Fill Out Your 83077 Form

The 83077 form serves a vital function for beneficiaries claiming benefits from retirement and deferred compensation plans following the death of a participant. Specifically designed for claims under 401(a), 401(k), 403(b), and non-ERISA deferred compensation plans, it requires several key pieces of information for processing. Initially, the form demands participant information, including account numbers, date of birth, and the name of the deceased. Accompanying the claim, an original or certified copy of the death certificate is generally necessary, unless a trustee certifies the participant’s death. Beneficiaries must complete their section, providing personal details such as their relationship to the deceased, Social Security number, and mailing address. Notably, the form also addresses tax implications, including conditions for U.S. residents and non-residents and the mandatory withholding rates that may apply. Options for how to receive the benefits are outlined as well, offering choices like direct rollovers or cash payments. Each section is designed to ensure that the claims process is clear and efficient while remaining compliant with relevant regulations.

83077 Example

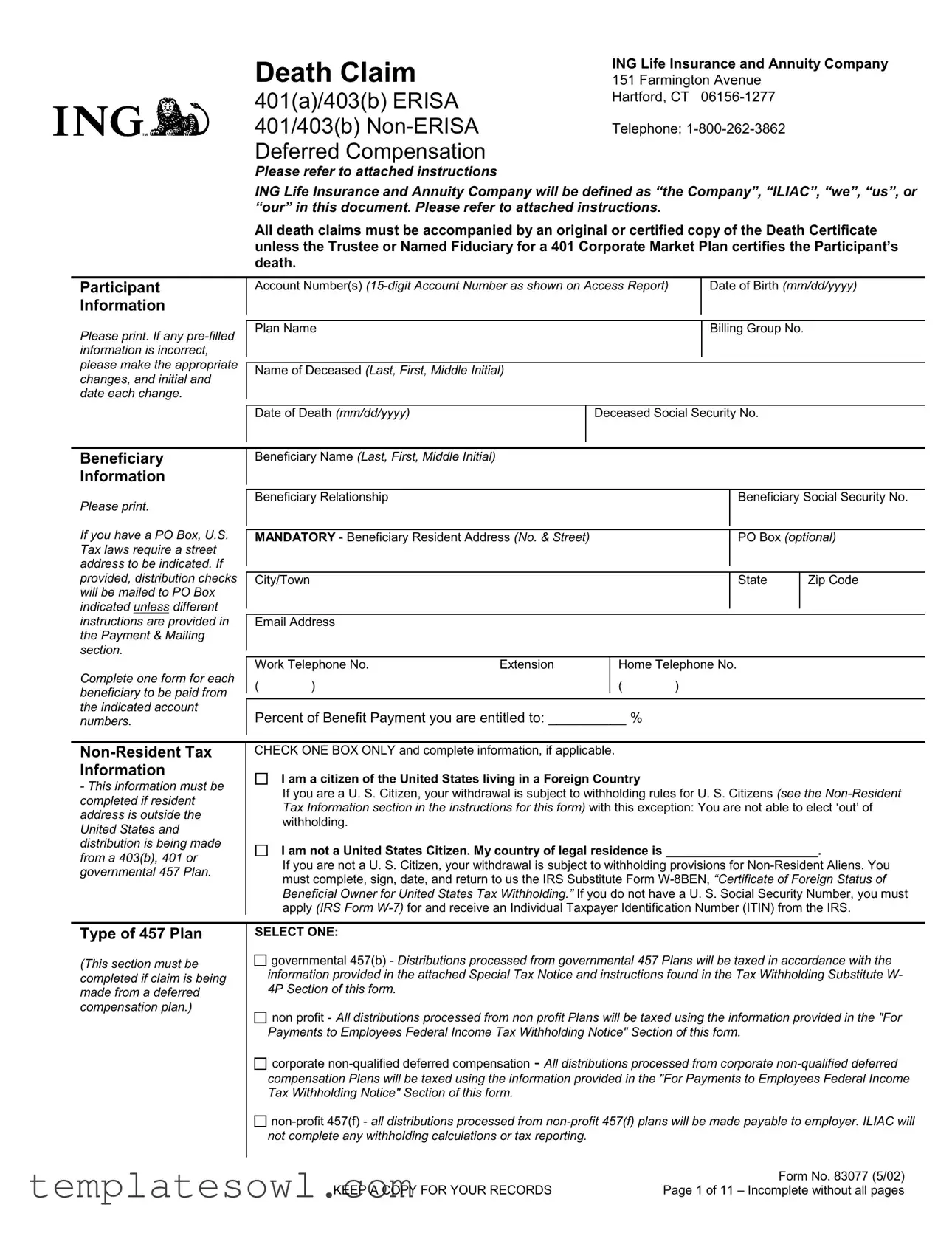

Death Claim

401(a)/403(b) ERISA

401/403(b)

Deferred Compensation

ING Life Insurance and Annuity Company

151 Farmington Avenue

Hartford, CT

Telephone:

Please refer to attached instructions

ING Life Insurance and Annuity Company will be defined as “the Company”, “ILIAC”, “we”, “us”, or “our” in this document. Please refer to attached instructions.

All death claims must be accompanied by an original or certified copy of the Death Certificate unless the Trustee or Named Fiduciary for a 401 Corporate Market Plan certifies the Participant’s death.

Participant Information

Account Number(s)

Date of Birth (mm/dd/yyyy)

Please print. If any

Plan Name |

Billing Group No. |

|

|

Name of Deceased (Last, First, Middle Initial)

Date of Death (mm/dd/yyyy)

Deceased Social Security No.

Beneficiary

Information

Please print.

If you have a PO Box, U.S. Tax laws require a street address to be indicated. If provided, distribution checks will be mailed to PO Box indicated unless different instructions are provided in the Payment & Mailing section.

Complete one form for each beneficiary to be paid from the indicated account numbers.

Beneficiary Name (Last, First, Middle Initial)

Beneficiary Relationship |

Beneficiary Social Security No. |

|

|

|

|

|

|

|

MANDATORY - Beneficiary Resident Address (No. & Street) |

PO Box (optional) |

|

|

|

|

|

|

|

City/Town |

State |

Zip Code |

|

|

|

Email Address |

|

|

|

|

|

|

|

||

|

|

|

|

|

Work Telephone No. |

Extension |

Home Telephone No. |

||

( |

) |

|

( |

) |

Percent of Benefit Payment you are entitled to: __________ %

-This information must be completed if resident address is outside the United States and distribution is being made from a 403(b), 401 or governmental 457 Plan.

CHECK ONE BOX ONLY and complete information, if applicable.

I am a citizen of the United States living in a Foreign Country

If you are a U. S. Citizen, your withdrawal is subject to withholding rules for U. S. Citizens (see the

I am not a United States Citizen. My country of legal residence is ______________________.

If you are not a U. S. Citizen, your withdrawal is subject to withholding provisions for

Type of 457 Plan

(This section must be completed if claim is being made from a deferred compensation plan.)

SELECT ONE:

governmental 457(b) - Distributions processed from governmental 457 Plans will be taxed in accordance with the information provided in the attached Special Tax Notice and instructions found in the Tax Withholding Substitute W- 4P Section of this form.

non profit - All distributions processed from non profit Plans will be taxed using the information provided in the "For Payments to Employees Federal Income Tax Withholding Notice" Section of this form.

non profit - All distributions processed from non profit Plans will be taxed using the information provided in the "For Payments to Employees Federal Income Tax Withholding Notice" Section of this form.

corporate

corporate

|

Form No. 83077 (5/02) |

KEEP A COPY FOR YOUR RECORDS |

Page 1 of 11 – Incomplete without all pages |

Type of Withdrawal

Note: Direct rollovers are only allowed from governmental 457(b), 403(b) or 401 Plans.

If Spouse,

Spousal Continuation if permitted by your Plan

Direct Rollover to an ILIAC IRA

Direct Rollover to a

(Letter of Acceptance required)

If

Cash withdrawal payable to

Cash withdrawal payable to minor Beneficiary (Guardianship papers

are required)

Cash withdrawal payable to employer

If Estate, only this option is available

Payable to Estate

_______________ (% or $)

_______________ (% or $)

_______________ (% or $)

_______________ (% or $)

_______________ (% or $)

_______________ (% or $)

_______________ (% or $)

_______________ (% or $)

_______________ (% or $)

_______________ (% or $)

_______________ (% or $)

Payment and Mailing Information

Check one only. If not indicated check will be made payable to and mailed to the Beneficiary.

Default – Check mailed to Beneficiary Resident Address noted above.

Not applicable if Spousal Continuation elected.

Mail to Beneficiary (as indicated in Beneficiary Information section)

Mail to Trustee

Mail to Other Carrier

Rollover/Transfer to ING Product

Mail to Contract Holder/Employer (Note: This is the only option available if this is a 457(f) Plan)

Make Check Payable to: |

New Account No. |

|

|

Send Check to:

Address (No. & Street / PO Box)

City/Town

State

Zip Code

Electronic Deposit to U. S. Bank Accounts Only

(Optional)

If you would like us to electronically deposit your withdrawal amount to your bank, please provide your bank’s name, complete address, ABA routing number, and your bank account number. (Please verify the correct ABA routing number with your bank.) We will not deposit to a third party account. If the electronic deposit cannot be completed using the information provided, we will issue and mail a check to the Beneficiary. This is not a wire transaction.

Please indicate whether this is a

Checking or

Checking or

Savings Account

Savings Account

Please print.

Account Holder(s) (as it is registered at your bank)

Bank Name |

|

Bank Telephone No. |

|

|

|

|

|

|

|

|

|

Bank Address (No. & Street) |

|

|

|

|

|

|

|

|

|

|

|

City/Town |

|

State |

Zip Code |

|

|

|

|

|

|

|

|

ABA Routing No. (9 digits) |

Bank Account No. |

|

|

|

|

|

|

|

Form No. 83077 (5/02) |

KEEP A COPY FOR YOUR RECORDS |

Page 2 of 11 – Incomplete without all pages |

Tax Withholding (Substitute

Complete only if U. S. Resident Address and the check is payable to Beneficiary and distribution is being made from 403 (b), 401 or governmental 457(b) Plan.

Distributions made payable to beneficiaries from non- qualified, and

Surviving Spouse or Former Spouse who is an Alternate Payee - If the withdrawal is to be made to you (and not directly rolled over to a traditional IRA), we are required by law to withhold 20% Federal Income Tax Withholding from that amount and send it to the Internal Revenue Service (IRS). You will report the tax withheld on your IRS Form 1040, and it will be credited against any Federal Income Tax you owe for the year. The withdrawal is taxed in the year you receive it unless, within 60 days, you roll it over to a traditional IRA.

If you are a Beneficiary other than the Surviving Spouse, or an Estate – If payment is made payable to an individual, 10% Federal Income Tax Withholding will automatically apply unless you elect to have no Federal Income Tax withheld. If payment is made to a

If you are a Surviving Spouse, an Alternate Payee, or another Beneficiary, your withdrawal is not subject to the additional 10% premature Federal Income Tax described in the Special Tax Notice, and you may be eligible to use the special tax treatment for

Even if you decide not to have Federal/State Income Tax Withheld, you are still liable for payment of Federal/State Income Tax on the taxable portion of this payment. You may be subject to tax penalties under the Estimated Tax Payment Rules if your payments of estimated tax and withholding, if any, are not sufficient to cover your tax liability.

Federal Withholding

If any part of this payment is exempt from the 20% mandatory Federal Income Tax Withholding:

GI want Federal Income Tax Withheld from this payment of 10%

GI do not want Federal Income Tax withheld from this payment (available only for payments to an individual).

DEFAULT: If no election is made, 10% Federal Income Tax Withholding will occur.

State Withholding (please refer to the State Income Tax Withholding Notification page of this form)

My residence state for tax purposes is: _________________ (please complete the attached State Income

Tax Withholding Notification form if applicable)

If any part of this payment is exempt from mandatory State Income Tax Withholding:

GI want State Income Tax withheld from this payment (please complete and submit your state of residence’s applicable State Income Tax Withholding Form).

GI do not want State Income Tax withheld from this payment.

DEFAULT: If no election is made, State Income Tax Withholding will occur, if applicable.

Certain states require the following statement: Any person who knowingly presents a false or fraudulent claim for payment of a loss or benefit or knowingly presents false information in an application for insurance may be guilty of a crime and may be subject to fines and confinement in prison.

For Contracts issued in California: For your protection California law requires the following to appear on this form. Any person who knowingly presents a false or fraudulent claim for the payment of a loss is guilty of a crime and may be subject to fines and confinement in state prison.

For Contracts issued in Florida: Any person who knowingly and with intent to injure, defraud, or deceive any insurer files a statement of claim or an application containing any false, incomplete, or misleading information is guilty of a felony of the third degree.

For Contracts issued in New Jersey: Any person who knowingly files a statement of claim containing any false or misleading information is subject to criminal and civil penalties.

For Contract issued in Pennsylvania: Any person who knowingly and with intent to defraud any insurance company or other person files an application for insurance or statement of claim containing any materially false information or conceals for the purpose of misleading, information concerning any fact material thereto commits a fraudulent insurance act, which is a crime and subjects such person to criminal and civil penalties.

|

Form No. 83077 (5/02) |

KEEP A COPY FOR YOUR RECORDS |

Page 3 of 11 – Incomplete without all pages |

Authorized

Signatures and

Certification

Employer, Trustee, or Named Fiduciary’s Authorized Signature and Certification is required for all ERISA plans and employer controlled plans unless there is a separate ILIAC agreement

I certify that:

a)the information stated on this form is correct and complete;

b)the social security number shown on this form is my correct taxpayer identification number and the correct taxpayer identification number for the deceased and that I am not subject to

c)if the Beneficiary’s signature has been obtained in a separate document, the Beneficiary has received from the Trustee or Named Fiduciary the Special Tax Notice regarding application of Federal Income Tax Withholding to certain Plan payments; the Beneficiary’s withholding elections for State and Federal Income Tax purposes, where applicable, have been obtained in a separate document along with the IRS Form Substitute

I further understand that the Company may rely conclusively on these certifications in processing the requested benefits above and that, in the case of any conflicting information, the Company is entitled to rely exclusively on the information contained in this withdrawal request.

I certify that I have received and read the Special Tax Notice section and waive the

I understand that ING Life Insurance and Annuity Company reserves the right to directly or through a third party recover any payments made in excess of amounts to which I am entitled under the terms of the Contract, regardless of the method of payment.

Beneficiary’s Signature |

Date (mm/dd/yyyy) |

|

|

|

|

Employer’s Signature (if applicable) |

Date (mm/dd/yyyy) |

|

|

|

Form No. 83077 (5/02) |

KEEP A COPY FOR YOUR RECORDS |

Page 4 of 11 – Incomplete without all pages |

State Income Tax Withholding Notification

401, 403(b), 408 and Governmental 457 Plan Distribution

ING Life Insurance and Annuity Company

151 Farmington Avenue

Hartford, CT

Telephone:

ING Life Insurance and Annuity Company will be defined as “the Company”, “we”, “us”, or “our” in this document.

Notification

If you are a resident of California, Iowa, Kansas, Maine, Massachusetts, North Carolina, Oklahoma, Oregon, Vermont, or Virginia*, your state requires State Income Tax Withholding on the taxable portion of your distribution from your 401, 403(b), 408 Individual Retirement or Governmental 457 Plan. This State Income Tax Withholding is in addition to the mandatory 20% (or, in some cases, elected 10%) Federal Income Tax Withholding. Please note, when a state cost basis differs from Federal, the Federal cost basis will be used in determining taxability for State Income Tax Withholding purposes.

•If you are a resident of California or Oregon, State Income Tax Withholding will be calculated according to the State Withholding Table (below) for your state unless you complete the bottom portion of this form indicating your election “out” of State Income Tax Withholding, and return it to us with, and to the same Hartford Service Center location as, your Withdrawal Request.

•If you are a resident of Iowa, Kansas, Maine, Massachusetts, Oklahoma, or Vermont, State Income Tax Withholding will be automatically calculated according to the State Withholding Table (below) for your state. These states do not allow an election “out” of State Income Tax Withholding when Federal Income Tax Withholding applies.

•If you are a resident of North Carolina or Virginia*, State Income Tax Withholding will be calculated automatically unless you meet certain income criteria and claim an exemption from withholding. To claim an exemption: for North Carolina complete Form

Please refer to the following table for State Income Tax Withholding rules on distributions from 401, 403(b), Governmental 457and 408 Individual Retirement Plans.

State Withholding |

|

California - |

10% of amount of Federal Income Tax withheld |

Table |

|

||

|

Kansas - |

5% of taxable portion of distribution |

|

|

|

||

|

|

Iowa - |

5% of taxable portion of distribution |

|

|

Maine - |

5% of taxable portion of distribution |

|

Massachusetts - |

5.3% of taxable portion of distribution |

|

|

North Carolina - |

4% of taxable portion of distribution |

|

|

|

Oklahoma - |

5% of taxable portion of distribution |

|

|

Oregon - |

9% of taxable portion of distribution |

|

|

Vermont - |

6.72% of taxable portion of distribution |

|

|

Virginia* - |

4% of taxable portion of distribution |

|

This reflects applicable states and their stated withholding rates effective 1/1/2001. Rates may be modified by |

||

|

the states at any time and additional states may add a requirement to withhold on these types of distributions |

||

|

at any time. Our withholding will reflect the current rate for the applicable state at the time of each individual |

||

|

payment. |

|

|

|

*Note: Virginia State Income Tax is not applicable to 408 plans. |

||

|

|

||

Payee/Account |

I am a resident of (check one) |

||

Information |

California |

Oregon |

|

|

|

||

|

and I wish to elect “out” of State Income Tax Withholding. |

||

|

|

|

|

Payee’s Signature

Date (mm/dd/yyyy)

|

Form No. 83077 (5/02) |

KEEP A COPY FOR YOUR RECORDS |

Page 5 of 11 – Incomplete without all pages |

Death Claim Instructions

401(a)/403(b) ERISA

401/403(b)

Deferred Compensation

ING Life Insurance and Annuity Company

151 Farmington Avenue

Hartford, CT

Telephone:

Good Order |

Good Order is receipt at our Hartford Service Center of this form and any other required information or |

|

|

forms (e.g., original or certified copy of the Death Certificate) that has been accurately and entirely |

|

|

completed, and includes the signature of you, the Beneficiary, and where appropriate, the Employer’s |

|

|

signature. Forms and any other requested information not received in Good Order, as we determine, may |

|

|

be returned to you for correction and processed upon |

|

|

Center. |

|

|

For those customers where the terms of the Contract allow us to accept a Plan Sponsor’s or Plan Trustee’s |

|

|

certification of the Participant’s death in lieu of the Death Certificate, when a death benefit payment |

|

|

request is made, we will not require an original or certified copy of the Death Certificate. If a Death |

|

|

Certificate is received it will become part of our file and will not be returned. |

|

|

|

|

Terms and |

The withdrawal effective date will be the date our Hartford Service Center has received the Withdrawal |

|

Conditions |

Request Form and any other required forms in Good Order. |

|

|

For purposes of calculating the amount, the value of the vested individual account will be determined after |

|

|

the final close of business of the New York Stock Exchange on the valuation date we have received the |

|

|

Death Claim Form and any other required forms in Good Order at our Hartford Service Center. A valuation |

|

|

date is any normal business day, Monday through Friday, that the New York Stock Exchange is open. |

|

|

There may be legal or tax considerations in connection with this withdrawal. Therefore, you may wish to |

|

|

consult your legal or tax advisor before submitting this Withdrawal Request. |

|

|

The furnishing of this form by us does not constitute an admission that there is a Contract in force. The |

|

|

undersigned warrants that no insolvency or bankruptcy proceedings are pending against the Contracts or |

|

|

against any interest of the undersigned therein. |

|

|

Withdrawals may be subject to market value adjustments. For partial withdrawals where a specific dollar |

|

|

amount of withdrawal has been requested, the check will be for the amount requested, less any applicable |

|

|

withholding for income taxes. For any other full or partial withdrawal, all adjustments will be deducted from |

|

|

the withdrawal amount requested on this form. |

|

|

Funds withdrawn from a Guaranteed Term in the Guaranteed Accumulation Account (GAA) prior to |

|

|

maturity are subject to a Market Value Adjustment (MVA). The MVA may increase in the current value. |

|

|

Please refer to the GAA prospectus for more information. |

|

|

The Code requires that distribution of death proceeds begin within a certain period of time. Generally, |

|

|

either payments must begin by December 31 of the year following the year of the Participant’s death, or |

|

|

the entire value of the your benefits must be distributed by December 31 of the fifth year following the year |

|

|

of the Participant’s death, unless the Beneficary is the Spouse. If the Beneficiary is the Spouse, distribution |

|

|

of the Participant’s benefits may be deferred until the end of the year in which the Participant would have |

|

|

attained age 70½. |

|

|

|

|

Beneficiary |

For those plans that have us as the Beneficiary Recordkeeper, this section must agree with the |

|

Information |

previous Beneficiary Designation recorded. |

|

|

For all other plans, we are entitled to rely exclusively on the Beneficiary information contained in |

|

|

this Withdrawal Request Form that has been provided and signed by the Beneficiary or Employer |

|

|

(if applicable). |

|

|

If multiple Beneficiaries, each Beneficiary must complete a Death Claim Form. |

|

|

|

|

Type of Withdrawal |

Please complete this information in its entirety. If Minor, |

|

|

Estate, you may defer distribution until the end of the fifth year following the Participant’s death. Please |

|

|

contact your Representative if you are interested in this option. |

|

|

|

|

Payment and Mailing |

Please complete this information in its entirety. |

|

Information |

|

|

|

|

|

Electronic Deposit to |

Take advantage of a convenient (avoid trips to your bank or mail delays) method of having your withdrawal |

|

U. S. Bank Accounts |

electronically deposited to your bank account. |

|

Only |

To ensure your payment is accurately deposited into your bank account please verify with your |

|

(Optional) |

||

bank or financial institution the proper instructions for Electronic Deposits. |

||

|

|

Form No. 83077 (5/02) |

KEEP A COPY FOR YOUR RECORDS |

Page 6 of 11 – Incomplete without all pages |

Income Tax

Withholding Notice

and Election

If any portion of the taxable withdrawal is not subject to mandatory 20% Federal Income Tax Withholding, complete this section and select the desired withholding option. This would generally include death benefits payable to a

Tax Reporting Information

On withdrawals made payable to a Beneficiary or direct rollovers, we will report distribution on IRS Form

This information is required only if your residency is outside the United States.

If you are a United States Citizen and the withdrawal is delivered to a

If you are not a United States Citizen and the withdrawal is delivered to a

Overpayment Recovery

I understand that ING Life Insurance and Annuity Company reserves the right to directly or through a third party recover any payments made in excess of amounts to which you are entitled under the terms of the Contract, regardless of the method of payment.

Authorized

Signatures and

Certification

This section must be signed by the Beneficiary. In addition to verifying that the information regarding this withdrawal request is correct and complete, the Beneficiary must certify that she/he has received and read the Special Tax Notice section and waives the

|

Form No. 83077 (5/02) |

KEEP A COPY FOR YOUR RECORDS |

Page 7 of 11 – Incomplete without all pages |

Special Tax Notice

ING Life Insurance and Annuity Company

151 Farmington Avenue

Hartford, CT

Telephone:

ING Life Insurance and Annuity Company will be defined as “the Company”, “we”, “us”, or “our” in this document.

Regarding Payments from your Account

This notice contains important information you will need before you decide how to receive benefits from your 403(b) Program, 401 Qualified Plan or, Governmental 457 Plan account. We are required to provide this notice to you at least 30 days, but no more than 90 days, before the date of distribution. You have the right to consider whether to elect a direct rollover for at least 30 days after the notice is provided. Your Employer’s retirement program may provide that by completing and returning the distribution request form in less than 30 days, you elect to waive the

If you are a participant or beneficiary under a Governmental 457 Plan, your plan may require that you choose the manner in which your deferred benefits will be paid within a specified period of time. Please consult with your plan administrator or us to determine the election period applicable to your benefits.

All or any portion of your payment that is an “eligible rollover distribution” may be either paid in a “direct rollover” or paid to you. A direct rollover is a direct payment of benefits to an “eligible retirement plan that accepts rollovers.” An “eligible retirement plan” is defined as a traditional Individual Retirement Arrangement (IRA), a 403(b) Program, a 401 Qualified Plan or a Governmental 457 Plan. Please note that a “traditional IRA” does not include a Roth IRA, SIMPLE IRA, or Education IRA (also known as a Coverdell Education Savings Account).

Payments that |

The following payments cannot be rolled over and must be paid to you. Note that if a portion of your payment |

cannot be Directly |

is taxable and is not an eligible rollover distribution, it is subject to 10% voluntary federal income tax |

Rolled Over |

withholding. |

|

|

|

Hardship Withdrawals and Unforeseeable Emergency Withdrawals – Hardship withdrawals from a 403(b) |

|

Program or 401(k) Qualified Plan and unforeseeable emergency withdrawals from a Governmental 457 Plan |

|

cannot be rolled over. |

Payments Spread Over Long Periods - You cannot roll over a payment if it is part of a series of equal or almost equal payments that are made at least once a year and that will last for:

•your lifetime (or your life expectancy),

•your lifetime and your Beneficiary’s lifetime (or joint life expectancies), or

•a period of ten years or more.

Required Minimum Distribution Payments - A certain portion of your distribution payment cannot be rolled over if it is a “required minimum payment.” (Certain payments made upon a Participant’s death are required minimum payments and cannot be rolled over.) Payments which are minimum required distributions generally must commence by April 1st of the calendar year following the calendar year in which the Participant (1) attains age 70½ or (2) retires, whichever is later. However, distributions from the 403(b) Program attributable to the 403(b) account value as of December 31, 1986 must begin by April 1st following the calendar year in which a Participant reaches age 75 or retires, whichever is later. If you are a Participant in a 401 Qualified Plan and you are considered a 5% Owner in the Employer sponsoring the Plan, special rules govern the timing of your required minimum distribution. If you attained age 70½ prior to January 1996 special rules apply to the definition of required minimum payment.

Corrective Distributions - A distribution that is made to correct a failed nondiscrimination test or because legal limits on certain contributions were exceeded cannot be rolled over.

Loans Treated as Distributions - The amount of a plan loan that becomes a taxable deemed distribution because of a default cannot be rolled over. However, a loan offset amount is eligible for rollover, as discussed in the “Special Tax Treatment” section below.

Direct Rollover |

You may choose a direct rollover of all or any portion of your payment that is an “eligible rollover distribution.” |

|

In a 403(b) Program, 401 Qualified Plan or Governmental 457 Plan direct rollover, payment is made to an |

|

“eligible retirement plan” that accepts rollovers. Your distribution cannot be rolled over to a Roth IRA, a |

|

SIMPLE IRA, or an Education IRA because these are not eligible retirement plans. If you choose a direct |

|

rollover, you are not taxed on the taxable portion of the payment until it is distributed from the traditional IRA, |

|

403(b) Program, or 401 Qualified Plan or from a Governmental 457 Plan. |

|

|

|

Form No. 83077 (5/02) |

KEEP A COPY FOR YOUR RECORDS |

Page 8 of 11 – Incomplete without all pages |

Direct Rollover |

Direct Rollover to a Traditional IRA– You can open a traditional IRA to receive the direct rollover. If you |

|

(continued) |

||

choose to have your payment made directly to a traditional IRA, contact an IRA Sponsor (usually a financial |

||

|

||

|

institution) to find out how to have your payment made in a direct rollover to a traditional IRA at that institution. |

|

|

If you are unsure of how to invest your money, you can temporarily establish a traditional IRA to receive the |

|

|

payment. However, in choosing a traditional IRA, you may wish to consider whether the traditional IRA you |

|

|

choose will allow you to move all, or a part of, your payment to another traditional IRA at a later date, without |

|

|

penalties or other limitations. See Internal Revenue Service (IRS) Publication 590, “Individual Retirement |

|

|

Arrangements,” for more information on traditional IRAs (including limits on how often you can rollover |

|

|

between IRAs). |

|

|

Direct Rollover from a 403(b) Program, 401 Qualified Plan, or Governmental 457 Plan to an eligible |

|

|

retirement plan - If you are employed by a new Employer that has an eligible retirement plan, ask the |

|

|

Employer whether it will accept your rollover. Even if the Employer’s plan does not accept the rollover you |

|

|

can choose a direct rollover to a traditional IRA. If the Employer’s plan accepts your rollover, the plan may |

|

|

provide restrictions on the circumstances under which you may later receive a distribution of the rollover |

|

|

amount or may require spousal consent to any subsequent distribution. |

|

|

Direct Rollover of a Series of Payments - If you receive eligible rollover distributions that are paid in a series |

|

|

for less than ten (10) years, your choice of whether or not to roll over the payment will apply to all later |

|

|

payments in the series until you change your election. You are free to change your election for any later |

|

|

payment in the series. |

Direct Rollover of

a)Rollover into a Traditional IRA. You can roll over your

b)Rollover into a 401(a) Qualified Plan. You can roll over

c)Rollover into a 403(b) program. You can roll over

NOTE:

•You CANNOT roll over

•If you want to roll over your

•You cannot first roll over

Payment Paid to |

Mandatory Withholding - If any portion of an eligible rollover distribution is paid to you, we are required by |

You |

federal law to withhold 20% of the taxable amount and send it to the IRS as Federal Income Tax Withholding. |

|

For example, if your rollover distribution is $10,000, only $8,000 will be paid to you because the Plan must |

|

withhold $2,000 or 20% of the taxable amount, as Federal Income Tax. You will need to report the $10,000 as |

|

a taxable payment from the 403(b) Program, 401 Qualified Plan or Governmental 457 Plan and the $2,000 as |

|

Federal Income Tax withheld on your IRS Form 1040. The $2,000 will be credited against any Federal Income |

|

Tax you owe for the year. The payment is taxed in the year you receive it unless, within sixty (60) days of |

|

receipt, you roll it over to a traditional IRA or to another type of eligible retirement plan that accepts rollovers. |

|

(see |

|

State Withholding - If State Income Tax Withholding is required on the payment, or if you elect to have it |

|

withheld, we will withhold such tax and send it to the state. For states that impose a State Income Tax on |

|

designated distributions (Pension Plans), we will assume that your state follows the Federal tax basis for state |

|

taxation purposes. In addition, if the state requires income tax withholding, we will apply the State Income Tax |

|

Withholding rate against the federal taxable amount. |

|

If a state requires mandatory Income Tax Withholding and a state withholding certificate/form is not submitted |

|

in a timely manner, State Income Tax Withholding will be deducted based on the appropriate state default |

|

withholding election and rate. |

|

|

|

Form No. 83077 (5/02) |

KEEP A COPY FOR YOUR RECORDS |

Page 9 of 11 – Incomplete without all pages |

Payment Paid To |

State Income Tax Withholding and Reporting will be determined using your legal residency at the time the |

|

You (continued) |

distribution is made. |

|

|

The tax determination of your distribution can be complex and does vary based on your state of residency. |

|

|

You may want to consult with your own tax advisor to determine the proper tax treatment of your distribution. |

|

|

Voluntary Withholding - If any portion of your payment is not an eligible rollover distribution but is taxable, |

|

|

the mandatory withholding rules do not apply. A 10% voluntary Federal Income Tax Withholding will |

|

|

automatically apply unless you elect to have no Federal Income Tax withheld. |

|

|

||

|

over all or part of it to an eligible retirement plan that accepts rollovers. If you decide to roll over, you must |

|

|

make the rollover within sixty (60) days after you receive the payment. The taxable portion of your payment |

|

|

that is rolled over will not be taxed until you take it out of the eligible retirement plan. You may roll over up to |

|

|

100% of the amount that was an eligible rollover distribution, including an amount equal to the 20% that was |

|

|

withheld. If, within the sixty (60) day period, you choose to roll over 100%, you must contribute other money to |

|

|

the eligible retirement plan to replace the 20% that was withheld. If you roll over only the 80% that you |

|

|

received, the 20% that was withheld will be included in your taxable income for the year. |

|

|

For example, if your eligible rollover distribution from an eligible retirement plan was $10,000 and you chose to |

|

|

have it paid to you, you will receive $8,000, and $2,000 will be sent to the IRS as Federal Income Tax |

|

|

Withholding. Within sixty (60) days after receiving the $8,000 you may roll over up to $10,000 to an eligible |

|

|

retirement plan that accepts rollovers. To do this, you roll over the $8,000 you received from the plan, and |

|

|

you will have to find $2,000 from other sources. In this case, the entire $10,000 is not taxed until you take it |

|

|

out of the eligible retirement plan, and you may be eligible to receive a refund of the $2,000 withheld when you |

|

|

file your income tax return. |

|

|

If, on the other hand, you roll over only $8,000, the $2,000 you did not roll over is taxed in the year it was |

|

|

withheld. When you file your income tax return, you may get a refund of part of the $2,000 withheld. (However, |

|

|

any refund is likely to be larger if you roll over the entire $10,000.) |

|

|

.Additional 10% Premature Withdrawal Tax If You Are Under Age 59½ - If you receive a payment before |

|

|

you reach age 59½ (and no other statutory exemption applies) and you do not roll it over, you may have to |

|

|

pay an extra premature distribution tax, in addition to Federal Income Tax. Unless an exception applies, you |

|

|

will have to pay this extra tax, equal to 10% of the taxable portion of the payment, when you file your income |

|

|

tax return. The additional 10% tax generally does not apply to (1) payments that are paid after you separate |

|

|

from service with your Employer during or after the year you reach age 55, (2) payments that are paid |

|

|

because you retire due to disability, (3) payments that are paid as equal (or almost equal) payments over your |

|

|

life or life expectancy (or your and your Beneficiary’s lives or life expectancies), (4) dividends paid with respect |

|

|

to stock by an Employee Stock Ownership Plan (ESOP) as described in IRS Code Section 404(k), (5) |

|

|

payments that are paid directly to the government to satisfy a federal tax levy, (6) payments that are paid to an |

|

|

Alternate Payee under a Qualified Domestic Relations Order (QDRO), or (7) payments that do not exceed the |

|

|

amount of your deductible medical expenses. See IRS Form 5329 for more information on the additional 10% |

|

|

tax. |

|

|

This additional 10% tax is not applicable to distributions from a Governmental 457 Plan, but will be applicable |

|

|

to monies originally contributed to another eligible retirement plan (e.g. 401, 403(b) or traditional IRA) subject |

|

|

to this tax which were subsequently rolled over to the Governmental 457 Plan. Any amount rolled from a |

|

|

Governmental 457 plan to another type of non governmental eligible retirement plan (e.g. 401, 403(b) or |

|

|

traditional IRA) will become subject to the additional 10% tax, if it is distributed to you before you reach age |

|

|

59 ½, unless one of the exceptions applies. |

|

|

|

|

Surviving |

With some exceptions, the rules summarized above also generally apply to payments to Surviving Spouses of |

|

Spouses, |

Employees, and to Spouses or former Spouses, who are Alternate Payees. (You are an Alternate Payee if |

|

Alternate Payees |

your interest in a 403(b) Program or 401 Qualified Plan results from a “Qualified Domestic Relations Order” or |

|

your interest in a Governmental 457 Plan results from a plan approved or certified “Domestic Relations Order” |

||

and Other |

||

issued in connection with a divorce or legal separation.) Some of these rules also apply to a deceased |

||

Beneficiaries |

||

Employee’s Beneficiary who is not a Spouse. |

||

|

||

|

• If you are a Surviving Spouse or an alternate payee (spouse or former spouse), you have the same |

|

|

choices as the employee; therefore you may choose to have an eligible rollover distribution paid in a |

|

|

direct rollover to an eligible retirement plan that accepts rollovers or paid to you. If you have the payment |

|

|

paid to you, you may keep it or roll it over yourself to an eligible retirement plan. If you do not request a |

|

|

direct rollover and you have the payment paid to you, we are required by federal law to withhold 20% of |

|

|

the taxable amount and send it to the IRS as Federal Income Tax Withholding. |

|

|

• If you are a Beneficiary other than the Surviving Spouse or alternate payee (spouse or former |

|

|

spouse), you cannot choose a direct rollover and you cannot roll over the payment yourself. A 10% |

|

|

Federal Income Tax Withholding will automatically apply unless you elect to have no Federal Income Tax |

|

|

withheld. |

|

|

If you are a Surviving Spouse, an Alternate Payee, or another Beneficiary, your payment is generally not |

|

|

subject to the additional 10% Premature Withdrawal Tax described above. You may also be able to use the |

|

|

special tax treatment for |

|

|

Stock, as described below. If you receive a payment because of the Employee’s death, you may be able to |

|

|

treat the payment as a |

|

|

or not the Employee had five (5) years of participation in the 401 Qualified Plan. |

|

Form No. 83077 (5/02) |

KEEP A COPY FOR YOUR RECORDS |

Page 10 of 11 – Incomplete without all pages |

Form Characteristics

| Fact Title | Fact Description |

|---|---|

| Purpose of the Form | The 83077 form is used for submitting a death claim for various retirement plans under ERISA and Non-ERISA guidelines. |

| Issuing Company | This form is issued by ING Life Insurance and Annuity Company, located in Hartford, Connecticut. |

| Required Documentation | An original or certified copy of the death certificate is mandatory, unless a Trustee certifies the Participant's death. |

| Beneficiary Details | Separate forms must be completed for each beneficiary entitled to a payment from the account. |

| Tax Information | U.S. tax laws require accurate reporting for both residents and non-residents when withdrawing from 401 or 403(b) plans. |

| Type of Withdrawal | Various withdrawal options are available, including cash withdrawal or direct rollover to an IRA. |

| Federal Tax Withholding | Federal income tax withholding applies, with specific rates depending on whether the beneficiary is a spouse or not. |

| State Tax Withholding | Certain states mandate income tax withholding on distributions. It's important to check state-specific laws. |

| Fraud Statement | The form includes a statement warning of penalties for submitting false information, which is a crime in many states. |

| Signature Requirement | Employer, Trustee, or Named Fiduciary must sign the form for ERISA plans unless a separate agreement exists. |

Guidelines on Utilizing 83077

The next steps involve carefully completing the 83077 form. This process is essential to establish the details associated with the death claim and ensure that the appropriate beneficiaries receive their benefits efficiently. Here are the steps to follow:

- Gather Required Documents: Obtain the original or certified copy of the death certificate. If applicable, ensure the Trustee or Named Fiduciary certifies the participant's death.

- Fill Out Participant Information: Enter the account number, date of birth, plan name, billing group number, name of the deceased, date of death, and the deceased’s Social Security number. Ensure all information is accurate and print legibly.

- Provide Beneficiary Information: For each beneficiary, fill out their name, relationship to the deceased, Social Security number, resident address (with street address), PO Box (if applicable), and contact information. Specify the percentage of benefit payment each beneficiary is entitled to receive.

- Complete Non-Resident Tax Information: If the beneficiary's address is outside the United States, check the appropriate box indicating whether the beneficiary is a U.S. citizen living abroad or not.

- Select the Type of Withdrawal: Indicate the type of withdrawal requested, such as a cash withdrawal, direct rollover, or payment to the estate. Check only one box that applies.

- Fill Out Payment and Mailing Information: Indicate how the payment should be processed and where it should be sent. Provide any necessary banking information if electronic deposit is selected.

- Tax Withholding Section: Complete the federal and state income tax withholding information. Choose whether you want federal and state taxes withheld or not. Make sure this section is filled out completely if applicable.

- Sign and Date: Ensure that both the beneficiary and the employer (if applicable) sign and date the form. This certification confirms the accuracy of the information provided.

- Review and Submit: Before submitting, review all entries for accuracy. Once confirmed, submit the completed form along with the death certificate to the ING Life Insurance and Annuity Company at the provided address.

What You Should Know About This Form

What is Form 83077?

Form 83077 is a document used to file a death claim related to retirement plans governed by ERISA, such as 401(a), 403(b), and certain types of deferred compensation plans. This form is particularly utilized by the beneficiaries of deceased participants in these plans to claim any benefits that may be due upon the participant's death.

Who should complete Form 83077?

The beneficiaries of a deceased participant should complete Form 83077. The form requires detailed information about both the deceased, including their account number and Social Security number, as well as information about the beneficiary, such as their relationship to the deceased and pertinent contact information.

What documents are required when submitting Form 83077?

An original or certified copy of the Death Certificate must accompany Form 83077, unless a trustee or named fiduciary certifies the participant's death. This requirement helps ensure the authenticity of the claim being made.

How is the benefit amount determined?

Benefits are typically distributed according to the plan’s rules and the relationship of the beneficiary to the deceased. The form provides a section for beneficiaries to indicate the percentage of benefit payment they are entitled to receive from the account. It's important for beneficiaries to understand their entitlement based on plan documents.

What is the significance of the Tax Withholding information on Form 83077?

The Tax Withholding section is crucial as it outlines how much tax may be withheld from any distributions. Beneficiaries who are U.S. residents should be aware that a mandatory 20% federal income tax withholding applies unless they opt not to have it withheld. States may also impose their own withholding requirements based on the beneficiary's state of residence.

Can Form 83077 be submitted electronically?

Submitting Form 83077 typically requires a physical signature and is not designed for electronic submission. It is advisable for beneficiaries to send the completed form and accompanying documentation directly to ING Life Insurance and Annuity Company via mail, to ensure that their claim is processed properly.

How long does it take for a claim to be processed after submitting Form 83077?

The processing time for claims submitted on Form 83077 can vary depending on completeness and the specific circumstances surrounding each claim. Beneficiaries are encouraged to allow some time for processing and to check in with the company if they have not received acknowledgment of their claim after a reasonable period, usually defined in the company’s internal policies.

What should I do if the information on Form 83077 is incorrect?

If any information on the form is found to be incorrect, beneficiaries should make the necessary corrections, initial and date each change. It is essential to ensure that all information is accurate to prevent delays in processing and to secure the correct benefit amount.

How can I contact ING Life Insurance and Annuity Company for questions about Form 83077?

Beneficiaries can reach out to ING Life Insurance and Annuity Company by calling their service number at 1-800-262-3862. This hotline can provide assistance regarding the form, processing of claims, and any further questions that might arise.

Common mistakes

Filling out Form 83077 can be a daunting task, especially during an emotional time. Many individuals make common mistakes when completing this form that can delay processing. Understanding these errors can help ensure that the claim is handled efficiently.

One frequent error is failing to include the original or certified copy of the Death Certificate. This document is essential for processing the death claim. Without it, the claim cannot proceed, leading to unnecessary delays. Make sure to include this vital paperwork with your submission.

Another mistake is providing incorrect information in the Participant Information section. It is crucial to verify that the name of the deceased, dates of birth and death, and Social Security number are accurate. Any discrepancies can complicate the claims process and may require additional paperwork.

People often forget to initial and date any changes made to pre-filled information. If any detail is incorrect, it must be corrected and noted clearly. Neglecting to do so can cause confusion and lead to further complications.

Some individuals mistakenly assume that a PO Box is sufficient for their mailing address. U.S. Tax laws require a physical street address, especially for distribution checks. Failure to provide the correct information can cause delays in receiving the funds.

Be aware of selecting the wrong type of withdrawal. This form includes several options for distributions and rollovers. Choosing the incorrect one can result in your request being inadequate or denied.

Many individuals overlook the Non-Resident Tax Information section if their address is outside the United States. This section is mandatory and must be filled out correctly to ensure that the proper withholding taxes are applied.

Another common issue arises when including beneficiary information. Each beneficiary must have a separate form to ensure accurate distributions. Many people mistakenly try to list multiple beneficiaries on one form, which can lead to processing errors.

Lastly, people sometimes neglect to sign and date the form. Omitted signatures can halt the entire process, requiring further follow-up. It is essential to review the form one last time before submission to ensure that all required signatures are present.

A thoughtful and careful approach to completing Form 83077 will help minimize errors and ensure that claims are processed smoothly. Taking the time to double-check all information can save significant time and effort for everyone involved.

Documents used along the form

The 83077 form serves as a critical document for beneficiaries of retirement plans, specifically concerning death claims related to 401(a)/403(b) ERISA and non-ERISA deferred compensation plans. However, additional documents and forms often accompany it to ensure compliance with guidelines and proper processing. Below is a list of commonly used forms and documents, each with a brief description.

- IRS Form W-8BEN: This form is essential for non-U.S. citizens to certify their foreign status for tax purposes. When claiming benefits, it helps determine the correct amount of withholding from distributions.

- IRS Form W-4P: This form informs the payer of the desired federal income tax withholding for pension or annuity payments. Beneficiaries may opt to have no withholding or specify a percentage to withhold.

- State Income Tax Withholding Notification: This document outlines the rules governing state income tax withholding based on a beneficiary's residency. It is crucial for ensuring the correct state tax is withheld from the distribution.

- IRS Form W-7: This form is necessary for individuals who do not have a Social Security Number and need to obtain an Individual Taxpayer Identification Number (ITIN) for tax reporting purposes.

- Beneficiary Designation Form: This form specifies who the beneficiaries of the retirement plan are. Updating this documentation is vital to ensure that distributions are correctly directed according to a participant's wishes.

- Death Certificate: An original or certified copy of the death certificate is typically required to validate the claim. This document provides legal confirmation of the participant’s passing and is critical for the processing of death claims.

Being aware of these documents is vital for beneficiaries navigating the claims process. Ensuring all required paperwork is accurate and submitted in a timely manner can help alleviate delays and ensure beneficiaries receive what they are entitled to under the plan.

Similar forms

- Form 5500: This is a report filed annually by employee benefit plans, including 401(k) and 403(b) plans. Like Form 83077, it addresses retirement benefits and compliance with ERISA (Employee Retirement Income Security Act). Both forms require accurate information about participants and beneficiaries for processing claims and monitoring plan health.

- Form W-4R: Used by individuals to designate tax withholding from retirement plan distributions, it shares similarities with the 83077 form in that both require tax-related information and election choices for beneficiaries taking distributions.

- IRS Form W-8BEN: This form applies to non-U.S. residents to claim a reduced rate of withholding tax on certain U.S. income. Like the 83077 form, it collects essential tax information from beneficiaries, specifically addressing those outside the U.S.

- Form 1099-R: This form reports distributions from pensions, annuities, retirement plans, and IRAs. Similar to the 83077 form, it tracks how payments were made to beneficiaries and calculates tax withholding.

- Beneficiary Designation Form: This document specifies who will receive benefits upon a participant’s death, mirroring the 83077 form’s focus on beneficiary information, including relationships and allocations.

- Plan Loan Application Forms: For participants who borrow from their retirement accounts, these forms determine the eligibility and repayment terms. They are similar because they both manage relationship details and participant contributions that affect beneficiaries.

- Special Tax Notice: Another document provided to participants regarding tax implications of plan distributions. Similar to the 83077, it comprehensively informs recipients about taxation so beneficiaries can make informed decisions.

- Distribution Request Form: This is used when participants request a withdrawal from their retirement account. Like the 83077 form, it tracks participant information, distribution amounts, and tax implications to ensure compliance and accuracy.

Dos and Don'ts

When filling out the 83077 form, it is essential to follow specific guidelines to ensure a smooth application process. Below are important considerations, including both what to do and what to avoid.

- Do: Provide an original or certified copy of the Death Certificate, unless certified by the Trustee for a 401 Corporate Market Plan.

- Do: Verify that all pre-filled information is accurate. Make necessary changes, initial, and date each modification.

- Do: Complete a separate form for each beneficiary. Ensure that all required fields are filled in, especially the beneficiary's social security number and address.

- Do: Check the appropriateness of the withholding tax options selected based on your residency status.

- Don't: Submit the form without double-checking for errors or missing information. Incomplete forms can delay processing.

- Don't: Ignore the need for a street address if you have a PO Box; this is required by U.S. tax laws.

- Don't: Forget to have the necessary signatures, especially from the Employer or Trustee if it is an ERISA plan.

- Don't: Assume that selecting 'out' of tax withholding without proper forms or exemptions will be allowed; confirm your state's rules first.

Misconceptions

Misconceptions about Form 83077 can lead to confusion when filing death claims or making withdrawals. Here are nine common myths clarified:

- The form is only for ERISA plans. While commonly associated with ERISA plans, Form 83077 can also be used for non-ERISA plans, including deferred compensation plans.

- A death certificate is not always needed. An original or certified copy of the death certificate is required unless a trustee certifies the participant’s death.

- All beneficiaries must use the same form. Each beneficiary entitled to payment must complete a separate form to facilitate their distribution from the account.

- There is no tax withholding on distributions. Depending on the type of withdrawal and beneficiary relationship, tax withholding may apply, including mandatory federal withholding in some cases.

- You can direct rollover to any IRA without restrictions. Direct rollovers are only permitted under specific conditions and to certain types of accounts, so it’s important to check eligibility.

- Changes made to pre-filled information should not be initialed. Any corrections to pre-filled fields must be initialed and dated to confirm their validity.

- The form can be submitted without an authorized signature. An authorized signature from an employer or trustee is required for ERISA plans, ensuring the legitimacy of the request.

- Using a PO Box for communications is sufficient. While a PO Box can be included, U.S. tax laws require a street address to be provided for all official mailing.

- All claims will be processed within a specific timeframe. Processing times vary based on verification needs and the specifics of the claim, so patience is often necessary.

Key takeaways

When filling out and using the 83077 form, several important points should be kept in mind for an effective and compliant submission. Here are key takeaways:

- Ensure you attach an original or certified copy of the Death Certificate, unless exempted by the Trustee.

- Provide accurate Participant Information, including the account number, date of birth, and name of the deceased.

- Accurately list Beneficiary Information, including names, relationships, and social security numbers.

- Use a street address for beneficiaries; PO Boxes alone are insufficient under U.S. tax laws.

- Complete a separate form for each beneficiary to ensure proper distribution and processing.

- For non-U.S. residents, select the appropriate box and provide necessary tax documentation, such as IRS Form W-8BEN.

- Identify the type of 457 plan clearly, as this affects tax treatment and withholding obligations.

- Understand the implications of different types of withdrawals. Some options, like direct rollovers, may have restrictions.

- Complete the Payment and Mailing Information section carefully to avoid delays in receiving benefits.

- Familiarize yourself with tax withholding rules to make informed elections regarding Federal and State taxes.

Following these guidelines will help minimize errors and ensure compliance when using the 83077 form for death claims associated with retirement plans.

Browse Other Templates

Ct Security Guard Card Renewal - Please adhere to all deadlines to maintain your registration without interruption.

Social Security Earnings Request Form,Earnings Information Request F4,Form for Earning Details,SSA Earnings Statement Application,Request for Earnings Record,Social Security Earnings Inquiry Form,SSA Earnings Certification Application,Earnings Inform - The form is designed for straightforward completion to assist individuals with their requests.

Corporate Officer Waiver Form,Workers’ Compensation Exclusion Statement,Iowa Employers’ Liability Rejection Form,Corporate Liability Exclusion Document,Workers’ Comp Coverage Rejection Notice,Employer Liability Coverage Opt-Out Form,Corporate Officer - This form allows corporate officers to voluntarily reject workers’ compensation coverage under specific Iowa Code sections.