Fill Out Your 1004 Form

The 1004 form, officially known as the Uniform Residential Appraisal Report, serves a crucial role in the real estate and mortgage industries. Intended primarily for lenders or clients seeking an objective assessment of a property's market value, this comprehensive document outlines key details about the subject property, such as its address, owner information, and legal description. It captures the current state and characteristics of the property, including its occupancy status, tax records, and neighborhood features. The form also addresses market conditions and comparable sales data, providing insights into recent trends. Elements like property rights, assignment type, and rehabilitation potential are examined to frame the property's value accurately. Additionally, it establishes the property’s condition and any relevant financial aspects or concessions that may apply, guiding lenders in their decision-making. The inclusion of visual inspections and detailed assessments further clarifies the property’s livability and integrity, ensuring that all stakeholders have a transparent understanding of its worth. In essence, the 1004 form acts as a vital tool for determining a property's fair market value, essential for both buyers and lenders in the real estate transaction process.

1004 Example

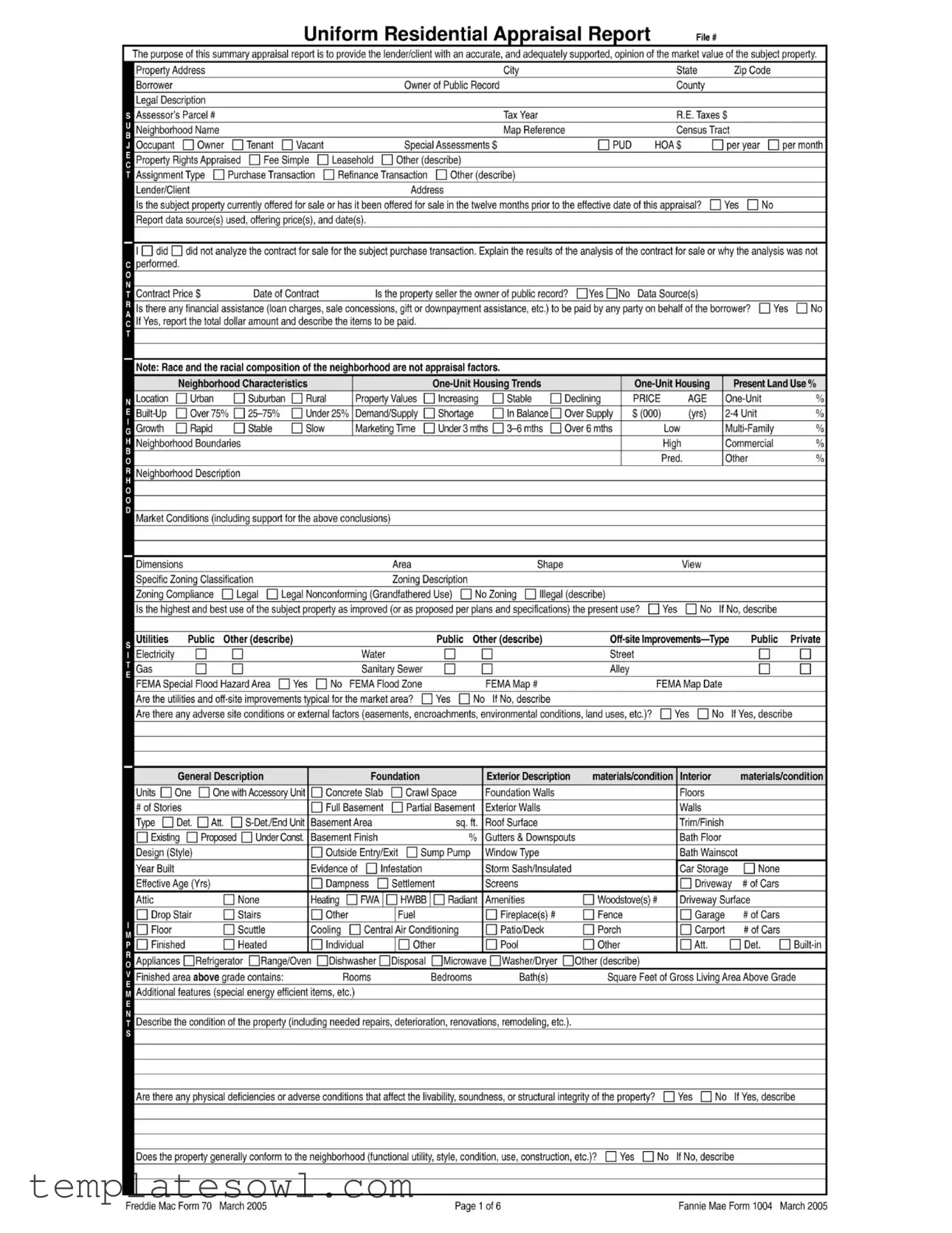

________________ Uniform Residential Appraisal Report №»_________

The purpose of this summary appraisal report is to provide the lender/client with an accurate, and adequately supported, opinion of the market value of the subject property.

Property Address |

City |

State |

Zip Code |

Borrower |

Owner of Public Record |

County |

|

Legal Description |

|

|

|

Assessor’s Parcel # |

Tax Year |

R.E. Taxes $ |

|

Neighborhood Name |

Map Reference |

Census Tract |

|

Occupant |

Owner |

|

Tenant |

Vacant |

|

Special Assessments $ |

PUD |

HOA $ |

per year |

per month |

|

Property Rights Appraised |

Fee Simple |

Leasehold |

Other (describe) |

|

|

|

|

||||

Assignment Type |

Purchase Transaction |

Refinance Transaction |

Other (describe) |

|

|

|

|

||||

Lender/Client |

|

|

|

|

|

Address |

|

|

|

|

|

Is the subject property currently offered for sale or has it been offered for sale in the twelve months prior to the effective date of this appraisal? |

Yes |

No |

|||||||||

Report data source(s) used, offering price(s), and date(s).

Il |

did |

did not analyze the contract for sale for the subject purchase transaction. Explain the results of the analysis of the contract for sale or why the analysis was not |

||||

performed. |

|

|

|

|

|

|

Contract Price $ |

Date of Contract |

Is the property seller the owner of public record? QYes QNo Data Source(s) |

|

|

||

I Is there any financial assistance (loan charges, sale concessions, gift or downpayment assistance, etc.) to be paid by any party on behalf of the borrower? |

Yes |

No |

||||

If Yes, report the total dollar amount and describe the items to be paid.

Note: Race and the racial composition of the neighborhood are not appraisal factors.

■ |

Neighborhood |

Characteristics |

|

|

Present Land Use % |

|

|||||

|

|

|

|

|

|

|

|||||

Location |

Urban |

Suburban |

Rural |

Property Values |

Increasing |

Stable |

Declining |

PRICE |

AGE |

% |

|

Over 75% |

Under 25% |

Demand/Supply |

Shortage |

In Balance |

Over Supply |

$ (000) |

(yrs) |

% |

|||

Growth |

Rapid |

Stable |

Slow |

Marketing Time |

Under 3 mths |

Over 6 mths |

|

Low |

% |

||

Neighborhood Boundaries |

|

|

|

|

|

|

|

High |

Commercial |

% |

|

|

|

|

|

|

|

|

|

|

Pred. |

Other |

% |

Neighborhood Description

Market Conditions (including support for the above conclusions)

Dimensions |

|

|

|

Area |

|

Shape |

|

|

View |

|

Specific Zoning Classification_____________________________ Zoning Description_________________________________________________________________ |

||||||||||

Zoning Compliance |

Legal |

Legal Nonconforming (Grandfathered Use) |

No Zoning |

Illegal (describe)____________________________________ |

||||||

Is the highest and best use of the subject property as improved (or as proposed per plans and specifications) the present use? |

Yes |

No If No, describe |

||||||||

Utilities |

Public |

Other (describe) |

Public |

Other (describe) |

Public Private |

|||||

Electricity |

|

|

|

Water |

|

|

Street |

|

|

|

Gas |

|

|

|

Sanitary Sewer |

|

|

Alley |

|

|

|

FEMA Special Flood Hazard Area |

Yes |

No FEMA Flood Zone |

|

|

FEMA Map# |

|

FEMA Map Date |

|

|

|||||||

Are the utilities and |

Yes |

No |

If No, describe |

|

|

|

|

|

||||||||

Are there any adverse site conditions or external factors (easements, encroachments, environmental conditions, land uses, etc.)? |

Yes |

No |

If Yes, describe |

|

||||||||||||

|

General Description |

|

|

Foundation |

|

|

Exterior Description |

materials/condition Interior |

materials/condition |

|||||||

Units |

One |

One with Accessory Unit |

Concrete Slab |

|

Crawl Space |

|

Foundation Walls |

|

Floors |

|

|

|||||

# of Stories |

|

|

|

Full Basement |

|

Partial Basement |

Exterior Walls |

|

Walls |

|

|

|||||

Type |

Det. |

Att. |

Basement Area |

|

|

sq. ft. |

Roof Surface |

|

Trim/Finish |

|

|

|||||

Existing |

Proposed |

Under Const. |

Basement Finish |

|

|

|

% |

Gutters & Downspouts |

|

Bath Floor |

|

|

||||

Design (Style) |

|

|

|

Outside Entry/Exit |

Sump Pump |

Window Type |

|

Bath Wainscot |

|

|||||||

Year Built |

|

|

|

|

Evidence of |

Infestation |

|

|

Storm Sash/lnsulated |

|

Car Storage |

None |

|

|||

Effective Age (Yrs) |

|

|

Dampness |

Settlement |

|

Screens |

|

|

Driveway |

# of Cars |

|

|||||

Attic |

|

None |

|

Heating |

FWA | |

|

HWBB | |

Radiant |

Amenities |

Woodstove(s) # |

Driveway Surface |

|

||||

Drop Stair |

Stairs |

|

Other |

|

| |

Fuel |

|

|

Fireplace(s) # |

Fence |

|

Garage |

# of Cars |

|

||

Floor |

|

Scuttle |

|

Cooling |

Central Air Conditioning |

|

Patio/Deck |

Porch |

|

Carport |

# of Cars |

|

||||

Finished |

Heated |

|

Individual |

| |

Other |

|

Pool |

Other |

|

Att. |

Det. |

|||||

Appliances |

Refrigerator |

□Range/Qven □Dishwasher □Disposal |

□Microwave □Washer/Dryer □Other (describe) |

|

|

|

|

|||||||||

Finished area above grade contains:____________ Rooms____________ Bedrooms__________Bath(s)____________ Square Feet of Gross Living Area Above Grade

Additional features (special energy efficient items, etc.)

Describe the condition of the property (including needed repairs, deterioration, renovations, remodeling, etc.).

Are there any physical deficiencies or adverse conditions that affect the livability, soundness, or structural integrity of the property? |

Yes |

No If Yes, describe |

|

Does the property generally conform to the neighborhood (functional utility, style, condition, use, construction, etc.)? |

Yes |

No If No, describe |

|

Freddie Mac Form 70 March 2005 |

Page 1 of 6 |

Fannie Mae Form 1004 March 2005 |

|

|

|

|

Uniform Residential Appraisal Report |

File# |

|

|||||||

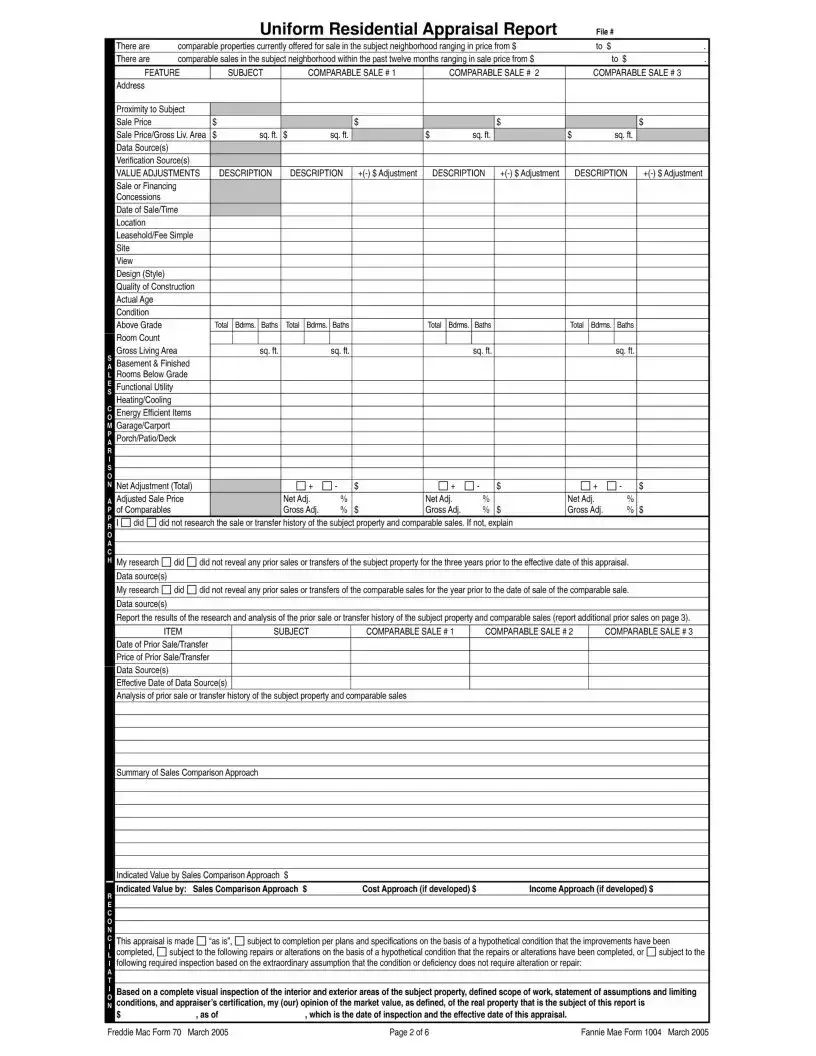

There are |

comparable properties currently offered for sale in the subject neighborhood ranging in price from $ |

to |

$ |

|

|||||||||

There are |

comparable sales in the subject neighborhood within the past twelve months ranging in sale price from $ |

|

to $ |

|

|||||||||

|

FEATURE |

| |

SUBJECT |

COMPARABLE SALE # 1 |

COMPARABLE SALE # 2 |

COMPARABLE SALE # 3 |

|||||||

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

Proximity to Subject |

|

|

|

|

|

|

|

|

|

|

|

||

Sale Price |

|

$ |

|

|

|

$ |

|

|

$ |

|

|

$ |

|

Sale Price/Gross Liv. Area $ |

sq. ft. |

$ |

sq. ft. |

|

$ |

sq. ft. |

|

$ |

sq. ft. |

|

|||

Data Source(s) |

|

|

|

|

|

|

|

|

|

|

|

||

Verification Source(s) |

|

|

|

|

|

|

|

|

|

|

|

||

VALUE ADJUSTMENTS |

DESCRIPTION |

DESCRIPTION |

DESCRIPTION |

DESCRIPTION |

|||||||||

Sale or Financing |

|

|

|

|

|

|

|

|

|

|

|

||

Concessions |

|

|

|

|

|

|

|

|

|

|

|

||

Date of Sale/Time |

|

|

|

|

|

|

|

|

|

|

|

||

Location |

|

|

|

|

|

|

|

|

|

|

|

|

|

Leasehold/Fee Simple |

|

|

|

|

|

|

|

|

|

|

|

||

Site |

|

|

|

|

|

|

|

|

|

|

|

|

|

View |

|

|

|

|

|

|

|

|

|

|

|

|

|

Design (Style) |

|

|

|

|

|

|

|

|

|

|

|

||

Quality of Construction |

|

|

|

|

|

|

|

|

|

|

|

||

Actual Age |

|

|

|

|

|

|

|

|

|

|

|

|

|

Condition |

|

|

|

|

|

|

|

|

|

|

|

|

|

Above Grade |

Total |

Bdrms. Baths |

Total Bdrms. Baths |

|

Total Bdrms. Baths |

|

Total Bdrms. Baths |

|

|||||

Room Count |

|

|

|

|

|

|

|

|

|

|

|

||

Gross Living Area |

|

sq.ft. |

|

sq. ft. |

|

|

sq.ft. |

|

|

sq. ft. |

|

||

H Basement & Finished |

|

|

|

|

|

|

|

|

|

|

|

||

N Rooms Below Grade |

|

|

|

|

|

|

|

|

|

|

|

||

Я Functional Utility |

|

|

|

|

|

|

|

|

|

|

|

||

■ Heating/Cooling |

|

|

|

|

|

|

|

|

|

|

|

||

Energy Efficient Items |

|

|

|

|

|

|

|

|

|

|

|

||

Garage/Carport |

|

|

|

|

|

|

|

|

|

|

|

||

Porch/Patio/Deck |

|

|

|

|

|

|

|

|

|

|

|

||

Net Adjustment (Total) |

|

|

+ |

□- |

$ |

+ |

□- |

$ |

+ |

□- |

$ |

||

H Adjusted Sale Price |

|

|

Net Adj. |

% |

|

Net Adj. |

% |

|

Net Adj. |

% |

|

||

Qof Comparables |

|

|

Gross Adj. |

% |

$ |

Gross Adj. |

% |

$ |

Gross Adj. |

% $ |

|||

ИI |

did |

did not research the sale or transfer history of the subject property and comparable sales. If not, explain |

|

|

|

||||||||

My research |

did |

did not reveal any prior sales or transfers of the subject property for the three years prior to the effective date of this appraisal. |

|

||||||||||

Data source(s) |

|

|

|

|

|

|

|

|

|

|

|

||

My research |

did |

did not reveal any prior sales or transfers of the comparable sales for the year prior to the date of sale of the comparable sale. |

|

||||||||||

Data source(s)

Report the results of the research and analysis of the prior sale or transfer history of the subject property and comparable sales (report additional prior sales on page 3).

ITEM |

SUBJECT |

COMPARABLE SALE # 1 |

COMPARABLE SALE #2 |

COMPARABLE SALE#3 |

Date of Prior Sale/Transfer |

|

|

|

|

Price of Prior Sale/Transfer |

|

|

|

|

Data Source(s) |

|

|

|

|

Effective Date of Data Source(s) |

|

|

|

|

Analysis of prior sale or transfer history of the subject property and comparable sales

Summary of Sales Comparison Approach

Indicated Value by Sales Comparison Approach S

Indicated Value by: Sales Comparison Approach $Cost Approach (if developed) $Income Approach (if developed) $

This appraisal is made |

“as is”, |

subject to completion per plans and specifications on the basis of a hypothetical condition that the improvements have been |

||

completed, |

subject to the following repairs or alterations on the basis of a hypothetical condition that the repairs or alterations have been completed, or |

subject to the |

||

following required inspection based on the extraordinary assumption that the condition or deficiency does not require alteration or repair:

Based on a complete visual inspection of the interior and exterior areas of the subject property, defined scope of work, statement of assumptions and limiting conditions, and appraiser’s certification, my (our) opinion of the market value, as defined, of the real property that is the subject of this report is

$ |

, as of |

, which is the date of inspection and the effective date of this appraisal. |

|

Freddie Mac Form 70 |

March 2005 |

Page 2 of 6 |

Fannie Mae Form 1004 March 2005 |

Uniform Residential Appraisal Report File#

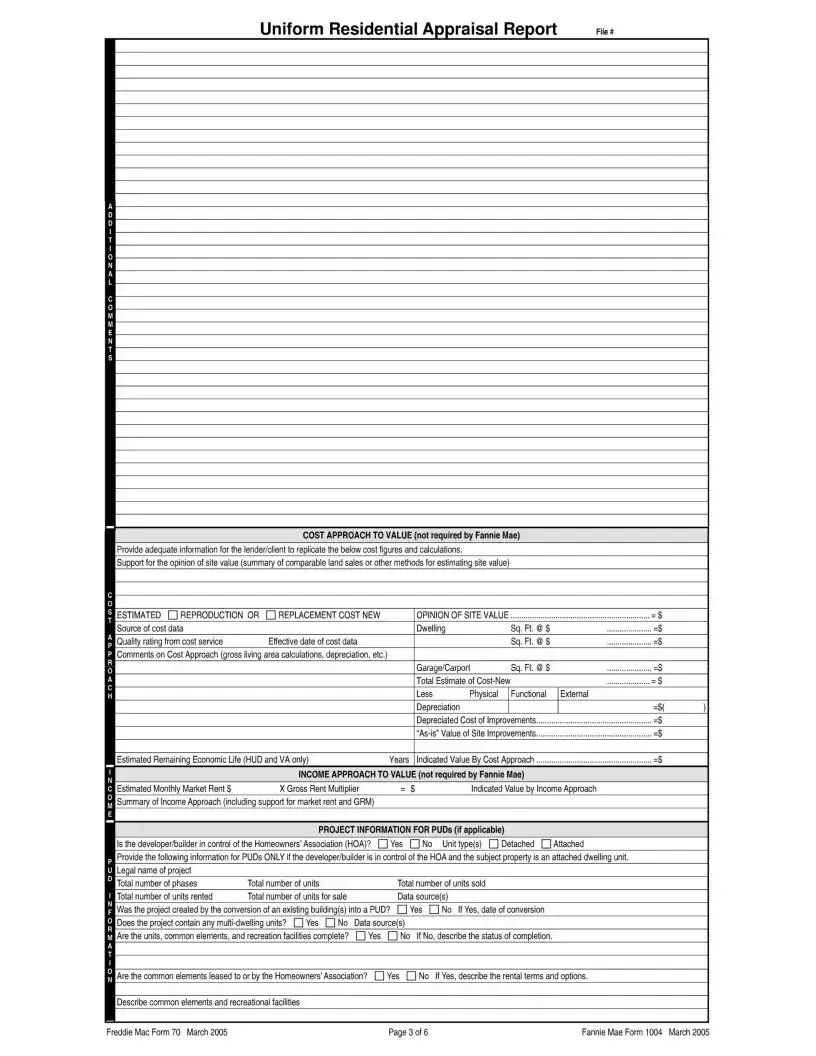

COST APPROACH TO VALUE (not required by Fannie Mae)

Provide adequate information for the lender/client to replicate the below cost figures and calculations.

Support for the opinion of site value (summary of comparable land sales or other methods for estimating site value)

ESTIMATED REPRODUCTION OR REPLACEMENT COST NEW

Source of cost data

Quality rating from cost service |

Effective date of cost data |

Comments on Cost Approach (gross living area calculations, depreciation, etc.)

Estimated Remaining Economic Life (HUD and VA only) |

Years |

OPINION OF SITE VALUE |

|

|||

Dwelling |

|

Sq. Ft. @ $ |

......................=$ |

|

|

|

Sq. Ft. @$ |

......................=$ |

|

Garage/Carport |

Sq. Ft. @ $ |

|

||

Total Estimate of |

.....................- $ |

|

||

Less |

Physical |

Functional |

External |

|

Depreciation |

|

|

=$( |

) |

Depreciated Cost of Improvements |

|

|||

|

||||

Indicated Value By Cost Approach |

|

|||

_____________________________________________INCOME APPROACH TO VALUE (not required by Fannie Mae)

[Estimated Monthly Market Rent $ |

X Gross Rent Multiplier |

= $ |

Indicated Value by Income Approach |

|

|

[Summary of Income Approach (including support for market rent and GRM)

PROJECT INFORMATION FOR PUDs (if applicable)

I Is the developer/builder in control of the Homeowners’ Association (НОА)? |

Yes |

No Unit type(s) |

Detached |

Attached |

Provide the following information for PUDs ONLY if the developer/builder is in control of the HOAand the subject property is an attached dwelling unit. [Legal name of project

[Total number of phases |

Total number of units |

|

|

Total number of units sold |

|||

|

|

|

|||||

Total number of units rented |

Total number of units for sale |

|

Data source(s) |

||||

Was the project created by the conversion of an existing building(s) into a PUD? |

Yes |

No If Yes, date of conversion |

|||||

Does the project contain any |

Yes |

No |

Data source(s)____________________________________ |

||||

Are the units, common elements, and recreation facilities complete? |

Yes |

|

No If No, describe the status of completion. |

||||

Are the common elements leased to or by the Homeowners’ Association? |

Yes |

No |

If Yes, describe the rental terms and options. |

||||

Describe common elements and recreational facilities

Freddie Mac Form 70 March 2005 |

Page 3 of 6 |

Fannie Mae Form 1004 March 2005 |

Uniform Residential Appraisal Report File#

This report form is designed to report an appraisal of a

This appraisal report is subject to the following scope of work, intended use, intended user, definition of market value, statement of assumptions and limiting conditions, and certifications. Modifications, additions, or deletions to the intended use, intended user, definition of market value, or assumptions and limiting conditions are not permitted. The appraiser may expand the scope of work to include any additional research or analysis necessary based on the complexity of this appraisal assignment. Modifications or deletions to the certifications are also not permitted. However, additional certifications that do not constitute material alterations to this appraisal report, such as those required by law or those related to the appraiser’s continuing education or membership in an appraisal organization, are permitted.

SCOPE OF WORK: The scope of work for this appraisal is defined by the complexity of this appraisal assignment and the reporting requirements of this appraisal report form, including the following definition of market value, statement of assumptions and limiting conditions, and certifications. The appraiser must, at a minimum: (1) perform a complete visual inspection of the interior and exterior areas of the subject property, (2) inspect the neighborhood, (3) inspect each of the comparable sales from at least the street, (4) research, verify, and analyze data from reliable public and/or private sources, and (5) report his or her analysis, opinions, and conclusions in this appraisal report.

INTENDED USE: The intended use of this appraisal report is for the lender/client to evaluate the property that is the subject of this appraisal for a mortgage finance transaction.

INTENDED USER: The intended user of this appraisal report is the lender/client.

DEFINITION OF MARKET VALUE: The most probable price which a property should bring in a competitive and open market under all conditions requisite to a fair sale, the buyer and seller, each acting prudently, knowledgeably and assuming the price is not affected by undue stimulus. Implicit in this definition is the consummation of a sale as of a specified date and the passing of title from seller to buyer under conditions whereby: (1) buyer and seller are typically motivated; (2) both parties are well informed or well advised, and each acting in what he or she considers his or her own best interest; (3) a reasonable time is allowed for exposure in the open market; (4) payment is made in terms of cash in U. S. dollars or in terms of financial arrangements comparable thereto; and (5) the price represents the normal consideration for the property sold unaffected by special or creative financing or sales concessions* granted by anyone associated with the sale.

‘Adjustments to the comparables must be made for special or creative financing or sales concessions. No adjustments are necessary for those costs which are normally paid by sellers as a result of tradition or law in a market area; these costs are readily identifiable since the seller pays these costs in virtually all sales transactions. Special or creative financing adjustments can be made to the comparable property by comparisons to financing terms offered by a third party institutional lender that is not already involved in the property or transaction. Any adjustment should not be calculated on a mechanical dollar for dollar cost of the financing or concession but the dollar amount of any adjustment should approximate the market’s reaction to the financing or concessions based on the appraiser’s judgment.

STATEMENT OF ASSUMPTIONS AND LIMITING CONDITIONS: The appraiser’s certification in this report is subject to the following assumptions and limiting conditions:

1.The appraiser will not be responsible for matters of a legal nature that affect either the property being appraised or the title to it, except for information that he or she became aware of during the research involved in performing this appraisal. The appraiser assumes that the title is good and marketable and will not render any opinions about the title.

2.The appraiser has provided a sketch in this appraisal report to show the approximate dimensions of the improvements. The sketch is included only to assist the reader in visualizing the property and understanding the appraiser’s determination of its size.

3.The appraiser has examined the available flood maps that are provided by the Federal Emergency Management Agency (or other data sources) and has noted in this appraisal report whether any portion of the subject site is located in an identified Special Flood Hazard Area. Because the appraiser is not a surveyor, he or she makes no guarantees, express or implied, regarding this determination.

4.The appraiser will not give testimony or appear in court because he or she made an appraisal of the property in question, unless specific arrangements to do so have been made beforehand, or as otherwise required by law.

5.The appraiser has noted in this appraisal report any adverse conditions (such as needed repairs, deterioration, the presence of hazardous wastes, toxic substances, etc.) observed during the inspection of the subject property or that he or she became aware of during the research involved in performing this appraisal. Unless otherwise stated in this appraisal report, the appraiser has no knowledge of any hidden or unapparent physical deficiencies or adverse conditions of the property (such as, but not limited to, needed repairs, deterioration, the presence of hazardous wastes, toxic substances, adverse environmental conditions, etc.) that would make the property less valuable, and has assumed that there are no such conditions and makes no guarantees or warranties, express or implied. The appraiser will not be responsible for any such conditions that do exist or for any engineering or testing that might be required to discover whether such conditions exist. Because the appraiser is not an expert in the field of environmental hazards, this appraisal report must not be considered as an environmental assessment of the property.

6.The appraiser has based his or her appraisal report and valuation conclusion for an appraisal that is subject to satisfactory completion, repairs, or alterations on the assumption that the completion, repairs, or alterations of the subject property will be performed in a professional manner.

Freddie Mac Form 70 March 2005 |

Page 4 of 6 |

Fannie Mae Form 1004 March 2005 |

Uniform Residential Appraisal Report File#

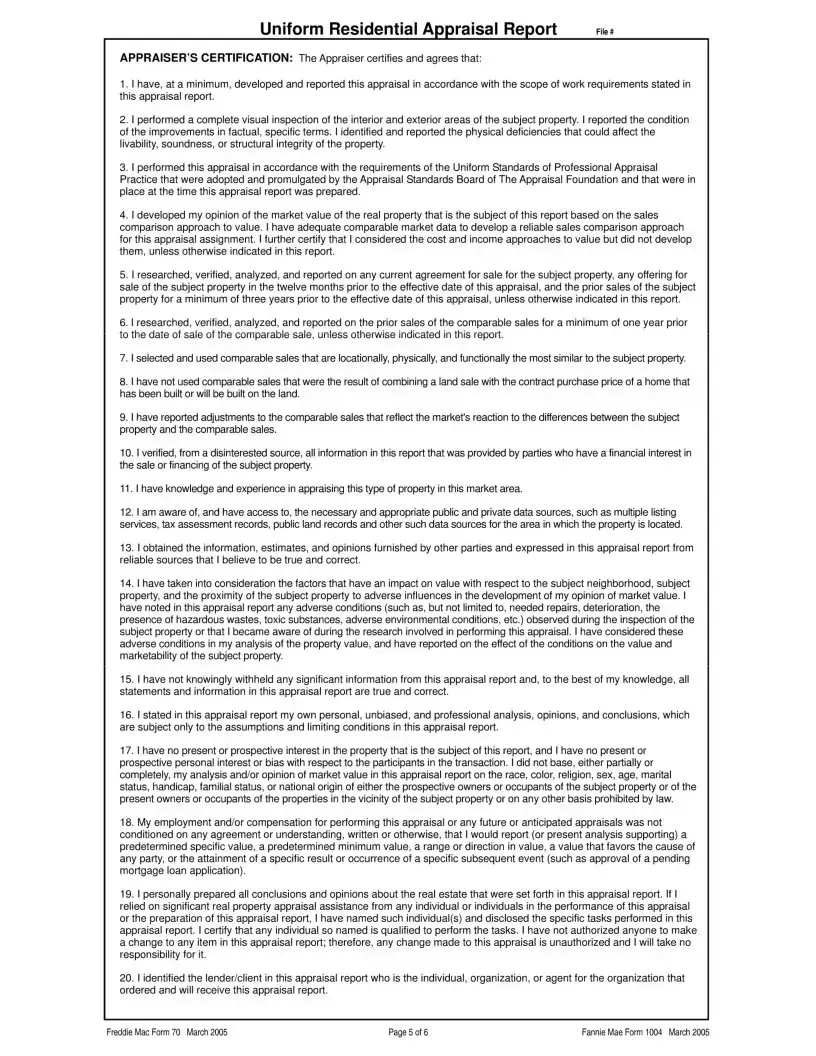

APPRAISER’S CERTIFICATION: The Appraiser certifies and agrees that:

1.1 have, at a minimum, developed and reported this appraisal in accordance with the scope of work requirements stated in this appraisal report.

2.I performed a complete visual inspection of the interior and exterior areas of the subject property. I reported the condition of the improvements in factual, specific terms. I identified and reported the physical deficiencies that could affect the livability, soundness, or structural integrity of the property.

3.I performed this appraisal in accordance with the requirements of the Uniform Standards of Professional Appraisal Practice that were adopted and promulgated by the Appraisal Standards Board of The Appraisal Foundation and that were in place at the time this appraisal report was prepared.

4.1 developed my opinion of the market value of the real property that is the subject of this report based on the sales comparison approach to value. I have adequate comparable market data to develop a reliable sales comparison approach for this appraisal assignment. I further certify that I considered the cost and income approaches to value but did not develop them, unless otherwise indicated in this report.

5.1 researched, verified, analyzed, and reported on any current agreement for sale for the subject property, any offering for sale of the subject property in the twelve months prior to the effective date of this appraisal, and the prior sales of the subject property for a minimum of three years prior to the effective date of this appraisal, unless otherwise indicated in this report.

6.1 researched, verified, analyzed, and reported on the prior sales of the comparable sales for a minimum of one year prior to the date of sale of the comparable sale, unless otherwise indicated in this report.

7.1 selected and used comparable sales that are locationally, physically, and functionally the most similar to the subject property.

8.1 have not used comparable sales that were the result of combining a land sale with the contract purchase price of a home that has been built or will be built on the land.

9.1 have reported adjustments to the comparable sales that reflect the market's reaction to the differences between the subject property and the comparable sales.

10.1 verified, from a disinterested source, all information in this report that was provided by parties who have a financial interest in the sale or financing of the subject property.

11.1 have knowledge and experience in appraising this type of property in this market area.

12.1 am aware of, and have access to, the necessary and appropriate public and private data sources, such as multiple listing services, tax assessment records, public land records and other such data sources for the area in which the property is located.

13.I obtained the information, estimates, and opinions furnished by other parties and expressed in this appraisal report from reliable sources that I believe to be true and correct.

14.1 have taken into consideration the factors that have an impact on value with respect to the subject neighborhood, subject property, and the proximity of the subject property to adverse influences in the development of my opinion of market value. I have noted in this appraisal report any adverse conditions (such as, but not limited to, needed repairs, deterioration, the presence of hazardous wastes, toxic substances, adverse environmental conditions, etc.) observed during the inspection of the subject property or that I became aware of during the research involved in performing this appraisal. I have considered these adverse conditions in my analysis of the property value, and have reported on the effect of the conditions on the value and marketability of the subject property.

15.I have not knowingly withheld any significant information from this appraisal report and, to the best of my knowledge, all statements and information in this appraisal report are true and correct.

16.I stated in this appraisal report my own personal, unbiased, and professional analysis, opinions, and conclusions, which are subject only to the assumptions and limiting conditions in this appraisal report.

17.1 have no present or prospective interest in the property that is the subject of this report, and I have no present or prospective personal interest or bias with respect to the participants in the transaction. I did not base, either partially or completely, my analysis and/or opinion of market value in this appraisal report on the race, color, religion, sex, age, marital status, handicap, familial status, or national origin of either the prospective owners or occupants of the subject property or of the present owners or occupants of the properties in the vicinity of the subject property or on any other basis prohibited by law.

18.My employment and/or compensation for performing this appraisal or any future or anticipated appraisals was not conditioned on any agreement or understanding, written or otherwise, that I would report (or present analysis supporting) a predetermined specific value, a predetermined minimum value, a range or direction in value, a value that favors the cause of any party, or the attainment of a specific result or occurrence of a specific subsequent event (such as approval of a pending mortgage loan application).

19.1 personally prepared all conclusions and opinions about the real estate that were set forth in this appraisal report. If I relied on significant real property appraisal assistance from any individual or individuals in the performance of this appraisal or the preparation of this appraisal report, I have named such individual(s) and disclosed the specific tasks performed in this appraisal report. I certify that any individual so named is qualified to perform the tasks. I have not authorized anyone to make a change to any item in this appraisal report; therefore, any change made to this appraisal is unauthorized and I will take no responsibility for it.

20.I identified the lender/client in this appraisal report who is the individual, organization, or agent for the organization that ordered and will receive this appraisal report.

Freddie Mac Form 70 March 2005 |

Page 5 of 6 |

Fannie Mae Form 1004 March 2005 |

Uniform Residential Appraisal Report File#

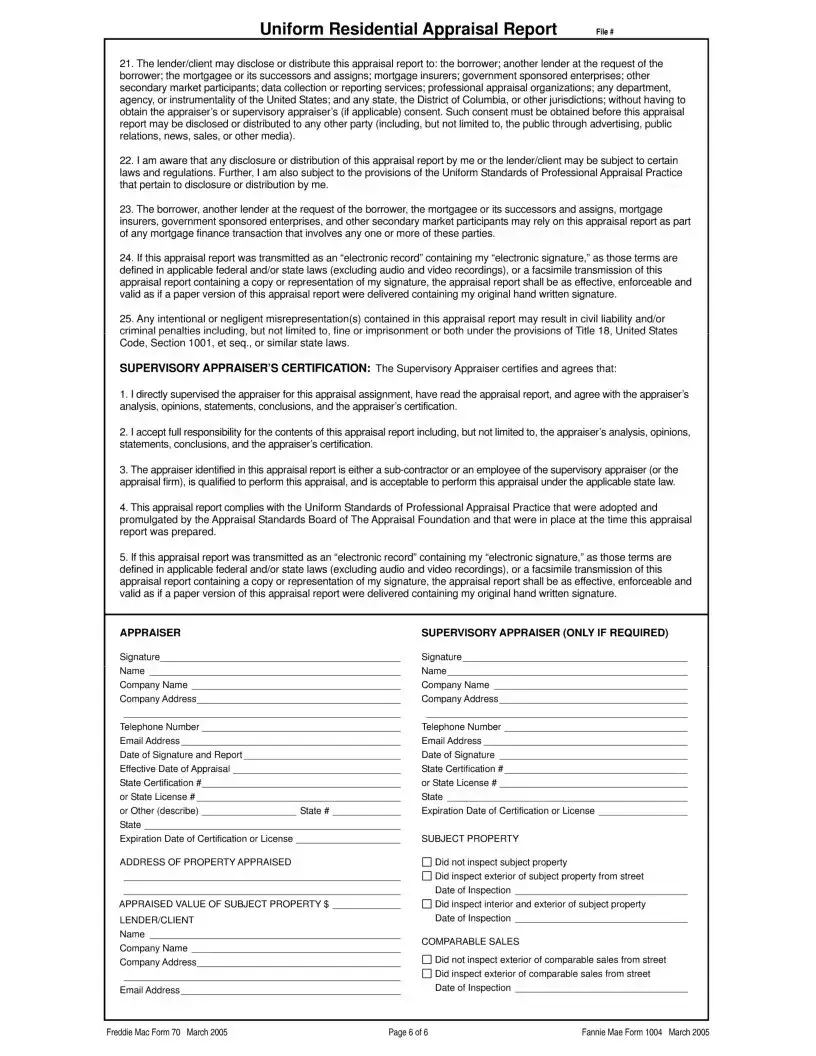

21.The lender/client may disclose or distribute this appraisal report to: the borrower; another lender at the request of the borrower; the mortgagee or its successors and assigns; mortgage insurers; government sponsored enterprises; other secondary market participants; data collection or reporting services; professional appraisal organizations; any department, agency, or instrumentality of the United States; and any state, the District of Columbia, or other jurisdictions; without having to obtain the appraiser’s or supervisory appraiser’s (if applicable) consent. Such consent must be obtained before this appraisal report may be disclosed or distributed to any other party (including, but not limited to, the public through advertising, public relations, news, sales, or other media).

22.1 am aware that any disclosure or distribution of this appraisal report by me or the lender/client may be subject to certain laws and regulations. Further, I am also subject to the provisions of the Uniform Standards of Professional Appraisal Practice that pertain to disclosure or distribution by me.

23.The borrower, another lender at the request of the borrower, the mortgagee or its successors and assigns, mortgage insurers, government sponsored enterprises, and other secondary market participants may rely on this appraisal report as part of any mortgage finance transaction that involves any one or more of these parties.

24.If this appraisal report was transmitted as an “electronic record” containing my “electronic signature,” as those terms are defined in applicable federal and/or state laws (excluding audio and video recordings), or a facsimile transmission of this appraisal report containing a copy or representation of my signature, the appraisal report shall be as effective, enforceable and valid as if a paper version of this appraisal report were delivered containing my original hand written signature.

25.Any intentional or negligent misrepresentation(s) contained in this appraisal report may result in civil liability and/or criminal penalties including, but not limited to, fine or imprisonment or both under the provisions of Title 18, United States Code, Section 1001, et seq., or similar state laws.

SUPERVISORY APPRAISER’S CERTIFICATION: The Supervisory Appraiser certifies and agrees that:

1.1 directly supervised the appraiser for this appraisal assignment, have read the appraisal report, and agree with the appraiser’s analysis, opinions, statements, conclusions, and the appraiser’s certification.

2.1 accept full responsibility for the contents of this appraisal report including, but not limited to, the appraiser’s analysis, opinions, statements, conclusions, and the appraiser’s certification.

3.The appraiser identified in this appraisal report is either a

4.This appraisal report complies with the Uniform Standards of Professional Appraisal Practice that were adopted and promulgated by the Appraisal Standards Board of The Appraisal Foundation and that were in place at the time this appraisal report was prepared.

5.If this appraisal report was transmitted as an “electronic record” containing my “electronic signature,” as those terms are defined in applicable federal and/or state laws (excluding audio and video recordings), or a facsimile transmission of this appraisal report containing a copy or representation of my signature, the appraisal report shall be as effective, enforceable and valid as if a paper version of this appraisal report were delivered containing my original hand written signature.

APPRAISER |

|

SUPERVISORY APPRAISER (ONLY IF REQUIRED) |

Signature |

|

Signature |

Name |

|

Name |

Company Name |

|

Company Name |

Company Address |

|

Company Address |

Telephone Number |

|

Telephone Number |

Email Address |

|

Email Address |

Date of Signature and Report |

|

Date of Signature |

Effective Date of Appraisal |

|

State Certification # |

State Certification # |

|

or State License # |

or State License # |

|

State |

or Other (describe) |

State # |

Expiration Date of Certification or License |

State |

|

|

Expiration Date of Certification or License |

|

SUBJECT PROPERTY |

ADDRESS OF PROPERTY APPRAISED |

|

Did not inspect subject property |

|

|

Did inspect exterior of subject property from street |

APPRAISED VALUE OF SUBJECT PROPERTY $ |

Date of Inspection |

|

LENDER/CLIENT |

|

Did inspect interior and exterior of subject property |

|

|

|

Name |

|

Date of Inspection |

|

|

|

Company Name |

|

COMPARABLE SALES |

Company Add ress |

|

|

|

|

|

|

|

Did not inspect exterior of comparable sales from street |

|

|

Did inspect exterior of comparable sales from street |

Email Address |

|

Date of Inspection |

Freddie Mac Form 70 March 2005 |

Page 6 of 6 |

Fannie Mae Form 1004 March 2005 |

Form Characteristics

| Fact Name | Detail |

|---|---|

| Form Purpose | The 1004 form is used to provide an opinion of the market value for residential properties. |

| Applicable Property Types | This form applies primarily to single-family homes and one-unit residential properties. |

| Mandatory Use | Lenders often require the 1004 form during the mortgage application process. |

| Governing Laws | State regulations and federal guidelines govern the appraisal process for this form. |

| Data Requirements | The appraiser must collect and analyze data related to the property and comparable sales. |

| Neighborhood Analysis | The form requires an assessment of neighborhood characteristics, trends, and market conditions. |

| Property Rights Appraised | Appraisers must indicate whether the property is under fee simple, leasehold, or another ownership type. |

| Sales Concessions | The appraiser must report any financial assistance or concessions provided to the borrower. |

| Condition Assessment | An evaluation of the property’s condition, including any needed repairs, is essential. |

| Potential Issues | Physical deficiencies and adverse conditions affecting property livability must be described. |

Guidelines on Utilizing 1004

The 1004 Form, or the Uniform Residential Appraisal Report, is an essential tool lenders use to evaluate the value of residential properties. Completing this form accurately is crucial for a successful appraisal process. Follow these steps carefully to ensure all necessary information is documented properly, reflecting the true market value of the property.

- Property Information: Start by filling in the property address, borrower’s name, legal description, assessor’s parcel number, and neighborhood name. Indicate whether the property is occupied by the owner, a tenant, or vacant. Provide the city, state, zip code, and county details.

- Tax and Assessment Data: Document the real estate taxes, census tract, and any special assessments. Specify if the property is a planned unit development (PUD) or part of a homeowners association (HOA), along with the respective fees.

- Type of Property Rights: Indicate the type of rights appraised: Fee Simple, Leasehold, or Other. Choose the assignment type: Purchase Transaction, Refinance Transaction, or Other.

- Sale Information: Answer whether the property has been offered for sale in the past twelve months. Provide data on offering prices and the dates associated with them. Comment on whether the contract for sale was analyzed, explaining the results.

- Borrower Assistance: State if any financial assistance relates to the purchase and detail it if applicable. Remember to note that race and neighborhood racial composition are not appraisal factors.

- Neighborhood Characteristics: Assess one-unit housing trends, land use, property values, and housing demand in the area. Describe neighborhood boundaries and relevant market conditions.

- Utilities and Improvements: Provide information about public and private utilities, off-site improvements, and whether these are typical for the area. Address any adverse site conditions that may impact the appraisal.

- General Property Description: Describe the property's foundation, exterior and interior conditions, number of stories, and any additional features. Include details about the heating, cooling, and security amenities.

- Comparable Sales Analysis: Enter details about comparable properties including location, sale price, adjustments made, and the adjusted sale price. Report results of any historical sale or transfer research done for both the subject property and comparable properties.

- Value Approaches: Indicate the market value reached via the sales comparison approach, cost approach (if developed), and income approach (if applicable). Conclude with your opinion of the property’s market value as of the appraisal date.

What You Should Know About This Form

What is the purpose of the 1004 form?

The 1004 form, officially known as the Uniform Residential Appraisal Report, serves to provide a thorough summary appraisal report. Its main goal is to furnish lenders or clients with an accurate and well-supported opinion on the market value of a specific residential property. This assessment helps in making informed decisions regarding property transactions, be it purchases or refinancing.

Who uses the 1004 form?

This form is primarily utilized by real estate appraisers to assess residential properties. Lenders often rely on the findings in the 1004 form when determining the value of a property before approving a mortgage or refinancing application. Additionally, homebuyers and sellers can use the insights from an appraisal to better understand market values and negotiate sales terms.

What information is typically included in a 1004 form?

The 1004 form includes a variety of critical information about the property being appraised. This encompasses property address, ownership details, description of the neighborhood, property rights, current market trends, and details about comparable sales in the area. The appraiser may also provide insights on any physical condition concerns and necessary repairs. All this data collectively helps in forming a comprehensive view of the property's value.

How does the appraiser determine the value of a property using the 1004 form?

To determine a property's value, the appraiser will analyze various components such as recent comparable sales, the condition of the property, market conditions, and economic factors. The 1004 form facilitates this evaluation by allowing the appraiser to input data concerning sales trends, adjustments for property features, and any depreciation or improvements made to the home. Finally, a summary of the appraisal's findings is compiled to support the determined market value.

What are comparable sales, and why are they important in the 1004 form?

Comparable sales, often referred to as "comps," are properties similar in characteristics, size, and location that have recently sold in the area. They are crucial for establishing a fair market value since they provide a benchmark against which the subject property's value can be measured. The 1004 form requires details about these comparable properties, allowing the appraiser to make necessary adjustments based on differences in features, age, and condition.

What does it mean if a property is described as "as-is" in the 1004 form?

If a property is appraised "as-is," it means that the appraisal reflects the property's current condition without factoring in any potential repairs or renovations. The appraisal's value is based solely on the existing state of the property, which can impact its market value, especially if significant deficiencies or repairs are needed.

Can the information in the 1004 form be contested?

Yes, information in the 1004 form can be contested. If a party involved in a property transaction believes that the appraisal does not accurately reflect the property's value, they can request a review or a second appraisal. This may involve presenting additional data or comparable sales not considered in the original appraisal. It’s typically done through the lender or financial institution involved.

What role does neighborhood analysis play in the 1004 form?

Neighborhood analysis is a key component of the 1004 form. It assesses the characteristics and trends within the neighborhood, including property values, location type (urban, suburban, rural), and the condition of similar properties. Understanding the neighborhood helps the appraiser gauge relevant market forces and trends, ultimately influencing the valuation process and supporting the appraisal conclusions.

What are some key terms and conditions appraisers consider in the 1004 form?

Appraisers consider various terms and conditions, including utilities, zoning laws, property rights, and any visible adverse conditions like easements or environmental hazards. Additionally, they assess local market demand, property age, and improvements made. All these factors contribute to understanding the property's position in the market, helping the appraiser render a fair and insightful evaluation.

Common mistakes

Filling out the 1004 form, also known as the Uniform Residential Appraisal Report, is critical for ensuring that a property is assessed accurately. However, individuals often make mistakes that can compromise the integrity of the appraisal. Understanding these common pitfalls can help prevent delays and ensure a smoother appraisal process.

One of the frequent errors occurs with property descriptions. When filling in the property address or the legal description, it’s vital to double-check the information. If even a small detail is incorrect, such as a number in the address or a typo in the legal description, it can lead to confusion and potentially misinform the appraisal process.

Another mistake revolves around the neighborhood characteristics. Appraisers rely heavily on accurate neighborhood data, so providing outdated or misleading information can skew the appraisal outcome. For instance, improperly identifying the neighborhood type or incorrectly assessing property values could lead to an inaccurate appraisal, affecting the loan approval process.

Additionally, many individuals fail to account for financial assistance which affects the property’s appraisal. When asked if there is financial aid, it is crucial to answer accurately. Neglecting to disclose assistance can misrepresent the buyer’s financial situation, potentially causing issues with the lender.

Another common error involves comparable sales data. When selecting comparable properties, it’s essential to choose those that are genuinely similar in size, locality, and condition. Failing to do so can lead to significant discrepancies in the appraisal value. Providing more appropriate comparables strengthens the appraisal report.

Misunderstanding the questions surrounding adverse conditions can also lead to mistakes. If there are issues like environmental hazards or easements that affect the property, failing to disclose these could mislead the appraisal. This section is crucial for clarifying the overall condition of the property and providing a true market picture.

Finally, neglecting to follow up on market conditions can result in outdated conclusions about property values. Pricing trends can shift rapidly, and not addressing these changes in the appraisal can substantially affect the assessed value. Including current data on market conditions reflects an accurate and thorough appraisal process.

Being mindful of these common mistakes when completing the 1004 form will aid individuals in ensuring a thorough and accurate appraisal. Attention to detail is essential in this process, as it dictates the property's assessed market value, ultimately impacting financing and sales opportunities.

Documents used along the form

The Uniform Residential Appraisal Report, commonly known as the 1004 form, is a vital document for assessing the value of residential properties. Additional documents often accompany the 1004 to provide comprehensive insights into various aspects of a property. Below is a list of key forms and documents that are frequently used alongside the 1004 form, including a brief description of each.

- Form 442: Transmittal Summary - This form summarizes the appraisal report and includes essential information for lenders. It allows quick access to the appraisal’s key findings.

- Form 1004MC: Market Conditions Addendum - This addendum provides data on the neighborhood’s market trends, such as inventory levels and sales trends. It helps assess local market conditions.

- Form 2055: drive-by Appraisal - A simplified version of the appraisal that doesn’t require a full inspection of the property interior. It involves a visual inspection of the exterior and neighborhood.

- Form 1073: The Individual Condominium Unit Appraisal Report - This form is specifically used for appraising individual condominium units. It includes details unique to condos, such as association fees.

- Form 70: Uniform Residential Appraisal Report for Freddie Mac - Similar to the 1004 form but tailored specifically for Freddie Mac's guidelines and requirements.

- Form 1004 Certificate of Appraisal - This certificate indicates that the property has been appraised according to professional standards and often needs to be signed by the appraiser.

- Land Use Map - A visual representation of the zoning and land use for the area surrounding the property. It helps assess the potential development opportunities.

- Flood Zone Determination Letter - This letter confirms whether the property is in a flood zone, which can significantly affect its value and financing requirements.

- Disclosure Forms - These documents provide important information about the property condition, including any known defects or issues that could influence its marketability.

Each of these documents contributes valuable information, ensuring that the appraisal process is thorough and accurate. When working with the 1004 form, these supplementary forms provide the necessary context and details for lenders and appraisers alike.

Similar forms

-

Form 70 (Freddie Mac): This form is also a residential appraisal report. Like the 1004 form, it provides a thorough overview of the property value based on comparable sales. It includes sections for property details, neighborhood analysis, and adjustments for differences between properties.

-

Fannie Mae Form 1025: Intended for two to four-unit residential properties, this form shares similarities with the 1004 by requiring assessments of property condition, neighborhood characteristics, and comparable sales data to determine market value.

-

Form 704 (Freddie Mac): This is a Small Residential Income Property Appraisal Report. It follows a similar structure to the 1004, focusing on providing a value opinion based on income-generating potential alongside comparable property data.

-

Fannie Mae Form 1004MC: This form is a Market Conditions Addendum to the 1004. It requires appraisers to analyze market trends, including supply and demand in the neighborhood, which is also assessed in the 1004.

-

Appraisal Institute Form APP1: This form is a general residential appraisal report. Similar to the 1004, it includes information about property description, neighborhood, and comparable sales, aiming to establish a fair market value.

-

Form 1073 (Fannie Mae): This is a Uniform Residential Appraisal Report designed for a one-unit property that is currently under construction or recently completed. It shares key components with the 1004, focusing on property value and condition analysis.

-

Form 2090 (Freddie Mac): This form is a Manufactured Home Appraisal Report. Similar to the 1004, it assesses the property’s market value, taking into account various characteristics and comparable sales in the area.

-

Form 2120 (Fannie Mae): This is the Uniform Residential Appraisal Report for Cooperative Units. It requires information about the unit and its market environment, similar to the assessments done in the 1004 form.

Dos and Don'ts

When filling out the 1004 form, careful attention to detail is crucial. Below are some important considerations to ensure accurate completion.

- Do include complete and accurate property information.

- Do provide clear explanations for any analyses performed or omitted.

- Don't overlook checking if the property seller is the owner of public record.

- Don't leave out any required supporting documents or data sources.

Misconceptions

Here are some common misconceptions about the 1004 form, also known as the Uniform Residential Appraisal Report:

- It is only for single-family homes. The 1004 form can be used for one-unit properties, which may include condos or townhomes, not just traditional single-family houses.

- All appraisals are the same. Each appraisal is unique and considers various factors, including property condition, location, and recent sales in the area.

- The appraiser must be a licensed real estate agent. While appraisers do need specific training and licensing, they are not required to be real estate agents.

- Appraisals determine the sale price. An appraisal gives an opinion of market value, but it does not set a sale price. The seller and buyer negotiate that based on many factors.

- The 1004 form is only for lenders. While lenders often use the 1004 form, it can also provide valuable information for buyers and sellers in the real estate market.

- Appraisers are biased towards the lender. Appraisers are required to remain impartial and perform their evaluations based on established guidelines and data.

- Adjustments on comparable properties are arbitrary. Adjustments are based on careful analysis of the differences between the subject property and comparable sales in the area.

Key takeaways

Filling out and using the Fannie Mae Form 1004, also known as the Uniform Residential Appraisal Report, is essential for accurately determining the market value of a property. Here are some key takeaways to consider:

- Understand the Purpose: The form provides a well-supported opinion of the property's value, crucial for lenders and clients in making informed decisions.

- Accurate Property Description: Complete the property address, legal description, and parcel number accurately. A clear description helps convey the property’s specifics.

- Neighborhood Analysis: Evaluate neighborhood characteristics carefully. Factors such as property values and housing trends can greatly influence the appraisal’s outcome.

- Comparable Sales: The appraisal should include information on comparable sales within the past year. These sales are vital for establishing a fair market value.

- Property Condition: Thoroughly assess the property's condition, including needed repairs and overall maintenance. A well-described condition can directly affect valuation.

- Market Conditions: Highlight current market conditions and any external factors that could impact property value. Whether prices are stable, increasing, or declining warrants careful consideration.

- Complete Necessary Sections: Ensure all relevant sections are filled out completely and accurately, including the assignment type and any special assessments. Missing information can lead to inaccurate valuations.

Browse Other Templates

Mc371 - Compliance with all instructions on the MC 371 may expedite the processing of applications.

Cms 40b Form - Eligibility for Part B is critical; make sure to meet all requirements before applying.