

–to pay rent in advance and/or removal expenses to secure fresh accommodation

–to pay for home improvements, maintenance or security

–with travelling, maternity and funeral expenses

–to pay for things to help you look for or start work

–to repay hire purchase (HP) or other debts that have been taken out

We cannot help with any other types of items or services.

Budgeting Loans have to be paid back but they are interest free.

SF500 10/19

Please turn over for more information ▶

Notes

You can have one of three rates of Budgeting Loan. The amount depends on whether you are single, a couple without children or qualifying young persons, or a one or two parent family with children or qualifying young persons. For a single person the maximum rate is £348, for a couple without children or qualifying young persons the maximum rate is £464, and for one or two parent families with children the maximum rate is £812. We cannot pay you more than these amounts.

The amount of Budgeting Loan you can have also depends on whether you still have any other Budgeting Loans or Crisis Loans you have not paid back to the Social Fund. We cannot make a payment for a loan if you already owe £1,500 or more to the Social Fund for any previous Crisis Loans or Budgeting Loans combined.

Savings

•If you and your partner are aged under 63, savings of more than £1,000 may affect the amount of money you can get.

•If you or your partner are aged 63 or over, savings of more than £2,000 may affect the amount of money you can get.

We cannot make a payment for a loan if you already owe £1,500 or more to the Social Fund.

We cannot pay a Budgeting Loan for expenses of less than £100.

How we decide what we can pay you

The decision maker will look at the relevant circumstances and decide the maximum size of Budgeting Loan you can have, if you have no existing Social Fund debt. Whether or not you can have a loan of up to that amount will depend on if you already have a budgeting loan debt.

How you pay back a loan

•We will look at what you can afford before we decide on the arrangements for repayments.

•If we can pay you a Budgeting Loan, we may make you up to three different offers. It will be up to you which of these offers you can afford to pay back. We may not be able to lower the repayment rate if you later feel

you cannot afford the rate you originally agree to.

•If we can pay you a Budgeting Loan, we will ask you to agree to repay it and also to agree the way you will repay it before we make the payment.

•We will take the money back in weekly repayments from your benefit. If you or your partner do not get any benefit, we will arrange for the loan to be repaid in another way.

•If you have problems later on making the repayments as originally agreed, we may be able to help, for example reducing your payments by extending the repayment period. Your local jobcentre can give you advice.

Help and advice

If you want more information:

•get in touch with Jobcentre Plus, phone 0800 169 0140. You can also get more information from www.gov.uk

or

•get in touch with an advice centre like Citizens Advice

We use partner to mean:

•a person you live with who is your husband, wife or civil partner, or

•a person you live with as if you are a married couple

We use child to mean a person aged under 16 who is living with you and you are getting Child Benefit for.

We use qualifying young person to mean a person aged 16, 17, 18 or 19 who is living with you, who you are getting Child Benefit for.

These notes give general guidance only and should not be treated as a complete and authoritative statement of the law.

Tear off this page to keep for your information ▶

Part 1: About you and your partner

•Before you complete this form, please read the notes sheet which tells you about all types of help you can get from the Social Fund.

•Use this form to apply for a Budgeting Loan. Sign and date any alterations you make.

•If you are getting Income Support,

•Tell us about yourself and your partner, if you have one. We use partner to mean:

–a person you are married to or a person you live with as if you are married to them, or

–a civil partner or a person you live with as if you are civil partners

•Fill in the form fully by answering all the questions and requests for information. Your application may be delayed if we do not have all the information we need.

•Please fill in this form with BLACK INK and in CAPITALS.

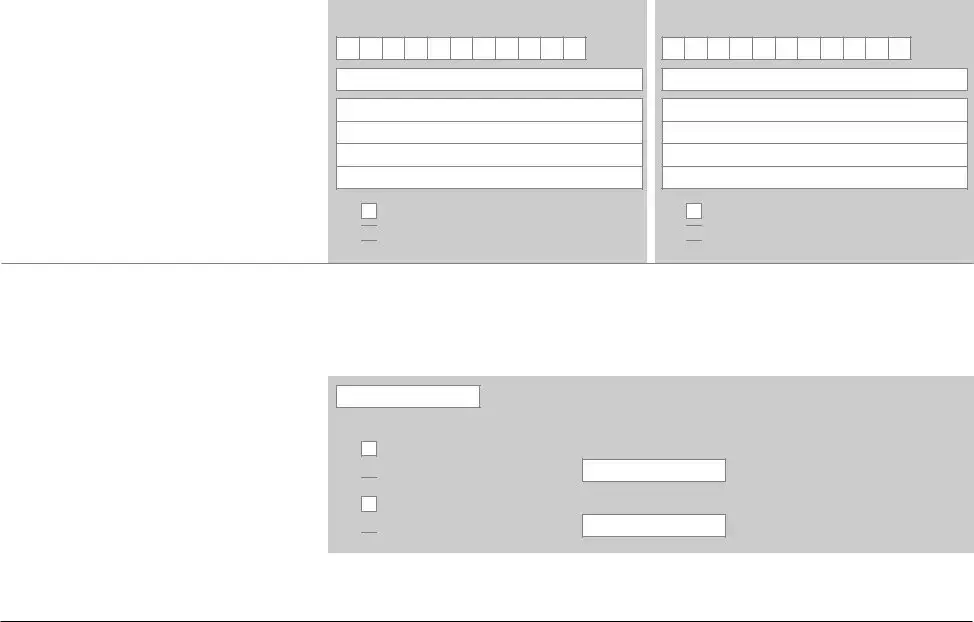

National Insurance (NI) number

Surname or family name

Any other surnames or family names you have been known by

All other names, in full

Date of birth

Daytime phone number

We may need to contact you by phone to ask for further information, or when we have made a decision on your application. Please note that the number may display as an 0800, unknown or witheld number.

You |

|

|

|

|

|

|

|

|

Your partner |

|

|

|

|

|

|

|

|

||||||||||

Letters Numbers |

|

|

|

|

|

|

Letter |

Letters Numbers |

|

|

|

|

|

Letter |

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

You can find the number on a National Insurance (NI) numbercard, letters about benefit, or payslips.

Mr/Mrs/Miss/Ms |

|

Mr/Mrs/Miss/Ms |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

/ |

/ |

|

|

/ |

/ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

SF500 10/19 |

Part 1: About you and your partner continued

Mobile phone number, if you have one

Email address, if you have one

Address where you live now

Please tell us your current address, and your partner’s current address, if it is different.

Are you or your partner involved in a trade dispute? We use trade dispute to mean a strike,

You

Postcode

No

Yes

Your partner

Postcode

No

Yes

Part 2: About your children or qualifying young persons

•We use child to mean a person aged under 16 who you are getting Child Benefit for.

•We use qualifying young person to mean a person aged 16, 17, 18 or 19 who you are getting Child Benefit for.

How many children or qualifying young persons are in your household?

Are you getting Child Tax Credit for your children or qualifying young persons?

Are you getting Child Benefit for your children or qualifying young persons?

No

Yes

How much do you get a week?

How much do you get a week?

No

Yes

How much do you get a week?

How much do you get a week?

£

£

SF500 10/19 |

2 |

Part 3: About what you need

Budgeting Loans can only be given for the types of items or services listed in this part.

Please enter the total amount you need in the Total amount applied for box.

Please refer to the notes sheets for the maximum rates of Budgeting Loans depending on your circumstances.

Total amount applied for |

£ |

What items are you applying for?

Please tick the box (or boxes) that apply to you. Furniture and household equipment

Clothing and footwear

Rent in advance or removal expenses to secure fresh accommodation Improvement, maintenance and security of the home

Travelling expenses within the UK

Expenses associated with seeking or

Maternity expenses

Funeral expenses

Repaying Hire Purchase and other debts – for any items or expenses which are associated with the categories above

3 |

SF500 10/19 |

Part 4: About benefits and entitlements

Are you or your partner currently getting Income Support,

No  Yes

Yes

Go to Part 8.

Tell us which benefits or entitlements you are getting.

Income Support

Jobseeker’s Allowance

Employment and Support Allowance (income related)

Pension Credit

Has a partner or an

•Income Support

•

•

•Pension Credit, or

•payment on account of one of these benefits or entitlements

for you, in the last 26 weeks?

No

Yes

Tell us about this person:

Tell us about this person:

Their name

Date of birth

Their National Insurance (NI) number Date of separation

Their address

/ /

/ /

Postcode

Have you made this claim because you have separated from someone?

No |

|

|

|

|

|

|

|

|

|

|

|

|

|

Yes |

|

Tell us about the person you have separated from: |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

Their name |

|

|

|

|

|

|

Date of birth |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

/ |

/ |

|

|

|

|

|

|

|

|

|

SF500 10/19 |

4 |

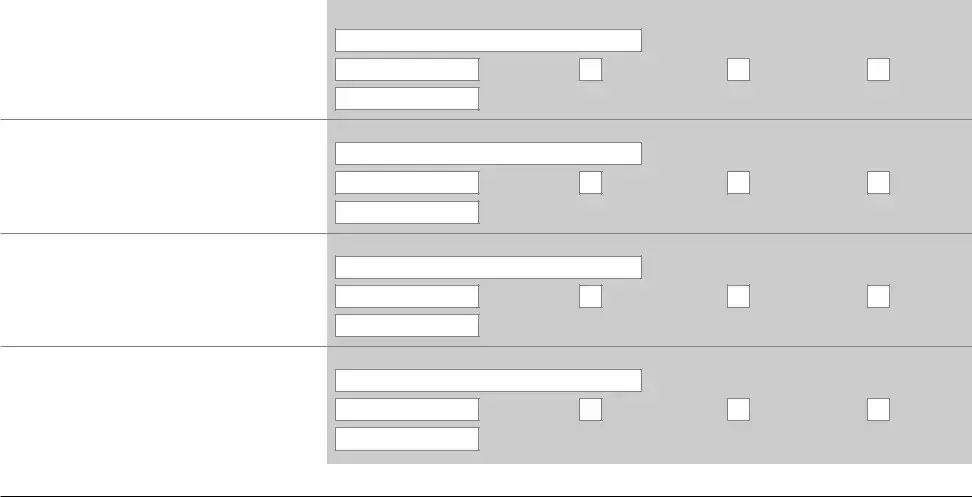

Part 5: About money you have to pay out

Please tell us about any money that you or your partner have to pay out regularly, but do not include normal living expenses like gas and electric charges or food bills.

Include things like catalogue money, hire purchase, loan payments and fines.

Please answer all the questions for each regular payment. If you do not give us all the information, we will not be able to decide this claim. The following responses will only be used to calculate your repayments if the offer of a loan is made.

Payment 1

Who do you pay the money to?

How much are you paying and how often? How much is owed?

£

£

every week

every fortnight

every month

Payment 2

Who do you pay the money to?

How much are you paying and how often? How much is owed?

£

£

every week

every fortnight

every month

Payment 3

Who do you pay the money to?

How much are you paying and how often? How much is owed?

£

£

every week

every fortnight

every month

Payment 4

Who do you pay the money to?

How much are you paying and how often? How much is owed?

£

£

every week

every fortnight

every month

5 |

SF500 10/19 |

Part 6: About your savings

Do you or your partner have any savings?

If you and your partner are both aged under 63, we may be able to disregard the first £1,000 of your savings. If either you or your partner are over 63, we may be able to disregard the first £2,000 of your savings.

Savings means any capital you and your partner have, including:

•any money you have at home, in the bank, in the building society or in a credit union account

•premium bonds

•investments, such as shares or unit trusts.

•the value of any property you or your partner own that you do not live in. For example,

a house you let out, a holiday home, or somewhere another member of your family lives

If you do not complete this part of the form your application may be delayed

No

Yes

How much savings do you have?

How much savings do you have?

£

SF500 10/19 |

6 |

Part 7: How we pay you

If you want to use the account you usually get your benefits paid into, please go straight to part 8

We normally pay your money directly into the same account as we pay your benefit into.

Many banks and building societies will let you collect your money at the Post Office.

We will tell you when your Social Fund payment will be made and how much it will be for.

Finding out how much we have paid into the account

You can check your payments on account statements. The statements may show your National Insurance (NI) number next to any payments we have made. If you think a payment is wrong, get in touch with the office that pays you straight away.

If we pay you too much money

If we pay you too much money we have the right to take back any money we pay that you are not entitled to. This may be because of the way the system works for payments into an account.

For example, you may give us some information which means you are entitled to less money. Sometimes we may not be able to change the amount we have already paid you. This means we will have paid you money that you are not entitled to.

We will contact you before we take back any money.

What to do now

•Go to Part 8, unless you want us to pay your Social Fund payment into a different account to the one we pay your benefit into.

•If you want us to pay your Social Fund payment into a different account, tell us about this on the next page. By giving us these account details you:

–agree that we will pay you into this account, and

–understand what we have told you above in the section If we pay you too much money

•If you are going to open an account, please tell us your account details as soon as you get them.

•If you do not have an account, and do not intend to open one, please tick this box and we will contact you.

Fill in the rest of this form. You do not have to wait until you have opened an account or contacted us.

7 |

SF500 10/19 |

Part 7: How we pay you continued

If you want to use a different account, please tell us about the account you want to use for this payment

•You can use an account in your name, or a joint account.

•You can use someone else’s account if:

–the terms and conditions of their account allow this

–they agree to let you use their account, and

–you are sure they will use your money in the way you tell them.

•You can use a credit union account. You must tell us the credit union’s account details. Your credit union will be able to help you with this.

•If you are an appointee or a legal representative acting on behalf of the claimant, the account should be in your name only.

Please tell us your account details below.

It is very important you fill in all the boxes correctly, including the building society roll or reference number, if you have one. If you tell us the wrong account details your payment may be delayed or you may lose money.

You can find the account details on your chequebook or bank statements. If you do not know the account details, ask the bank or building society.

Name of the account holder

Please write the name of the account holder exactly as it is shown on the chequebook or statement.

Full name of bank or building society

Sort code

Please tell us all 6 numbers, for example:

Account number

Most account numbers are 8 numbers long. If your account number has fewer than 10 numbers, please fill in the numbers from the left.

Building society roll or reference number

If you are using a building society account you may need to tell us a roll or reference number. This may be made up of letters and numbers, and may be up to 18 characters long. If you are not sure if the account has a roll or reference number, ask the building society.

You may get other benefits and entitlements we do not pay into an account. If you want us to pay them into the above account, please tick this box.

SF500 10/19 |

8 |

Form Characteristics

| Fact Name | Details |

|---|---|

| Eligibility Requirements | Applicants must have received Income Support, income-based Jobseeker’s Allowance, income-related Employment and Support Allowance, or Pension Credit for at least 26 weeks at the time of application processing. |

| Types of Expenses Covered | Budgeting Loans can assist with furniture, clothing, rent in advance, home improvements, travel, maternity, funeral costs, starting work, and repaying debts. |

| Maximum Loan Amounts | The maximum loan is £348 for singles, £464 for couples without children, and £812 for families with children or qualifying young persons. |

| Existing Debt Limit | Applicants cannot owe more than £1,500 combined from previous Crisis Loans or Budgeting Loans from the Social Fund. |

| Impact of Savings | If aged under 63, savings over £1,000 may affect loan eligibility. Those 63 or older may have their eligibility impacted by savings exceeding £2,000. |

| Minimum Loan Amount | Budgeting Loans cannot be issued for less than £100. |

| Repayment Plans | Repayments are typically deducted weekly from benefits, with options for up to three repayment offers based on what the borrower can afford. |

| Contact Information | For assistance, applicants can call 0800 169 0140 or visit www.gov.uk for further resources. |

| Definition of Partner and Child | A partner is defined as someone you live with in a relationship akin to marriage. A child is someone under 16 for whom you receive Child Benefit. |

| Form Completion Guidelines | The application must be filled out fully in black ink and capital letters to avoid delays in processing. |

Guidelines on Utilizing Dwp Budgeting Loan Application

Completing the DWP Budgeting Loan Application form is an important step toward acquiring financial assistance when you need it. To ensure that you are fully prepared and that the information you provide is complete, follow these step-by-step instructions carefully. This will help expedite the application process and avoid potential delays.

- Gather all required personal information, including your name, address, date of birth, and National Insurance number.

- Use black ink and capital letters to fill out the form clearly. This will ensure legibility and help prevent misunderstandings.

- In part 1, indicate whether you or your partner is involved in a trade dispute. Select "Yes" or "No" as appropriate.

- Provide details about your current address, including the postcode. If your partner resides at a different address, include that as well.

- In part 2, list the number of children or qualifying young persons in your household. Specifically define these terms as needed, based on the child's age and benefits received.

- Answer questions regarding Child Tax Credit and Child Benefit, stating the amounts you receive weekly.

- Move to part 3, where you will detail the types of aid you seek. Determine the total amount you are applying for and provide that figure in the specified box.

- Tick the appropriate boxes for the items or services for which you are requesting financial help, ensuring that your selections align with the guidelines provided in the notes.

- Review the entire form for completeness and accuracy. Corrections should be signed and dated, if necessary.

- Submit your application via the designated method, either by mail or in person, ensuring it reaches the appropriate office.

After submission, the next steps will involve a review of your application. Decisions will be made based on the information provided, and you may be contacted for further details if necessary. It's crucial to keep a copy of your application for your records and refer to the contact information provided should you need assistance or updates regarding your application status.

What You Should Know About This Form

What is a Budgeting Loan?

A Budgeting Loan is a type of interest-free financial assistance provided by the Social Fund to help individuals cover necessary expenses. These loans are intended for those who have been receiving certain benefits, such as Income Support or Pension Credit, for at least 26 weeks. The funds can be used for various purposes, including purchasing furniture, clothing, paying rent in advance, and managing other essential costs.

Who is eligible to apply for a Budgeting Loan?

Eligibility for a Budgeting Loan generally requires you to have been receiving specific benefits for at least 26 weeks. This includes Income Support, income-based Jobseeker’s Allowance, income-related Employment and Support Allowance, and Pension Credit. Additionally, you should demonstrate a need for help with necessary expenses as outlined in the application form.

What types of expenses can a Budgeting Loan cover?

Budgeting Loans can assist with a variety of necessary expenses, including:

- Furniture and household equipment

- Clothing and footwear

- Rent in advance or removal expenses

- Home improvements, maintenance or security

- Traveling expenses within the UK

- Expenses related to seeking or re-entering work

- Maternity and funeral expenses

- Repaying hire purchase and other debts associated with these categories

How is the amount of the Budgeting Loan determined?

The maximum loan amount varies based on your household composition. For a single person, the maximum is £348; for a couple without children, it is £464; and for one or two parents with children, it may be up to £812. Your current savings and any outstanding loans from the Social Fund may also influence the total amount you can receive.

How do I repay the Budgeting Loan?

Loan repayments are typically deducted from your benefits in weekly installments. Before the loan is approved, the decision maker will assess what you can afford. You may be presented with different repayment options, and you must agree to the chosen arrangement before disbursement of the funds. If you encounter difficulties later, adjustments to the repayment schedule may be possible.

What happens if I already owe money to the Social Fund?

If you currently owe £1,500 or more to the Social Fund through previous loans, you won't qualify for a new Budgeting Loan. Additionally, if you have outstanding Crisis Loans or Budgeting Loans that have not been repaid, this will affect your eligibility and the amount available to you.

How can I get help or further information regarding my application?

If you need additional guidance, you can contact Jobcentre Plus at 0800 169 0140 or visit their website at www.gov.uk. Local advice centers, such as Citizens Advice, are also valuable resources for assistance with your Budgeting Loan application.

Common mistakes

Completing the DWP Budgeting Loan Application form is an important step for many individuals seeking financial assistance. However, simple mistakes can delay the process or cause misunderstandings. Awareness of common pitfalls can help applicants avoid frustration.

One frequent error occurs when applicants fail to read the accompanying notes thoroughly. These notes provide crucial information regarding eligibility and guidelines for assistance. When individuals skip over this important context, they may find themselves applying for loans for ineligible expenses or missing key details about repayment terms.

An omission in providing personal information is another area where mistakes happen. It's vital to fill out every section completely, including personal identification details and information about your partner if applicable. Inadequate information can lead to delays or the rejection of the application.

Additionally, using the wrong pen color or font style is a surprisingly common mistake. The instructions specify filling out the form with black ink and using capital letters. Ignoring these guidelines may result in the form being deemed illegible or unprofessional, which could adversely affect the application.

Some applicants underestimate the significance of accurately reporting their savings. Misunderstanding how savings affect their eligibility can lead to complications later on. It’s essential to provide truthful figures, especially since both the amount saved and the age of the applicants can influence potential loan approval.

Not checking for existing loans from the Social Fund ranks high on the mistake list. Applicants should know their current financial obligations. If they owe over £1,500 to the Social Fund from previous loans, their application for additional assistance will be denied automatically.

Another mistake involves providing unclear or incomplete expenditure details. It's critical to specify the reasons for the loan request clearly. Vague explanations may confuse the decision-makers and result in a less favorable assessment of the application.

Failing to update contact information is another misstep. If the daytime or mobile phone number changes, it’s important to inform the DWP promptly. This ensures that communication remains seamless, especially if the department needs further details to process the application.

Some applicants also skip the part where they need to sign and date any alterations made on the form. Such signatures are necessary for the authenticity of the information provided. Failing to date changes can lead to further delays and questions about the application.

Lastly, overlooking the necessity to consult local job centers or advisory services can hinder the application process. Seeking assistance from resources such as Citizens Advice can provide valuable insights and clarify doubts. Accessibility to professional guidance can improve the chances of a successful application.

Documents used along the form

The DWP Budgeting Loan Application form is a crucial step for individuals seeking financial aid through the Social Fund. Along with this application form, several other documents may support the process, providing necessary information about personal circumstances that can influence loan eligibility. Here’s a list of other forms and documents that are often used in conjunction with the Budgeting Loan Application.

- Income Support Statement: This document shows the current amount of Income Support received by the applicant, necessary to demonstrate eligibility based on income criteria.

- Jobseeker's Allowance Claim Form: It provides detailed information regarding the applicant's jobseeking efforts and financial situation, assisting in the verification process for loans.

- Benefit Entitlement Letter: Issued by the DWP, this letter confirms the various benefits the applicant receives, essential for understanding their financial standing.

- National Insurance Number Evidence: Any official letter containing the applicant's National Insurance number proves residency and can facilitate verification of benefits.

- Proof of Income: Recent pay slips or bank statements can provide details about current earnings, vital for assessing financial need.

- Details of Existing Debts: Documentation outlining any outstanding debts helps determine the applicant's financial obligations and repayment capacity.

- Housing Benefit Claim Form: If applicable, this form outlines the housing situation, necessary for assessing housing-related applications for budgeting loans.

- Child Benefit Documentation: Any record of receiving Child Benefit is crucial for families, as it affects the amount of Budgeting Loan available.

- Expense Justification Documentation: Receipts or estimates for expenses related to the application, like moving costs or home improvements, provide clarity about requested funds.

- Social Fund Application Guidelines: A summary of the guidelines offers applicants a comprehensive understanding of what items or services their loans can cover, aiding in the completion process.

Assembling the relevant documentation alongside the DWP Budgeting Loan Application ensures a smoother and likely more successful application process. Proper preparation can make a significant difference in obtaining the necessary support during challenging times.

Similar forms

Personal Loan Application Form: This document serves a similar purpose by allowing individuals to request a loan from a financial institution. Like the DWP Budgeting Loan, it requires personal information and reasons for borrowing, and it also involves a repayment plan.

Housing Benefit Application Form: This form is used to apply for financial support towards housing costs. It shares similarities in that it collects personal information and assesses eligibility based on specific criteria, such as income and living conditions.

Universal Credit Application Form: This form is for individuals seeking Universal Credit, which combines several benefits into one payment. It also assesses the applicant’s financial situation and living circumstances, resembling the Budgeting Loan’s structure.

Disability Living Allowance Application Form: This document is used to claim financial assistance for those with disability needs. Similar to the Budgeting Loan, it requires details about the applicant’s situation and expenses related to their condition.

Food Bank Voucher Request: Individuals can use this document to seek immediate food assistance. It typically asks for personal details and reasons for need, much like the Budgeting Loan’s request for justification of expenses.

Crisis Loan Application Form: Like the Budgeting Loan, this form is for urgent financial support in times of crisis. Both documents require comprehensive information about financial circumstances and eligibility criteria.

Social Security Disability Insurance Application: This form is designed for those seeking benefits after a disabling condition. It evaluates current incomes and living situations, paralleling the Budgeting Loan’s assessments.

Veteran’s Benefits Application: Veterans can apply for funds through this process. Information regarding personal and financial status is collected, similar to the approach taken in the Budgeting Loan Application.

Emergency Assistance Fund Application: This form is used to request urgent financial help, often from charities or local governments. It may also require income information and demonstrates a similar focus on immediate financial needs.

Child Tax Credit Application Form: Families use this form to assess their eligibility for child-related tax support. Both this and the Budgeting Loan require information about family circumstances to determine eligibility.

Dos and Don'ts

When filling out the DWP Budgeting Loan Application form, it is important to take certain steps to ensure your application is processed smoothly. Below are four dos and don'ts to consider.

- Do read all instructions carefully. Ensure that you understand the eligibility requirements and the information needed to complete the form.

- Do provide complete and accurate information. Fill in all sections of the form. Incomplete applications can lead to delays.

- Do use black ink and capital letters. This helps to ensure that your application is legible and easy to process.

- Do keep a copy of your application. It’s useful to have a reference for any future communications regarding your loan application.

- Don't rush through the application. Take your time to provide thorough responses to each question.

- Don't forget to sign and date any changes. If you make alterations to the form, it's essential to indicate that these changes are intentional.

- Don't ignore correspondence from the DWP. If they reach out for further information, respond promptly to avoid delays in processing your application.

- Don't apply for items outside the eligible categories. Ensure that the expenses you are requesting funding for fall within the guidelines provided.

Misconceptions

The following are common misconceptions regarding the DWP Budgeting Loan Application form:

- Only individuals on benefits can apply. Although the form is primarily for those receiving certain benefits, it is possible for specific exemptions to apply. Anyone experiencing financial hardship may explore alternative forms of assistance.

- Budgeting Loans are free money. While Budgeting Loans do not incur interest, they must be repaid. Understanding this is crucial to avoid future financial strain.

- There is no limit to how much you can borrow. Each application is subject to maximum limits based on individual circumstances. For example, single individuals can borrow up to £348, while families may qualify for a higher amount.

- You need perfect credit to qualify. Credit history is not a consideration for these loans. The focus is on current financial circumstances and whether the applicant meets other eligibility criteria.

- The application process is overly complicated. While necessary details must be provided, the application can be completed by following the straightforward guidelines set forth in the form. Seeking help or advice can further simplify the process.

Key takeaways

Filling out the DWP Budgeting Loan Application form can feel overwhelming, but breaking the process down into key points can ease your experience. Here are some critical takeaways to keep in mind:

- Eligibility Requirements: To qualify for a Budgeting Loan, you must have received certain benefits for at least 26 weeks before applying. Make sure you understand which benefits count towards this requirement.

- Specific Uses: The loan can only be used for specific needs such as buying furniture, covering rent in advance, or managing travel expenses. Be clear about your intended use when completing the form.

- Repayment Terms: Budgeting Loans need to be repaid, but they are interest-free. Understand that repayment will be taken directly from your benefits. Ensure you choose a repayment plan you can realistically manage.

- Keep It Complete: Fill out the form completely and accurately. Incomplete applications can lead to delays. Remember to sign any changes and use BLACK INK with CAPITAL letters.

By following these guidelines, you can move through the application process more effectively, ensuring you get the assistance you need in a timely manner.

Browse Other Templates

Free Printable Templates - Visual planning can aid in minimizing distractions.

54244 640p - This form is confidential and must be handled according to state privacy regulations regarding Social Security Numbers.

Employee Travel Request Form - Estimation of travel costs is a necessary component of the request.