Fill Out Your Gp5479Us Form

If you're navigating the landscape of retirement savings and considering a cash distribution from your eligible plan, understanding the Gp5479Us form is essential. This form serves as a key document when making critical decisions about your retirement funds at John Hancock, particularly if you're transitioning to a different job or retiring altogether. You'll have various options to manage your funds, including keeping your money in the current plan, rolling it over to an IRA, or cashing out. Each choice comes with its own potential tax implications, so it’s wise to be informed. The withdrawal process is straightforward; you can fill out the attached form, which guides you through essential sections covering your information and your withdrawal preferences. Moreover, John Hancock's Rollover Specialists are available to assist you in making an informed decision, ensuring that you understand all possible avenues and potential consequences. Always remember—each choice carries specific implications based on your unique circumstances. Thus, consulting with independent advisors for personalized advice is encouraged to help you navigate your options with confidence.

Gp5479Us Example

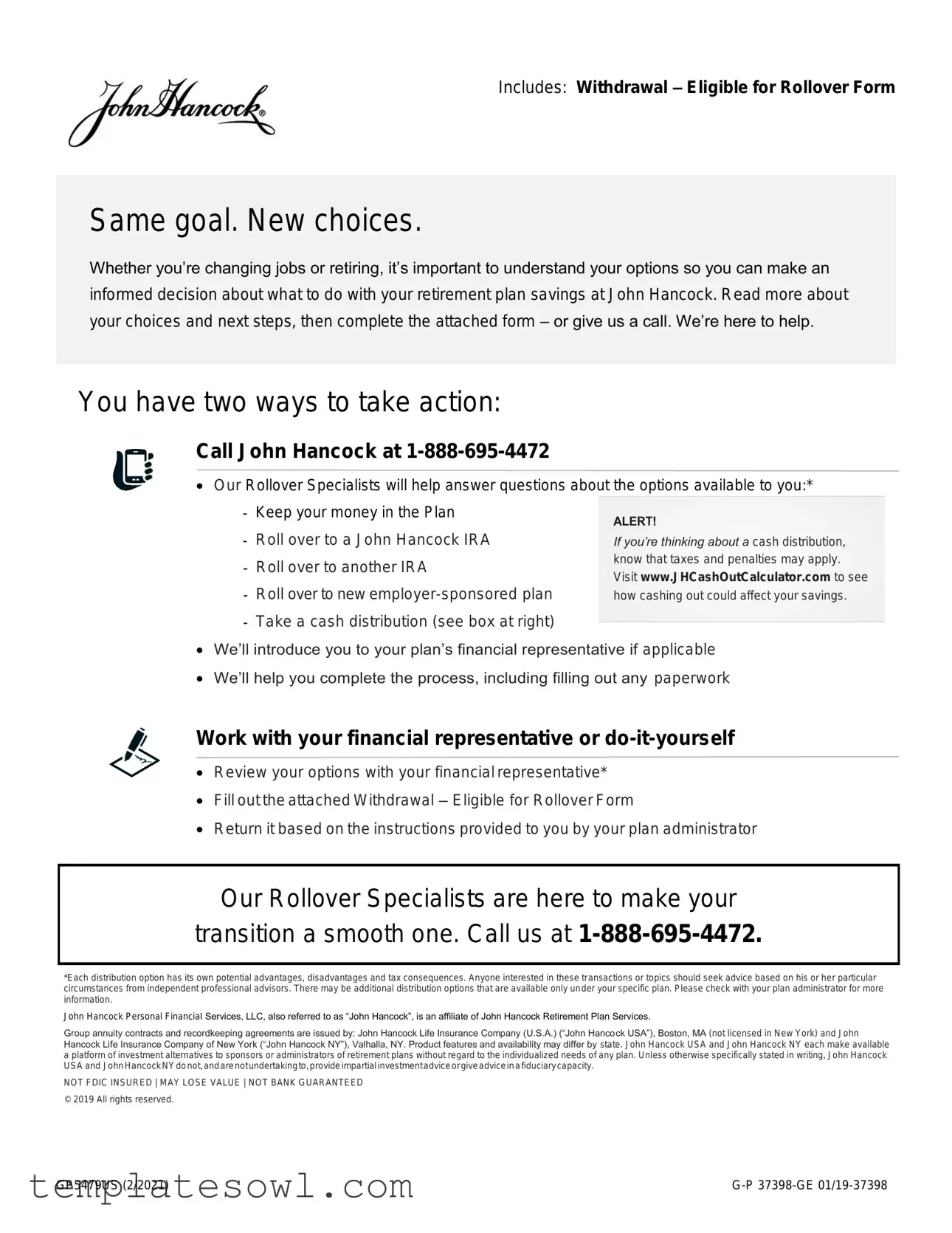

Includes: Withdrawal – Eligible for Rollover Form

Same goal. New choices.

Whether you’re changing jobs or retiring, it’s important to understand your options so you can make an informed decision about what to do with your retirement plan savings at John Hancock. Read more about your choices and next steps, then complete the attached form – or give us a call. We’re here to help.

You have two ways to take action:

Call John Hancock at

Our Rollover Specialists will help answer questions about the options available to you:*

-Keep your money in the Plan

- Roll over to a John Hancock IRA - Roll over to another IRA

- Roll over to new

-Take a cash distribution (see box at right)

We’ll introduce you to your plan’s financial representative if applicable

We’ll help you complete the process, including filling out any paperwork

Work with your financial representative or

Review your options with your financial representative*

Fill out the attached Withdrawal – Eligible for Rollover Form

Return it based on the instructions provided to you by your plan administrator

Our Rollover Specialists are here to make your

transition a smooth one. Call us at

*Each distribution option has its own potential advantages, disadvantages and tax consequences. Anyone interested in these transactions or topics should seek advice based on his or her particular circumstances from independent professional advisors. There may be additional distribution options that are available only under your specific plan. Please check with your plan administrator for more information.

John Hancock Personal Financial Services, LLC, also referred to as “John Hancock”, is an affiliate of John Hancock Retirement Plan Services.

Group annuity contracts and recordkeeping agreements are issued by: John Hancock Life Insurance Company (U.S.A.) (“John Hancock USA”), Boston, MA (not licensed in New York) and John Hancock Life Insurance Company of New York (“John Hancock NY”), Valhalla, NY. Product features and availability may differ by state. John Hancock USA and John Hancock NY each make available a platform of investment alternatives to sponsors or administrators of retirement plans without regard to the individualized needs of any plan. Unless otherwise specifically stated in writing, John Hancock USA and John Hancock NY do not, and are not undertaking to, provide impartial investment advice or give advice in a fiduciary capacity.

NOT FDIC INSURED | MAY LOSE VALUE | NOT BANK GUARANTEED

© 2019 All rights reserved.

GP5479US (2/2021) |

Reset Form

Withdrawal - Eligible for Rollover

Important Information about this Form

Your plan may require you to provide supporting documents or additional information before your request can be processed.

As the participant, you complete Sections 1 - 7 of this form and return it to your Plan Representative.

As the Plan Representative, you review Sections 1 - 7, and complete Sections 8 - 10 of this form.

If the participant address provided below is new or different than what is currently on record with John Hancock Retirement Plan Services, we will update our records accordingly. Ensure your next census submission includes revised employee information to avoid your file superseding the information supplied on this form.

A 1099R form will be issued for each distribution and loan default (if applicable) by January 31 of the following year.

This request is subject to the processing and procedure guidelines contained in John Hancock’s Administrative Guidelines for Financial Transactions (“AGFT”). The latest AGFT is available on the John Hancock plan sponsor website or you may contact your John Hancock representative for a copy.

All changes must be initialed in pen (including numbers crossed out or changed using correction fluid).

1. General Information

The Trustee of |

{Contractholder_name} |

Plan (“the Plan”) |

{ContractNum2} |

|||

Contractholder Name |

|

|

|

|

|

Contract Number |

{Participant_name} |

|

|

|

{SSN} |

|

|

Participant Name as displayed on your Social Security Card (Last Name, First Name, Initial) |

|

|

Participant Social Security Number (Full SSN Required) |

|||

|

|

|

|

Date |

|

|

{ppt_address} |

|

|

|

of Birth {DCCIASec3EffectiveDate} |

||

Participant Address – Street Address |

|

|

|

|

|

|

|

|

Participant |

{PhoneNumber} |

|

||

{ppt_cszip} |

|

Phone No. |

|

|||

City, State, Zip Code, Country

2. What is the reason for your withdrawal? – Select ONE option only

It is the responsibility of the Plan Administrator, and not of John Hancock Retirement Plan Services, to ensure that the participant is permitted under the terms of the Plan to receive the distribution selected below.

TE – |

Termination date |

RE – |

Retirement date |

IR – |

Employee Money Transferred into Plan |

DI – |

Disability |

|

(Must complete Section 3B) |

|

|

VC – |

Employee Voluntary Money |

PD – |

|

|

(Must complete Section 3B) |

|

(If permitted by the Plan) |

Information about Deferred Distributions

Section 1102 of the Pension Protection Act of 2006 requires plans to notify participants that they have the right to defer distributions as well as the consequences of making that choice. The investment options available under your group annuity contract as well as the fees related to the investment options are part of this consideration.

For a description of the investment options available under your group annuity contract, including fees:

Log onto www.johnhancock.com/myplan.

Select: Your contract reports - Investments - Contract investment options and view Selected investment options only. Alternatively, participants may obtain this information by calling our toll free service line at

You should also review your plan's Summary Plan Description (SPD) which may contain special provisions that may materially affect your decision to defer a distribution. For a copy of the SPD, please contact your Plan Administrator.

GP5479US (2/2021) |

Page 1 of 9 |

Group annuity contracts and recordkeeping agreements are issued by: John Hancock Life Insurance Company (U.S.A.) (“John Hancock USA”), Boston, MA (not licensed in New York) and John Hancock Life Insurance Company of New York (“John Hancock NY”), Valhalla, NY. Product features and availability may differ by state. John Hancock USA and John Hancock NY each make available a platform of investment alternatives to sponsors or administrators of retirement plans without regard to the individualized needs of any plan. Unless otherwise specifically stated in writing, John Hancock USA and John Hancock NY do not, and are not undertaking to, provide impartial investment advice or give advice in a fiduciary capacity.

3. How much do you want to withdraw? Select ONE option only

If no option is selected a TOTAL withdrawal will be processed.

The amount or percentage below will be withdrawn as a gross withdrawal before income tax withholding.

A - Withdraw 100% of my vested account value

OR

B - Withdraw only a portion of the funds in my plan as follows - Tell us how much to withdraw from each eligible money type (Amount or Percentage). Completing the Investment Fund Code is not mandatory. If the Investment Fund Code is left blank, John Hancock Retirement Plan Services’ standard withdrawal order will be used.

Money Type |

Investment Fund |

Amount |

|

Percentage |

|

(Mandatory) |

Code (Optional) |

|

|||

|

|

|

|||

{PortionType1} |

{PortionFund1} |

${PortionAmt1} |

OR |

{PortionPct1}% |

|

{PortionType2} |

{PortionFund2} |

${PortionAmt2} |

{PortionPct2}% |

||

|

|||||

{PortionType3} |

{PortionFund3} |

${PortionAmt3} |

|

{PortionPct3}% |

4. What do you want to do with your money?

Complete Section A if you wish to make your distribution payable to only a single destination. For multiple destinations, complete Section B.

A - Send my payment to ONE destination only - Select ONE option only.

Direct Rollover to an IRA or Roth IRA - Complete Section 5A or 5B

Direct Rollover to Employer Sponsored Qualified Plan - Complete Section 5C Payment Directly to Me - Complete Section 5D

Pay to the Plan Trustee for Deposit into the Plan’s Trust Account - A check will be mailed to the Trustee address on record with John Hancock Retirement Plan Services unless EFT instructions are provided in Section 5C. Taxes will not be withheld and a 1099R Form will not be issued. The Plan Trustee will be responsible for implementing the participant's direction and performing the applicable withholding and reporting obligations. Continue to Section 6.

Leave my money in the Plan. You may defer your distribution to a later date. Consult your Plan Administrator. Continue to Section 6.

OR

B - Send my payments to MULTIPLE destinations - If applicable, you may provide separate instructions for the taxable and non taxable money that make up your requested withdrawal.

•IRC § 402(c)(2) will apply to any request withdrawing only a portion of the funds in your plan (Section 3B).

•Payments directly to you will be deemed to come first from

•Payments directly to you will be processed first. Any remaining funds will be directly rolled over to the appropriate rollover vehicle indicated below.

•Your withdrawal will be processed in accordance with the time frame described in our Administrative Guidelines.

GP5479US (2/2021) |

Page 2 of 9 |

Group annuity contracts and recordkeeping agreements are issued by: John Hancock Life Insurance Company (U.S.A.) (“John Hancock USA”), Boston, MA (not licensed in New York) and John Hancock Life Insurance Company of New York (“John Hancock NY”), Valhalla, NY. Product features and availability may differ by state. John Hancock USA and John Hancock NY each make available a platform of investment alternatives to sponsors or administrators of retirement plans without regard to the individualized needs of any plan. Unless otherwise specifically stated in writing, John Hancock USA and John Hancock NY do not, and are not undertaking to, provide impartial investment advice or give advice in a fiduciary capacity.

•Split my payment - Select all the applicable options below and then complete the next Section.

{F34}

{F36}

{F45}

Pay directly to me $ {TaxDollar}

(Section 5D)

|

|

|||||

{F37} |

Non Taxable balance directly rolled over to: |

|

||||

|

{F38} |

Traditional IRA |

{F39} |

Roth IRA |

{F40} |

Employer Sponsored Qualified Plan |

|

|

(Section 5A) |

|

(Section 5B) |

|

(Section 5C) |

{F41} |

Taxable balance directly rolled over to: |

|

|

|||

|

{F42} |

Traditional IRA |

{F43} |

Roth IRA |

{F44} |

Employer Sponsored Qualified Plan |

|

|

(Section 5A) |

|

(Section 5B) |

|

(Section 5C) |

Roth: |

|

|

|

|

|

|

Directly rolled over to: |

|

|

|

|

||

|

{F46} |

Roth IRA |

{F47} |

A Designated Roth Account |

||

|

|

(Section 5B) |

|

in an |

||

(Section 5C)

5. Where do you want your money sent?

Select and complete option(s) A, B, C, and/or D (as applicable)

Federal law requires that 20% of the taxable amount of an eligible rollover distribution be withheld, unless payment is directly rolled over to an eligible retirement plan. The amount withheld may not represent your entire tax bill. The rollover will be reported to the IRS and you are responsible for the payment of the income tax(es) that apply in connection with the rollover. Please refer to the Special Tax Notice provided by your Plan Administrator regarding these tax rules. Contact your tax advisor or Plan Administrator if you have any questions.

A - Traditional IRA

{F51} Direct Rollover to the following John Hancock product. Your funds will be transferred automatically by wire. You must provide the account number. For more information contact John Hancock at

Elect one:

{F49}

{F53}

{F52}

John Hancock Investments Rollover IRA |

Account Number: {AccNum1} |

|

|

|

|

John Hancock Managed IRA |

Account Number: {AccNum2} |

|

|

|

|

John Hancock GIFL Rollover Variable Annuity IRA |

Account Number: {AccNumG1} |

|

|

|

|

OR |

|

|

|

|

{F55} Direct Rollover to another Financial Institution |

Account Number: {AccNum3} |

|

||

|

{RO_ Inst_Name} |

|

|

|

|

Financial Institution Name |

|

|

|

|

{RO_ Inst_Addr} |

|

|

|

|

Financial Institution Address – Street, City, State, Zip Code, Country |

|

|

|

Electronic Fund Transfer Information (REQUIRED)

You must provide electronic fund transfer information below, unless the financial institution requires a check be issued. Where a check is issued it will be mailed according to the standard mailing instructions on file with John Hancock Retirement Plan Services, as established by the Plan Trustee.

|

Expected Delivery: • |

Checks: |

||||

|

Electronic Fund Transfer Details |

|

|

|||

|

|

Direct Deposit |

OR |

Wire – Verify with receiving bank if they accept wires and/or charge a fee |

||

|

Provide Domestic Bank details: |

|

|

|||

|

{BankName} |

|

|

|

|

|

|

Bank Name |

|

|

|

|

|

|

{BankABA} |

|

|

{BankAcctNo} |

|

|

|

Bank ABA/Routing (9 digits) |

|

|

Bank Account No. |

||

|

{F64} |

For international banks, complete and attach the International Banking Instructions form. |

||||

GP5479US (2/2021) |

|

|

|

Page 3 of 9 |

||

Group annuity contracts and recordkeeping agreements are issued by: John Hancock Life Insurance Company (U.S.A.) (“John Hancock USA”), Boston, MA (not licensed in New York) and John Hancock Life Insurance Company of New York (“John Hancock NY”), Valhalla, NY. Product features and availability may differ by state. John Hancock USA and John Hancock NY each make available a platform of investment alternatives to sponsors or administrators of retirement plans without regard to the individualized needs of any plan. Unless otherwise specifically stated in writing, John Hancock USA and John Hancock NY do not, and are not undertaking to, provide impartial investment advice or give advice in a fiduciary capacity.

B - Roth IRA

{F62} Direct Rollover to the following John Hancock product. Your funds will be transferred automatically by wire. You must provide the account number. For more information contact John Hancock at

Elect one:

{F66}

{F68}

{F69}

John Hancock Investments Rollover IRA |

Account Number: {AccNumR1} |

|

|

|

|

John Hancock Managed IRA |

Account Number: {AccNumR2} |

|

|

|

|

John Hancock GIFL Rollover Variable Annuity IRA |

Account Number: {AccNumRG1} |

|

|

|

|

OR |

|

|

|

|

{F72} Direct Rollover to another Financial Institution |

Account Number: {AccNumR3} |

|

||

|

{RO_ Inst_NameR} |

|

|

|

|

Financial Institution Name |

|

|

|

|

{RO_ Inst_AddrR} |

|

|

|

|

Financial Institution Address – Street, City, State, Zip Code, Country |

|

|

|

Electronic Fund Transfer Information (REQUIRED)

You must provide electronic fund transfer information below, unless the financial institution requires a check be issued. Where a check is issued it will be mailed according to the standard mailing instructions on file with John Hancock Retirement Plan Services, as established by the Plan Trustee.

Expected Delivery: • |

Checks: |

||||

Electronic Fund Transfer Details |

|

|

|||

|

Direct Deposit |

OR |

Wire – Verify with receiving bank if they accept wires and/or charge a fee |

||

Provide Domestic Bank details: |

|

|

|||

{BankNameR} |

|

|

|

|

|

Bank Name |

|

|

|

|

|

{BankABAR} |

|

|

{BankAcctNoR} |

|

|

Bank ABA/Routing (9 digits) |

|

|

Bank Account No. |

||

{F82} |

For international banks, complete and attach the International Banking Instructions form. |

||||

C - Employer Sponsored Qualified Plan

The Trustee of {Trustee_Name} |

|

{PContractNum} |

|

|

Plan Name |

|

Plan Account Number |

{RO_ Inst_NameEP} |

|

|

|

Financial Institution Name |

|

|

|

{RO_ Inst_AddrEP} |

|

|

|

Financial Institution Address – Street, City, State, Zip Code, Country |

|

|

|

GP5479US (2/2021) |

Page 4 of 9 |

Group annuity contracts and recordkeeping agreements are issued by: John Hancock Life Insurance Company (U.S.A.) (“John Hancock USA”), Boston, MA (not licensed in New York) and John Hancock Life Insurance Company of New York (“John Hancock NY”), Valhalla, NY. Product features and availability may differ by state. John Hancock USA and John Hancock NY each make available a platform of investment alternatives to sponsors or administrators of retirement plans without regard to the individualized needs of any plan. Unless otherwise specifically stated in writing, John Hancock USA and John Hancock NY do not, and are not undertaking to, provide impartial investment advice or give advice in a fiduciary capacity.

Electronic Fund Transfer Information (REQUIRED)

You must provide electronic fund transfer information below, unless the financial institution requires a check be issued. Where a check is issued it will be mailed according to the standard mailing instructions on file with John Hancock Retirement Plan Services, as established by the Plan Trustee.

Expected Delivery: • |

Checks: |

||||

Electronic Fund Transfer Details |

|

|

|||

|

Direct Deposit |

OR |

Wire – Verify with receiving bank if they accept wires and/or charge a fee |

||

Provide Domestic Bank details: |

|

|

|||

{BankNameEP} |

|

|

|

|

|

Bank Name |

|

|

|

|

|

{BankABAEP} |

|

|

{BankAcctNoEP} |

|

|

Bank ABA/Routing (9 digits) |

|

|

Bank Account No. |

||

{F93} |

For international banks, complete and attach the International Banking Instructions form. |

||||

D - Payment Directly to Me – All applicable taxes will be withheld

Federal Tax

A taxable distribution (and, if applicable, each outstanding loan balance) is subject to 20% mandatory minimum federal tax withholding for a U.S. person (including a U.S. resident alien).

To request a higher tax rate, specify a whole number above 20%: {TaxPercent} % (refer to DOL Field Assistance Bulletin

OR {F96} I am neither a U.S. person nor a U.S. resident alien. Country of residence: {CountryRes}

Unless I have attached a completed IRS Form

GP5479US (2/2021) |

Page 5 of 9 |

Group annuity contracts and recordkeeping agreements are issued by: John Hancock Life Insurance Company (U.S.A.) (“John Hancock USA”), Boston, MA (not licensed in New York) and John Hancock Life Insurance Company of New York (“John Hancock NY”), Valhalla, NY. Product features and availability may differ by state. John Hancock USA and John Hancock NY each make available a platform of investment alternatives to sponsors or administrators of retirement plans without regard to the individualized needs of any plan. Unless otherwise specifically stated in writing, John Hancock USA and John Hancock NY do not, and are not undertaking to, provide impartial investment advice or give advice in a fiduciary capacity.

State Tax Withholding Instructions

State of |

Enter state of residence at time of withdrawal if state tax withholding should be taken for a state |

||||||||||

Residence |

other than the state provided to us. |

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

State of Residence |

|

Options for State Tax Withholding |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|||

AR, DC, KS, MA, MD, ME, NC, NE, |

You may not opt out. Since your distribution was subject to federal income tax, these states |

||||||||||

OK, VA, VT |

|

require mandatory state withholding based on the states’ applicable minimum requirements. |

|||||||||

|

|

|

|

|

|

|

|

|

|

||

|

|

Generally, state tax withholding will be applied to your taxable distribution at the rate of |

|||||||||

|

|

6.99%. However, if you elected a partial withdrawal, a flat dollar amount may be withheld |

|||||||||

|

|

instead, but the amount must be calculated based on a completed |

|||||||||

CT |

|

the Plan Administrator. If no amount is indicated, 6.99% will be withheld. |

|||||||||

|

|

{F100} |

I elected a partial distribution on this form and provided a completed |

||||||||

|

|

|

Plan Administrator. The calculated amount to be withheld is: ${TaxDollar6} |

||||||||

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

||||

|

|

State tax withholding will be applied to your taxable distribution unless one of the following |

|||||||||

|

|

boxes is checked below: |

|

|

|

||||||

|

|

{F98} |

I elect to opt out of withholding. (This option is only available for residents of Michigan.) |

||||||||

MI, IA |

|

{F99} |

I am eligible to claim exemption of $ {TaxDollar2} |

; withhold tax only on the |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

taxable, distributed amount that is in excess of the exempt amount. |

|||||||||

|

|

If you check one of the boxes above, you are required to return a completed Form |

|||||||||

|

|

your Plan Administrator. Ensure that the election made above is consistent with the election |

|||||||||

|

|

made on your completed Form |

|

|

|

||||||

|

|

|

|

|

|

|

|||||

CA, OR |

|

You may opt out of the mandatory state withholding by checking here. {F101} |

|||||||||

|

|

|

|

|

|

|

|||||

AL, CO, DE, GA, ID, IL, IN, KY, LA, |

You may elect voluntary state income tax withholding by providing a percentage or whole |

||||||||||

dollar amount to be applied for state tax withholding here. Some states mandate a minimum |

|||||||||||

MN, MO, MT, ND, NJ, NM, OH, |

and/or maximum percentage. |

|

|

|

|||||||

SC, UT, WV, WI |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

{TaxPercent2} % or $ {TaxDollar3} |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Electronic Fund Transfer Information (REQUIRED)

You must provide electronic fund transfer information below, unless the financial institution requires a check be issued. Where a check is issued it will be mailed according to the standard mailing instructions on file with John Hancock Retirement Plan Services, as established by the Plan Trustee.

Expected Delivery: • Checks:

Electronic Fund Transfer Details |

|

|

|

Direct Deposit – My personal bank account is |

Checking |

OR |

Savings |

OR |

|

|

|

Wire – Verify with receiving bank if they accept wires and/or charge a fee

Provide domestic bank details:

{BankName4}

Bank Name

{BankABA4} |

|

{BankAcctNo4} |

|

|

|

Bank ABA/Routing (9 digits) |

|

Bank Account No. |

{F111}For international banks, complete and attach the International Banking Instructions form.

6. Waiver of Waiting Period

In general, you have a right to a period of at least 30 days to consider the decision of whether to elect a withdrawal from the day that you receive the Special Tax Notice from your Plan Administrator. However, if your plan permits, you may elect to waive this

I wish to waive the

The information provided in this section shall not be maintained or acted upon by John Hancock Retirement Plan Services.

GP5479US (2/2021) |

Page 6 of 9 |

Group annuity contracts and recordkeeping agreements are issued by: John Hancock Life Insurance Company (U.S.A.) (“John Hancock USA”), Boston, MA (not licensed in New York) and John Hancock Life Insurance Company of New York (“John Hancock NY”), Valhalla, NY. Product features and availability may differ by state. John Hancock USA and John Hancock NY each make available a platform of investment alternatives to sponsors or administrators of retirement plans without regard to the individualized needs of any plan. Unless otherwise specifically stated in writing, John Hancock USA and John Hancock NY do not, and are not undertaking to, provide impartial investment advice or give advice in a fiduciary capacity.

7. Participant Signature

If my withdrawal is made from Funds with the Guaranteed Income feature, I acknowledge that I have read and reviewed the Guaranteed Income feature brochure and fully understand the consequences and impact that my withdrawal will have on my Benefit Base and other benefits provided by this feature. I understand that a brief outline of the terms and conditions governing my withdrawal is also contained in the summary entitled “Important Information about the Guaranteed Income Feature” which can be found on the John Hancock Retirement Plan Services participant website or obtained from my Plan Administrator.

John Hancock Retirement Plan Services may charge a fee for this withdrawal request. Other charges or fees may also apply. Please refer to your plan’s

For participants under a contract issued by John Hancock Life Insurance Company of New York, any person who knowingly and with intent to defraud any insurance company or other person files an application for insurance or statement of claim containing any materially false information, or conceals for the purpose of misleading, information concerning any fact material thereto, commits a fraudulent insurance act, which is a crime, and shall also be subject to a civil penalty not to exceed five thousand dollars and the stated value of the claims for each such violation. For all other states, civil penalties may apply.

Certification required of U.S. persons only (including U.S. citizens or U.S. resident aliens).

Under penalties of perjury, I certify that:

1.The number shown in Section 1 of this form is my correct taxpayer identification number, and

2.I am not subject to backup withholding because: (a) I am exempt from backup withholding, or (b) I have not been notified by the Internal Revenue Service (IRS) that I am subject to backup withholding as a result of a failure to report all interest or dividends, or (c) the IRS has notified me that I am no longer subject to backup withholding, and

3.I am a U.S. citizen or other U.S. person, including a U.S. resident alien (as defined in the IRS Form

Certification Instructions

You must check the box below if you have been notified by the IRS that you are currently subject to backup withholding because you failed to report all interest and dividends on your tax return.

{FCB1} I am subject to backup withholding as a result of a failure to report all interest and dividends.

Since the Plan is an account held in the United States, you are not required to provide a code indicating that you are exempt from FATCA reporting.

The Internal Revenue Service does not require your consent to any provision of this document other than the certifications required to avoid backup withholding.

Please note that, by signing this form, you declare that you make the above certifications under penalties of perjury. Under penalties of perjury, I certify the above statements.

|

|

{FNamePrint} |

|

{FSigDate} |

Signature of Participant |

|

Name - please print |

|

Date |

The following sections are to be completed by the Plan Representative.

8. Withdrawal Details

Has the final contribution been submitted for this participant?

If the final payroll for this participant has not been submitted

to John Hancock Retirement Plan Services, provide the final payroll ending date.

If a date is provided, John Hancock Retirement Plan Services will coordinate processing of this distribution with receipt of the final payroll to avoid additional contribution payouts that often remain uncashed.

Is the participant withdrawing

For a total withdrawal, we will report the original rollover amount processed as the amount allocable to IRR assets. For a partial withdrawal, provide the amount allocable to IRR assets $ {TaxDollar4}

Note: All Roth assets held by the participant would need to be taken into consideration when calculating the amount allocable to the IRR. If left blank, we will report the amount requested as being first allocable to the IRR assets.

GP5479US (2/2021) |

Page 7 of 9 |

Group annuity contracts and recordkeeping agreements are issued by: John Hancock Life Insurance Company (U.S.A.) (“John Hancock USA”), Boston, MA (not licensed in New York) and John Hancock Life Insurance Company of New York (“John Hancock NY”), Valhalla, NY. Product features and availability may differ by state. John Hancock USA and John Hancock NY each make available a platform of investment alternatives to sponsors or administrators of retirement plans without regard to the individualized needs of any plan. Unless otherwise specifically stated in writing, John Hancock USA and John Hancock NY do not, and are not undertaking to, provide impartial investment advice or give advice in a fiduciary capacity.

It is important that information on the allocable amount be provided to John Hancock Retirement Plan Services if this allocation order is not consistent with the terms of your Plan.

IRS Distribution Code

The applicable IRS distribution code will be based on the type of distribution and/or age of the participant.

If the early distribution exception code applies check here. |

(Code 2 will be applied) |

Code B will be included with the applicable code if the distribution includes Designated Roth contributions and the combination is valid.

Loans

If a loan is active at time of distribution (Termination, Retirement or Disability), we will apply the applicable age dependent loan distribution code.

Loans can only be rolled over to an employer sponsored qualified plan.

If the loan rollover code applies check here. |

(Code G will be applied) |

Vesting percentage(s)

Vesting is mandatory for partial and total termination, retirement, disability and total

The unvested money will be forfeited using instructions given in the Employer Unvested Money section below. For all other withdrawals vesting is not required.

% for ALL Employer money types

OR

Vesting varies by money type as indicated below

Money Type |

% |

|

|

ER Match |

{VestPct} |

Profit Sharing |

{VestPct2} |

Employer Unvested Money

Other ER Money |

% |

|

|

{PortionTypeER1} |

{VestPct3} |

{PortionTypeER2} |

{VestPct4} |

Other ER Money |

% |

|

|

{PortionTypeER3} |

{VestPct5} |

{PortionTypeER4} |

{VestPct6} |

If no box is selected below, direction for forfeitures previously provided to John Hancock will be applied to any unvested money in the participant’s account. If no direction for forfeitures has been provided and no box is selected below, any unvested money will remain in the participant’s account invested according to the current investment instructions.

If you determine the unvested portion of the account is not forfeitable, then you may wish to select leave in participant’s account as invested so that the participant continues to have the ability to direct the investment of the full balance of his/her account (including any unvested money).

Transfer to Cash Account |

Pay outstanding John Hancock charges |

Refund to Plan Trustee |

Leave in Participant account and transfer to default fund |

|

Leave in Participant account as invested |

9. Third Party Administrator (TPA) Withdrawal Fee

${TaxDollar5} |

OR |

{TaxPercent4}% |

||

|

|

|

|

|

Flat Fee Amount |

|

Percentage of |

||

|

|

|

Invested Balance |

|

John Hancock Retirement Plan Services is not responsible for any uncollected fee amounts as a result of insufficient funds. These shortages will be reported on the transaction and summary confirmations.

No Fee will be applied if this section is not completed.

GP5479US (2/2021) |

Page 8 of 9 |

Group annuity contracts and recordkeeping agreements are issued by: John Hancock Life Insurance Company (U.S.A.) (“John Hancock USA”), Boston, MA (not licensed in New York) and John Hancock Life Insurance Company of New York (“John Hancock NY”), Valhalla, NY. Product features and availability may differ by state. John Hancock USA and John Hancock NY each make available a platform of investment alternatives to sponsors or administrators of retirement plans without regard to the individualized needs of any plan. Unless otherwise specifically stated in writing, John Hancock USA and John Hancock NY do not, and are not undertaking to, provide impartial investment advice or give advice in a fiduciary capacity.

10. Trustee/Authorized Signer Signature

If the participant fails to sign the Signature section, the Trustee/Authorized Signer below certifies, under penalties of perjury, that based on the plan sponsor's record, (i) the name shown on this form is the legal name of the participant; (ii) the number shown on this form is the correct taxpayer identification number (Social Security Number) of the participant; and, (iii) the participant is a U.S. person (including a U.S. resident alien) unless indicated otherwise above. I acknowledge that John Hancock Retirement Plan Services will rely on this certification in determining the tax withholding and reporting requirements applicable to the requested distribution and agree to hold John Hancock Retirement Plan Services harmless for any errors made in reliance upon this certification.

I hereby authorize John Hancock Retirement Plan Services to rely and act upon the instructions provided on this form. I understand that it is my responsibility to ensure that the withdrawal(s) requested herein are permitted by law and, if applicable, consistent with the terms of the Plan. If the amount withdrawn is paid directly to the Plan Trustee, I also agree and acknowledge that I am responsible for the proper handling of the funds in accordance with the requirements of the law.

I certify that all the above information is complete and correct, that the required participant elections and consent and, if applicable, spousal consent for married participants as required by IRC Sec. 417, have been properly obtained, and that the funds being withdrawn are not for the purpose of prohibited transactions as defined in IRC Sec. 4975. I also certify that all necessary and applicable information required to be furnished to the participant under IRC Sec. 417 and an explanation of the direct rollover option and related tax rules required by IRC Sec. 402 have been provided. I also certify that, if applicable, (i) the participant has waived the

In the event that the participant is under the age of 18, I certify that consent to this request has been obtained from the parent or legal guardian authorized to act on the participant's behalf.

I hereby direct John Hancock Retirement Plan Services to pay to the Third Party Administrator currently on record the above referenced fee (if applicable). I understand that this fee will be deducted from the participant's account balance at the time of the distribution using standard withdrawal protocol and will be held in the general business account of John Hancock Retirement Plan Services until paid to the Third Party Administrator. I hereby represent that this fee is in accordance with the fee schedule that has been approved by the plan's trustee or named fiduciary as reasonable and authorized under the terms of the plan.

On behalf of the Plan Sponsor, the Plan and its related trust, and the Plan Trustee or named Fiduciary, I further agree to indemnify and hold harmless John Hancock Retirement Plan Services, its employees, agents, directors, and officers from any liability, penalties, and taxes that may be incurred as a result of the requested distribution giving rise to one or more prohibited transactions or for implementing requests (including, if applicable, a direct rollover request) based solely on the instructions provided on this form, or if any of the certifications provided on this form are incorrect.

|

|

{FNamePrint} |

|

{FSigDate} |

Signature of Trustee/Authorized Signer |

|

Name - please print |

|

Date |

GP5479US (2/2021) |

Page 9 of 9 |

Group annuity contracts and recordkeeping agreements are issued by: John Hancock Life Insurance Company (U.S.A.) (“John Hancock USA”), Boston, MA (not licensed in New York) and John Hancock Life Insurance Company of New York (“John Hancock NY”), Valhalla, NY. Product features and availability may differ by state. John Hancock USA and John Hancock NY each make available a platform of investment alternatives to sponsors or administrators of retirement plans without regard to the individualized needs of any plan. Unless otherwise specifically stated in writing, John Hancock USA and John Hancock NY do not, and are not undertaking to, provide impartial investment advice or give advice in a fiduciary capacity.

Form Characteristics

| Fact Name | Details |

|---|---|

| Form Purpose | The GP5479US form is used for requesting a withdrawal from a retirement plan, with options for cash distribution or rollover. |

| Withdrawal Options | Participants can choose to keep money in the plan, roll over to an IRA or employer-sponsored plan, or take a cash distribution. |

| Tax Implications | Withdrawals may be subject to taxes and penalties. Consulting a tax advisor is recommended before proceeding. |

| Eligibility Requirement | Participants must provide necessary supporting documents as required by their plan before processing the withdrawal. |

| Form Completion | Sections 1-7 are completed by the participant, while Sections 8-10 are completed by the Plan Representative. |

| 1099 Reporting | A 1099R form will be issued for each distribution, indicating the taxable amount, by January 31 of the following year. |

| Processing Guidelines | The form is subject to John Hancock's Administrative Guidelines, which outline processing protocols for financial transactions. |

| State-Specific Regulations | Product features and availability may differ by state. Certain laws govern retirement distributions, so participants should consult their plan administrator. |

Guidelines on Utilizing Gp5479Us

Completing the GP5479US form is an important step if you're considering a cash distribution or other options related to your retirement benefits. It's essential to provide accurate information and follow the outlined instructions carefully to ensure your request is processed smoothly. Below are the steps to fill out the form correctly.

- Fill Out General Information: Include your Plan's name, Contract number, your name as it appears on your Social Security Card, and your Social Security Number. Provide your birthdate, address, and phone number.

- Select the Reason for Withdrawal: Choose one option that best describes your reason for withdrawal from the drop-down list provided on the form.

- Specify Withdrawal Amount: Indicate whether you want to withdraw 100% of your vested account value or a specific portion. If choosing the latter, specify the amount or percentage from each eligible money type.

- Decide on Your Distribution Destination: If the funds are going to one destination, complete Section A. If splitting to multiple destinations, complete Section B.

- Provide Payment Information: Fill in the necessary details for your selected payout option including account numbers for IRAs or employer-sponsored plans. Also, indicate whether the payment will be via direct deposit, wire, or check.

- Submit Your Form: Once all sections are filled out, return the completed form to your Plan Representative as instructed.

- Consult with a Professional: If uncertain on any section, consider consulting with a financial advisor or the John Hancock Rollover Specialists for assistance before finalizing your submission.

After submitting the form, the Plan Representative will review it and facilitate the processing based on your provided instructions. Keep an eye out for a 1099R form, which you should receive by January 31 of the following year for tax purposes. If you have any questions or need additional assistance, John Hancock's customer service is available to help.

What You Should Know About This Form

What is the Gp5479Us form used for?

The Gp5479Us form is primarily used for requesting withdrawals from a retirement plan. It allows participants to specify whether they want to take a cash distribution or roll over their funds to another retirement account, such as an IRA or their new employer's plan. The form includes various sections where participants provide their personal information, the withdrawal amount, and their desired destination for the funds.

What should I consider before taking a cash distribution?

Before opting for a cash distribution, it's important to understand that taxes and potential penalties may apply. Cashing out can significantly affect your long-term savings due to these deductions. To better understand the financial implications, you can visit www.JHCashOutCalculator.com, which offers tools to assess how a cash distribution could impact your overall retirement savings strategy.

Who can assist me in completing the Gp5479Us form?

Participants have two avenues for assistance when completing the Gp5479Us form. They can either call John Hancock at 1-888-695-4472 to connect with Rollover Specialists who can guide them through their options and help with paperwork, or they can work directly with their financial representative. They can also review their options independently by utilizing the attached form and following the provided instructions.

Are there any specific steps I need to follow when submitting the form?

Yes, participants must complete Sections 1 to 7 of the Gp5479Us form and return it to their Plan Representative. The Plan Representative will then review these sections and complete Sections 8 to 10. Keep in mind that your plan may require additional supporting documents before processing your withdrawal request, so check with your plan administrator for any specific submission guidelines.

Common mistakes

Filling out the GP5479US form can have significant implications for your retirement savings. Here are some common mistakes people make:

People often overlook the need to provide complete and accurate personal information. Missing details, such as Social Security numbers or addresses, can delay processing or lead to denial of the request. It’s essential to ensure that all sections are filled out correctly, as incomplete forms typically complicate matters.

Another common error involves selecting the wrong option for the reason of withdrawal. Each option comes with specific requirements. Selecting a reason that does not align with your situation could result in unnecessary delays or complications. Read the options carefully and choose the one that accurately describes your circumstances.

Many individuals fail to fully understand the tax implications of their choices on the form. Each distribution method has its own tax consequences. For instance, opting for a direct rollover may not incur immediate taxes, while taking a cash distribution usually does. It’s crucial to consult tax professionals or the provided guidance to make informed decisions.

Moreover, people sometimes assume that simply signing the form is the last step. However, the form may require additional supporting documents. Ignoring this can slow down the process or result in rejection. Always check if attachments or extra documentation are needed before submission.

Another mistake is choosing to leave the money in the plan without reviewing the implications. Some participants do so without fully understanding their options, which might limit future financial flexibility. It’s advisable to assess all available alternatives and the benefits or drawbacks associated with each choice.

Failing to notify changes in personal information can create issues as well. For example, if your address has changed, it is important to update this on the form and ensure your old records are corrected. Otherwise, future correspondence or notices may not reach you.

People may also neglect the section on where to send the money. This can introduce confusion regarding where funds are directed. Double-check that the information for account destinations is accurate, whether rolling over to an IRA or receiving a cash distribution.

Lastly, many individuals do not reach out for help when needed. Whether it's to clarify sections of the form or to ask about their options, seeking assistance can prevent mistakes. Utilizing resources such as the helpline or your financial representative can lead to a smoother process.

Documents used along the form

The Gp5479Us form is a crucial document for participants considering withdrawing from or rolling over their retirement plan savings. When completing this process, there are several other forms and documents that may be necessary. Understanding these documents can facilitate a smoother transition and ensure compliance with necessary regulations.

- Withdrawal – Eligible for Rollover Form: This form allows participants to officially request a cash withdrawal or rollover of their retirement funds. It requires detailed information about the amount to be withdrawn and how the funds should be distributed.

- 1099-R Form: The IRS issues this form to report distributions from pensions, annuities, retirement plans, and individual retirement accounts (IRAs). Participants will receive this form by January 31 of the following year for tax purposes.

- Administrative Guidelines for Financial Transactions (AGFT): This document outlines the rules and procedures that govern how John Hancock processes withdrawals and rollovers. It serves as a reference to understand the requirements and any penalties tied to early distributions.

- Summary Plan Description (SPD): This is a comprehensive guide that contains vital information about the retirement plan, including benefits, rights, and responsibilities. It can help participants understand the specific options available under their particular plan.

Familiarity with these additional documents is essential for participants navigating their retirement savings options. Ensuring all forms are completed accurately and submitted on time will help avoid delays and potential issues with tax implications.

Similar forms

The GP5479US form bears similarities to several other documents related to retirement plan distributions. Here are four that share commonalities:

- Withdrawal Request Form: Like the GP5479US, a typical withdrawal request form allows participants to request a distribution from their retirement plans. Both forms require personal information and details about the requested distribution amount and type.

- Rollover Request Form: This document facilitates the transfer of retirement funds to another qualified plan or IRA. Similar to the GP5479US, it provides options for participants to indicate where they want their funds deposited and includes tax implications for each choice.

- Tax Withholding Election Form: Participants must use this form to decide how much tax to withhold on their distributions. Both forms highlight potential tax consequences and require similar personal and account information to ensure accuracy in processing withdrawals.

- Plan Distribution Agreement: This agreement outlines the terms and conditions under which funds can be distributed from a retirement plan. It parallels the GP5479US in providing necessary details about the participant's rights and the required steps to take a distribution.

Dos and Don'ts

- Do read the entire form carefully before filling it out.

- Don't leave any required fields blank; incomplete forms can delay processing.

- Do ensure your personal information matches your Social Security card.

- Don't forget to sign and date the form where indicated.

- Do consult with a financial advisor to understand tax implications.

- Don't use correction fluid; make changes with initials in pen only.

- Do ask questions if you're unclear about any of the options.

- Don't skip the instructions provided by your plan administrator.

- Do keep a copy of your completed form for your records.

Misconceptions

Here are ten common misconceptions about the GP5479US form, along with clarifications for each:

- Misconception 1: The form is only for retirement plan participants.

- Misconception 2: Submitting the form guarantees immediate cash distribution.

- Misconception 3: There are no tax consequences when taking a cash distribution.

- Misconception 4: Participants can complete the form however they want.

- Misconception 5: The GP5479US form is used the same way across all plans.

- Misconception 6: All forms of withdrawal incur the same penalties.

- Misconception 7: A 1099R will not be issued for rolled-over amounts.

- Misconception 8: Once submitted, the form cannot be changed.

- Misconception 9: Participants must be retiring to use this form.

- Misconception 10: You only need to fill out the form; no further assistance is available.

This form is intended for participants, but it also requires the plan administrator's involvement for validation.

Processing takes time. The form submission must adhere to the procedures outlined by the plan administrator.

Tax implications and potential penalties may apply. Participants should consult a tax advisor for personalized advice.

Accuracy is crucial. The form requires specified sections to be completed in order to process requests correctly.

Each retirement plan may have unique rules. It is essential to refer to the plan's specific guidelines and the Summary Plan Description.

Different withdrawal types have different tax consequences and penalties. Understanding these differences is critical.

A 1099R form will be issued for all taxable distributions, including those rolled over, by January 31 of the following year.

Changes can be made to the form. However, they must be done carefully, following the outlined processes for corrections.

The form can also be used in circumstances such as job changes or financial hardship, not limited to retirement.

John Hancock provides Rollover Specialists to assist participants throughout the process. Support is readily available.

Key takeaways

Filling out and using the GP5479Us form requires attention to detail. Be sure to read all instructions carefully to avoid mistakes that could delay the process.

- Understand tax implications before choosing a cash distribution. Taxes and possible penalties may apply.

- Identify the reason for your withdrawal. Options include termination of employment, retirement, disability, or voluntary contributions.

- Complete Sections 1 through 7 if you are the participant. Your Plan Representative will fill out Sections 8 through 10.

- Provide your correct personal information, including your Social Security Number and address. Inaccuracies may lead to complications in processing your request.

- Consider your options carefully before you decide to take a cash distribution. There may be better alternatives that could benefit you in the long run.

- Seek help if needed. Contact John Hancock at 1-888-695-4472 for assistance or clarification regarding the options available.

- Stay informed about potential changes. The address or other details provided may need updating in your account records.

- Be aware that a 1099R form will be issued for any distribution. You will need this for tax reporting purposes.

Approaching the GP5479Us form with clarity will help ensure a smoother process. If you have questions, do not hesitate to reach out for support.

Browse Other Templates

External User Access Request,OASAS Access Authorization Form,Confidential Data Access Application,User Access Registration Form,OASAS System Access Application,Access Request Form for OASAS Systems,Agency Access Approval Form,Authorized User Access R - The accessing individual must sign to confirm they understand access rules.

Donor Profile - History of any events attended by the donor.