Fill Out Your Mf 10023 16 Form

The MF 10023 16 form serves as an essential tool for individuals looking to establish an Individual Retirement Account (IRA) or a Roth IRA with The Hartford Mutual Funds. Designed for various retirement account options such as Traditional IRAs, Rollover IRAs, and Roth IRAs, this form guides users in selecting investment funds, indicating the desired contributions, and completing essential personal information. The form incorporates sections for beneficiaries, fund selection, and investment amounts, which help streamline the account setup process. Importantly, it outlines requirements for annual maintenance fees, account type categorizations, and specific contributions related to different tax years. Additionally, this comprehensive form includes information on transferring funds, setting up direct rollovers from qualified plans, and stipulations for telephone exchanges. With careful attention to detail, users can navigate through investment choices and regulatory requirements while ensuring compliance with tax laws, paving the way for effective retirement planning.

Mf 10023 16 Example

|

|

|

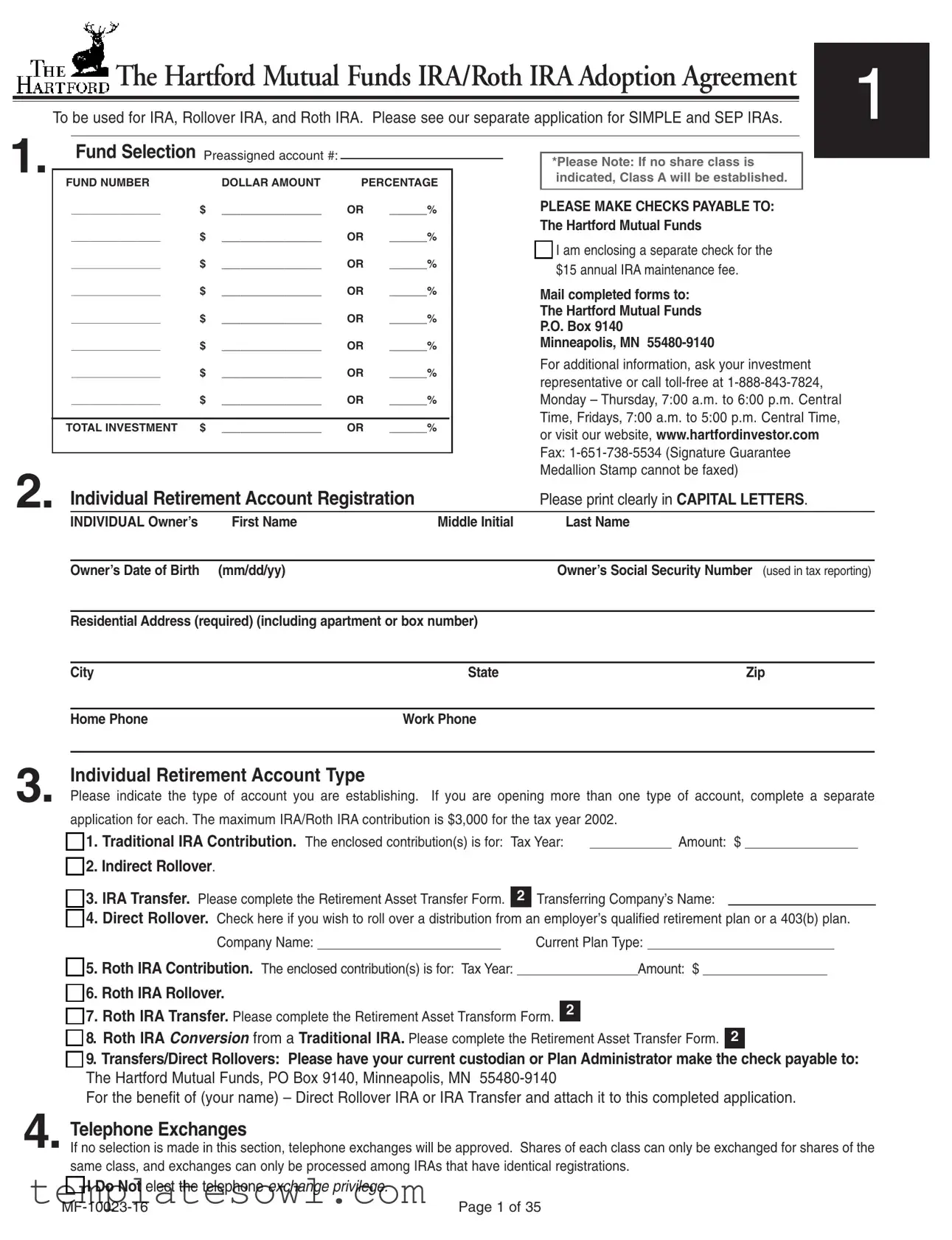

The Hartford Mutual Funds IRA/Roth IRA Adoption Agreement |

|

1 |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

To be used for IRA, Rollover IRA, and Roth IRA. Please see our separate application for SIMPLE and SEP IRAs. |

|

|||||||||||||

1. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

Fund Selection Preassigned account #: |

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

*Please Note: If no share class is |

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||

FUND NUMBER |

|

DOLLAR AMOUNT |

PERCENTAGE |

|

|

indicated, Class A will be established. |

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

____________________ |

$ |

________________ |

OR |

______% |

|

|

|

PLEASE MAKE CHECKS PAYABLE TO: |

|

|

||||

|

|

|

|

$ |

________________ |

OR |

______% |

|

|

|

The Hartford Mutual Funds |

|

|

|||

|

|

____________________ |

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

■ I am enclosing a separate check for the |

|

|

|||

|

|

____________________ |

$ |

________________ |

OR |

______% |

|

|

|

$15 annual IRA maintenance fee. |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

____________________ |

$ |

________________ |

OR |

______% |

|

|

|

Mail completed forms to: |

|

|

||||

|

|

____________________ |

$ |

________________ |

OR |

______% |

|

|

|

The Hartford Mutual Funds |

|

|

||||

|

|

|

|

|

P.O. Box 9140 |

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

____________________ |

$ |

________________ |

OR |

______% |

|

|

|

Minneapolis, MN |

|

|

||||

|

|

____________________ |

$ |

________________ |

OR |

______% |

|

|

|

For additional information, ask your investment |

|

|

||||

|

|

|

|

|

representative or call |

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

____________________ |

$ |

________________ |

OR |

______% |

|

|

|

Monday – Thursday, 7:00 a.m. to 6:00 p.m. Central |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

Time, Fridays, 7:00 a.m. to 5:00 p.m. Central Time, |

|

|

|||

|

|

TOTAL INVESTMENT |

$ |

________________ |

OR |

______% |

|

|

|

|

|

|||||

|

|

|

|

|

or visit our website, www.hartfordinvestor.com |

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

Fax: |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

2. Individual Retirement Account Registration |

|

Medallion Stamp cannot be faxed) |

|

|

|||||||||||

|

Please print clearly in CAPITAL LETTERS. |

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

INDIVIDUAL Owner’s |

First Name |

Middle Initial |

Last Name |

|

|

|

|

Owner’s Date of Birth |

(mm/dd/yy) |

|

Owner’s Social Security Number (used in tax reporting) |

|

|

||

Residential Address (required) (including apartment or box number) |

|

||

|

|

|

|

City |

|

State |

Zip |

|

|

|

|

Home Phone |

|

Work Phone |

|

3. |

Individual Retirement Account Type |

|

|

|

|

|

|

|

|

||

|

Please indicate the type of account you are establishing. If you are opening more than one type of account, complete a separate |

||||

|

application for each. The maximum IRA/Roth IRA contribution is $3,000 for the tax year 2002. |

|

|

|

|

|

■ 1. Traditional IRA Contribution. The enclosed contribution(s) is for: Tax Year: |

|

Amount: $ |

|

|

|

■ 2. Indirect Rollover. |

|

|

|

|

■ 3. IRA Transfer. Please complete the Retirement Asset Transfer Form. 2 Transferring Company’s Name:

■4. Direct Rollover. Check here if you wish to roll over a distribution from an employer’s qualified retirement plan or a 403(b) plan.

Company Name: |

|

Current Plan Type: |

■

■

■

■

■

5. Roth IRA Contribution. The enclosed contribution(s) is for: Tax Year:

6.Roth IRA Rollover.

7.Roth IRA Transfer. Please complete the Retirement Asset Transform Form. 2

8.Roth IRA CONVERSION from a Traditional IRA. Please complete the Retirement Asset Transfer Form. 2

9.Transfers/Direct Rollovers: Please have your current custodian or Plan Administrator make the check payable to: The Hartford Mutual Funds, PO Box 9140, Minneapolis, MN

For the benefit of (your name) – Direct Rollover IRA or IRA Transfer and attach it to this completed application.

4. Telephone Exchanges

If no selection is made in this section, telephone exchanges will be approved. Shares of each class can only be exchanged for shares of the same class, and exchanges can only be processed among IRAs that have identical registrations.

■

I Do Not elect the telephone exchange privilege.

Page 1 of 35 |

5. Broker Dealer Your investment representative can supply this information

Registered Representative’s First Name |

Middle Initial |

Last Name: |

|

|

|

Broker Dealer Name |

|

|

|

|

|

Branch Street Address |

|

|

|

|

|

City |

State |

Zip |

|

|

|

Phone Number |

Dealer Number |

Branch Number |

|

|

|

Rep Number |

|

|

Reduced Sales Charges (optional) |

|

|

6. RIGHTS OF ACCUMULATION To qualify for sales discounts on Class A shares, list below the account or contract numbers of all classes of shares of other Hartford Mutual Funds and The Director variable annuity or Variable Life insurance, Saver Plus and CRC con-

tracts that you or your family (spouse, children,

Fund Name |

Fund Name |

|

|

|

|

Account Number |

Account Number |

|

|

|

|

SSN/Tax ID |

SSN/Tax ID |

|

|

|

|

The variable annuity contract or variable life insurance policy #__________________________ |

Approximate Value $ ___________ |

|

LETTER OF INTENTION I intend to buy more Class A shares and understand that I can reduce my sales charges through accumulated investments. I plan to invest over a 13 month period following the date of this application (or a date within the

past 90 days) an aggregate amount of at least:

■

$50,000

■

$100,000

■$250,000

■

$500,000

■

$1,000,000

|

QUALIFY FOR NET ASSET VALUE (NAV): This account qualifies for NAV purchase as described in the fund prospectus as stated below. |

|||||||||

|

|

|

|

|

Other Explain |

|

|

|||

|

■ |

Proceeds from another load fund within 60 days. (initial purchase only) |

|

■ |

|

|

||||

7. |

Beneficiary Instructions (use an additional page if necessary.) I hereby designate the person(s) named below as Primary Beneficiary(ies) in accordance with the |

|||||||||

IRA custodial agreement: This Designation of Beneficiary may have important tax or estate planning effects. Also, if you are married and reside in a community prop- |

||||||||||

erty or marital property state (Arizona, California, Idaho, Louisiana, Nevada, Texas, Washington or Wisconsin), you may need to obtain your spouse’s consent if you have not |

||||||||||

|

designated your spouse as Primary Beneficiary for at least half of your Roth or traditional IRA. See your lawyer or other tax professional for additional information and advice. |

|||||||||

|

|

|

|

|

|

Social Security |

Date of Birth/ |

Spouse: Yes/No |

||

|

|

|

First Name, Middle Initial, Last Name |

Percentage |

|

Number |

Date of Trust |

or Trust |

||

|

Name of |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Primary |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Beneficiaries |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

Please be sure that Percentages add up to a total of 100%

Name of Contingent Beneficiaries (optional)

8. IRA Agreement

I (i) am of legal age and legal capacity; (ii) have received and read a current prospectus of any fund and description of any choice selected; (iii) agree that an annual maintenance fee of $15 will be deducted from my IRA unless I have paid the fee separately;(iv) certify under the penalties of perjury that the taxpayer identification number (Social Security Number) set forth in Section 2 is true, correct, and complete;(v) appoint U.S. Bank National Association as custodian. The depositor and the custodian hereby adopt an agreement establish- ing an individual retirement account IRA. Its terms are described in the appropriate IRA custodial agreement. The depositor acknowledges having received and read the agreement. The agreement shall govern the depositor’s IRA established pursuant to this adoption agreement and investing in the

I assume complete responsibility for determining whether I am eligible to contribute to a Roth or Traditional IRA, and that my contributions, including rollovers and conversions, meet the limits and guidelines set forth under tax law. I understand the tax consequences associated with both contributions to, and distributions from my Hartford Mutual Funds Roth or Traditional IRA.

Owner’s Signature |

|

Date ______________________________________ |

Please make all checks payable to The Hartford Mutual Funds.

Page 2 of 35 |

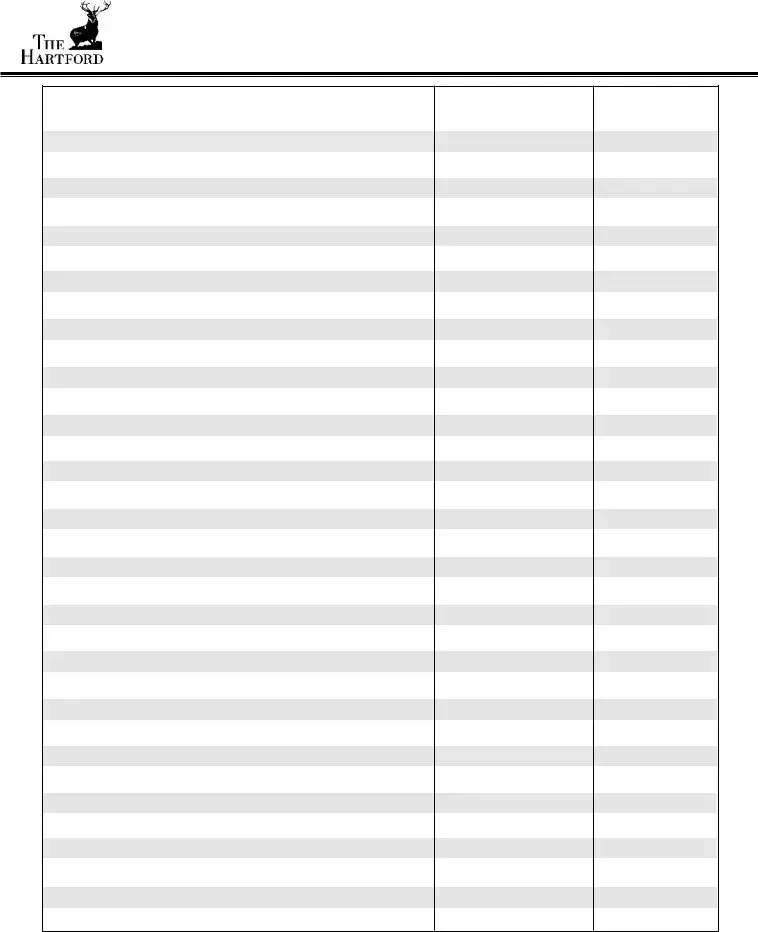

The Hartford Mutual Funds (Fund Numbers)

The Hartford Mutual Funds |

Class A |

|

Fund # |

Advisers Fund |

210 |

Capital Appreciation Fund |

214 |

Disciplined Equity Fund |

215 |

Dividend and Growth Fund |

223 |

Equity Income Fund |

1658 |

Focus Fund |

1269 |

Global Communications Fund |

1224 |

Global Financial Services Fund |

1220 |

Global Health Fund |

1610 |

Global Leaders Fund |

206 |

Global Technology Fund |

1606 |

Growth Fund |

1228 |

Growth Opportunities Fund |

1618 |

High Yield Fund |

316 |

Income Fund |

1638 |

Inflation Plus Fund |

1646 |

International Capital Appreciation Fund |

1273 |

International Opportunities Fund |

207 |

International Small Company Fund |

1277 |

MidCap Fund* |

937 |

MidCap Value Fund |

1281 |

Money Market Fund |

940 |

Short Duration Fund |

1642 |

Small Company Fund |

205 |

SmallCap Growth Fund |

1622 |

Stock Fund |

221 |

1650 |

|

1626 |

|

1630 |

|

1654 |

|

Total Return Bond Fund |

217 |

U.S. Government Securities Fund |

1634 |

Value Fund |

1285 |

Value Opportunities Fund |

1614 |

Class B Fund #

211

228

220

224

1659

1270

1225

1221

1611

285

1607

1229

1619

202

1639

1647

1274

208

1278

978

1282

290

1643

227

1623

972

1651

1627

1631

1655

218

1635

1286

1615

Class C Fund #

212

237

243

248

1660

1271

1226

1222

1612

291

1608

1230

1620

203

1640

1648

1275

239

1279

238

1283

259

1644

231

1624

242

1652

1628

1632

1656

254

1636

1287

1616

*The Hartford MidCap Fund is closed to new investors as of end of day July 31, 2003.

Page 3 of 35 |

Traditional/Roth IRA Disclosure Statement

This disclosure statement explains our Traditional/Roth IRA and the basic federal tax rules for Traditional and Roth IRAs.

It does not cover state or local tax rules.

Disclaimer. Please note the following limitations to this disclosure:

•This disclosure statement is based on federal laws and regulations on September 1, 2002, which are effective for tax years beginning on or after January 1, 2002.

•Additional information has been obtained from sources believed to be accurate and current as of September 1, 2002, but we do not guarantee its accuracy.

•Changes to the federal tax laws may have been made after the date this disclosure statement was prepared.

•This disclosure statement is provided for general informational purposes. You should consult with your attorney, accountant or other tax adviser before making any investments in, making withdrawals from, or taking any other actions with respect to your IRA.

•This disclosure statement does not discuss the state and local tax treatment of IRA contributions and distributions which may differ substantially from the federal tax rules. You should consult with your attorney, accountant or other tax advisor regarding any state or local tax rules that may apply to your IRA.

•Our employees and agents cannot give you tax or legal advice with respect to your IRA.

1. INTRODUCTION

You may revoke this IRA for any reason during the

If you revoke your IRA as described above, we will return everything you paid us.

2. KINDS OF IRAS

We offer you the following Traditional and Roth IRA choices:

Traditional IRA. You may establish a Traditional IRA to hold tax- deductible and

Roth IRA. You may establish a Roth IRA to hold

Conduit IRA. A Conduit IRA is designed to maintain certain IRA assets separate from other assets to preserve rollover options in the case of rollovers and transfers from a retirement plan. (See item 9(c).) The Conduit IRA may also simplify recordkeeping when converting a Traditional IRA to a Roth IRA. It is your responsibility to maintain the IRA as a Conduit IRA, if you so desire. To maintain its conduit status, you must ensure that it receives no contributions other than rollover contributions from employer retirement plans (or the converted assets).

This Traditional/Roth IRA cannot be used for the following:

Coverdell Education Savings Accounts. Formerly called Education IRAs, these accounts are used to hold

SIMPLE IRAs: These IRAs are used to hold employer

However, we offer Coverdell Education Savings Accounts and SIM- PLE IRAs through other vehicles. Please contact us for more infor- mation.

3. CONTRIBUTIONS TO YOUR IRAS

You may maintain and contribute to more than one kind of IRA. Also, you may have more than one IRA of the same type.

3(a) Maximum Contributions.

There is a combined tax law limit on how much you can contribute to all of your Traditional and Roth IRAs in a given year. The annual limit that applies to you depends on your age at the end of the calendar year

Page 4 of 35 |

Traditional/Roth IRA Disclosure Statement continued

in question and the Internal Revenue Code maximum for that tax year. For the limit in effect for any given tax year, refer to the chart below.

Limit for Taxpayers under Age 50. For 2002, your total Traditional and Roth IRA contributions cannot exceed the lesser of $3,000 or 100% of your compensation, or if you are married and file a joint tax return, the combined compensation of you and your spouse. You may also contribute to your spouse’s IRAs if you file a joint tax return, so long as the contributions made for each spouse do not exceed $3,000 (if both spouses are under age 50) and the combined IRA contributions for you and your spouse do not exceed 100% of your combined compen- sation.

Limit for Taxpayers Age 50 or Over. Starting in 2002, if you are 50 or over by the end of the applicable calendar year you may make addi- tional

Contribution Limits.

For tax years |

Contribution limit for |

Contribution limit for |

beginning in |

taxpayers under age 50 |

taxpayers age 50 or over |

2002 |

$3,000 |

$3,500 |

2003 |

$3,000 |

$3,500 |

2004 |

$3,000 |

$3,500 |

2005 |

$4,000 |

$4,500 |

2006 |

$4,000 |

$5,000 |

2007 |

$4,000 |

$5,000 |

2008 and after |

$5,000 |

$6,000 |

The annual contribution limits will be adjusted for inflation for years after 2008.

The appropriate dollar figure for the applicable tax year will replace all references to the $3,000 annual limit (or $3,500 for those age 50 or over) used in this disclosure statement.

3(b) Minimum Contribution.

You may contribute less than the maximum amount for a year, if you wish. Under our

3(c) Compensation and Alimony/Maintenance.

Compensation. Generally, if you work, the amount that you earn is compensation. Compensation includes wages, salaries, professional fees and other amounts (such as bonuses, commissions and tips) you receive for providing personal services. Compensation is based on your own earnings, without regard to state community property laws.

However, compensation does not include the following: (i) deferred compensation, (ii) pensions, annuities and other retirement income,

(iii)earnings and profits from property (including dividends, interest and rents) and (iv) amounts excluded from income (such as foreign earned income).

You may determine your compensation based on your

Alimony/Maintenance. All taxable alimony or maintenance payments received by a divorced spouse under a decree of divorce or separate maintenance is treated as compensation for IRA purposes.

Marital Status. If a taxpayer and the taxpayer’s spouse did not live together at any time during a year and did not file a joint return for that year, these married taxpayers will be treated as unmarried for pur- poses of determining the IRA contribution limits for that year.

4.TRADITIONAL IRAS 4(a) Eligibility.

General Rules. You may contribute to your Traditional IRA for any year that you (or your spouse) have compensation. You may have an IRA even if you participate in another retirement plan.

Age Limit. Under federal tax rules, you cannot contribute to your Traditional IRA for the year in which you reach age 701/2 or any later year. However, you may continue to make contributions to your spouse’s Traditional IRA until your spouse reaches age 701/2.

4(b) Types of Contributions.

There are two types of Traditional IRA contributions: those that are deductible on your income tax return

4(c)

The federal income tax deduction for contributions to a Traditional IRA for you and/or your spouse may be less than the IRA maximum contribution limit. The deduction depends on:

(1)Whether you (or your spouse) are an active participant in a retire- ment plan, and

(2)The amount of your adjusted gross income (“AGI”), or if you file a joint return, the combined AGI of you and your spouse.

Active Participant. You are an “active participant” for a year if, at any point in that year, your employer or union has a retirement plan under which money is added to your account or you are eligible to earn retirement credits. For example, you are likely to be an active partici- pant if you are covered under:

•A profit sharing plan, a pension plan, a stock bonus plan, an ESOP or an annuity plan;

•A salary reduction arrangement (for instance, under a 401(k) plan, SIMPLE IRA, or

•A

•A SIMPLE IRA with

Page 5 of 35 |

Traditional/Roth IRA Disclosure Statement continued

IRA Highlights (with 2002 values)*

Traditional |

|

Roth |

|

SEP |

|

|

|

|

|

Eligibility

•You are eligible if you (or your spouse) has taxable compensation for the year.

•There is no upper limit on your income.

•You must be under 701/2 to con- tribute.

•You are eligible to contribute if you (or your spouse) has taxable compen- sation for the year and your modified adjusted gross income is less than $110,000 (single), $160,000 (married filing jointly), or $10,000 (married fil- ing separately).

•There is no upper limit on age.

•You are eligible to participate in a

•If you are

•There is no upper limit on age.

Maximum Contribution

•$3,000 ($3,500 if age 50 or over) or, if less, 100% of your compensation (or your combined compensation, if you are married and filing jointly).

•Your maximum deductible contribu- tions will be reduced if you partici- pate in another retirement plan and your adjusted gross income is $34,000 or more (single), $54,000 or more (married filing jointly), or $0 (married filing separately).

•Your maximum

•No income restrictions on non- deductible contributions.

•No minimum annual contributions.

•$3,000 ($3,500 if age 50 or older) or, if less, 100% of your compensation (or your combined compensation, if you are married and filing jointly).

•Your maximum contribution to the Roth will be reduced if your income is between $95,000 and $110,000 (single), $150,000 and $160,000 (married filing jointly), or up to $10,000 (married filing separately).

•No minimum annual contributions.

•Your employer may contribute up to $40,000 or 25% of your compensa- tion, if less. For this purpose, your compensation will be capped at $200,000.

•If your plan offers a salary deferral option, you may contribute up to $11,000 ($12,000 if age 50 or over).

•Your participation in a SEP may reduce your

Tax Benefits

•Contributions are

•Earnings on the contributions are not taxed until withdrawn.

•Possible tax credit for making contri- butions.

•Contributions are

•Earnings are never taxed if taken as qualified distributions.

•Possible tax credit for making contri- butions.

•Contributions are excluded from your income and are not taxed until with- drawn.

•Earnings on the contributions are not taxed until withdrawn.

•Possible tax credit for making salary deferral contributions.

Payment ofBenefits

•You generally control how the bene- fits are paid and when.

•You must begin receiving minimum distributions after age 701/2.

•Distributions prior to 591/2 are subject to 10% penalty tax, unless an excep- tion applies.

•You generally control how benefits are paid and when.

•No required minimum distributions after age 701/2.

•Contributions (other than conver- sions) may be withdrawn

•Conversion contributions may be withdrawn without penalty after a 5- year holding period or after 591/2.

•Distribution of earnings not taken as qualified distributions are subject to income tax and, if prior to 591/2, a 10% penalty tax, unless an exception applies.

•You generally control how benefits are paid and when.

•You must begin receiving minimum distributions after age 701/2.

•Distributions prior to 591/2 are subject to 10% penalty tax, unless an excep- tion applies.

* This chart reflects 2002 contribution and threshold limits. Information regarding future years’ limits is located within this Disclosure Statement.

Page 6 of 35 |

Traditional/Roth IRA Disclosure Statement continued

•A

•Certain governmental plans.

Your Form

The following situations alone do not make you an active participant: receiving benefits from a previous employer’s retirement benefit plan or being covered by social security or railroad retirement.

AGI Defined. “AGI” for purposes of determining your

Full Deduction If Not Active Participants. If you (and your spouse) are not an active participant, your entire Traditional IRA contribution may be made as a

4(d)

If you are an active participant, the maximum amount of tax- deductible contributions that you may make to your Traditional IRA is

• |

Single Return/Head of Household: |

$34,000 to $44,000 |

• |

Joint Return/Qualified Widow(er): |

$54,000 to $64,000 |

• |

Married Filing Separate Return: |

$0 to $10,000 |

Full Deduction Below Range. If your AGI is below the

No Deduction Above Range. If your AGI is above the

Future Increases in

Tax Year Beginning |

Single Person |

2002 |

$34,000 - 44,000 |

2003 |

$40,000 - 50,000 |

2004 |

$45,000 - 55,000 |

2005 and thereafter |

$50,000 - 60,000 |

Tax Year Beginning |

Married Filing Jointly |

|

2002 |

$54,000 - 64,000 |

|

2003 |

$60,000 - 70,000 |

|

2004 |

$65,000 |

- 75,000 |

2005 |

$70,000 |

- 80,000 |

2006 |

$75,000 |

- 85,000 |

2007 and thereafter |

$80,000 |

- 100,000 |

4(e)

If your spouse is an active participant, but you are not, the maximum amount of

• |

Joint Return: |

$150,000 to $160,000 |

•Married Filing Separate Return: $0 to $10,000

Full Deduction Below Range. If your AGI is below this range, you (or your spouse) may make the maximum amount of

No Deduction Above Range. If your AGI is above this range, you (or your spouse) may not make any

4(f) Figuring Your Deduction Limit if Your AGI is Within a Phase- out Range.

If your AGI is within a

The second step is to apply the following formula:

$10,000 - Excess AGI x $3,000 = Deduction Limit $10,000

The third step is to adjust your result by rounding the result down to the next lower $10 level (the next lower number which ends in zero). For example, if the result is $1,525, you must round it down to $1,520. However, if the final result is between $0 and $200, your deduction limit is $200.

If both you and your spouse are active participants, the deduction limit applies separately to each spouse. You do not have to divide it between the spouses.

Your deduction limit cannot, in any event, exceed 100% of your com- pensation (or 100% of the combined compensation of you and your spouse).

Example 1 - Single, Active Participant: Ms. Smith, a single person under age 50, is an active participant and has an AGI of $38,619 in

2002. She calculates her

Her AGI is $38,619

Her Threshold Level is $34,000

Her Excess AGI is (AGI - Threshold Level) = $4,619

Page 7 of 35 |

Traditional/Roth IRA Disclosure Statement continued

So, her Traditional IRA deduction limit is:

$10,000 - $4,619 x $3,000 = $1,614 (rounded to $1,610) $10,000

Example 2 - Married Participants, Filing Joint Tax Return: Mr. and Mrs. Young file a joint tax return. Each spouse earns more than $3,000 and each is an active participant. They are both under age 50. They have a combined AGI of $56,255 in 2002. They may each contribute to an IRA and calculate their

Their AGI is $56,255

Their Threshold Level is $54,000

Their Excess AGI is (AGI - Threshold Level) = $2,255

So, each spouse would determine their Traditional IRA deduction limit as follows:

$10,000 - $2,255 x $3,000 = $2,324 (rounded to $2,320) $10,000

The deduction limit is $2,320 for Mr. Young’s Traditional IRA and $2,320 for Mrs. Young’s Traditional IRA. This gives the Youngs a max- imum deduction of $4,640 on their joint return.

Example 3 - Married Participant, Filing Separate Tax Return: Mr. Jones, a married person over 50 (and eligible to make

His AGI is $1,500

His Threshold Level is $0

His Excess AGI is (AGI - Threshold Level) = $1,500 So, his Traditional IRA deduction limit is:

$10,000 - $1,500 x $3,500 = $2,975 (rounded to $2,970) $10,000

Even though his IRA deduction limit under the formula is $2,970, Mr. Jones may not deduct an amount in excess of his compensation, so his actual deduction is limited to $1,500.

Example 4 - Spouse of Active Participant, Filing Joint Tax Return:

Mr. and Mrs. Wilson file a joint tax return. Each spouse earns more than $3,000 and are under 50. Mr. Wilson is an active participant, but Mrs. Wilson is not. Mrs. Wilson calculates her

Their AGI is $155,000.

Her threshold level is $150,000.

Her Excess AGI is (AGI - threshold level) is $5,000. Therefore her Traditional IRA deduction limit is:

$10,000 - $5,000 x $3,000 = $1,500

$10,000

Mrs. Wilson’s deduction limit is $1,500. However, because the Wilsons’ AGI is above the

4(g)

If your

(See item 3.) In addition, you may also elect to treat a Traditional IRA contribution as

Investment earnings on your

If you make a

Note: A penalty of $50 is imposed for each failure to properly file the Form 8606. In addition, a $100 penalty is imposed for any overstatement of the amount of des- ignated

4(h) Corrective Withdrawals.

You may make a

The withdrawal amount cannot be deducted on your tax return or reported as a

4(i) Tax Credit for Making IRA Contributions.

You may qualify for a new nonrefundable tax credit for contributing to your IRA. The credit is effective for the tax years beginning in 2002 through 2006. Generally, the credit for a tax year will be equal to your “applicable percentage” times the amount of “qualified retirement sav- ings contributions” as reduced by certain distributions received from retirement plans. The credit is in addition to any deduction from gross income that is otherwise allowed for the contribution.

Applicable Percentage. Your applicable percentage is determined by your filing status and your federal adjusted gross income. The maxi- mum credit rate is 50% and is subject to a

Joint |

Head of |

All other |

Applicable |

||||

Return |

Household |

Cases |

|

Percentage |

|||

Over |

Not Over |

Over |

Not Over |

Over Not Over |

|

||

$ 0 |

$30,000 |

$ 0 |

$22,500 |

$ 0 |

$15,000 |

50% |

|

30,000 |

32,500 |

22,500 |

24,375 |

15,000 |

|

16,250 |

20% |

32,500 |

50,000 |

24,375 |

37,500 |

16,250 |

|

25,000 |

10% |

50,000 |

37,500 |

25,000 |

|

0% |

|||

For example, if you and your spouse file a joint return with a federal adjusted gross income of $36,000, your applicable percentage is 10%.

Qualified Retirement Savings Contributions. Qualified retirement savings contributions include IRA contributions, as well as contribu- tions to certain other plans. The total contribution amount is reduced by any distributions to you from:

(1) a qualified retirement plan or eligible deferred compensation plan

Page 8 of 35 |

Traditional/Roth IRA Disclosure Statement continued

(which is includible in your gross income during the “testing period” which includes the current tax year, the two preceding tax years, as well as the period after such tax year and before the due date for filing the tax return), or

(2)a Roth IRA within the testing period that are not qualified rollover contributions to a Roth IRA.

Note: A distribution received by your spouse is considered your distribution if you filed a joint tax return for the year of the distribution.

The total contribution amount taken into consideration for the tax credit is capped at $2,000.

Eligible Individuals. In addition to qualifying under the income

Effect on Your Tax Liability. The credit may be used against both reg- ular and alternate minimum tax liability. The credit is applied after you apply any credit for child and dependent care and the child tax cred- it. In addition, the credit is nonrefundable and cannot reduce your total tax liability below zero.

Professional Advice. The requirements for this tax credit are very complex. We encourage you to consult with an accountant, lawyer or other qualified tax adviser about your situation.

4(j) Benefits Before Age 591/2.

Request for Payment. Upon written request, you may receive pay- ment of any or all of your Traditional IRA at any time before age 591/2. Payment may be requested for any reason, however, you must include a statement of the reason with the request.

10% Penalty Tax. In addition to regular income tax, you are subject to a penalty tax equal to 10% of the amount of taxable benefits paid before you reach age 591/2, unless an exception applies.

Exceptions. The penalty tax does not apply to benefits paid from a Traditional IRA:

•After age 591/2.

•After your death.

•After your disability (as defined below).

•In substantially equal periodic payments for your lifetime or the lifetimes of you and your beneficiary.

•For

•For higher education expenses for you, your spouse, your chil- dren and grandchildren, and your spouse’s children and grand- children.

•For unreimbursed medical expenses exceeding 7.5% of adjusted gross income for the medical care of yourself, your spouse and your dependents.

•For medical insurance premiums for you, your spouse and your dependents if all four of the following conditions apply:

(1)You lost your job;

(2)You received unemployment compensation paid under any federal or state law for 12 consecutive weeks;

(3)The distributions are made during either the year you received the unemployment compensation or the following year; and

(4)The distributions are made no later than 60 days after you have been reemployed.

Note: This includes a

•On account of a tax levy on your IRA.

Disability. You are considered disabled for purposes of the exception if you cannot do any substantial gainful activity because of your phys- ical or mental condition. A physician must determine that the condi- tion is expected to be of

A person who has not owned a principal residence for two years is considered a

If there is a delay or cancellation of the purchase or construction, the distribution may be rolled back into an IRA,

Higher Education Expenses. The exception applies to the extent that your IRA distributions during the year do not exceed the qualified higher education expenses for academic periods in that year. Such expenses include tuition, fees, books, supplies and equipment required for enrollment or attendance at an eligible educational institution on a

The qualified expenses must be reduced by the amount of any Pell Grant or other

An eligible educational institution is any college, university, vocation- al school or other

Rollover or Transfer. There is no penalty tax on the payment if it is used to make a rollover contribution. (See item 9.) Also, there is no

Page 9 of 35 |

Traditional/Roth IRA Disclosure Statement continued

penalty tax if a direct transfer between custodians or trustees is made. (See item 10.)

4(k) Benefits Between Ages 591/2 and 701/2.

Request for Payments. Upon written request, you may receive pay- ment of any or all of your Traditional IRA at any time between ages 591/2 and 701/2. Payment may be requested for any reason and you do not need to mention the reason with the request.

4(l) Benefits After Age 701/2.

Deadline. Federal tax rules require that benefit payments from your Traditional IRAs begin no later than the April 1 following the calen- dar year in which you reach age

Request for Payment. You must select, in writing, one or a combina- tion of the following forms of payment for your Traditional IRA:

•A single

•Periodic payments.

If you elected periodic payments, you may request additional pay- ments at any time.

Required Minimum Distributions. If you do not receive the entire balance of your Traditional IRA by the April 1 date, you must have started receiving payments each year that satisfy the federal required minimum distribution rules by that date. In April 2002, the IRS issued final regulations that simplify how required minimum distributions will be determined. The new rules must be used for required minimum distributions made for 2003 and beyond. In addition, the new rules may be used in 2002. This item 4(l) describes the new rules, which will result in lower required minimum distributions for most people. If you wish to determine your 2002 required minimum distribution under the old rules, consult your tax advisor for additional information.

Penalties for Failure to Take Minimum Distributions. After you reach age 701/2, you are subject to a penalty tax if the part of your Traditional IRA actually paid to you in a year is less than the minimum payment required by law. The penalty is 50% of the difference between the minimum required payment and the actual payment. If you have a pattern of failing to receive the required minimum distri- bution, the IRA could lose its

Periodic Payments. If you do not receive the entire balance of your Traditional IRA by your required beginning date, you must receive payment each year of at least your required minimum distribution.

Payments During Owner’s Lifetime. You have until April 1 of the year following the year you reach age 701/2 (your 701/2 year) to receive your distribution for your 701/2 year. The required minimum distribution for any year after your 701/2 year must be made by December 31 of that later year.

Example. You were born on February 20, 1932. You reach 701/2 on August 20, 2002. For 2002 (your 701/2 year), you must receive the required minimum distribution from your Traditional IRA no later than April 1, 2003. You must receive the required minimum distribu- tion for 2003 by December 31, 2003.

Figuring Your Required Minimum Distribution. Your required mini- mum distribution for each year is calculated by dividing the Traditional IRA account balance as of the close of business on December 31 of the preceding year by the applicable distribution period from the table.

The distribution period is based on your age and is not affected by your beneficiary’s age unless your sole beneficiary is your spouse who is more than 10 years younger than you, as discussed below.

To figure the required minimum distribution for 2003, divide your account balance at the end of 2002 by the distribution period from the table for your age as of your birthday in 2003.

Note: The table, found in the June 2002 Supplement to IRS Publication 590 (titled “Individual Retirement Arrangements (IRAs)”) is Table III (Uniform Lifetime). The correct distribution period is the "applicable divisor" listed next to your age as of the last day of the year for which you are calculating the required distribution.

However, there is a special rule for the second distribution year to take into account the fact that the first required minimum distribution need not be taken until April 1 of the year following your 701/2 year. The Traditional IRA account balance as of December 31 of the owner’s 701/2 year must be reduced by the portion (if any) of the required min- imum distribution made after the end of such year and prior to April 1 of the following year.

Example. Joe, born October 1, 1932, reached age 701/2 in 2003. He must receive his 2003 required minimum payment by April 1, 2004. Joe’s Traditional IRA account balance is $24,000 as of December 31,

Joe’s distribution period for 2003 is 26.5, as Joe turns 71 in 2003. The required minimum distribution for 2003, Joe’s first distribution year (his 701/2 year), is $905.66 ($24,000 divided by 26.5). This amount is distribut- ed to Joe by April 1, 2004.

Joe’s Traditional IRA account balance as of December 31, 2003 is $26,400. To figure the minimum amount required to be distributed for 2004, this balance is reduced by the $905.66 minimum required dis- tribution for 2003 that was made by April 1, 2004. Thus, the account balance for determining the 2004 required distribution is $25,494.36.

Joe’s distribution period for 2004 is 25.6. The required minimum dis- tribution for 2004, his second distribution year, is $995.87 ($25,494.36 divided by 25.6). This amount is distributed to Joe by December 31, 2004.

Required Minimum Distribution When a Spouse is the Sole Beneficiary. If your spouse is more than 10 years younger than you, you may figure the required minimum distribution based on your joint life expectancy. To qualify, your spouse must be the sole beneficiary of your IRA account at all times during the year for which the distribu- tions are being made. (If your spouse was your sole beneficiary in a year until the time you are divorced or widowed, you may still determine your required minimum distribution for that year using your joint life expectancy. Consult your tax advisor for additional information.)

If you qualify, your required minimum distribution for each year is cal- culated in the same manner as above, except that the distribution peri- od is based on your joint life expectancy. The distribution period is the number at the intersection of the ages of you and your spouse (as of

Page 10 of 35 |

Form Characteristics

| Fact Name | Description |

|---|---|

| Purpose | The MF 10023 16 form is intended for establishing an IRA, Rollover IRA, or Roth IRA. |

| Annual Fee | An annual maintenance fee of $15 applies unless it's paid separately at account opening. |

| Contribution Limits | The maximum contribution for tax year 2002 is $3,000 for individuals under age 50. |

| Governing Laws | Federal tax laws govern the terms of this form, subject to changes post-September 1, 2002. |

| Contact Information | For assistance, individuals can call 1-888-843-7824 during business hours. |

| Beneficiary Designation | The form requires naming primary and contingent beneficiaries, which has tax implications. |

| Revocation Period | Account holders can revoke their IRA within seven days of signing the application without penalty. |

Guidelines on Utilizing Mf 10023 16

Filling out the Mf 10023 16 form correctly is essential for setting up your Individual Retirement Account (IRA) or Roth IRA. This structured process requires attention to detail and accurate representation of your personal and financial information. Below are the steps to guide you through completing the form.

- Begin by entering the amount you wish to invest: Write the total investment amount in the designated section at the top of the form.

- Select your fund: Indicate the fund by filling in the FUND NUMBER, DOLLAR AMOUNT, and PERCENTAGE for each investment choice.

- Provide your personal details: Section 2 requires you to print your first name, middle initial, last name, date of birth, and social security number. Make sure to include your residential address, home phone, and work phone.

- Choose your IRA type: In Section 3, check the box corresponding to the account you are establishing, such as Traditional IRA, Roth IRA Contribution, or Indirect Rollover. If necessary, include details about the transferring company.

- Fill out the telephonic exchanges section: Decide whether to elect the telephone exchange privilege and make the appropriate selection.

- Provide your investment representative's information: Enter the details of your registered representative and the broker dealer.

- Complete the Rights of Accumulation: List the account or contract numbers already owned by you or your family that qualify for sales discounts.

- Designate your beneficiaries: In Section 7, provide the names and information of primary and contingent beneficiaries, ensuring percentages total 100%.

- Read and sign the IRA agreement: Acknowledge that you have read the agreement and sign where indicated. Include the date of your signature.

- Attach the necessary fees: If applicable, include a separate check for the $15 annual IRA maintenance fee and ensure all checks are made payable to The Hartford Mutual Funds.

- Mail the completed form: Finally, send the filled-out form along with any necessary documents to the specified address: The Hartford Mutual Funds, P.O. Box 9140, Minneapolis, MN 55480-9140.

What You Should Know About This Form

What is the purpose of the MF 10023 16 form?

The MF 10023 16 form is designed for individuals looking to establish a mutual fund Individual Retirement Account (IRA) or Roth IRA. It serves as an adoption agreement that allows users to select different types of accounts such as Traditional IRAs, Rollover IRAs, and Roth IRAs. Through this form, individuals can also specify their fund selections, designate beneficiaries, and understand the terms and fees associated with the accounts.

What are the different types of accounts that can be opened using this form?

This form allows you to establish several types of accounts, including Traditional IRAs, Roth IRAs, Indirect Rollovers, IRA Transfers, Direct Rollovers, and Roth IRA Conversions. If an individual wishes to open more than one type of account, a separate application must be completed for each type.

What fees are associated with the IRA set up?

There is an annual maintenance fee of $15 for the IRA. This fee can either be deducted directly from the IRA account or a separate check can be enclosed with the form. This ensures that individuals are aware of any potential charges before finalizing their account setup.

How can beneficiaries be designated on this form?

The form allows you to name both primary and contingent beneficiaries. It is crucial to list the names, dates of birth, and social security numbers of beneficiaries accurately. Additionally, ensure the total percentages add up to 100%. This designation has significant tax and estate planning implications, especially for married individuals living in community property states.

Where should the completed form be sent?

Once the form is completed, send it to The Hartford Mutual Funds at their designated address: P.O. Box 9140, Minneapolis, MN 55480-9140. This ensures that your application is handled promptly and accurately. If you have any questions, you can contact customer service at 1-888-843-7824 or visit their website for further assistance.

Common mistakes

Filling out the Mf 10023 16 form can be a straightforward process, but there are common mistakes that individuals often make, which can lead to delays or complications in their applications. One prevalent mistake is failing to provide the required account information accurately. Each section of the form asks for specific details, such as the fund number, dollar amount, and percentage of investment. Leaving these fields blank or providing incorrect information can result in the submission being deemed incomplete.

Another mistake involves overlooking the necessity of checks being made payable to the right entity. Inadequate attention to detail can lead to checks addressed incorrectly, which may cause funds to be rejected or delayed in processing. Participants should double-check the information to ensure they are following the instructions precisely.

People often struggle with the account type selection aspect of the form. Individuals sometimes mark more than one type of account without realizing that the form requires a single selection for each application. If someone intends to open multiple account types, they must complete separate applications. This error can prolong the account setup process and may lead to confusion on the part of the financial institution.

Another common oversight occurs in the beneficiary designation section. It is vital that individuals specify their primary and contingent beneficiaries clearly. If the percentages do not total 100% or if names are illegible, this can create further complications down the line. Giving attention to detail in this section is crucial for ensuring that funds are distributed according to the owner’s wishes.

Lastly, people sometimes fail to read the IRA agreement and the additional disclosures included with the form. Understanding the terms, fees, and potential penalties is essential when deciding on contributions or account types. Ignorance of these terms can lead to unintentional violations of IRS rules or the investor’s misalignment with their financial goals.

Documents used along the form

The Mf 10023 16 form is used to establish an Individual Retirement Account (IRA) with The Hartford Mutual Funds. Along with this form, several other documents and forms may be required or beneficial in the IRA application process. Below is a description of commonly used forms and documents related to the Mf 10023 16.

- Retirement Asset Transfer Form: This form facilitates the transfer of assets from another retirement account into a new or existing IRA. It provides the necessary information for the transferring institution to process the rollover efficiently.

- Annual IRA Maintenance Fee Payment Form: This document allows account owners to manage their annual maintenance fee payment obligations, which are typically required to keep the IRA active with certain institutions.

- Beneficiary Designation Form: This form is used to specify primary and contingent beneficiaries for the account. It is essential for ensuring that assets are distributed according to the owner’s wishes upon death.

- Contribution Information Form: This document details the contributions being made to the IRA, including the types of contributions (e.g., tax-deductible, non-deductible) and the tax years they apply to.

- Broker Dealer Information Sheet: This sheet collects details about the investment representative handling the IRA application. It includes broker dealer names, addresses, and contact information.

- Tax Reporting Information Form: This form outlines how contributions, distributions, and other transactions will be reported for tax purposes. It’s crucial for tax compliance and planning.

- Traditional/Roth IRA Disclosure Statement: This statement informs investors about the terms, conditions, and tax implications of both Traditional and Roth IRAs, helping them make informed investment decisions.

Each of these documents plays a vital role in ensuring that the IRA setup and management process is carried out smoothly and in compliance with federal regulations. Understanding the function of each document can help individuals effectively navigate their retirement investment journey.

Similar forms

- IRA Transfer Form: Similar to the Mf 10023 16 form, this document is used to move assets from one individual retirement account (IRA) to another. Like the Mf 10023 16, the IRA Transfer Form requires details on the account owner and the amounts being transferred, ensuring a smooth transition between accounts.

- Rollover IRA Application: Much like the Mf 10023 16, the Rollover IRA Application is designed for transferring funds from employer-sponsored retirement plans into an IRA. Both documents collect similar information regarding account numbers and asset amounts to facilitate proper rollover processing.

- SIMPLE IRA Adoption Agreement: This document is akin to the Mf 10023 16 form in that it establishes a specific type of IRA intended for small businesses. Each form requires various details about the account holder and contributions, ensuring compliance with tax regulations.

- SEP IRA Adoption Agreement: Similar to the Mf 10023 16, this agreement establishes a Simplified Employee Pension (SEP) IRA for self-employed individuals or small business owners. Both documents necessitate information on contributions and beneficiaries to comply with IRS guidelines.

- Beneficiary Designation Form: This form is comparable to the Mf 10023 16 as it allows account holders to specify beneficiaries for their retirement accounts. Both documents highlight the importance of properly identifying beneficiaries to secure financial benefits according to the account owner's wishes.

Dos and Don'ts

Things to Do When Filling Out the MF 10023 16 Form:

- Use CAPITAL LETTERS when printing your information to ensure clarity.

- Confirm that all necessary information is provided, including Social Security Numbers and dates.

- Attach a separate check for the annual maintenance fee, if applicable.

- Double-check the contribution amounts for accuracy before submission.

- Mail the completed form to the correct address provided in the instructions.

Things to Avoid When Filling Out the MF 10023 16 Form:

- Do not leave any required fields blank; incomplete forms may delay processing.

- Avoid using small or illegible handwriting to ensure your entries are readable.

- Do not submit multiple applications for the same account type; complete a separate application for each account type.

- Refrain from providing inaccurate or outdated personal information.

- Do not forget to review all sections before mailing the form to prevent mistakes.

Misconceptions

Misconceptions can lead to confusion and mistakes when filling out the MF 10023 16 form. Here are six common misconceptions, along with clarifications:

- All IRAs are the same. Many believe that all IRAs function the same way. However, the MF 10023 16 form is specifically for Traditional IRAs, Roth IRAs, Rollover IRAs, and does not cover SIMPLE or SEP IRAs.

- The contribution limits are the same for everyone. Contribution limits depend on factors such as age and filing status. For example, taxpayers under age 50 have a lower contribution limit compared to those aged 50 or older.

- You can contribute any amount you want each year. Each year has a maximum contribution limit, which must be adhered to. Exceeding this limit can result in penalties.

- You do not need to report any income to make contributions. To contribute to an IRA, you must have earned income, which includes wages and salaries. Simply having investment income does not qualify.

- Beneficiary designations are not important. Some individuals think it’s acceptable to leave this section blank. However, designating a beneficiary is crucial for ensuring your assets are distributed according to your wishes after your death.

- Your account is automatically managed once opened. Many assume that once the IRA is established, no further action is required. Active management and periodic review of investments are essential to ensure they align with financial goals.

Understanding these misconceptions can help make the process smoother and ensure compliance with regulations.

Key takeaways

Here are key takeaways for filling out and using the MF 10023 16 form:

- Before starting, ensure you are using the appropriate form for your IRA type – Traditional, Rollover, or Roth.

- Clearly indicate your fund selections; if no share class is specified, Class A will automatically be established.

- Include a separate check for the annual $15 IRA maintenance fee if not already covered by your total investment.

- Accurate personal information is crucial, including your full name, Social Security number, and residential address.

- The maximum contribution limit for IRAs is $3,000 for most individuals; those aged 50 and above can contribute $3,500.

- Choose the right type of account (e.g., Roth IRA, Traditional IRA) and document the tax year for your contributions.

- Be aware of the rights of accumulation, which can allow discounts on Class A shares based on previous investments.

- Make sure your beneficiary designations are clear and that they add up to 100% for proper allocation.

- Verify your completed application is sent to the correct address for processing, and keep a copy for your records.

Browse Other Templates

Nj Court Forms - This form enables you to file a cross-motion responding to an original motion.

Registrar Famu - Majors can impact future career opportunities, so students should choose carefully.