Fill Out Your Mw506Nrs Form

The Maryland MW506NRS form is an important document designed specifically for the sale of real estate by nonresidents of the state. If you're selling property in Maryland and are not a resident, it’s essential to understand how to properly complete this form to ensure compliance with local tax laws. This form provides essential information such as the description of the property being sold, the identification of the seller, and how to calculate the income tax withholding amount that must be submitted at the time of the sale. Each section of the form requires specific details, including the property address, transfer date, and pertinent financial aspects such as the total sales price and related debts. Additionally, if you’re reporting a gain under the installment method, there's a checkbox you should mark. It’s vital to complete each section accurately because multiple sellers will necessitate individual forms, especially when dealing with partnerships, corporations, or business trusts. This ensures that the correct income tax is withheld at closing and properly reported to the tax authorities, thus safeguarding you from potential penalties or complications in the future.

Mw506Nrs Example

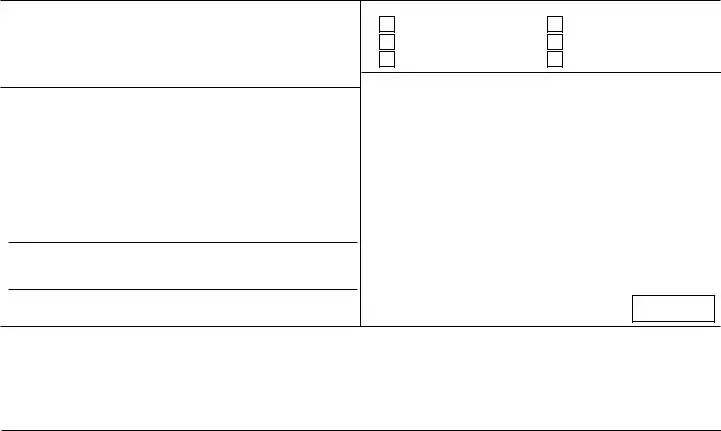

Form |

Maryland Return of Income Tax Withholding |

2022 |

MW506NRS |

for Nonresident Sale of Real Property |

|

CHECK OR MONEY ORDER AND FILE WITH THE CLERK OF THE CIRCUIT COURT •

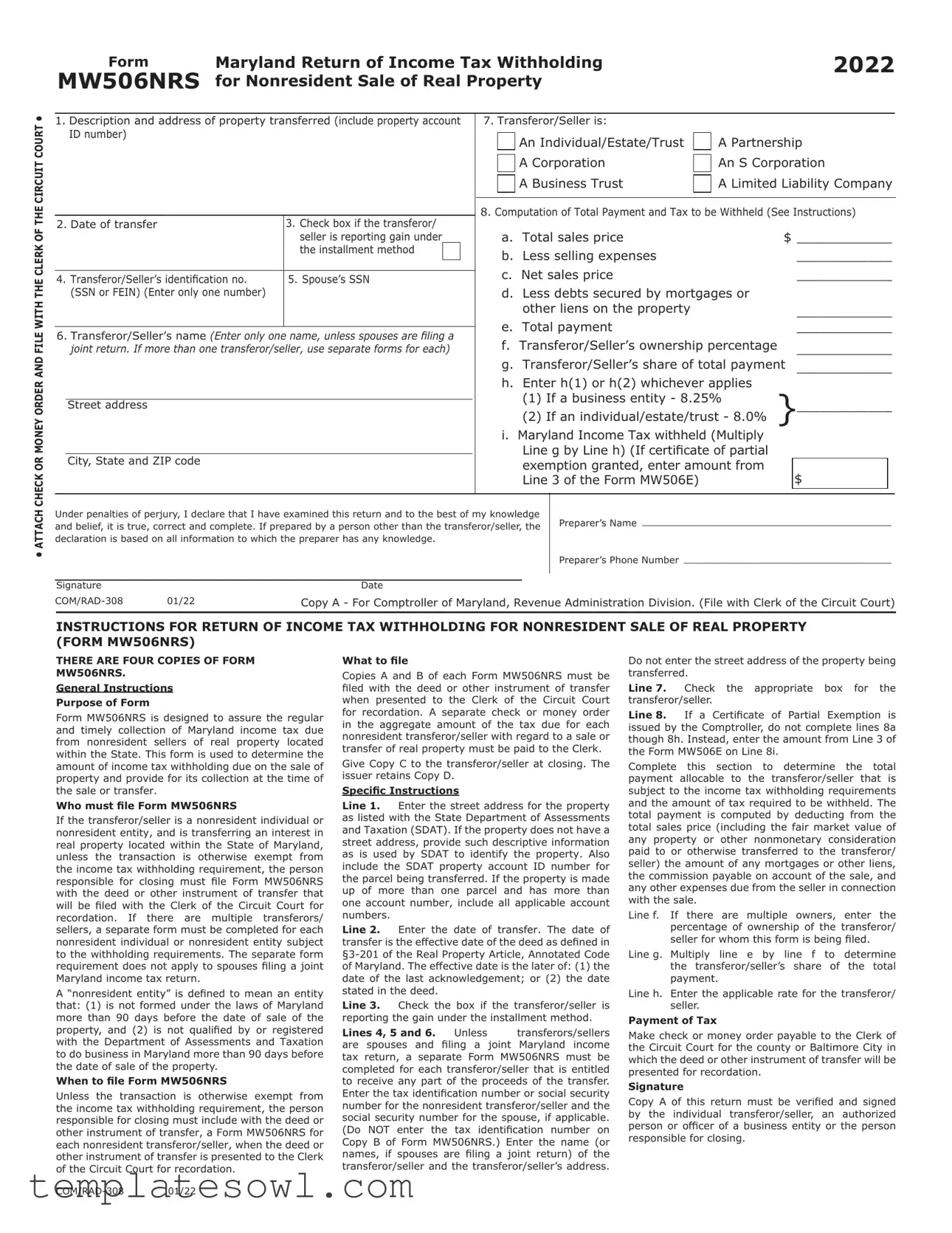

1.Description and address of property transferred (include property account ID number)

2. |

Date of transfer |

3. Check box if the transferor/ |

||

|

|

seller is reporting gain under |

||

|

|

the installment method |

|

|

|

|

|

|

|

4. |

Transferor/Seller’s identification no. |

5. Spouse’s SSN |

||

|

(SSN or FEIN) (Enter only one number) |

|

|

|

|

|

|

|

|

6.Transferor/Seller’s name (Enter only one name, unless spouses are filing a joint return. If more than one transferor/seller, use separate forms for each)

Street address

City, State and ZIP code

7. Transferor/Seller is: |

|

An Individual/Estate/Trust |

A Partnership |

A Corporation |

An S Corporation |

A Business Trust |

A Limited Liability Company |

8. Computation of Total Payment and Tax to be Withheld (See Instructions)

a. Total sales price |

$_____________ |

b. Less selling expenses |

_____________ |

c. Net sales price |

_____________ |

d. Less debts secured by mortgages or |

|

other liens on the property |

_____________ |

e. Total payment |

_____________ |

f. Transferor/Seller’s ownership percentage |

_____________ |

g.Transferor/Seller’s share of total payment _____________

h.Enter h(1) or h(2) whichever applies

(1)If a business entity - 8.25% }_____________

(2)If an individual/estate/trust - 8.0%

i.Maryland Income Tax withheld (Multiply

Line g by Line h) (If certificate of partial exemption granted, enter amount from

Line 3 of the Form MW506E) |

$ |

• ATTACH

Under penalties of perjury, I declare that I have examined this return and to the best of my knowledge |

Preparer’s Name_ __________________________________________ |

|

and belief, it is true, correct and complete. If prepared by a person other than the transferor/seller, the |

||

|

||

declaration is based on all information to which the preparer has any knowledge. |

|

|

|

Preparer’s Phone Number_ ___________________________________ |

Signature |

|

Date |

|

01/22 |

Copy A - For Comptroller of Maryland, Revenue Administration Division. (File with Clerk of the Circuit Court) |

||

|

|

|

|

INSTRUCTIONS FOR RETURN OF INCOME TAX WITHHOLDING FOR NONRESIDENT SALE OF REAL PROPERTY (FORM MW506NRS)

THERE ARE FOUR COPIES OF FORM

MW506NRS.

General Instructions

Purpose of Form

Form MW506NRS is designed to assure the regular and timely collection of Maryland income tax due from nonresident sellers of real property located within the State. This form is used to determine the amount of income tax withholding due on the sale of property and provide for its collection at the time of the sale or transfer.

Who must file Form MW506NRS

If the transferor/seller is a nonresident individual or nonresident entity, and is transferring an interest in real property located within the State of Maryland, unless the transaction is otherwise exempt from the income tax withholding requirement, the person responsible for closing must file Form MW506NRS with the deed or other instrument of transfer that will be filed with the Clerk of the Circuit Court for recordation. If there are multiple transferors/ sellers, a separate form must be completed for each nonresident individual or nonresident entity subject to the withholding requirements. The separate form requirement does not apply to spouses filing a joint Maryland income tax return.

A “nonresident entity” is defined to mean an entity that: (1) is not formed under the laws of Maryland more than 90 days before the date of sale of the property, and (2) is not qualified by or registered with the Department of Assessments and Taxation to do business in Maryland more than 90 days before the date of sale of the property.

When to file Form MW506NRS

Unless the transaction is otherwise exempt from the income tax withholding requirement, the person responsible for closing must include with the deed or other instrument of transfer, a Form MW506NRS for each nonresident transferor/seller, when the deed or other instrument of transfer is presented to the Clerk of the Circuit Court for recordation.

What to file

Copies A and B of each Form MW506NRS must be filed with the deed or other instrument of transfer when presented to the Clerk of the Circuit Court for recordation. A separate check or money order in the aggregate amount of the tax due for each nonresident transferor/seller with regard to a sale or transfer of real property must be paid to the Clerk.

Give Copy C to the transferor/seller at closing. The issuer retains Copy D.

Specific Instructions

Line 1. Enter the street address for the property as listed with the State Department of Assessments and Taxation (SDAT). If the property does not have a street address, provide such descriptive information as is used by SDAT to identify the property. Also include the SDAT property account ID number for the parcel being transferred. If the property is made up of more than one parcel and has more than one account number, include all applicable account numbers.

Line 2. Enter the date of transfer. The date of transfer is the effective date of the deed as defined in

Line 3. Check the box if the transferor/seller is reporting the gain under the installment method.

Lines 4, 5 and 6. |

Unless |

transferors/sellers |

are spouses and |

filing a joint |

Maryland income |

tax return, a separate Form MW506NRS must be completed for each transferor/seller that is entitled to receive any part of the proceeds of the transfer. Enter the tax identification number or social security number for the nonresident transferor/seller and the social security number for the spouse, if applicable. (Do NOT enter the tax identification number on Copy B of Form MW506NRS.) Enter the name (or names, if spouses are filing a joint return) of the transferor/seller and the transferor/seller’s address.

Do not enter the street address of the property being transferred.

Line 7. Check the appropriate box for the transferor/seller.

Line 8. If a Certificate of Partial Exemption is issued by the Comptroller, do not complete lines 8a though 8h. Instead, enter the amount from Line 3 of the Form MW506E on Line 8i.

Complete this section to determine the total payment allocable to the transferor/seller that is subject to the income tax withholding requirements and the amount of tax required to be withheld. The total payment is computed by deducting from the total sales price (including the fair market value of any property or other nonmonetary consideration paid to or otherwise transferred to the transferor/ seller) the amount of any mortgages or other liens, the commission payable on account of the sale, and any other expenses due from the seller in connection with the sale.

Line f. If there are multiple owners, enter the percentage of ownership of the transferor/ seller for whom this form is being filed.

Line g. Multiply line e by line f to determine the transferor/seller’s share of the total payment.

Line h. Enter the applicable rate for the transferor/ seller.

Payment of Tax

Make check or money order payable to the Clerk of the Circuit Court for the county or Baltimore City in which the deed or other instrument of transfer will be presented for recordation.

Signature

Copy A of this return must be verified and signed by the individual transferor/seller, an authorized person or officer of a business entity or the person responsible for closing.

Form |

Maryland Return of Income Tax Withholding |

2022 |

MW506NRS |

for Nonresident Sale of Real Property |

|

• ATTACH CHECK OR MONEY ORDER AND FILE WITH THE CLERK OF THE CIRCUIT COURT •

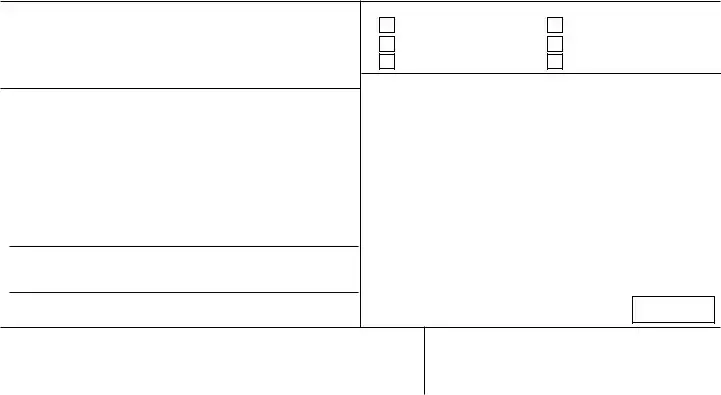

1.Description and address of property transferred (include property account ID number)

2. |

Date of transfer |

3. Check box if the transferor/ |

||

|

|

seller is reporting gain under |

||

|

|

the installment method |

|

|

|

|

|

|

|

4. |

Transferor/Seller’s identification no. |

5. Spouse’s SSN |

||

|

(SSN or FEIN) (Enter only one number) |

|

|

|

|

|

|

|

|

6.Transferor/Seller’s name (Enter only one name, unless spouses are filing a joint return. If more than one transferor/seller, use separate forms for each)

Street address

City, State and ZIP code + 4

7. Transferor/Seller is: |

|

An Individual/Estate/Trust |

A Partnership |

A Corporation |

An S Corporation |

A Business Trust |

A Limited Liability Company |

8. Computation of Total Payment and Tax to be Withheld (See Instructions)

a. Total sales price |

$_____________ |

b. Less selling expenses |

_____________ |

c. Net sales price |

_____________ |

d. Less debts secured by mortgages or |

|

other liens on the property |

_____________ |

e. Total payment |

_____________ |

f. Transferor/Seller’s ownership percentage |

_____________ |

g.Transferor/Seller’s share of total payment _____________

h.Enter h(1) or h(2) whichever applies

(1)If a business entity - 8.25% }_____________

(2)If an individual/estate/trust - 8.0%

i.Maryland Income Tax withheld (Multiply

Line g by Line h) (If certificate of partial exemption granted, enter amount from

Line 3 of the Form MW506E) |

$ |

01/22 |

Copy B - For Clerk of the Court |

INSTRUCTIONS FOR RETURN OF INCOME TAX WITHHOLDING FOR NONRESIDENT SALE OF REAL PROPERTY (FORM MW506NRS)

THERE ARE FOUR COPIES OF FORM

MW506NRS.

General Instructions

Purpose of Form

Form MW506NRS is designed to assure the regular and timely collection of Maryland income tax due from nonresident sellers of real property located within the State. This form is used to determine the amount of income tax withholding due on the sale of property and provide for its collection at the time of the sale or transfer.

What to file

A copy of each Copy A will be filed with Form MW508NRS on or before the 21st day of the month following the month in which the Form MW506NRS is filed with the Clerk of the Circuit Court. The Clerk of the Circuit Court shall remit the forms to the Comptroller of Maryland in accordance with the instructions for Form MW508NRS.

Form |

Maryland Return of Income Tax Withholding |

2022 |

MW506NRS |

for Nonresident Sale of Real Property |

|

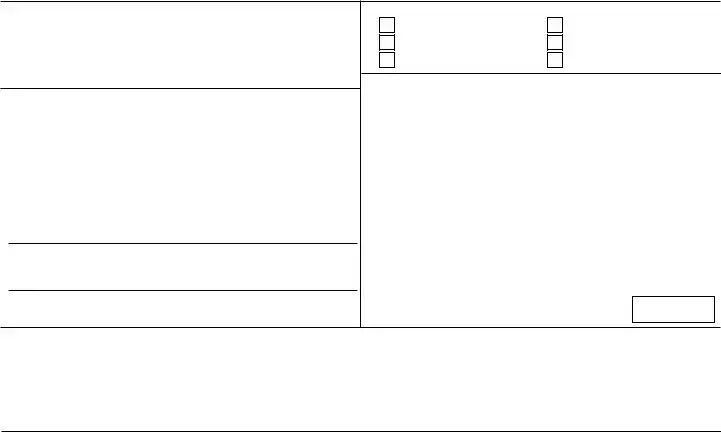

1.Description and address of property transferred (include property account ID number)

2. |

Date of transfer |

3. Check box if the transferor/ |

||

|

|

seller is reporting gain under |

||

|

|

the installment method |

|

|

|

|

|

|

|

4. |

Transferor/Seller’s identification no. |

5. Spouse’s SSN |

||

|

(SSN or FEIN) (Enter only one number) |

|

|

|

6.Transferor/Seller’s name (Enter only one name, unless spouses are filing a joint return. If more than one transferor/seller, use separate forms for each)

Street address

City, State and ZIP code + 4

7. Transferor/Seller is: |

|

An Individual/Estate/Trust |

A Partnership |

A Corporation |

An S Corporation |

A Business Trust |

A Limited Liability Company |

8. Computation of Total Payment and Tax to be Withheld (See Instructions)

a. Total sales price |

$_____________ |

b. Less selling expenses |

_____________ |

c. Net sales price |

_____________ |

d. Less debts secured by mortgages or |

|

other liens on the property |

_____________ |

e. Total payment |

_____________ |

f. Transferor/Seller’s ownership percentage |

_____________ |

g.Transferor/Seller’s share of total payment _____________

h.Enter h(1) or h(2) whichever applies

(1)If a business entity - 8.25% }_____________

(2)If an individual/estate/trust - 8.0%

i.Maryland Income Tax withheld (Multiply

Line g by Line h) (If certificate of partial exemption granted, enter amount from

Line 3 of the Form MW506E) |

$ |

Copy C - For Transferor/Seller (Records Copy).

INSTRUCTIONS FOR RETURN OF INCOME TAX WITHHOLDING FOR NONRESIDENT SALE OF REAL PROPERTY (FORM MW506NRS)

THERE ARE FOUR COPIES OF FORM MW506NRS.

General Instructions

Purpose of Form

Form MW506NRS is designed to assure the regular and timely collection of Maryland income tax due from nonresident sellers of real property located within the State. This form is used to determine the amount of income tax withholding due on the sale of property and provide for its collection at the time of the sale or transfer.

Who must file

A nonresident individual or nonresident entity that sells real property located in Maryland must file a Maryland income tax return. The appropriate income tax return must be filed for the year in which the transfer of the real property occurred. The due date for each income tax return type can be found in the instructions to the specific income tax return.

What to file

The nonresident individual or nonresident entity must file the appropriate Maryland income tax return for the year in which the transfer of the property occurred. Do NOT submit Copy C of the Form MW506NRS with the return filed with the Comptroller of Maryland. See the specific instructions for the tax return being filed.

Specific Instructions for Transferor/Seller

How to claim the tax withheld

The manner in which the income tax withheld is claimed by the nonresident individual or nonresident entity depends on the type of

Maryland income tax return you are required to file. Follow the specific instructions below. Claiming the income tax withheld on a line other than as described below may result in the withholding being denied.

Individuals and Revocable Living Trusts

Nonresident individuals are required to file a Nonresident Maryland Income Tax Return (Form 505). The income tax withheld and reported on Line 8 of the Form MW506NRS must be claimed as an estimated income tax payment.

C Corporations

C corporations are required to file a Maryland Corporation Income Tax Return (Form 500). The income tax withheld and reported on Line 8 of the Form MW506NRS must be claimed as an estimated income tax payment.

S Corporations, Partnerships and Limited Liability Companies and Business Trusts

S corporations, partnerships and limited liability companies and business trusts that elect to be treated as

This tax, and any other tax paid with the Form 510 must be allocated to the nonresident shareholders, partners or members and reported on a modified federal Schedule

Trusts and Estates

Trustees of trusts and personal representatives of estates are required to file a Maryland Fiduciary Income Tax Return (Form 504). The income tax withheld and reported on Line 8 of the Form MW506NRS must be claimed as an estimated tax payment.

Form |

Maryland Return of Income Tax Withholding |

2022 |

MW506NRS |

for Nonresident Sale of Real Property |

|

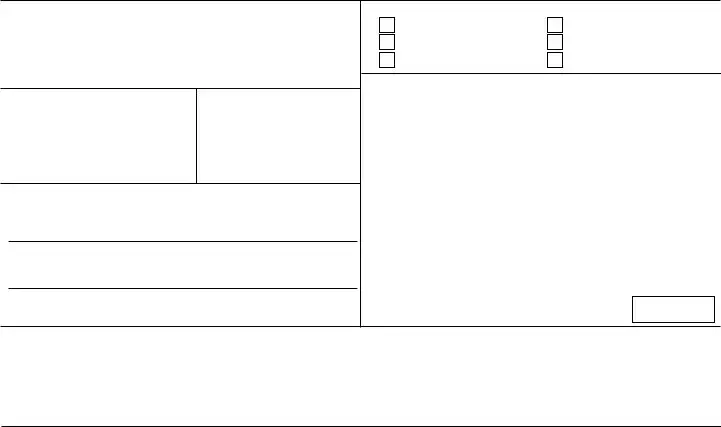

1.Description and address of property transferred (include property account ID number)

2. |

Date of transfer |

3. Check box if the transferor/ |

||

|

|

seller is reporting gain under |

||

|

|

the installment method |

|

|

|

|

|

|

|

4. |

Transferor/Seller’s identification no. |

5. Spouse’s SSN |

||

|

(SSN or FEIN) (Enter only one number) |

|

|

|

|

|

|

|

|

6.Transferor/Seller’s name (Enter only one name, unless spouses are filing a joint return. If more than one transferor/seller, use separate forms for each)

Street address

City, State and ZIP code + 4

7. Transferor/Seller is: |

|

An Individual/Estate/Trust |

A Partnership |

A Corporation |

An S Corporation |

A Business Trust |

A Limited Liability Company |

8. Computation of Total Payment and Tax to be Withheld (See Instructions)

a. Total sales price |

$_____________ |

b. Less selling expenses |

_____________ |

c. Net sales price |

_____________ |

d. Less debts secured by mortgages or |

|

other liens on the property |

_____________ |

e. Total payment |

_____________ |

f. Transferor/Seller’s ownership percentage |

_____________ |

g.Transferor/Seller’s share of total payment _____________

h.Enter h(1) or h(2) whichever applies

(1)If a business entity - 8.25% }_____________

(2)If an individual/estate/trust - 8.0%

i.Maryland Income Tax withheld (Multiply

Line g by Line h) (If certificate of partial exemption granted, enter amount from

Line 3 of the Form MW506E) |

$ |

Copy D - For Issuer

INSTRUCTIONS FOR RETURN OF INCOME TAX WITHHOLDING FOR NONRESIDENT SALE OF REAL PROPERTY (FORM MW506NRS)

THERE ARE FOUR COPIES OF FORM MW506NRS.

General Instructions

Purpose of Form

Form MW506NRS is designed to assure the regular and timely collection of Maryland income tax due from nonresident sellers of real property located within the State. This form is used to determine the amount of income tax withholding due on the sale of property and provide for its collection at the time of the sale or transfer.

Who must file Form MW506NRS

If the transferor/seller is a nonresident individual or entity, and is transferring an interest in real property located within the State of Maryland, unless the transaction is otherwise exempt from the income tax withholding requirement, the person responsible for closing must file Form MW506NRS with the deed or other instrument of transfer that will be filed with the Clerk of the Circuit Court for recordation. If there are multiple transferors/sellers, a separate form must be completed for each nonresident individual or nonresident entity subject to the withholding requirements. The separate form requirement does not apply to spouses filing a joint Maryland income tax return.

When to file Form MW506NRS

Unless the transaction is otherwise exempt from the income tax withholding requirement, the person responsible for closing must include with the deed or other instrument of transfer, a Form MW506NRS for each nonresident transferor/ seller, when the deed or other instrument of transfer is presented to the Clerk of the Circuit Court for recordation.

What to file

Copies A and B of each Form MW506NRS must

be filed with the deed or other instrument of transfer when presented to the Clerk of the Circuit Court for recordation. A separate check or money order in the aggregate amount of the tax due for each nonresident transferor/seller with regard to a sale or transfer of real property must be paid to the Clerk.

Give Copy C to the transferor/seller at closing. The issuer retains Copy D.

Specific Instructions

Line 1. Enter the street address for the property as listed with the State Department of Assessments and Taxation (SDAT). If the property does not have a street address, provide such descriptive information as is used by SDAT to identify the property. Also include the SDATproperty account ID number for the parcel being transferred. If the property is made up of more than one parcel and has more than one account number, include all applicable account numbers.

Line 2. Enter the date of transfer. The date of transfer is the effective date of the deed as defined in

Line 3. Check the box if the transferor/seller is reporting the gain under the installment method.

Lines 4, 5 and 6. Unless transferors/sellers are spouses and filing a joint Maryland income tax return, a separate Form MW506NRS must be completed for each transferor/seller that is entitled to receive any part of the proceeds of the transfer. Enter the tax identification number or social security number for the nonresident transferor/seller and the social security number for the spouse, if applicable. (Do NOT enter the

tax identification number on Copy B of Form MW506NRS.) Enter the name (or names, if spouses filing a joint return) of the transferor/ seller and the transferor/seller’s address. Do not enter the street address of the property being transferred.

Line 7. Check the appropriate box for the transferor/seller.

Line 8. If a Certificate of Partial Exemption is issued by the Comptroller, do not complete lines 8a though 8h. Instead, enter the amount from Line 3 of the Form MW506E on Line 8i.

Complete this section to determine the total payment allocable to the transferor/seller that is subject to the income tax withholding requirements and the amount of tax required to be withheld. The total payment is computed by deducting from the total sales price (including the fair market value of any property or other nonmonetary consideration paid to or otherwise transferred to the transferor/seller) the amount of any mortgages or other liens, the commission payable on account of the sale and any other expenses due from the seller in connection with the sale.

Line f. If there are multiple owners, enter the percentage of ownership of the transferor/ seller for whom this form is being filed.

Line g. Multiply line e by line f to determine the transferor/seller’s share of the total payment.

Line h. Enter the applicable rate for the transferor/seller.

Payment of Tax

Make check or money order payable to the Clerk of the Circuit Court for the county or Baltimore City in which the deed or other instrument of transfer will be presented for recordation.

Form Characteristics

| Fact Name | Description |

|---|---|

| Form Purpose | Form MW506NRS is used to collect Maryland income tax from nonresident sellers of real property, ensuring timely revenue collection. |

| Filing Requirement | A nonresident individual or entity must file this form when selling real estate in Maryland, unless exempt from withholding. |

| Copies | Four copies of Form MW506NRS are processed: Copy A is for the Comptroller, Copy B for the Clerk of the Court, Copy C for the seller, and Copy D for the issuer. |

| Governing Law | This form is governed by Maryland law, specifically under the Maryland Annotated Code, §3-201 of the Real Property Article. |

| Deadline for Filing | The form should be filed with the deed to the Clerk of the Circuit Court at the time of transfer to comply with withholding requirements. |

| Ownership Details | Transferors who are joint sellers must complete a separate form unless filing a joint return, ensuring accurate tax withholding. |

| Tax Calculation | Withholding tax is calculated based on the share of the total payment. If a business entity sells, 8.25% is withheld; for individuals or trusts, 8.0% is applicable. |

Guidelines on Utilizing Mw506Nrs

Completing the MW506NRS form is essential for nonresidents selling real property in Maryland. This form is crucial for calculating the appropriate amount of income tax that needs to be withheld from the sale. It is important to ensure accuracy, as various pieces of information must be filled in correctly. Below are the steps to properly complete this form.

- Property Description: Enter the street address of the property you are selling, including the property account ID number.

- Date of Transfer: Write the date when the property transfer occurs.

- Installment Method: Check the box if you, as the transferor or seller, are reporting gain under the installment method.

- Identification Number: Fill in the transferor/seller's identification number.

- Spouse's SSN: Enter the Social Security Number or FEIN for your spouse, but include only one number.

- Transferor/Seller's Name: Provide the full name of the transferor or seller, or both if filing jointly. Do not enter the property address again.

- Transferor/Seller Type: Indicate whether the transferor/seller is an individual, estate, trust, partnership, corporation, S corporation, business trust, or LLC.

- Total Payment Computation: Calculate the following:

- a. Total sales price

- b. Less selling expenses

- c. Net sales price

- d. Less debts secured by mortgages or other liens

- e. Total payment

- f. Transferor/seller's ownership percentage

- g. Transferor/seller's share of total payment

- h. Apply the correct tax rate: 8.25% for business entities or 8.0% for individuals/estates/trusts.

- i. Calculate Maryland Income Tax withheld by multiplying Line g by Line h.

- Declaration: The preparer must sign and date the return, affirming that the information provided is correct.

- Payment: Attach a check or money order for the total tax amount due, made payable to the Clerk of the Circuit Court.

After completing the form, ensure to file Copies A and B with the Clerk of the Circuit Court alongside the deed or other instrument of transfer. Keep Copy C for your records, and the issuer retains Copy D. Following these steps will facilitate a smooth transaction and compliance with Maryland tax regulations.

What You Should Know About This Form

1. What is the purpose of the MW506NRS form?

The MW506NRS form is designed to ensure the timely collection of Maryland income tax owed by nonresident sellers of real estate within the state. This form calculates the income tax withholding required on the sale of property and provides for its collection at the time of the transaction.

2. Who is required to file the MW506NRS form?

Any nonresident individual or nonresident entity selling real property located in Maryland must file the MW506NRS form unless the transaction qualifies for an exemption from income tax withholding requirements. The person responsible for closing the sale must submit this form along with the deed or other transfer instrument to the Clerk of the Circuit Court.

3. When must the MW506NRS form be filed?

The form must be filed at the time the deed or other instrument of transfer is presented to the Clerk of the Circuit Court for recordation. This requirement holds unless the transaction meets specific exemption criteria outlined in Maryland tax regulations.

4. How should the total payment and withheld tax be calculated on the MW506NRS form?

The total payment is calculated by taking the total sales price, subtracting selling expenses, and debts secured by mortgages or liens. The shares of each transferor/seller are then determined based on ownership percentages. The applicable tax rate, either 8.0% for individuals or 8.25% for entities, is applied to the transferor/seller's share to find the amount of Maryland income tax to be withheld.

5. What information is needed to complete the MW506NRS form?

To accurately fill out the form, the following information is required: description and address of the property (including account ID), date of transfer, identification numbers for the transferor/seller and spouse, ownership structure of the transferor/seller, and calculations relevant to the total sales price and taxes withheld. Separate forms are required for multiple sellers, unless they are spouses filing jointly.

6. What must be done after filing the MW506NRS form?

After filing the form, the person responsible for closing must ensure that Copies A and B are filed with the Clerk of the Circuit Court and pay the total amount of tax due with a separate check or money order. Copy C is provided to the transferor/seller at closing for their records, while Copy D is retained by the issuer.

7. How is the tax withheld claimed by the nonresident seller?

The method of claiming withheld income tax depends on the type of return the seller is required to file. Nonresident individuals must report the withheld tax as an estimated payment on Maryland Income Tax Return Form 505. Similar requirements apply for corporations and pass-through entities, which must carry over the withheld amounts to their respective tax returns.

8. What happens if a Certificate of Partial Exemption is issued?

If a Certificate of Partial Exemption is issued by the Maryland Comptroller, the seller should not complete lines calculating the total payment and tax to be withheld in the usual manner. Instead, the amount from Line 3 of Form MW506E should be entered directly on Line 8i of the MW506NRS.

9. Is it necessary to consult a tax professional when filling out the MW506NRS form?

While it is possible to complete the MW506NRS form on one's own, consulting a tax professional is advisable, especially for individuals unfamiliar with tax laws or those with complex situations. Professional guidance can help ensure compliance with tax regulations and accurate reporting, reducing the risk of errors or penalties.

Common mistakes

Filling out the MW506NRS form can be complex, and mistakes can lead to delays or issues with the filing process. One common mistake is not providing a complete description of the property being transferred. This section requires detailed information, including the street address and the property account ID number. Missing these details can cause the form to be rejected.

Another frequent error involves the date of transfer. It is crucial to enter the correct effective date as defined by the law. Many people mistakenly use the date of the sale agreement or another unrelated date, which can lead to complications in processing the form.

Checking the wrong box concerning installment sales is also a mistake. If the seller is reporting gain under the installment method, it is essential to check that box accurately. Not doing so may result in incorrect tax calculations and could lead to penalties later.

Additionally, individuals sometimes confuse the transferor/seller’s identification number and the spouse’s Social Security Number. Each number must be clearly labeled and entered correctly. Failure to do so can create unnecessary hurdles in tax calculations.

Another area where mistakes frequently occur is in calculating the ownership percentage. It’s essential to accurately represent each transferor/seller's share. This figure directly impacts the total payment and withholding tax, and inaccuracies could lead to improper tax filings.

When it comes to calculations, ensuring accuracy on total sales prices and related deductions is vital. Errors in these areas can lead to incorrect tax withheld amounts. Always double-check these computations to mitigate issues.

Finally, neglecting to sign the form or failing to include the necessary payment can halt the filing process entirely. Ensure that the form is signed by the authorized party and that the appropriate check or money order accompanies the submission.

Documents used along the form

The MW506NRS form is essential for nonresident sellers of real property in Maryland, as it ensures the timely collection of income tax withholding. Various other documents complement this form, each serving a unique role in the transaction process. Below is a list of forms and documents often used alongside the MW506NRS.

- Form MW506E: This form is a Certificate of Partial Exemption from the income tax withholding for eligible nonresident sellers. It allows sellers to apply for a reduced withholding based on specific exemptions.

- Form MW508NRS: This form reports the income tax withholding collected on sales of real property for nonresident sellers to the Maryland Comptroller. It must be filed by the Clerk of the Circuit Court following the completion of the MW506NRS form(s).

- Form 505: Nonresidents use this income tax return to report their overall income, including any tax withheld on real estate sales. It is crucial for claiming any withholdings as estimated tax payments.

- Form 500: C corporations completing the sale of real property need this form to report income and tax liabilities. They will claim any withheld amounts on this corporate income tax return.

- Form 510: This form is for pass-through entities, such as S corporations and partnerships. It ensures that the income tax withheld is appropriately allocated to nonresident shareholders, partners, or members.

- Form 504: Trusts and estates use this fiduciary income tax return to report income. They can also claim any tax withheld on real estate sales as an estimated payment using this form.

- Settlement Statement (HUD-1): This document details the financial aspects of the real estate transaction, including costs associated with the sale. It helps confirm the amounts reported on the MW506NRS form.

- Deed of Transfer: This official document records the transfer of property ownership. It must accompany the MW506NRS when filed with the Clerk of the Circuit Court.

- Closing Disclosure: This disclosure summarizes the mortgage terms, monthly payments, and closing costs. It is particularly useful for both buyers and sellers in understanding financial obligations.

- Tax Identification Documents: These documents include the tax identification numbers or Social Security numbers of the transferor or seller. They are necessary for accurately completing the MW506NRS form.

In summary, these forms and documents work together to facilitate the sale of real property while ensuring compliance with Maryland tax regulations. Each plays a critical role in reporting income, claiming withheld taxes, and providing the necessary information for a smooth transaction process.

Similar forms

Form 1099-S: This document reports proceeds from the sale or exchange of real estate. Similar to the MW506NRS, it captures essential transaction details such as the sales price and parties involved.

Form 5404: Used for reporting the sale of a principal residence and any capital gains, it functions similarly to the MW506NRS by determining tax obligations linked to property dispositions.

Form 8300: This form is intended for reporting cash payments over $10,000 received in a trade or business. It resembles the MW506NRS in that it tracks financial transactions that may have tax implications.

Form W-9: Primarily for providing a taxpayer's identification number to payers, it serves a purpose akin to the MW506NRS by facilitating appropriate tax reporting for payments made to individuals and entities.

Form 1040: The standard individual income tax return form where income details are consolidated, it parallels the MW506NRS as both forms deal with income generated through real estate transactions.

Form 1120-S: This form is for S corporations to report income, deductions, and tax credits, similar in purpose to the MW506NRS regarding tax implications from real estate sales.

Form 1041: Created for estates and trusts to report income, deductions, and tax obligations, this form aligns with the MW506NRS in capturing financial details related to property transfers from nonresidents.

Form MW508NRS: Specifically for Maryland income tax withholding for nonresidents, it directly relates to the MW506NRS as a complementary form that outlines additional withholding requirements in the state.

Dos and Don'ts

- Do ensure you have all necessary information before starting. Gather details like the property description, transfer date, and identification numbers.

- Don't skip the appropriate boxes. Always check if the transferor/seller reports gain under the installment method if applicable.

- Do fill out a separate form for each nonresident seller, unless spouses are filing jointly. Each scenario requires its own form for clarity.

- Don't forget to include the street address and property account ID number. This information is crucial for proper identification.

- Do verify your calculations. Make sure that the total payment and tax to be withheld are accurate, as errors can delay processing.

- Don't enter the tax identification number on Copy B of the form. This step is key to maintaining confidentiality.

- Do sign and date the form. Failure to do so may result in the form being rejected by the Clerk of the Circuit Court.

Misconceptions

Misconception 1: The MW506NRS form is only necessary for residents of Maryland.

This is incorrect. The MW506NRS form is specifically for nonresidents who are selling real property in Maryland. Regardless of where you live, if you’re selling property located in Maryland, you need to file this form.

Misconception 2: Only individual sellers need to file this form.

In reality, both nonresident individuals and nonresident entities must file the MW506NRS form. This includes partnerships, corporations, and other types of entities that sell real property in Maryland.

Misconception 3: You can combine multiple sellers on one MW506NRS form.

This is not true. Each nonresident seller must complete a separate MW506NRS form. The only exception is for spouses filing a joint return in Maryland.

Misconception 4: This form only collects tax on the sales price.

Actually, the MW506NRS form is used to calculate the income tax withholding based on the net sales price after deducting certain expenses like selling costs and debts secured by mortgages. It’s not just about the sales price.

Misconception 5: If I file the MW506NRS, I don’t have to worry about my Maryland income tax return.

That’s a common misunderstanding. Filing the MW506NRS does not replace the need to file your Maryland income tax return for nonresidents. You'll still need to handle your taxes according to the type of return you are required to file.

Misconception 6: I don’t need to worry about the MW506NRS if I receive a Certificate of Partial Exemption.

This isn’t entirely accurate. Even with a Certificate of Partial Exemption, you must still complete part of the MW506NRS form. Specifically, you would enter the amount from your exemption onto the appropriate line but must still file the form to adhere to regulations.

Key takeaways

- The MW506NRS form is necessary for nonresident sellers of real property in Maryland to report income tax withholding.

- Each nonresident individual or entity involved in the sale must complete a separate form.

- Ensure that the property description and address, along with the property account ID number, are accurately entered in Line 1.

- The date of transfer must be specified. This is defined as the effective date of the deed.

- If the transferor is using the installment method to report gain, be sure to check the appropriate box in Line 3.

- Only one transferor/seller's name should be entered unless spouses are filing jointly.

- Provide the identification numbers, such as Social Security Number or Federal Employer Identification Number, in Lines 4 and 5.

- Calculate the total payment and tax withholding carefully, following sections outlined in Line 8.

- A check or money order for the total tax amount must be filed alongside Copies A and B with the Clerk.

- Keep a copy of the completed MW506NRS for your records, especially Copy C, which is for the transferor/seller.

Browse Other Templates

Payvor - Keep a copy of this form for your records.

Michigan Special Mailer - The form facilitates direct communication regarding title issuance and ownership.

Property Management Inspection Checklist Template - Check outdoor areas, including lawns and patios, for maintenance status.