Fill Out Your For Life Insurance Trust Form

Creating a life insurance trust is a crucial step for individuals looking to secure their family's financial future. The For Life Insurance Trust form facilitates this by detailing the relationship between the policy owner, known as the Trustor, and the Trustee who will manage the trust. This legal document outlines specific terms, such as the policy number, the face amount of the insurance, and the beneficiaries who will receive support from the trust funds. Responsibilities are clearly defined; the Trustor is tasked with paying premiums while retaining significant rights unless otherwise specified. Notably, the Trustee’s duties involve claiming the policy proceeds after the insured's passing and managing the funds until the beneficiaries reach adulthood. The document emphasizes the need for responsible fund management, ensuring that the beneficiaries' education and support are prioritized. Furthermore, it allows the Trustor to amend the terms if necessary and provides a mechanism for changing trustees under specified conditions to maintain stability and oversee the trust's integrity. The form highlights the importance of protecting the insurance proceeds and outlines the legal safeguards in place, making it an essential tool for effective estate planning.

For Life Insurance Trust Example

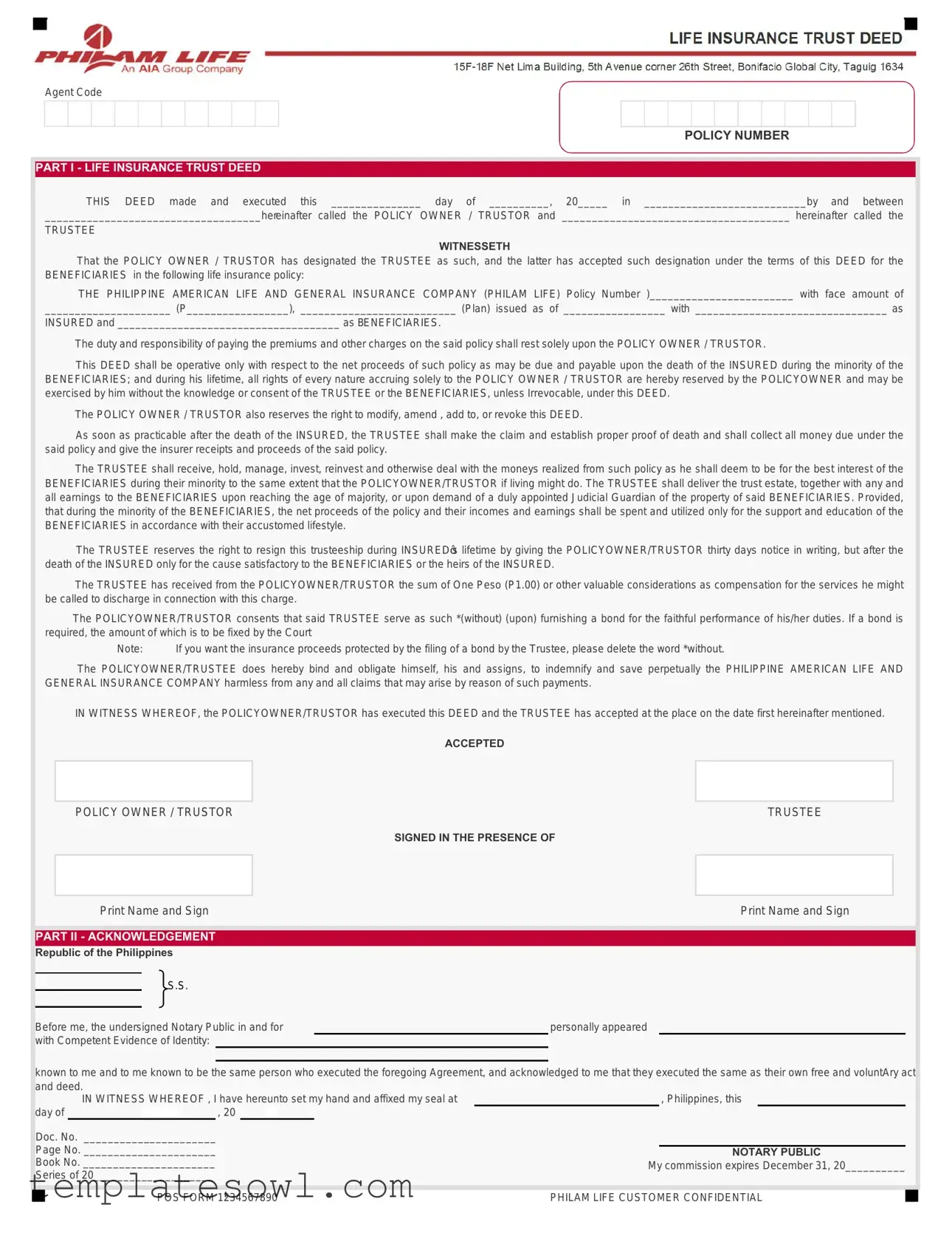

LIFE INSURANCE TRUST DEED

Agent Code

POLICY NUMBER

PART I - LIFE INSURANCE TRUST DEED

THIS DEED made and executed this _______________ day of __________, 20_____ in ___________________________by and between

____________________________________hereinafter called the POLICY OWNER / TRUSTOR and ______________________________________ hereinafter called the

TRUSTEE

WITNESSETH

That the POLICY OWNER / TRUSTOR has designated the TRUSTEE as such, and the latter has accepted such designation under the terms of this DEED for the BENEFICIARIES in the following life insurance policy:

THE PHILIPPINE AMERICAN LIFE AND GENERAL INSURANCE COMPANY (PHILAM LIFE) Policy Number )________________________ with face amount of

_____________________ (P_________________), __________________________ (Plan) issued as of _________________ with ________________________________ as

INSURED and _____________________________________ as BENEFICIARIES.

The duty and responsibility of paying the premiums and other charges on the said policy shall rest solely upon the POLICY OWNER / TRUSTOR.

This DEED shall be operative only with respect to the net proceeds of such policy as may be due and payable upon the death of the INSURED during the minority of the BENEFICIARIES; and during his lifetime, all rights of every nature accruing solely to the POLICY OWNER / TRUSTOR are hereby reserved by the POLICYOWNER and may be exercised by him without the knowledge or consent of the TRUSTEE or the BENEFICIARIES, unless Irrevocable, under this DEED.

The POLICY OWNER / TRUSTOR also reserves the right to modify, amend , add to, or revoke this DEED.

As soon as practicable after the death of the INSURED, the TRUSTEE shall make the claim and establish proper proof of death and shall collect all money due under the said policy and give the insurer receipts and proceeds of the said policy.

The TRUSTEE shall receive, hold, manage, invest, reinvest and otherwise deal with the moneys realized from such policy as he shall deem to be for the best interest of the BENEFICIARIES during their minority to the same extent that the POLICYOWNER/TRUSTOR if living might do. The TRUSTEE shall deliver the trust estate, together with any and all earnings to the BENEFICIARIES upon reaching the age of majority, or upon demand of a duly appointed Judicial Guardian of the property of said BENEFICIARIES. Provided, that during the minority of the BENEFICIARIES, the net proceeds of the policy and their incomes and earnings shall be spent and utilized only for the support and education of the BENEFICIARIES in accordance with their accustomed lifestyle.

The TRUSTEE reserves the right to resign this trusteeship during INSURED’s lifetime by giving the POLICYOWNER/TRUSTOR thirty days notice in writing, but after the death of the INSURED only for the cause satisfactory to the BENEFICIARIES or the heirs of the INSURED.

The TRUSTEE has received from the POLICYOWNER/TRUSTOR the sum of One Peso (P1.00) or other valuable considerations as compensation for the services he might be called to discharge in connection with this charge.

The POLICYOWNER/TRUSTOR consents that said TRUSTEE serve as such *(without) (upon) furnishing a bond for the faithful performance of his/her duties. If a bond is required, the amount of which is to be fixed by the Court

Note: |

If you want the insurance proceeds protected by the filing of a bond by the Trustee, please delete the word *without. |

The POLICYOWNER/TRUSTEE does hereby bind and obligate himself, his and assigns, to indemnify and save perpetually the PHILIPPINE AMERICAN LIFE AND GENERAL INSURANCE COMPANY harmless from any and all claims that may arise by reason of such payments.

IN WITNESS WHEREOF, the POLICYOWNER/TRUSTOR has executed this DEED and the TRUSTEE has accepted at the place on the date first hereinafter mentioned.

|

|

|

|

|

|

ACCEPTED |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

POLICY OWNER / TRUSTOR |

|

|

|

TRUSTEE |

|

|||||

|

|

|

|

|

|

SIGNED IN THE PRESENCE OF |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Print Name and Sign |

|

|

|

Print Name and Sign |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PART II - ACKNOWLEDGEMENT |

|

|

|

|

|

|

|

||||

|

Republic of the Philippines |

|

|

|

|

|

|

|

||||

|

|

|

S.S. |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

||||

|

Before me, the undersigned Notary Public in and for |

|

personally appeared |

|

||||||||

|

with Competent Evidence of Identity: |

|

|

|

|

|

|

|

|

|||

known to me and to me known to be the same person who executed the foregoing Agreement, and acknowledged to me that they executed the same as their own free and voluntAry act

|

and deed. |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

IN WITNESS WHEREOF , I have hereunto set my hand and affixed my seal at |

|

|

, Philippines, this |

|

||||||||||

|

day of |

|

|

|

, 20 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Doc. No. ______________________ |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Page No. ______________________ |

|

|

|

|

|

|

|

NOTARY PUBLIC |

|

|

|

|||||

|

Book No. ______________________ |

|

|

|

|

|

My commission expires December 31, 20__________ |

|

|||||||||

|

Series of 20____________________ |

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

POS FORM 1234567890 |

PHILAM LIFE CUSTOMER CONFIDENTIAL |

|

|

||||||||||

|

|

|

|

|

|

||||||||||||

Form Characteristics

| Fact Title | Details |

|---|---|

| Purpose of the Trust | This trust is designed to manage life insurance policy proceeds for the benefit of minor beneficiaries until they reach the age of majority. |

| Revocation Rights | The policy owner or trustor retains the right to modify, amend, or revoke the trust deed at any time prior to the death of the insured. |

| Trustee's Responsibilities | Upon the death of the insured, the trustee must collect the policy proceeds and manage the funds for the beneficiaries' support and education. |

| Governing Laws | Governed under the laws applicable in the Philippines, particularly focusing on trusts and estates within that jurisdiction. |

| Trustee's Bond Requirement | The trustee may need to provide a bond for the performance of duties if the policy owner does not choose to waive this requirement. |

Guidelines on Utilizing For Life Insurance Trust

Filling out the For Life Insurance Trust form involves providing detailed information about the life insurance policy, the policy owner, trustee, and beneficiaries. This is an essential step in establishing a trust that designates how the policy proceeds will be managed and distributed.

- Begin by writing the date at the top of the form in the format _______________ day of __________, 20_____.

- In the first blank line, enter the place where the deed is executed, e.g., city or state.

- Fill in the name of the POLICY OWNER / TRUSTOR in the appropriate space.

- Enter the name of the TRUSTEE where indicated.

- Provide the policy number of the life insurance policy in the designated space.

- Record the face amount of the life insurance policy (both in words and numbers) next to "face amount of".

- Specify the plan issued under the life insurance policy next to "(Plan) issued as of".

- In the next blank, enter the name of the INSURED under the policy.

- List the names of the BENEFICIARIES in the designated area.

- In the last section of Part I, both the POLICY OWNER / TRUSTOR and the TRUSTEE should sign and print their names in the respective areas provided at the bottom of the deed.

- Complete Part II by including the date, location, and notarization details. The notary public will complete this section, so leave it blank for them.

What You Should Know About This Form

What is a Life Insurance Trust and why would I need one?

A Life Insurance Trust is a legal arrangement that holds the proceeds of a life insurance policy for the benefit of designated beneficiaries. By establishing this trust, you can ensure that the insurance payout is managed according to your wishes, especially for minors or individuals who may not be financially savvy. This trust can help avoid probate, reduce estate taxes, and allow the trustee to manage funds until the beneficiaries are ready to receive the money. Having this structure can provide peace of mind, knowing that your loved ones will be taken care of financially if something happens to you.

Who can serve as a trustee for the Life Insurance Trust?

The trustee is typically a trusted individual, such as a family member or close friend, or a professional entity like a bank or trust company. The trustee's role is to manage the life insurance proceeds according to the terms set in the trust deed. It's essential to choose someone who is responsible and capable of handling financial matters. The selected trustee has the authority to make decisions regarding the funds until the beneficiaries reach adulthood or meet certain conditions for receiving their inheritance.

Can I change the terms of my Life Insurance Trust once it has been established?

Yes, as the policy owner or trustor, you retain the right to modify, amend, or revoke the trust at any time while you are alive, provided these changes are documented appropriately. This flexibility allows you to adapt the trust to changing circumstances, ensuring that it continues to meet your family's needs and your intentions. Always consult with a legal professional when making alterations to ensure compliance with local laws and to maintain the intended benefits of the trust.

What happens to the insurance proceeds if the insured person passes away?

Upon the death of the insured, the trustee is responsible for filing a claim with the insurance company to collect the policy's proceeds. The trustee will ensure that the funds are managed responsibly and spent for the support and education of the beneficiaries until they reach the age of majority. Once beneficiaries reach adulthood, the trustee will transfer the remaining funds to them. This process is designed to protect the beneficiaries and ensure the funds are used in their best interest during their childhood.

Common mistakes

When filling out the For Life Insurance Trust form, individuals often encounter pitfalls that can derail the process. Here are six common mistakes to be aware of to help ensure that everything is filled out correctly and effectively.

One major mistake occurs with the policy number. People sometimes forget to enter the correct policy number or leave this field blank. This number is essential as it identifies your specific insurance policy. Without it, the trustee may find it challenging to claim the benefits intended for the beneficiaries. Always double-check that you have the right number from your insurance documents.

Another frequent error involves the beneficiaries’ information. Many individuals fail to list all beneficiaries accurately or omit their full names and details. Including incomplete or incorrect beneficiary information can lead to delays in fund distribution after the policyholder's passing. Ensure you take the time to gather complete names, relationships, and contact information for each beneficiary.

Some also overlook the section regarding the trustee’s responsibilities. It's critical to fully understand and specify the powers and duties of the trustee. If individuals either do not designate a trustee or choose someone who may be unsuitable, it can lead to conflicts and complications in managing the trust. Carefully select a trustworthy and competent person who will act in the beneficiaries’ best interests.

A common mistake also manifests in section titles, such as when people incorrectly use trustor and trustee interchangeably. Confusion arises because the trustor is the policy owner who creates the trust, while the trustee manages the trust. Understanding these roles distinctly is crucial for clarity and fulfilling the legal requirements laid out in the form.

Another issue is the lack of a witnessed signature. Sometimes, signers neglect to have their signatures witnessed by a third party. Notarization or witnessing is necessary to validate the document legally. This oversight can render the trust ineffective or could lead to challenges if the form is contested in the future.

Finally, failing to review legal terms and conditions can be detrimental. Some people hastily sign the form without fully understanding its implications. This can result in unintended consequences, such as waiving rights to certain benefits or misunderstanding the terms of the trust. It is always wise to take a moment to read through the document carefully and, if possible, seek advice from a qualified professional.

By being aware of these common mistakes and taking the necessary time to ensure accuracy, you can help safeguard your loved ones’ future and create a trust that works as intended. Simple diligence can make a significant difference in the effectiveness of a life insurance trust.

Documents used along the form

The For Life Insurance Trust form is an important document that establishes a life insurance trust. It designates a trustee to manage the proceeds of a life insurance policy for the benefit of specific beneficiaries. Along with this form, there are several other documents frequently used to support the trust and ensure its proper execution. Below are a few key documents that may be needed in conjunction with the For Life Insurance Trust form.

- Life Insurance Policy: This document outlines the details of the insurance coverage, including the policy number, terms, and conditions. It confirms the existence of the life insurance being placed in trust and specifies the insured individual.

- Trust Agreement: This document lays out the rules and guidelines for the operation of the trust. It includes details on how the trust will be managed and the responsibilities of the trustee and the beneficiaries.

- Beneficiary Designation Form: This form is often used to designate the beneficiaries who are entitled to receive the insurance proceeds. It ensures that the trustee will disburse funds to the correct individuals once conditions trigger the release of the proceeds.

- Certification of Trust: This document serves as a summary of the trust terms and can be presented to financial institutions or other entities without disclosing the full trust agreement. It helps in verifying the trust’s existence and the trustee's authority to act on its behalf.

Using the For Life Insurance Trust form alongside these documents helps ensure that all aspects of the trust are properly addressed. This combination provides clarity and security for both the trustee and the beneficiaries, safeguarding the interests of those involved.

Similar forms

- Last Will and Testament: Like the For Life Insurance Trust form, a Last Will and Testament outlines the disposition of assets upon death. Both documents allow for the designation of beneficiaries and provide instructions for managing the estate, ensuring that the wishes of the deceased are fulfilled.

- Living Trust: A Living Trust, similar to a For Life Insurance Trust, enables the trustor to transfer assets outside of probate. Both trust types protect assets for beneficiaries, provide for management during the trustor’s lifetime, and specify how and when the assets will be distributed after death.

- Powers of Attorney: While a For Life Insurance Trust designates a trustee to manage life insurance proceeds, a Power of Attorney allows an appointed individual to make financial decisions on behalf of someone else. Both documents establish authority and outline responsibilities, although Powers of Attorney focus on decision-making rather than asset distribution.

- Health Care Proxy: Similar to the mechanisms of a For Life Insurance Trust, a Health Care Proxy designates an individual to make medical decisions if one becomes incapacitated. Both documents empower a trusted individual to act on behalf of the original party concerning their well-being and finances.

- Beneficiary Designation Forms: These forms specify who receives proceeds from financial accounts or life insurance policies. Like the For Life Insurance Trust, they aim to ensure that assets go directly to named beneficiaries, thereby avoiding probate and ensuring quicker access to funds for loved ones.

Dos and Don'ts

Filling out the For Life Insurance Trust form requires careful attention to detail. Here are five essential guidelines to follow, along with practices to avoid:

- Do read the form thoroughly before starting to fill it out. Understanding the requirements is vital.

- Do provide accurate information for all parties involved, including the policy owner, trustee, and beneficiaries.

- Do ensure all signatures are obtained, including that of the trustee and policy owner, to avoid complications later.

- Do review the completed form for any errors or omissions before submission. Double-check names, dates, and policy numbers.

- Do consider having a legal professional review the document to ensure it meets your intentions.

- Don't rush to complete the form. Take your time to ensure accuracy and comprehensiveness.

- Don't leave any sections blank unless specifically instructed. Every part of the form is important.

- Don't withhold information or be misleading in the details provided. Transparency is crucial for the trust's integrity.

- Don't forget to specify any preferences regarding the trustee's responsibilities, especially concerning financial matters.

- Don't neglect to retain a copy of the completed form for your records and future reference.

Misconceptions

Here are eight common misconceptions about the For Life Insurance Trust form:

- Misconception 1: The policy owner loses all control over the life insurance policy once it's placed in a trust.

- Misconception 2: The trust automatically pays out to the beneficiaries upon the policy owner's death.

- Misconception 3: Once a trustee is named, it cannot be changed.

- Misconception 4: Life insurance proceeds are subject to probate.

- Misconception 5: The trustee must immediately distribute funds to beneficiaries upon the insured’s death.

- Misconception 6: A bond is always required for the trustee.

- Misconception 7: The beneficiaries can access trust funds at any time.

- Misconception 8: All life insurance policies must be placed in a trust.

This is incorrect. The policy owner retains the right to manage and amend the trust during their lifetime, provided that rights are not irrevocably transferred.

This is not true. The trustee must first make a claim and establish proof of death before funds are distributed.

This is a misunderstanding. The policy owner can modify or revoke the trust, including changing the trustee, as long as their rights are not irrevocable.

This is false. Life insurance trust proceeds typically avoid probate, which can help expedite distribution to beneficiaries.

This is misleading. The trustee holds funds until beneficiaries reach the age of majority or until instructed by a guardian.

This statement is not accurate. The policy owner can choose whether a bond is needed, depending on their preferences.

This is not permitted. Access to funds is restricted to education and support during the beneficiaries' minority or upon reaching the age of majority.

This is incorrect. Placing insurance policies in trust is optional and depends on individual financial goals and estate planning needs.

Key takeaways

Creating a Life Insurance Trust is a structured process that involves specific steps. Here are some key takeaways from the Life Insurance Trust form:

- The form must be completed and dated properly to ensure validity.

- Identify the Policy Owner or Trustor. This person has the responsibility for the life insurance policy.

- The chosen Trustee accepts the role and is responsible for managing the trust provisions.

- Provide details of the life insurance policy, including the policy number and the face amount.

- The Trustor retains all rights related to the policy until the insured's death, unless otherwise specified.

- The Trustee is liable for managing the policy proceeds in the best interest of the beneficiaries during their minority.

- Upon the death of the insured, the Trustee must file a claim to access the policy proceeds.

- The policy proceeds can be used solely for the support and education of the beneficiaries while they are minors.

- The Trustee can resign with appropriate notice during the insured’s lifetime, but may only resign after the insured's death under specific circumstances.

- There is an option to require a bond for the Trustee’s duties, which can provide additional protection for the trust's assets.

Browse Other Templates

Time Limit to Challenge Relinquishment Deed - Obtaining a copy of the notarized form can assist in tracking the transaction status.

Entry Form Template - Every participant makes the game even more exciting!