Fill Out Your 5196 Application Loan Form

The 5196 Application Loan form is an essential document for those seeking their first loan against life insurance policies issued before June 1, 1969. This form is directed to the Senior Divisional Manager of the Life Insurance Corporation of India. The applicant must provide relevant details, including the policy number and the amount requested, which could be either a specific sum or the maximum available as a loan. The interest rate is fixed at 10.5% per annum, compounding half-yearly, and the borrower agrees to several conditions regarding the loan. These conditions include assigning the policy as security for the loan and specifying that the loan amount shall not be available for disbursal within six months of settlement. Importantly, the borrower must also confirm their understanding of these terms, which may vary depending on whether the policy already carries specific endorsements. Additional sections in the form cater to various situations, such as when a prior loan exists, ensuring clarity in the borrowing process. A declaration must be completed for borrowers who do not read English, emphasizing the importance of comprehension. Alongside this application, there’s a separate receipt form that acknowledges the loan amount received, further ensuring proper documentation of the transaction. Overall, the 5196 Application Loan form is designed to facilitate a structured and transparent loan process for policyholders, protecting both the borrower's and the corporation's interests.

5196 Application Loan Example

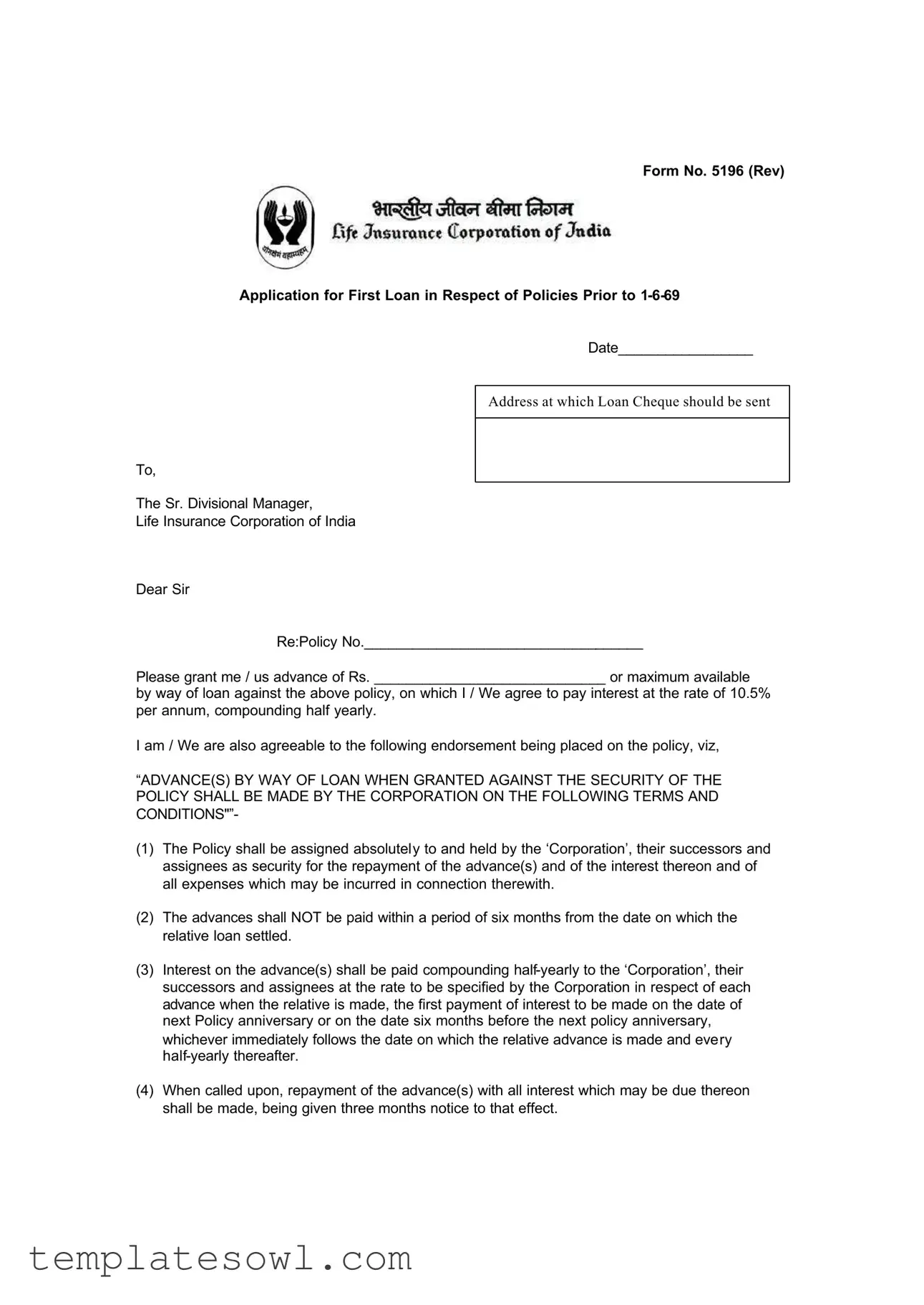

Form No. 5196 (Rev)

Application for First Loan in Respect of Policies Prior to

To,

The Sr. Divisional Manager,

Life Insurance Corporation of India

Date_________________

Address at which Loan Cheque should be sent

Dear Sir

Re:Policy No.___________________________________

Please grant me / us advance of Rs. _____________________________ or maximum available

by way of loan against the above policy, on which I / We agree to pay interest at the rate of 10.5% per annum, compounding half yearly.

I am / We are also agreeable to the following endorsement being placed on the policy, viz,

“ADVANCE(S) BY WAY OF LOAN WHEN GRANTED AGAINST THE SECURITY OF THE POLICY SHALL BE MADE BY THE CORPORATION ON THE FOLLOWING TERMS AND CONDITIONS"”-

(1)The Policy shall be assigned absolutely to and held by the ‘Corporation’, their successors and assignees as security for the repayment of the advance(s) and of the interest thereon and of all expenses which may be incurred in connection therewith.

(2)The advances shall NOT be paid within a period of six months from the date on which the relative loan settled.

(3)Interest on the advance(s) shall be paid compounding

(4)When called upon, repayment of the advance(s) with all interest which may be due thereon shall be made, being given three months notice to that effect.

(5)The Corporation, their successors and assignees shall not be bound to accept payment of any of the advance(s) unless tendered in full.

(6)In the event of failure to repay the advance(s) to repay the advance(s) when required or to pay interest on the date as hereinbefore mentioned or within one calendar month after each due date respectively the Policy shall be held without the necessity of any notice being given to be forfeited to the Corporation, their successors and assignees, and Corporation, shall be entitled to apply the Surrender Value allowable in respect of the Policy in terms of their Regulation and condition in payment of the advance(s) interest and expenses, the balance only shall become due and payable under the policy.

(7)In case the policy shall mature or become a claim by death when the amount of the advance(S) or any Portion there of shall remain outstanding, the Corporation shall be entitled to deduct such amount together with all interest upto the date of maturity or of death as the case may be from the policy moneys and the balance due and payable under the policy.

The Policy duly assigned in your favour, the receipt for the loan amount andn declaration regarding assignment duly completed are sent herewith.

|

Yours faithfully |

(1) |

_________________________________ |

(2) |

_________________________________ |

|

Signature(s) |

APPLICATION FOR LOAN AS UNDER WHERE THE POLICY ALREADY BEARS THE ENDORSEMENT OF TERMS AND CONDITIONS OF LOAN OR WHERE THE POLICY HAS BEEN ISSUED ON OR AFTER

(1)Fresh loan where previous loan is subsisting.

(2)Further loan where previous loan granted at 6% or 7 ½ % or 9% is subsisting.

The Sr. Divisional Manager,

Life Insurance Corporation of India.

Date __________________2000

Dear Sir,

Re : Policy No. __________________________________

(1)Please grant me / us an advance of Rs. _____________________ (Rupees ___________ __

_____________________________________________________________________________

_____________________________________________________________________________

in words) or maximum aailable by way of loan against above policy on which I / We agree to pay interest at the rate of 10.5% per annum payable every half year.

(2)I / am / We are aware of the terms and conditions on which the loan will be advanced. I / am / We are also aware that said terms and conditions:-

* have already been endorsed on the Policy.

**will those as contained in the clause headed “Loans” appearing in the Conditions and Privileges printed in the Policy.

The receipt for the loan amount along with the assignment declaration slip is returned herewith duly completed.

*** The policy duly assigned in your favour is also endorsed.

Yours faithfully

(1)__________________________________

(2)_________________________________

Signature(s)

*Strike out in respect of the Poliies issued on or after

***Delete where previous loan is subsisting.

_____________________________________________________________________________

Form No 5200

FORM OF RECIPT FOR THE LOAN ADVANCE

Rs. ____________________Palace_______________Dated______________________

I /We (1) _________________________________ (2) __________________________________

do hereby acknowledge receipt of an amount of Rs. ___________________________________

(Rupees ______________________________________________________________________

(in words) paid to me / us by the LIFE INSURANCE DORPORATION OF INDIA as an advance against the Policy No.

1.Assured

Revenue

Stamp Rs.1/-

2. Assignee |

Signature(s) |

3.Trustee

DECLARATION TO BE COMPLETED WHEN BORROWER/S CANNOT READ ENGLISH

I hereby declare that the contents of the above APPLICATION FOR LOAN (Form No. 5196/5205) and the FORM OF RECEIPT FOR THE LOAN ADVANCE (Form No. 5200) have been translated and explained by me to

(1)______________________________________and (2) _______________________________

and further declare that he / she they fully understand(s) the meaning there of.

_______________________________

Signature of the declarant

________________________________________________________________

INSTRUCTIONS :-

If either or both the borrowers be

NOTE OF AUTHORITY

If the within receipt is signed by more than one person and payment is desired to be made to one of the signatories or to third party, the following Note of Authority should be completed and signed by all of them.

Mark |

|

Place_________________________ |

Date _____________________ |

I/We hereby authorise the Life Insurance Corporation of India to pay the within mentioned loan amount of Rs. _________/out of within mentioned loan, a sum of Rs. __________to __________

________________Signature

________________Signature

and he/she/they has/have agreed to payment to _______________________________________

be made to the party or parties authorised.

(Signature of the Declarant)

INSTRUCTION :

If either or both the persons completing the Note of Authority be

TO BE COMPLETED IN CASE OF MULTI PURPOSE POLICIES) ( Table Nos. 33 and 34)

|

Place__________________ |

The Sr. Divisional Manager, |

|

Life Insurance Corporation of India, |

Date __________________ |

Re: Policy No.__________________________

Dear Sir,

With reference to my application for the loan to meet the___________________premium and for

private purpose under the above Policy which has been issued under the Corporation’s Multi Purpose Plan, I hereby agree that in the event of my death during the selected term of the Policy the Corporation may immediately on my death occuring, call for the repayment of the loan with interest there on giving the claimant/s however, the option to have the loan and interest duly repaid, in the first instance, out of the lump sum payment of 10% of the Sum Assured of instalments and if both these are not sufficient to meet the repayment, the balance from the remainder i.e. 90% of the sum assured when payable or a alternative option to have the benefits Reduced to such an extent as would provide for liquidation of the loan.

|

|

Yours faithfully |

_____________________ |

|

|

_____________________ |

Assignee/s |

|

_____________________ |

|

(Signature of Assured) |

|

|

|

Please detach it from here and paste it on the Policy. |

Form No. 5198 |

|

FORM OF ASSIGNMENT OF THE POLICY BY THE POLICY HOLDER IN FAVOUR OF

THE CORPORATION FOR THE PURPOSE OF LOAN AGAINST THE POLICY

I, the undersigned _________________(full name) the life assured and ____________________

(Conditional Assignee) under the within Policy of Assurance and the moneys thereby secured and all the benefits attached thereto to the Life Insurance Corporation of India, their successors and assignees absolutely for value received and which may be received hereafter.

Dated this __________________day of __________ |

(Signature of Assured) |

Witness____________________ |

|

Signature___________________

Full name__________________

Designation_________________

Address ___________________

(Signature of Assignee)

Certified that the contents of the above assignment were explained by me to the Assignor in Vernacular and that he/she affixed his/her signature/thumb impression thereto in my presence after thoroughly understanding the same.

(INSTRUCTIONS OVERLEAF) |

(Signature of witness) |

(TO BE COMPLETED IN CASE OF ANTICIPATED ENDOWMENT POLICIES)

(Table Nos. 24, 25 and 26)

Place________________

The Sr. Divisional Manager,

Life Insurance Corporation of India,

Date ________________

Re : Policy No. __________________________

Dear Sir,

With reference to my application dated___________ for a loan under the above Policy, which has

been issued under with Profits Anticipated Endowement Assurance Scheme, I hereby agree that in the event of (1) my surviving ______________ years from the date of commencement of the

Policy and (2) surviving ____________years from the dated of commencement of the Policy, the

Corporation may adjust the Instalment of sum assured then payable towards repayment of the loan outstanding under the Policy, provided however, if any balance of the aforesaid instalment of sum assured is left over after the entire outstanding loan is liquidated by such adjustment such balance should be payable to me.

|

Yours faithfully |

__________________ |

|

__________________ |

|

__________________ Assignee/s |

(Signature of Assured) |

_____________________________________________________________________________

Please detach it from here

INSTRUCTIONS

1.The form of Assignment on the reverse should be detached along the perforation and should be pasted over blank space on the back of the Policy and then completed in which case no Stamp Duty will be payable. If the assignement is executed on a separate paper, the wordings should be copied out on a stamp paper (special adhesive or

2.The Assignor must affix his/her signature to the assignment in the presence of a witness. If the Assignor is not conversant with English, he/she must sign the assignment before an English Knowing person and if he/she be illiterate he/she must affix his/her thumb impression to the assignment before a Magistrate, Special Executive Magistrate or Gazetted Officer. The witness in such case should certify as follows : "he/she affixed his/her signature/left thumb impression thereto in my presence after thoroughly understanding the same."

3.Signature of any other matter written in vernacular should have the English translation thereof written beneath the same.

NOTE : In case of dispute in respect of interpretation of terms the English version shall stand valid.

Form Characteristics

| Fact Name | Details |

|---|---|

| Loan Purpose | The 5196 Application Loan form is used to request a loan against life insurance policies issued prior to June 1, 1969. |

| Repayment Conditions | Repayment of the loan along with interest is required after giving three months' notice, with specific conditions outlined. |

| Interest Rate | The provided interest rate for the loan is 10.5% per annum, compounding half-yearly. |

| Policy Assignment | The policy must be assigned to the Corporation as security for the loan, ensuring they can claim any unpaid amounts. |

| Forfeiture Clause | If the loan is not repaid or interest is not paid within the required time, the policy may be forfeited without notice. |

| State-Specific Laws | Laws governing the use of this form may vary by state. Ensure compliance with local insurance and loan laws. |

Guidelines on Utilizing 5196 Application Loan

To proceed with your application for a loan against your insurance policy, you'll need to fill out Form 5196. It's essential to ensure that all details provided are accurate and complete to facilitate a smooth processing of your request. Below are the steps required to properly fill out the form.

- Date: Write the current date in the space provided.

- Address: Fill in the address where you would like the loan cheque sent.

- Policy Number: Enter the policy number for which you are applying for a loan.

- Loan Amount: Specify the amount you are requesting as a loan, both in numerical and written form.

- Interest Agreement: Affirm your agreement to pay interest at the rate of 10.5% per annum with options for compounding half-yearly.

- Endorsement Agreement: Agree to the conditions surrounding the loan, including the assignment of the policy to the corporation as security.

- Signature(s): Sign the form where indicated. Each applicant must provide their signature.

- Fresh or Further Loan: Indicate whether this is a fresh loan or if it is a further loan on an existing one, based on the conditions set out for loan issuance.

- Return Required Documents: Ensure that you include the receipt for the loan amount and the declaration regarding the assignment along with your application.

What You Should Know About This Form

What is the purpose of the 5196 Application Loan form?

The 5196 Application Loan form is used to request a loan against a life insurance policy that was issued before June 1, 1969. This form is necessary to formally apply for an advance against the policy's benefits. It outlines the terms and conditions under which the loan will be granted, including interest rates and repayment obligations.

What information do I need to provide in the application?

When filling out the 5196 Application Loan form, you will need to provide your policy number, the amount you wish to borrow, and your contact details. You will also need to agree to the interest rate of 10.5% per annum and follow the terms regarding repayment and security for the loan. Make sure to sign the form as well.

What is the interest rate for the loan?

The interest rate for the loan is set at 10.5% per annum. Interest will be compounded every six months, which means it can add up quickly if not paid on time. It's essential to understand these terms before agreeing to the loan.

How is the repayment structured?

Repayment of the loan and any accrued interest is required upon notice, typically after three months of a repayment request. The policyholder must repay the full loan amount and any interest by the specified due dates. Failing to do so may result in the forfeiture of the policy.

What happens if I cannot repay the loan?

If you are unable to repay the loan, the insurance company may forfeit your policy without providing any further notice. They may use the surrender value of the policy to cover the outstanding loan amount and any interest due. Thus, it’s crucial to understand your obligations and seek alternatives if repayment becomes difficult.

Can I still apply for a loan if I have an existing loan on my policy?

Yes, you can apply for a further loan on a policy even if there is an existing loan, as long as the previous loan terms allow it. However, specific rules and conditions apply depending on the loan type and your policy's terms. Make sure to check the details in your policy before submitting your application.

Where should I send the completed application?

You should send the completed 5196 Application Loan form to the Senior Divisional Manager at the Life Insurance Corporation of India. Ensure that the address you use is the one specified for submitting loan applications to avoid delays.

Common mistakes

When filling out the 5196 Application Loan form, several mistakes frequently occur. These errors can delay the loan process or even lead to a denial. Understanding these common pitfalls can help ensure a smoother experience.

One common error is omitting the policy number. This detail is crucial for the processing of the loan. Without it, the institution may struggle to identify and link the application to the correct insurance policy. Ensure this information is clearly written in the designated area.

Another mistake involves incorrectly stating the loan amount. Applicants sometimes choose a figure that exceeds the maximum available or neglect to check the amount they qualify for based on their policy's current value. Taking the time to verify the maximum loan amount can prevent unnecessary complications.

Many applicants fail to provide a complete address for the loan check. The address is essential for the timely delivery of the loan proceeds. Double-check that the address field is filled out entirely to avoid any delays in receiving funds.

Inadequate attention to interest payment details can also cause issues. Some individuals overlook the agreed-upon interest rate or the compounding terms. Read these sections carefully and make sure to acknowledge them explicitly in the application. This will ensure clarity and understanding of financial obligations.

Not understanding the endorsement clause is another frequent mistake applicants make. This includes not being aware that the policy will be assigned to the lender as security. Consequently, a lack of understanding can lead to confusion later. Take time to comprehend this clause to avoid surprises down the road.

Failure to provide necessary signatures is a significant oversight. Applications with missing signatures are often deemed incomplete and can lead to processing delays. Review the form to confirm that all required parties have signed before submission.

Some applicants neglect to send the required supporting documents along with the loan application. This may include a receipt for a prior loan or declaration forms. Prepare and gather all necessary paperwork beforehand to ensure a complete submission.

Finally, a lack of attention to deadlines can derail the process. Many people underestimate how quickly paperwork needs to be submitted, especially if prior loans or other conditions exist. Keep track of time limits to avoid any unnecessary hurdles in the loan approval process.

Documents used along the form

The 5196 Application Loan form is a vital document when applying for a loan against a life insurance policy prior to June 1, 1969. However, it is often accompanied by several other forms and documents that help facilitate the loan process. Understanding these documents can ensure a smoother experience, whether you're applying, managing your loan, or resolving any issues related to the policy.

- Form No. 5200 - Receipt for Loan Advance: This form serves as proof that the borrower has received the loan amount from the Life Insurance Corporation of India. It includes essential details like the amount borrowed and is signed by the borrower and an assignee.

- Assignment Declaration Slip: This slip indicates that the policy has been assigned as collateral for the loan. It confirms the lender’s rights to the policy should the borrower default.

- Policy Document: The original policy document is crucial. It contains the terms and conditions of the insurance coverage and any existing endorsements related to loans.

- Identification Proof: Borrowers need to provide valid identification, such as a driver's license or passport, to verify their identity and ownership of the policy.

- Proof of Income: Documentation such as recent pay stubs or tax returns may be requested to assess the borrower’s ability to repay the loan.

- Authority Note: If the loan is being requested by multiple individuals, this document designates who is authorized to receive the funds. All parties must sign this note.

- Loan Terms and Conditions Leaflet: This document explains the specific terms and conditions associated with the loan, including interest rates and repayment schedules.

- Form for Illiterate Borrowers: This declaration ensures that borrowers who cannot read English have understood the loan application and receipt forms through translation, confirming their acknowledgment of the loan details.

Having these documents ready can make the loan application process more efficient. Each one plays a specific role in ensuring that everything is clear and properly recorded. This clarity can help prevent misunderstandings and potential complications down the road.

Similar forms

-

Form No. 5200 - Receipt for Loan Advance: This document acknowledges the receipt of the loan amount against a specified policy, similar to the 5196 form which requests the loan. Both forms involve confirmation about loans against insurance policies.

-

Form 5205 - Loan Application Declaration: This form is utilized when borrowers cannot read English. Like the 5196 form, it ensures that the terms of the loan are understood by all parties involved, reinforcing clarity in communication.

-

Form No. 5400 - Loan Agreement: The loan agreement outlines the terms of borrowing, comparable to the conditions specified on the 5196 form, including interest rates and repayment details.

-

Form No. 5401 - Termination of Loan: This document formalizes the conclusion of the loan agreement. It echoes the 5196 form's provisions for the repayment of loans and associated obligations.

-

Form No. 5402 - Request for Loan Extension: This document allows for the extension of loan terms, paralleling the original loan request in the 5196 form by providing options for policyholders seeking continued financial support.

-

Form No. 5403 - Loan Prepayment Request: This request form probably shares similarities with Form 5196 since both deal with the repayment of loans, allowing policyholders to manage their outstanding debts.

-

Form No. 5800 - Reserve Policy Loan Agreement: This document covers loans against reserve policies, akin to the 5196 form, which deals with loans in the context of insurance policies.

-

Form No. 5801 - Policy Assignment Form: Required for assigning a policy as collateral for a loan, this form resembles the 5196 by also emphasizing the importance of the assignment of the insurance policy for securing loans.

-

Form No. 5802 - Indemnity Agreement: This agreement protects the lender and outlines obligations similar to those mentioned in 5196. It further explains how repayments will be managed and secured against the assigned policy.

Dos and Don'ts

When completing the 5196 Application Loan form, certain practices can impact your application’s success. Below are tips on what you should and shouldn’t do.

- Do double-check your policy number. Ensure that the policy number you provide corresponds accurately to the policy under which you are applying for the loan.

- Do clearly state the loan amount. Specify the exact amount you wish to borrow, ensuring that it is within the limits allowed by your policy.

- Do read the terms and conditions carefully. Make sure you fully understand the interest rates, repayment process, and any implications of defaulting on the loan.

- Do provide all necessary documentation. Include all supporting documents along with the application form to avoid delays.

- Don’t leave any fields blank. Fill in every required section to prevent processing delays or denials.

- Don’t forget to sign the form. Ensure that all necessary signatures are included, as unsigned forms will not be accepted.

- Don’t overlook the importance of accurate contact information. Provide up-to-date contact details to facilitate communication throughout the loan processing period.

- Don’t rush through the process. Take your time to review each section of the form to avoid mistakes that could complicate your application.

Misconceptions

Misconceptions can create confusion when dealing with the 5196 Application Loan form. Here is a list of nine common misunderstandings:

- This form only applies to policies issued after June 1, 1969: Many believe the 5196 form is only for newer policies. It is designed for loans on policies before this date.

- Interest rates are negotiable: Some applicants think they can negotiate the interest rate. The rate is fixed at 10.5% per annum as specified in the form.

- The loan can be repaid at any time: There is a strict repayment timeline involving a three-month notice for repayment. Failure to adhere may lead to forfeiture of the policy.

- Loan proceeds can be collected immediately: The advances mentioned in the form cannot be paid within six months of settling the loan.

- Partial repayments are accepted: The form states that the Corporation is not required to accept partial repayments. Full amount repayment is necessary.

- The policyholder retains control of the policy: When a loan is taken, the policy is assigned to the Corporation as security, meaning the Corporation has control until the debt is settled.

- Outstanding loans are eliminated upon maturity: If the policy matures or a claim occurs, the Corporation will deduct outstanding loans from the policy amount, which may result in lower returns for the policyholder.

- Assignee signatures are optional: The form requires signatures from all borrowers and assignees, making these signatures vital to the loan process.

- Instructions on the form are suggestions: The instructions are mandatory and must be followed carefully to ensure proper processing of the loan application.

Understanding these misconceptions can help policyholders navigate the loan application process more effectively.

Key takeaways

When filling out the 5196 Application Loan form, keep the following key points in mind:

- Policy Number: Clearly write the correct policy number at the beginning to avoid delays.

- Loan Amount: Specify the amount you are requesting. This can be a fixed amount or the maximum available.

- Interest Rate: Understand that the interest rate is set at 10.5% per annum and compounds half-yearly.

- Endorsement Agreement: Acknowledge that the policy will be assigned to the Corporation as security for the loan and its repayment.

- Repayment Terms: Be aware that you must repay the advance within three months of notice from the Corporation.

- Full Payment Required: The Corporation does not accept partial payments for the loan advance.

- Forfeiture Clause: Failure to repay may result in the policy being forfeited without prior notice.

- Maturity and Claims: If the policy matures or a claim is made, the Corporation may deduct the outstanding loan amount from the policy’s payout.

When you complete the form, ensure that all signatures are present, and the required documents are attached. It is essential to follow each instruction carefully to facilitate a smooth loan approval process.

Browse Other Templates

Masshealth Non Custodial Parent Form - Please ensure your contact information is current for effective communication.

Allergy Action Plan Form - Parents are reassured their child’s safety is prioritized through clear procedures.