Fill Out Your 438Bfu Form

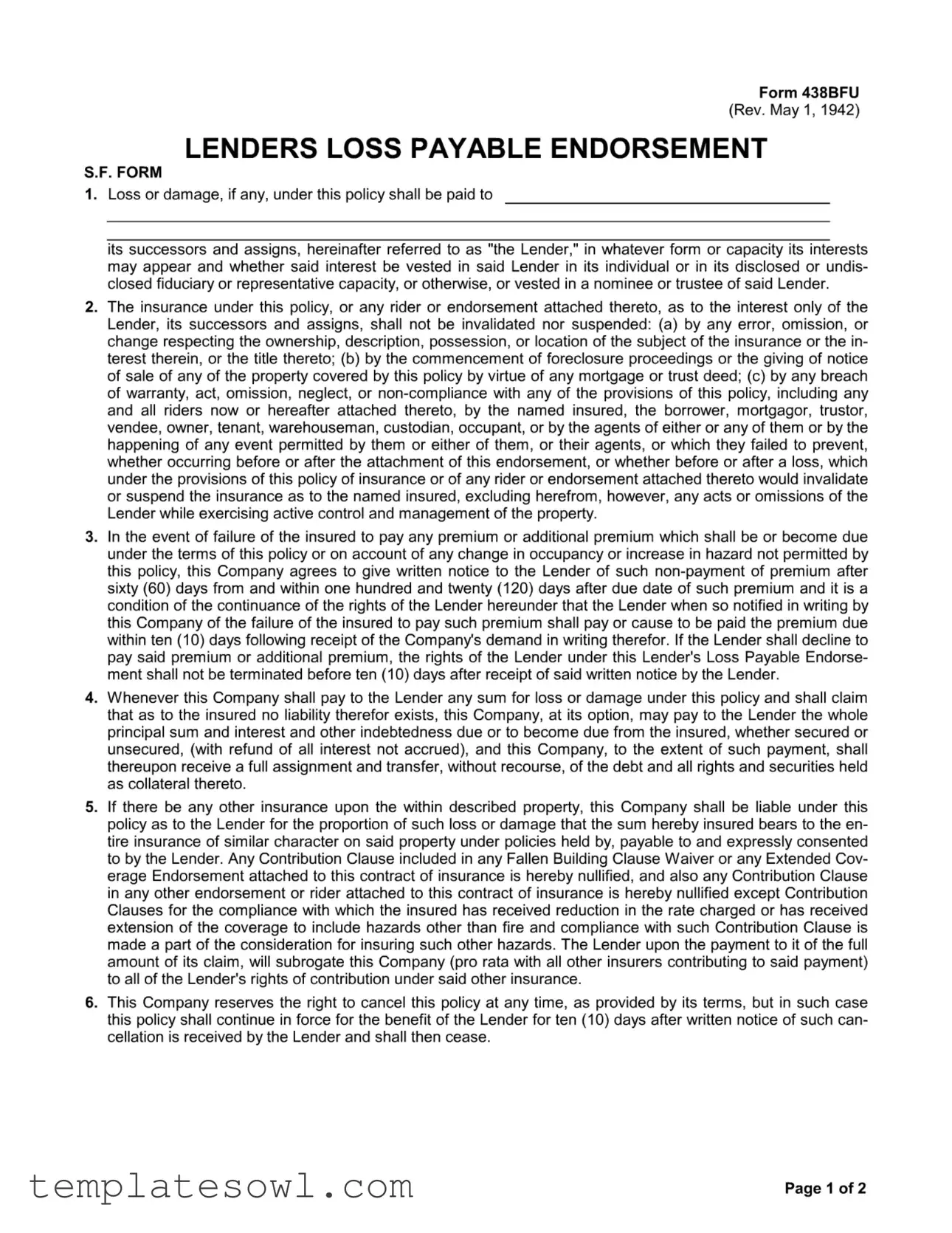

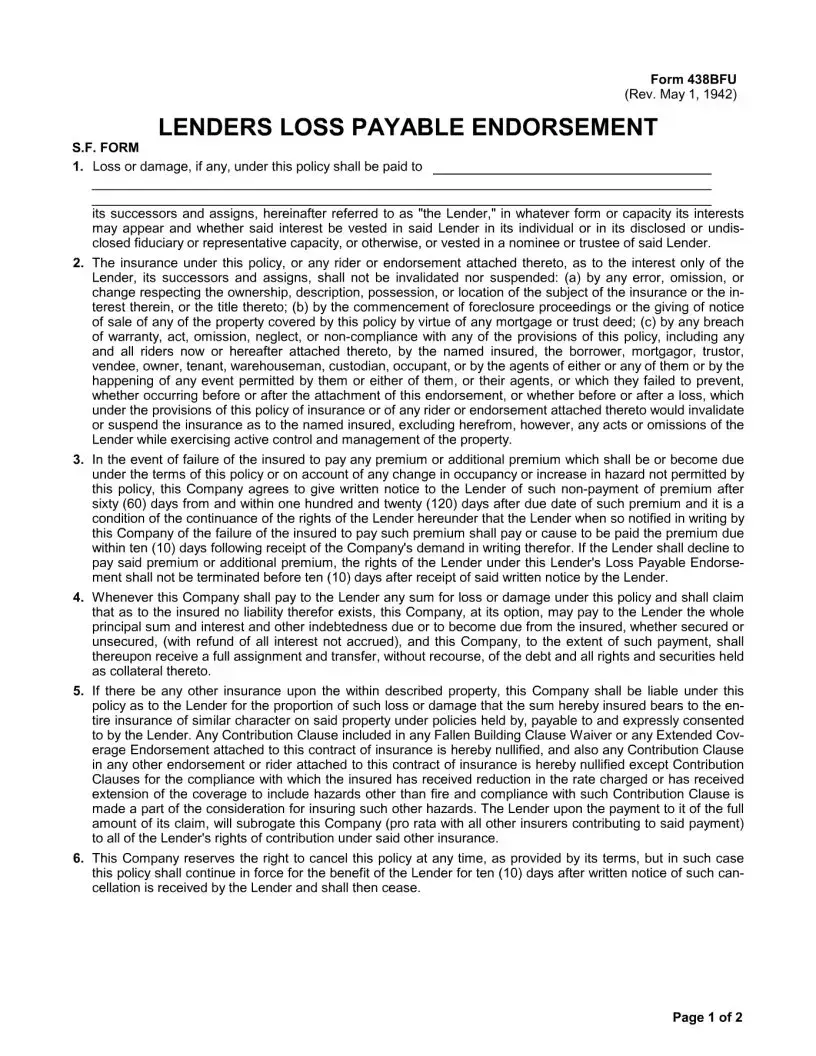

The Form 438Bfu, also known as the Lenders Loss Payable Endorsement, plays a crucial role in the relationship between lenders and insurance policies. Initially introduced in 1942, it is designed to protect the interests of lenders when an insured property suffers loss or damage. One of the form's major characteristics is that it ensures payment to lenders, their successors, and assigns when a claim arises, regardless of the situation surrounding ownership or the interests in the property. The policy remains in effect even if there are errors, omissions, or changes regarding the property’s ownership, or in events such as foreclosure proceedings. Additionally, the form lays out specific requirements for notifying lenders about premium non-payment and provides rights to lenders if the insurance policy is canceled or expires. It also addresses the complexities of multiple insurance policies, clarifying how losses will be allocated among them. Lastly, it outlines the procedure for the assignment of claims, allowing lenders to retain certain rights if a claim is paid. This interplay between adherence to policy details and lender protections makes the Form 438Bfu a vital document in the domain of property insurance."

438Bfu Example

Form Characteristics

| Fact Name | Description |

|---|---|

| Form Name | The form is officially called "Form 438BFU" and is a Lenders Loss Payable Endorsement. |

| Revision Date | This form was last revised on May 1, 1942. |

| Purpose | The form is designed to ensure that lenders are compensated for losses on insured properties. |

| Payment of Loss | Losses under the policy are to be paid directly to the lender, its successors, or assigns. |

| Valid Insurance | The lender's interest in the insurance remains valid despite errors or changes relating to ownership or occupancy. |

| Notice Requirement | The insurance company must inform the lender about any non-payment of premiums within a specified time frame. |

| Subrogation Rights | Upon receiving payment for a claim, the insurance company may assume the lender’s rights to recover from other insurers. |

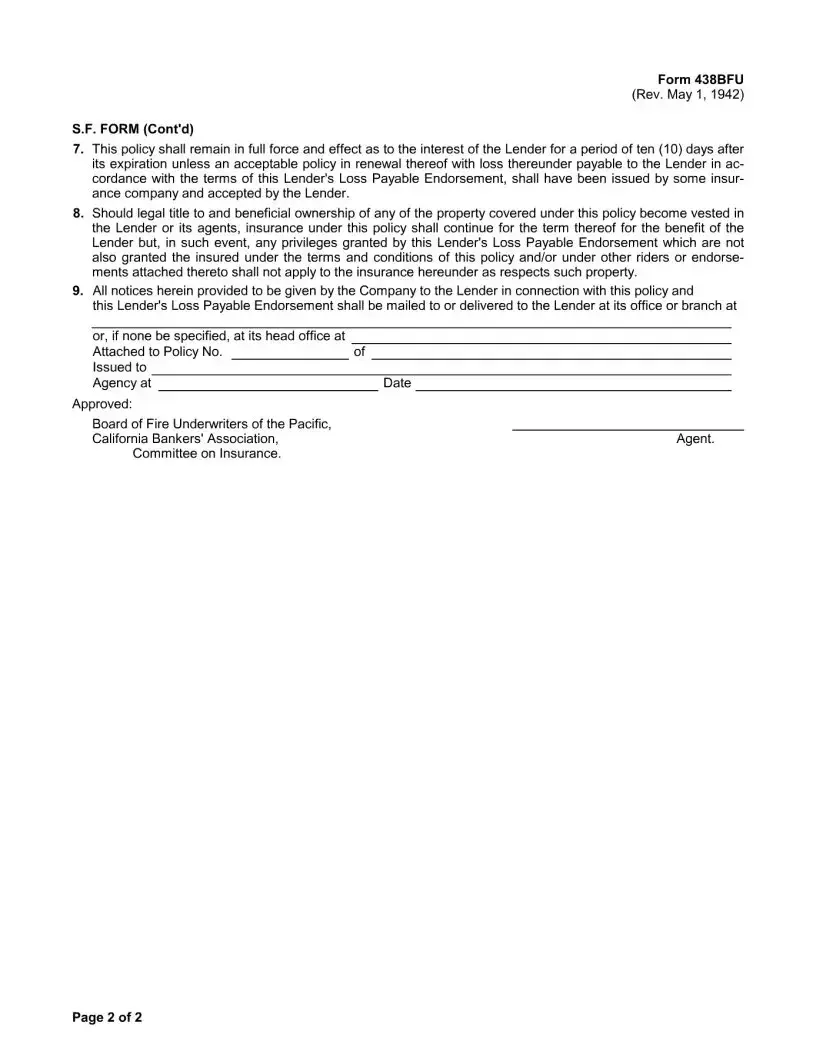

| Cancellation Policy | The insurance policy can be canceled by the company, but it remains in force for the lender's benefit for an additional ten days. |

| Continuation of Coverage | Coverage will continue for ten days after expiration unless a renewal policy is accepted by the lender. |

| Notification Process | All notices from the insurance company to the lender regarding this policy must be delivered to specified addresses. |

Guidelines on Utilizing 438Bfu

Filling out the 438Bfu form is an essential step for lenders and policyholders when addressing insurance matters. Completing this form accurately ensures that your interests are protected under the insurance policy.

- Obtain the Form: Get a copy of the 438Bfu form, which may be available online or from your insurance provider.

- Review Instructions: Before filling it out, carefully read any instructions that accompany the form to ensure you understand what information is needed.

- Policy Information: Fill in the policy number at the top of the form where it asks for the associated insurance policy.

- Lender Information: Provide the name and address of the lender or their representative in the designated spaces.

- Property Description: Accurately describe the property covered by the insurance policy. Include details like location, type of property, and any other required specifics.

- Owner Information: If applicable, enter the name of the property owner, especially if different from the lender.

- Sign and Date: Once you have filled out all the necessary information, sign and date the form to validate it.

- Submit the Form: Send the completed form to your insurance provider, making sure to keep a copy for your records.

After submitting the form, your insurance company will process your request. They will notify you once your endorsement is active, confirming that coverage aligns with your interests as a lender. Keep an eye on any communications for next steps or additional information they may require.

What You Should Know About This Form

What is the purpose of Form 438Bfu?

Form 438Bfu serves as a Lender's Loss Payable Endorsement. It ensures that if a loss or damage occurs, the insurance company will pay the loan amount or losses directly to the lender. This form helps protect the lender’s financial interests in the insured property.

What happens if the insured fails to pay the premium?

If the insured does not pay the premium, the insurance company will notify the lender in writing after sixty days. The lender has ten days to pay the overdue premium. If the lender chooses not to pay, their rights under this endorsement will remain valid for ten days after they receive notice.

Can the insurance policy be canceled?

Yes, the insurance company reserves the right to cancel the policy. If cancellation occurs, the policy will still protect the lender for ten days after the lender receives written notice of the cancellation. After this period, coverage will cease.

What happens if the insured property has other insurance?

In cases where the insured property is covered by other insurance, the insurance company will only be liable for the proportion of the loss that correlates to the amount insured under this policy. Any clauses in other endorsements that conflict with this arrangement will be nullified, except for those related to compliance that provide benefits, like reduced rates or expanded coverage.

Common mistakes

Filling out Form 438BFU can present challenges for individuals and businesses alike. Many mistakes can arise during this process. Recognizing these errors can help ensure compliance and prevent complications. Below are some common mistakes people make when completing this form.

One prevalent mistake is failing to provide complete information. Incomplete or vague answers can lead to misunderstandings about the coverage offered. It is essential to fully disclose the details of the property being insured, including the address, ownership details, and any other relevant information. Missing this information can result in reduced coverage or denial of claims.

Another common error is not understanding the definition of the lender. The term "lender" in the context of this form can encompass various entities, which might include banks, credit unions, or private lenders. If individuals mistakenly assume that the lender is a single entity or do not properly identify the lender's roles and capacities, it can affect the endorsement's effectiveness.

Maintaining awareness of deadlines and notifications is also crucial. Participants often overlook the timelines for payment or notifications associated with this policy. For example, if a premium payment is overdue, the lender must pay it within ten days of receiving a notification from the insurance company. Missing these deadlines can jeopardize the policyholder's rights.

Additionally, individuals frequently overlook the importance of reading attached endorsements. Riders or endorsements that accompany the policy can modify coverage terms significantly. Not reviewing these modifications can create gaps in coverage, leaving an insured potentially vulnerable during a loss event.

Finally, failure to keep records of communication can be detrimental. Documentation of all correspondences with the insurance company and lender should be retained. Should disputes arise, having a clear record can strengthen claims and clarify responsibilities under the policy. Ensuring proper documentation can aid in protecting the interests of the lender and the insured.

Documents used along the form

The Form 438BFU, known as the Lender's Loss Payable Endorsement, plays a crucial role in the realm of insurance claims related to property. Several other forms and documents typically accompany it, each serving a specific purpose to ensure clarity and compliance throughout the insurance process. Below are these important documents with brief descriptions.

- Certificate of Insurance: This document confirms the existence of an insurance policy and outlines the coverage details, including the insured party, coverage limits, and any relevant endorsements. It provides proof of insurance to lenders or other interested parties.

- Insurance Policy: The comprehensive contract between the insured and the insurance company stipulates terms, conditions, and exclusions. It details the scope of coverage, including losses covered under the policy.

- Proof of Loss Form: Following a loss event, this form is submitted by the insured to initiate a claim. It outlines the claim amount and provides documentation to support the loss incurred, enabling the insurance company to evaluate the claim promptly.

- Loss Run Report: A loss run report compiles all past claims data related to the property, including open and closed claims. This document is essential for lenders to assess risk and make informed decisions regarding insurance continuation.

- Endorsement Forms: These forms modify the original insurance policy terms by adding, changing, or removing coverage. They are crucial for keeping the policy updated in accordance with any significant changes in risk or property status.

- Subrogation Agreement: This document outlines the right of the insurer to pursue a third party that caused a loss after the insurer has paid out on a claim. It allows the insurance company to recover some or all of the losses from the responsible party.

- Waiver of Subrogation: In certain circumstances, this agreement may be executed to allow one party to relinquish its rights to seek reimbursement from the other party for losses or damages, usually in a contractual context.

- Declaration Page: Included as part of the insurance policy, this page summarizes the coverage provided, including the insured parties, coverage limits, and policy period. It serves as a quick reference for the key details of the insurance agreement.

- Claim Adjustment Report: After a claim is filed, this report documents the findings of the insurance adjuster. It outlines the investigation results, estimated damages, and recommendations for payment, guiding the insurer's response to the claim.

Understanding these accompanying documents and their functions is instrumental for all stakeholders involved in the insurance process. Proper management and awareness of these forms can significantly facilitate smoother transactions and ensure compliance with necessary requirements.

Similar forms

The 438Bfu form, known as the Lenders Loss Payable Endorsement, has several similar documents that function within the insurance and lending space. Each document is designed to protect the interests of lenders and outline specifics regarding policy coverage. Below are descriptions of seven documents akin to the 438Bfu form:

- Loss Payable Clause: This document ensures that in the event of a claim, the insurer will pay the loss directly to the lender. Like the 438Bfu form, it provides security for lenders, affirming their right to recover losses despite the borrower’s default.

- Mortgagee Clause: Similar in structure to the lenders loss payable endorsement, this clause protects the mortgagee's interest in the insurance policy. It guarantees that the mortgagee will receive payment in case of a loss, regardless of any policy breaches by the insured.

- Additional Insured Endorsement: This endorsement extends coverage to additional parties involved in a property policy, ensuring that they receive protection similar to that specified in the 438Bfu form. It establishes that under certain conditions, these additional parties will also be compensated for losses.

- Subrogation Rights Agreement: This document outlines the rights an insurer has to pursue recovery from third parties responsible for a loss after compensating the insured or lender. The concept aligns with provisions in the 438Bfu form regarding lender rights upon payment of claims.

- Collateral Insurance Endorsement: This endorsement operates in tandem with other insurance policies that may cover the same property. It delineates how claims will be settled between different insurers, akin to the provisions seen in the 438Bfu regarding multiple coverages.

- Property Insurance Policy: While broader in scope, a standard property insurance policy includes similar concepts about coverage and claims processes. Like the 438Bfu form, it outlines the insurer's obligations upon loss and the conditions under which those obligations may change.

- Owner’s Policy of Title Insurance: This document protects property owners against losses related to defects in title. Although it serves a different primary purpose, its intention of safeguarding financial interests reflects the protective nature found within the 438Bfu form.

Dos and Don'ts

When completing the Form 438Bfu, here are some essential dos and don'ts to help ensure accuracy and compliance.

- Do read the form carefully before beginning to fill it out.

- Do provide accurate and current information throughout the form.

- Do double-check for any errors before submitting the form.

- Do include all required signatures and dates where necessary.

- Don’t leave any sections blank unless specifically instructed to do so.

- Don’t use abbreviations or shorthand that might confuse the reviewer.

Following these guidelines will help ensure a smooth process when submitting the Form 438Bfu. Always prioritize clear and complete information to avoid potential delays in processing.

Misconceptions

Misconceptions about the Form 438Bfu can lead to misunderstandings regarding its purpose and implications. Here are nine common misconceptions clarified:

- 1. The form only protects the lender. While it does prioritize the lender in instances of loss, it is also meant to safeguard the insured's interests, clarifying their responsibilities and rights.

- 2. The lender is responsible for paying all premiums. This is not the case. The borrower is responsible for any premiums. The lender may need to step in only if the borrower fails to pay.

- 3. Any insurance claims will automatically benefit the lender. Not necessarily. The form specifies that claims are paid proportionately, depending on the total coverage and how much was insured by other policies.

- 4. The insurance remains active indefinitely. This is a misconception. The insurance has a specific term and may need renewal or a new policy for continuous coverage.

- 5. Cancellation of the policy means abrupt termination of coverage for the lender. Actually, the policy remains in force for a limited time after cancellation—10 days—providing a buffer for the lender.

- 6. Lenders have unlimited rights over insured property. The form clarifies that while the lender has significant rights, certain privileges are restricted in cases where the lender or their agents gain legal title.

- 7. Only the insured can notify the lender about changes affecting the policy. This is inaccurate. The insurance company is responsible for notifying the lender of non-payment or major changes, ensuring they remain informed.

- 8. The form requires the lender to always act in accordance with the insured. There are instances when the lender’s actions may not be limited by the insured's preferences, especially regarding their rights to manage risk.

- 9. The form is outdated and irrelevant. Despite being revised in 1942, the principles established in the form remain pertinent. Many lenders and borrowers continue to engage with these foundational concepts.

Key takeaways

Filling out and utilizing the 438Bfu form, also known as the Lender's Loss Payable Endorsement, requires attention to specific guidelines. Here are some essential takeaways:

- The form provides a guarantee: When loss or damages occur under the insurance policy, payments will go directly to the lender and their successors or assigns.

- No invalidation from various situations: The lender's interest under the policy remains intact despite errors, changes in ownership, or foreclosure proceedings.

- Notification of premium non-payment: If the insured fails to pay premiums, the insurance company must notify the lender within 60 to 120 days, allowing the lender a chance to pay the owed amount.

- Full assignment of debt: Upon payment for a loss, the company may require the lender to assign the debt and rights back to them to recover their losses.

- Proportional liability: If there are other insurance policies covering the property, liability under this policy will be proportional to the amount of coverage.

- Cancellation clause: The insurance company can cancel the policy, but it remains effective for the lender for 10 days post-notification of cancellation.

- Renewal terms: The policy remains valid for 10 days after expiration unless a renewed policy has been accepted by the lender.

- Ownership impacts coverage: Should the title of the property pass to the lender, the original insurance terms apply, but certain privileges may not transfer.

- Communication requirements: All notices from the insurance company regarding this policy must be sent to the lender's specified office.

Understanding these key points can help ensure the effective completion and utilization of the 438Bfu form. This process, while detailed, is designed to protect the interests of the lender in the full scope of potential risks related to property insurance.

Browse Other Templates

Publx - Feedback from references can greatly influence hiring decisions.

Leosa Restrictions - The protection provided by the FOP Legal Plan can be crucial in various legal matters.

Write Certificate - Completion of this form is essential for compliance with Illinois licensing laws.