Fill Out Your Sls Form

The SLS form serves as a crucial communication tool for homeowners facing potential foreclosure. It emphasizes that this notice is issued by a debt collector and outlines the primary purpose of collecting relevant information to assist in debt recovery. To qualify for various loss mitigation programs, recipients are required to complete the enclosed Request for Mortgage Assistance (RMA) form and provide supporting documentation detailing their financial situation. Homeowners may authorize a third party to communicate on their behalf regarding their loan. The form also provides various methods through which documentation can be submitted, along with clear timelines and contact information for further assistance. Additionally, it details the types of alternative options available to avoid foreclosure, such as loan modifications or payment plans, and encourages proactive communication to explore these solutions. A checklist accompanies the form, ensuring that all required documentation is collected and submitted correctly, thus enhancing the chances of a positive outcome. The SLS form is both a starting point for negotiating financial relief and a guide for navigating the complexities of mortgage assistance programs.

Sls Example

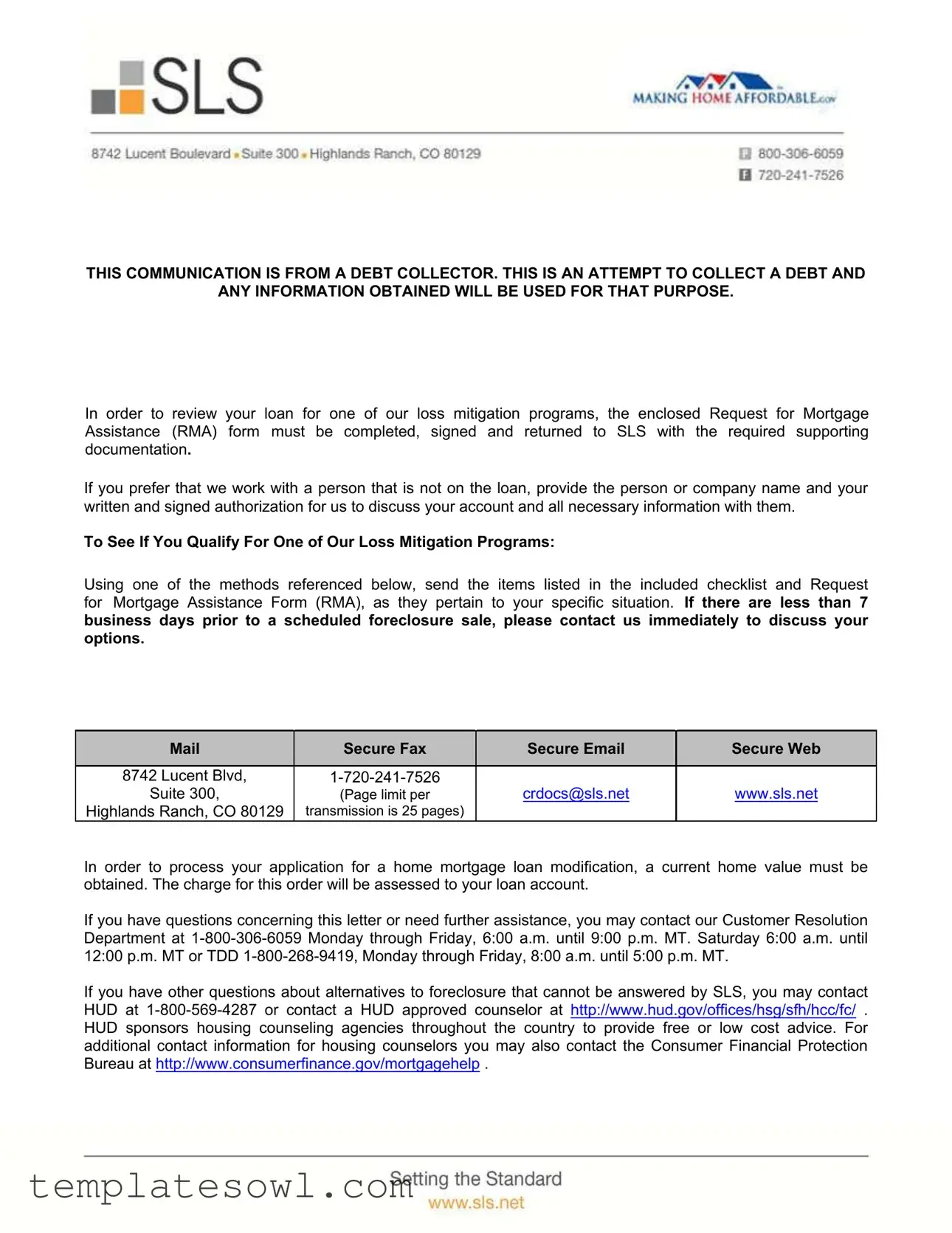

THIS COMMUNICATION IS FROM A DEBT COLLECTOR. THIS IS AN ATTEMPT TO COLLECT A DEBT AND

ANY INFORMATION OBTAINED WILL BE USED FOR THAT PURPOSE.

In order to review your loan for one of our loss mitigation programs, the enclosed Request for Mortgage Assistance (RMA) form must be completed, signed and returned to SLS with the required supporting documentation.

If you prefer that we work with a person that is not on the loan, provide the person or company name and your written and signed authorization for us to discuss your account and all necessary information with them.

To See If You Qualify For One of Our Loss Mitigation Programs:

Using one of the methods referenced below, send the items listed in the included checklist and Request for Mortgage Assistance Form (RMA), as they pertain to your specific situation. If there are less than 7 business days prior to a scheduled foreclosure sale, please contact us immediately to discuss your options.

Secure Fax |

Secure Email |

Secure Web |

|

|

|

|

|

8742 Lucent Blvd, |

|

|

|

Suite 300, |

(Page limit per |

crdocs@sls.net |

www.sls.net |

Highlands Ranch, CO 80129 |

transmission is 25 pages) |

|

|

In order to process your application for a home mortgage loan modification, a current home value must be obtained. The charge for this order will be assessed to your loan account.

If you have questions concerning this letter or need further assistance, you may contact our Customer Resolution Department at

If you have other questions about alternatives to foreclosure that cannot be answered by SLS, you may contact HUD at

Sincerely,

Customer Resolution Department

Specialized Loan Servicing LLC

Enclosures:

•Mortgage Assistance Application Checklist

•Information on Avoiding Foreclosure

•Frequently Asked Questions (FAQ)

•Request for Mortgage Assistance Form (RMA)

•IRS Form 4506T and IRS Form

•Index of Document Descriptions

SPECIALIZED LOAN SERVICING LLC IS REQUIRED BY LAW TO INFORM YOU THAT THIS COMMUNICATION IS FROM A DEBT COLLECTOR. HOWEVER, THE PURPOSE OF THIS COMMUNICATION IS TO OFFER YOU LOSS MITIGATION ASSISTANCE THAT MAY HELP YOU BRING OR KEEP YOUR LOAN CURRENT THROUGH AFFORDABLE PAYMENTS. IF YOU ARE CURRENTLY IN A BANKRUPTCY PROCEEDING, OR HAVE PREVIOUSLY OBTAINED A DISCHARGE OF THIS DEBT UNDER APPLICABLE BANKRUPTCY LAW, THIS NOTICE IS FOR INFORMATION ONLY AND IS NOT AN ATTEMPT TO COLLECT THE DEBT, A DEMAND FOR PAYMENT, OR AN ATTEMPT TO IMPOSE PERSONAL LIABILITY FOR THAT DEBT. YOU ARE NOT OBLIGATED TO DISCUSS YOUR HOME LOAN WITH US OR ENTER INTO A LOAN MODIFICATION OR OTHER

Mortgage Assistance Application Checklist

Get Started – Use this checklist to ensure you have completed all required forms and have the right information.

1Review the information provided to help you understand your options, responsibilities, and next steps:

Avoiding Foreclosure |

Frequently Asked |

Beware of Foreclosure |

|

Questions |

Rescue Scams (RMA) |

2Complete and sign the enclosed Request for Mortgage Assistance Form (RMA). Must be signed by all borrowers on the mortgage (notarization is not required) and must include:

An explanation of financial hardship that makes it difficult to pay the mortgage

Your preferred intent with the property (i.e. Retain the property, Sell the property or Deed the property back)

All income, expenses, and assets for each contributing borrower and

Your acknowledgment and agreement that all information that you provide is true and accurate

3Provide required Hardship Documentation. This documentation will be used to verify your hardship.

Write your loan number on all pages if it’s not already listed to aid in identifying your documents

Follow the instructions set forth on the RMA attached

4Provide required Income Documentation. This documentation will be used to verify your hardship and all of your income.

Write your loan number on all pages if it’s not already listed to aid in identifying your documents

Follow the instructions set forth on the RMA attached

Disclose any income from a household member who is not on the promissory note

•If you elect to disclose and rely upon this income to qualify, the required income documentation is the same as the income documentation required for a borrower in addition to the credit authorization form

•See the RMA for specific details on income documentation.

Proof of Income must be provided for all borrowers and

If noted as required for your income type, complete and sign a dated copy of the enclosed IRS Form

5Send your completed application package. Send in all required documentation listed in steps

Complete and Executed Request for Mortgage Assistance Form (RMA)

Hardship Documentation as outlined in the RMA

Income Documentation for each borrower and

|

|

Fax |

|

|

Web |

||

|

8742 Lucent Blvd, |

|

|

|

|

||

|

|

(Page limit per transmission |

|

|

|

|

|

|

Suite 300, |

|

|

crdocs@sls.net |

|

www.sls.net |

|

|

|

is 25 pages) |

|

|

|||

|

Highlands Ranch, CO 80129 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

IMPORTANT INFORMATION:

•If you cannot provide the documentation within the time frame provided, have other types of income not specified on the RMA, cannot locate some or all of the required documents, or If you have any questions regarding this information, please contact our Customer Resolution Department toll free at

•Don’t send original income or hardship documents. Copies are acceptable.

•Upon receipt of your complete application, SLS will utilize the intent you’ve noted in your RMA to determine which program we will evaluate you for first. However, SLS will perform an evaluation to determine your eligibility of all available programs offered by your investor. The results of our evaluation will be communicated to you in a decision letter.

•SLS encourages you to consider contacting other servicers of loans secured by the same property to discuss loss mitigation options.

This Document is for your reference only. Do not return with your application package.

Information on Avoiding Foreclosure

Mortgage Programs Are Available to Help

There are a variety of programs available to help you resolve your delinquency and keep your home. You may be eligible to refinance or modify your mortgage to make your payments and terms more manageable, for instance, lowering your monthly payment to make it more affordable. Or, if you have missed a few payments, you may qualify for a temporary (or permanent) solution to help you get your finances back on track. Depending on your circumstances, staying in your home may not be possible. However, a short sale or

|

|

OPTION |

|

|

OVERVIEW |

|

|

BENEFIT |

|

|

|

|

|

|

|

|

|

|

|

|

Reinstatement |

|

Pay the total amount you owe, in a lump sum |

|

Allows you to avoid foreclosure by bringing your |

||||

|

|

|

|

|

payment and by a specific date. This may follow a |

|

mortgage current if you can show you have funds |

||

|

|

|

|

|

forbearance plan as described below. |

|

that will become available at a specific date in the |

||

|

|

|

|

|

|

|

|

future. |

|

|

|

|

|

|

|

||||

|

Repayment Plan |

|

Pay back your |

|

Allows you time to catch up on late payments without |

||||

|

|

|

|

|

your regular payments over an extended period of |

|

having to come up with a lump sum. |

||

|

|

|

|

|

time. |

|

|

|

|

|

|

|

|

|

|

||||

|

Forbearance Plan |

|

Make reduced mortgage payments or no mortgage |

|

Have time to improve your financial situation and get |

||||

|

|

|

|

|

payments for a specific period of time. |

|

back on your feet. |

||

|

|

|

|

|

|

||||

|

Modification |

|

Receive modified terms of your mortgage to make |

|

Permanently modifies your mortgage so that your |

||||

|

|

|

|

|

it more affordable or manageable after successfully |

|

payments or terms are more manageable as a |

||

|

|

|

|

|

making the reduced payment during a “trial period” |

|

permanent solution to a |

||

|

|

|

|

|

(i.e., completing a three month trial period plan). |

|

hardship. |

||

|

|

|

|

|

|

||||

|

Short Sale |

|

Sell your home and pay off a portion of your |

|

Allows you to transition out of your home without |

||||

|

|

|

|

|

mortgage balance when you owe more on the |

|

going through foreclosure. In some cases, relocation |

||

|

|

|

|

|

home than it is worth. |

|

assistance may be available. |

||

|

|

|

|

|

|

||||

|

|

Transfer the ownership of your property to us. |

|

Allows you to transition out of your home without |

|||||

|

Foreclosure |

|

|

|

|

going through foreclosure. In some cases, relocation |

|||

|

|

|

|

|

|

|

|

assistance may be available. This is useful when |

|

|

|

|

|

|

|

|

|

there are no other liens on your property. |

|

|

|

|

|

|

|

|

|

|

|

This Document is for your reference only. Do not return with your application package.

Frequently Asked Questions

Q. Why Did I Receive This Package?

A. You received this package because we have not received one or more of your monthly mortgage payments and want to help find a foreclosure prevention option or you have requested information on obtaining assistance. We are sending this information to you now so that we can work with you to quickly resolve any temporary or

Q. Where Can I Find More Information on Foreclosure Prevention?

A. Please see the Avoiding Foreclosure attachment in this package for more information. If you have any questions regarding this information, please contact Customer Resolution toll free at

Q. Will It Cost Money to Get Help?

A. There should never be a fee from your servicer or qualified counselor to obtain assistance or information about foreclosure prevention options. However, foreclosure prevention has become a target for scam artists. Be wary of companies or individuals offering to help you for a fee, and never send a mortgage payment to any company other than the one listed on your monthly mortgage statement or one designated to receive your payments under a state assistance program.

Q. What Happens Once I Have Sent the Application Package to You?

A. We will contact you upon receipt of your Borrower Response Package to confirm that we have received your package and will review it to determine whether it is complete. Within five business days of receipt of your application documents, we will send you an acknowledgement letter outlining which documents are still need to complete or application or if we believe to have received a complete application and proceeding with the evaluation. We cannot guarantee that you will receive any (or a particular type of) assistance. We will let you know which foreclosure alternatives, if any, are available to you and will inform you of your next steps to accept our offer. Please submit your Application Package as soon as possible.

Q. What Happens to My Mortgage While You Are Evaluating My Application Package?

A. You remain obligated to make all mortgage payments as they come due, even while we are evaluating the types of assistance that may be available.

Q. Will the Foreclosure Process Begin If I Do Not Respond to this Letter?

A. If we do not receive an application within the timeline disclosed and you have missed four monthly payments or there is reason to believe the property is vacant or abandoned, we may refer your mortgage to foreclosure.

Q. What if My Property is scheduled for a Foreclosure Sale in the Future?

A.

oIf this is your first review or if you have had a qualifying change in circumstance and you submit a complete loss mitigation application and SLS has not made the first notice or filing required by applicable law for any judicial or

oIf this is your first review or if you have had a qualifying change in circumstance and you submit a complete loss mitigation application after a SLS has made the first notice or filing required by applicable law for any judicial or

oIf SLS has already moved for a foreclosure judgment or order of sale prior to receiving a completed application but more than 37 days before a foreclosure sale, SLS will take reasonable steps, such as requesting the court delay the consideration of the motion, to avoid a ruling on such a motion until SLS has completed the loss mitigation evaluation, however, there is no guarantee that we will be able to postpone a scheduled sale, because a court with jurisdiction over the foreclosure proceeding (if any) or public official charged with carrying out the sale may not agree to halt the scheduled sale

Q.Will My Property be Sold at a Foreclosure Sale If I Accept a Foreclosure Alternative?

A. No. If you are approved for a foreclosure prevention option and accept, any foreclosure sale will not occur if you continue

to honor the terms of the Agreement. However, if you fail to comply with the terms of the Agreement and do not make other arrangements with us, your loan will be enforced according to its original terms. This could include foreclosure. In addition, if you are currently in a bankruptcy proceeding, approval of any foreclosure prevention alternative for which you may be eligible is contingent on approval of the bankruptcy court in your bankruptcy case.

This Document is for your reference only. Do not return with your application package.

Frequently Asked Questions (Continued)

Q. Will My Credit Score Be Affected by My Late Payments or Being in Default?

A. The delinquency status of your loan will be reported to credit reporting agencies as well as your entry into a Repayment Plan, Forbearance Plan, or Trial Period Plan in accordance with the requirements of the Fair Credit Reporting Act and the Consumer Data Industry Association requirements.

Q. Will My Credit Score Be Affected if I Accept a Foreclosure Prevention Option?

A. While the impact on your credit will depend on your individual credit history, credit scoring companies generally would consider entering into a plan with reduced payments as increasing your credit risk. As a result, entering into a plan with reduced payments may adversely affect your credit score, particularly if you are current on your mortgage or otherwise have a good credit score.

Q. Is Foreclosure Prevention Counseling Available?

A. Yes,

Q. I Have Seen Ads and Flyers From Companies Offering to Help Me Avoid Foreclosure for a Fee. Are These Companies on the Level?

A. Foreclosure prevention has become a target for scam artists. We suggest using the HUD Web site referenced in question 12 to locate a counselor near you. Also, please refer to the attached “Beware of Foreclosure Rescue Scams” disclosure in your Request for Mortgage Assistance form (RMA) for more information.

This Document is for your reference only. Do not return with your application package.

Government Assistance May Be Available!

As part of the newly established Hardest Hit Fund SM, the U.S. Treasury Department has implemented programs which may help preserve homeownership for some United States homeowners. If you live in one of the following states you may be eligible for assistance:

State |

Agency Phone Number |

Agency Website |

Alabama |

(877) 497.8182 |

www.hardesthitalabama.com |

Arizona |

(877) 448.1211 |

www.savemyhomeaz.gov |

California |

(888) 954.5337 |

www.keepyourhomecalifornia.org |

District of Columbia |

(202) 777.1690 |

www.homesaverdc.org |

Florida |

(877) 863.5244 |

www.flhardesthithelp.org |

Georgia |

(888) 946.6723 |

www.homesafegeorgia.com |

Illinois |

(855) 873.7405 |

www.illinoishardesthit.com |

Indiana |

(877) 498.4673 |

www.877gethope.org |

Kentucky |

(800) 633.8896 |

www.protectmykyhome.org |

Michigan |

(866) 946.7432 |

www.stepforwardmichigan.org |

Mississippi |

N/A (Visit Website) |

www.mshomesaver.com |

North Carolina |

(888) 623.8631 |

www.ncforeclosureprevention.gov |

New Jersey |

N/A (Visit Website) |

www.njhomekeeper.gov |

Nevada |

(855) 428.4997 |

www.nevadahardesthitfunds.org |

Ohio |

(888) 404.4674 |

www.savethedream.ohio.gov |

Oregon |

(503) 986.2025 |

www.oregonhomeownerhelp.org |

Rhode Island |

(401) 277.1500 |

www.hhfri.org |

South Carolina |

N/A (Visit Website) |

www.scmortgagehelp.net |

Tennessee |

(855) 890.8073 |

www.keepmytnhome.org |

|

|

|

What Should You Do Now?

•Find out if you qualify for one of these programs by contacting your local Hardest Hit Fund Housing Agency

•Once you have established an action plan with a Hardest Hit Fund representative you should contact Specialized Loan Servicing LLC to reach a joint resolution.

Please be advised that all HHF contact information has been obtained directly from the HHF housing authority and may be subject to change based on state program updates

This is not an offer to extend credit. Program subject to conditions and eligibility requirements. Offer invalid if your loan is sold prior to satisfaction of the debt. Calls will be monitored and recorded for quality assurance purposes. If you do not wish for your call to be recorded, please notify the Customer Assistance Associate when calling.

If you have other questions about HAMP that cannot be answered by us, please call the Homeowner’s HOPE™ Hotline at 1-

You may have received documents from SLS concerning a home mortgage loan modification. The purpose of this solicitation is to offer you another option with respect to your loan, if you qualify; however it is not meant to take the place of the HAMP option, if applicable.

If you are experiencing a financial hardship and need help, you must complete and submit this form along with other required documentation to be considered |

|

for foreclosure prevention options under the Making Home Affordable (MHA) Program. You must provide information about yourself and your intentions to either |

|

keep or transition out of your property; a description of the hardship that prevents you from paying your mortgage(s); information about all of your income, expenses |

|

and financial |

assets; whether you have declared bankruptcy; and information about the mortgage(s) on your principal residence and other single family real estate that |

you own. When you sign and date this form, you will make important certifications, representations and agreements, including certifying that all of the information in |

|

this RMA is |

accurate and truthful. |

SLS Loan Number:

|

|

|

|

|

|

SECTION 1: BORROWER INFORMATION |

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

PRIMARY BORROWER |

|

|

|

|

|

|

|

|

|

|||||||||

|

BORROWER’S NAME |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

SOCIAL SECURITY NUMBER |

|

|

|

DATE OF BIRTH (MM/DD/YY) |

|

|

SOCIAL SECURITY NUMBER |

|

|

|

DATE OF BIRTH (MM/DD/YY) |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

HOME PHONE NUMBER WITH AREA CODE |

|

|

|

|

HOME PHONE NUMBER WITH AREA CODE |

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

CELL OR WORK NUMBER WITH AREA CODE |

|

|

|

|

CELL OR WORK NUMBER WITH AREA CODE |

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

MAILING ADDRESS |

|

|

|

|

|

|

|

|

MAILING ADDRESS (IF SAME AS BORROWER, WRITE “SAME”) |

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

EMAIL ADDRESS |

|

|

|

|

|

|

|

|

EMAIL ADDRESS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

BORROWER’S NAME |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

SOCIAL SECURITY NUMBER |

|

|

|

DATE OF BIRTH (MM/DD/YY) |

|

|

SOCIAL SECURITY NUMBER |

|

|

|

DATE OF BIRTH (MM/DD/YY) |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

HOME PHONE NUMBER WITH AREA CODE |

|

|

|

|

HOME PHONE NUMBER WITH AREA CODE |

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

CELL OR WORK NUMBER WITH AREA CODE |

|

|

|

|

CELL OR WORK NUMBER WITH AREA CODE |

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|||||||||||||

|

MAILING ADDRESS (IF SAME AS BORROWER, WRITE “SAME”) |

|

|

MAILING ADDRESS (IF SAME AS BORROWER, WRITE “SAME”) |

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

EMAIL ADDRESS |

|

|

|

|

|

|

|

|

EMAIL ADDRESS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

My intent with the property is: |

|

Keep the Property |

Sell the Property |

|

Deed the Property back |

I’m Unsure |

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||

|

NOTE: SLS will perform an evaluation to determine your eligibility for all available programs offered by your investor. |

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The property is currently: |

|

|

My Primary Residence |

|

|

A Second Home |

|

|

An Investment Property |

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

The property is currently: |

|

|

Owner Occupied |

|

|

|

Renter Occupied |

|

|

Vacant |

|

|

|

|

||||

|

Has any borrower filed for bankruptcy? |

|

Chapter 7 |

Chapter 13 |

|

Is any borrower a Service member? |

|

Yes |

No |

|

|

|

|||||||

|

Filing date: ___ /___ /___ |

Case Number: _______________ |

|

Have you recently been deployed away from your principal residence or |

|||||||||||||||

|

|

recently received a permanent change of station order? |

Yes |

No |

|||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

Is any borrower the surviving spouse of a deceased service member who was on |

||||||||||

|

Has your bankruptcy been discharged? |

|

Yes |

No |

|

|

active duty at the time of death? |

Yes |

|

|

No |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

Have you contacted a credit counseling agency for help? |

Yes |

No |

|

|

|

|

|

|

|

|

|

|||||||

|

Counselors Name:______________________________ |

Counselors Phone Number:___________/____________/_________________ |

|

|

|||||||||||||||

|

Agency’s Name:________________________________ |

Counselors Email Address:___________________________________________ |

|

|

|||||||||||||||

|

|

|

|

||||||||||||||||

|

Has the mortgage on your principal residence ever had a Home Affordable Modification Program (HAMP) trial period plan or other permanent |

|

|

||||||||||||||||

|

modification? |

Yes |

No |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

Has any property that you or any |

Yes |

No If “Yes”, how many? __________ |

|

|

||||||||||||||

|

|

|

|

||||||||||||||||

|

Are you or any |

|

|

||||||||||||||||

Yes

No

SECTION 2: HARDSHIP AFFIDAVIT

I am requesting review of my current financial situation to determine whether I qualify for temporary or permanent mortgage relief options.

Date Hardship Began is:_______________

I Believe my situation is:

___ Short Term (under 6 months) |

___ Medium term |

___Long Term/Permanent (Greater than 12 months) |

I (We) am/are requesting review under the Specialized Loan Servicing Loan Modification Program.

I am having difficulty making my monthly payment because of reason set forth below:

(Please check the primary reason and submit required documentation demonstrating your primary hardship)

|

If your hardship is: |

Then the required hardship documentation is: |

|

I am unemployed and (a) I am receiving/will receive unemployment |

No Hardship Documentation Required. |

|

benefits or (b) my unemployment benefits ended less than 6 months |

|

|

ago. |

|

|

Reduction in Income: a hardship that has caused a decrease in your |

No Hardship Documentation Required. |

|

income due to circumstances outside of your control (e.g., |

|

|

elimination of overtime, reduction in regular working hours, a |

|

|

reduction in base pay) |

|

|

Increase in Housing Expenses: a hardship that has caused an |

No Hardship Documentation Required. |

|

increase in your housing expenses due to circumstances outside of |

|

|

your control. |

|

|

Divorce or legal separation; Separation of Borrowers unrelated by |

Divorce Decree filed by the court; OR |

|

marriage, civil union or similar domestic partnership under |

Separation agreement filed by the court; OR |

|

applicable law. |

Current Credit Report evidencing divorce, separation, or |

|

|

borrower has a different address; OR |

|

|

Recorded quitclaim deed evidencing that the |

|

|

|

|

Death of a borrower or death of either the primary or secondary |

Death certificate; OR |

|

wage earner in the household |

Obituary or newspaper article reporting the death |

borrower or dependent family member |

Written statement or other documentation verifying disability or illness; |

|

OR |

|

Doctor’s certificate of illness or disability; OR |

|

Medical bills |

|

*None of the above shall require providing detailed medical information |

Disaster (natural or |

Insurance claim; OR |

Borrower’s place of employment |

Federal Emergency Management Agency grant or Small Business |

|

Administration loan; OR |

|

Borrower or Employer Property located in a federally declared disaster |

|

area |

Distant employment transfer/relocation |

For active duty service members: |

|

Notice of permanent change of station (PCS) or actual PCS orders. |

|

For employment transfers/new employment: |

|

Copy of signed offer letter or notice from employer showing transfer of |

|

new employment location; OR |

|

Pay stub from new employer; OR |

|

If none of these apply, provide written explanation |

|

In addition to the above, documentation that reflects the amount of any |

|

relocation assistance provided, if applicable (not required for those with PCS |

|

orders) |

Business Failure |

Tax return from the previous year (including all schedules) AND |

|

Proof of business failure supported by one of the following: |

|

Bankruptcy Filing for business; OR |

|

Two months of recent bank statements for the business account |

|

evidencing cessation of business activity; OR |

|

Most recent signed and dated quarterly or |

|

statement |

Other: a hardship not covered above |

Written explanation describing the details of the hardship and relevant |

|

documentation (below) |

Additional Explanation (continue on a separate sheet of paper if necessary): |

|

SECTION 3: COMBINED INCOME AND EXPENSES FOR BORROWER AND

*Details regarding the required supporting documentation can be found in Section 5

Only include income information for household contributing BORROWERS

If you include income from a contributor who is NOT a Borrower, specify their income in Section 4

You are not required to disclose Child Support, Alimony or Separation Maintenance income, unless you choose to have it considered.

Include mortgage payments on all properties you own EXCEPT your principal residence and the property you are seeking assistance in Section 7.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Borrower Name: ________________________ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Child |

|

|

Other (investment |

|

|

|

|

|

|

Monthly Gross Wages |

|

|

$ |

|

income, royalties, |

$ |

|

|

|

|

|

|

$ |

|

Support/Alimony/Separation |

|

|

|

|

||||

|

|

|

|

|

|

dividends, etc.) |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Overtime |

$ |

|

Social Security/SSDI |

$ |

|

Gross Rents Received |

$ |

|

|

|

|

|

|

(Taxable) |

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tips, commissions, |

$ |

|

Social Security/SSDI (Non- |

$ |

|

Other: |

$ |

|

|

|

|

|

bonus |

|

Taxable) |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

|

Public Assistance |

$ |

|

Other: |

$ |

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

Income |

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Unemployment |

|

|

Other monthly income: |

|

|

|

|

|

|

|

|

|

$ |

|

pension, annuity, retirement, |

$ |

|

Total (Gross Income) |

$ |

|

|

|

|

|

|

Income |

|

|

|

|

|

|||||

|

|

|

|

etc. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Monthly Gross |

$ |

|

Wages |

|

|

|

|

|

|

|

|

Overtime |

$ |

|

|

|

|

Tips, commissions, |

$ |

|

|

||

bonus |

|

|

|

|

|

$ |

|

|

|

||

Income |

|

|

|

|

|

Unemployment |

$ |

|

|

||

Income |

|

|

|

|

|

|

|

|

Child |

$ |

||

Support/Alimony/Separation |

|||

|

|||

Social Security/SSDI (Taxable) |

$ |

||

Social Security/SSDI (Non- |

$ |

||

Taxable) |

|||

|

|||

Public Assistance |

$ |

||

Other monthly income: |

|

|

|

|

|

||

pension, annuity, retirement, |

|

$ |

|

etc. |

|

|

|

|

|

|

|

|

Other (investment |

|

|

income, royalties, |

$ |

|

dividends, etc.) |

|

|

|

|

|

Gross Rents Received |

$ |

|

|

|

|

Other: |

$ |

|

|

|

|

Other: |

$ |

|

|

|

|

|

|

|

Total (Gross Income) |

$ |

|

|

|

Monthly Gross |

$ |

|

Wages |

|

|

|

|

|

|

|

|

Overtime |

$ |

|

|

||

|

|

|

Tips, commissions, |

$ |

|

|

||

bonus |

|

|

|

|

|

$ |

|

|

|

||

Income |

|

|

|

|

|

Unemployment |

$ |

|

|

||

Income |

|

|

|

|

|

|

|

|

Child |

$ |

||

Support/Alimony/Separation |

|||

|

|||

Social Security/SSDI (Taxable) |

$ |

||

Social Security/SSDI (Non- |

$ |

||

Taxable) |

|||

|

|||

Public Assistance |

$ |

||

Other monthly income: |

|

|

|

|

|

||

pension, annuity, retirement, |

|

$ |

|

etc. |

|

|

|

|

|

|

|

|

Other (investment |

|

|

income, royalties, |

$ |

|

dividends, etc.) |

|

|

|

|

|

Gross Rents Received |

$ |

|

|

|

|

Other: |

$ |

|

|

|

|

Other: |

$ |

|

|

|

|

|

|

|

Total (Gross Income) |

$ |

|

|

|

Monthly Gross |

$ |

|

Wages |

|

|

|

|

|

|

|

|

Overtime |

$ |

|

|

||

|

|

|

Tips, commissions, |

$ |

|

|

||

bonus |

|

|

|

|

|

$ |

|

|

|

||

Income |

|

|

|

|

|

Unemployment |

$ |

|

|

||

Income |

|

|

|

|

|

|

|

|

Child |

$ |

||

Support/Alimony/Separation |

|||

|

|||

Social Security/SSDI (Taxable) |

$ |

||

Social Security/SSDI (Non- |

$ |

||

Taxable) |

|||

|

|||

Public Assistance |

$ |

||

Other monthly income: |

|

|

|

|

|

||

pension, annuity, retirement, |

|

$ |

|

etc. |

|

|

|

|

|

|

|

|

|

Other (investment |

|

|

|

|

|

|

income, royalties, |

$ |

|

||

|

|

dividends, etc.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross Rents Received |

$ |

|

||

|

|

|

|

|

|

|

|

|

Other: |

$ |

|

||

|

|

|

|

|

|

|

|

|

Other: |

$ |

|

||

|

|

|

|

|

|

|

|

|

Total (Gross Income) |

|

|

$ |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

Form Characteristics

| Fact Name | Description |

|---|---|

| Purpose of Communication | This document serves as a notification from a debt collector. It is crucial as it aims to assist borrowers in addressing their mortgage debt through loss mitigation programs. Understanding this can help individuals navigate their options more effectively. |

| Required Documentation | To participate in the loss mitigation programs, borrowers must complete the Request for Mortgage Assistance (RMA) form. This form necessitates signatures from all borrowers and must be submitted along with additional supporting documentation. |

| Response Timeline | If a foreclosure sale is scheduled within seven business days, immediate contact with SLS is essential to discuss potential options. This urgency emphasizes the importance of timely action for those in financial distress. |

| Contact Information | Borrowers may reach out to the Customer Resolution Department at 1-800-306-6059 for assistance. This connection provides a critical resource for inquiries regarding the process and available options. |

| Governing Law | The activities surrounding this form are subject to federal laws such as the Fair Debt Collection Practices Act (FDCPA) and relevant state laws that govern mortgage servicing. These statutes aim to protect consumers while ensuring fair practices in the collection of debts. |

Guidelines on Utilizing Sls

The following steps outline how to fill out the SLS Request for Mortgage Assistance (RMA) form. Completing this process accurately will ensure your loan application is reviewed for potential loss mitigation programs. Follow each instruction carefully to ensure all required information is submitted.

- Gather necessary information before starting. You will need details about your financial situation, including income, expenses, and assets.

- Carefully read the included information to understand your options and responsibilities. Review the checklist in the Mortgage Assistance Application to cover all requirements.

- Fill out the Request for Mortgage Assistance (RMA) form. The form must be signed by all borrowers. Include:

- An explanation of your financial hardship.

- Your preferred outcome for the property, such as retaining or selling it.

- Income, expenses, and assets for all contributing borrowers and non-borrowers.

- Your acknowledgment that the information provided is accurate.

- Provide hardship documentation to verify your financial situation. Write your loan number on all pages to aid in identification.

- Submit income documentation for each borrower and non-borrower contributor. Include income from household members not on the promissory note if applicable.

- If required, complete and sign a dated IRS Form 4506T-EZ or 4506T.

- Compile your application package, including:

- Completed and signed RMA form.

- Hardship documentation.

- Income documentation for all borrowers and contributors.

- Send your completed application package via one of the designated methods:

- Mail: 8742 Lucent Blvd, Suite 300, Highlands Ranch, CO 80129

- Secure Fax: 1-720-241-7526 (page limit per transmission is 25 pages)

- Email: crdocs@sls.net

- Web: www.sls.net

After submitting your application, SLS will review the provided information and contact you to confirm receipt. It’s important to act promptly to avoid potential delays in applying for assistance. If you have any questions during this process, assistance is available through their Customer Resolution Department.

What You Should Know About This Form

What is the SLS form and why did I receive it?

The SLS form is a Request for Mortgage Assistance (RMA) form designed to help homeowners who may be struggling to make their mortgage payments. You received this package because there have been missed payments on your loan. SLS wants to assist you in exploring foreclosure prevention options and provide guidance based on your financial situation.

What steps do I need to take to complete the SLS form?

Start by carefully reviewing the materials included in the package. Complete the RMA form by providing details about your financial hardships, your intentions for the property, and necessary income and expense details. Don’t forget to gather supporting documentation, such as hardship evidence and income verification. It’s vital to send the completed package promptly to avoid any delays.

Will it cost me anything to get assistance?

No, you should not pay any fees to your servicer or to qualified counselors for assistance. Be cautious of scams where individuals may ask for payment in exchange for help with your mortgage issues. Always make payments directly to the servicer listed on your mortgage statements.

What happens after I submit my application package?

Upon receipt of your application, SLS will acknowledge it within five business days. They will inform you if any documentation is missing or if your application is complete. While a review is conducted, you will be informed of available foreclosure alternatives, though there’s no guarantee of specific assistance being granted.

Do I need to continue making mortgage payments while my application is being reviewed?

Yes, you are still responsible for making your mortgage payments on time, even if you have submitted an application for assistance. Failure to do so may have consequences, including further accrual of late fees or the potential for foreclosure.

What if I do not respond to the SLS letter?

If you do not submit your application within the timeline provided in the letter, SLS may refer your mortgage for foreclosure, especially if there are four missed payments or if they have reason to believe the property is vacant or abandoned. Prompt action is crucial to protect your home.

What if my property is scheduled for a foreclosure sale?

If you submit a complete application for loss mitigation before a foreclosure sale, and it is your first review or you have experienced a qualifying change in circumstances, SLS may halt foreclosure proceedings. However, if SLS has already filed for foreclosure before receiving your application, they will try to delay further actions but cannot guarantee it will be postponed.

Will accepting a foreclosure alternative stop the sale of my property?

If you are approved for a foreclosure prevention option and agree to its terms, no foreclosure sale will occur as long as you adhere to the agreement. If you do not comply with the terms after acceptance, you risk having your loan enforced under its original conditions, which may include foreclosure.

Who can I contact for more help regarding my options?

You can reach out to the Customer Resolution Department at SLS at 1-800-306-6059. They are available Monday through Friday from 6:00 a.m. to 9:00 p.m. MT, and Saturday from 6:00 a.m. to 12:00 p.m. MT. Alternatively, HUD-approved counseling services are available at no or low cost to help provide guidance on your situation.

Common mistakes

When filling out the SLS form, many individuals make mistakes that can delay or complicate their applications for mortgage assistance. Understanding these common pitfalls can make the process smoother and more effective, bringing you one step closer to obtaining the help you need.

One of the most frequent mistakes is failing to provide complete information. Each section of the Request for Mortgage Assistance (RMA) form requires specific details. Skipping any portion can lead to unnecessary delays. Be thorough. Double-check that all parts of the form are filled out and that every required document is included in your application package.

Another common error occurs when applicants do not adequately explain their financial hardship. It is crucial to clearly articulate the reasons behind your difficulties in making mortgage payments. Use specific examples relating to job loss, unexpected medical expenses, or other significant changes in your financial situation. A vague explanation may not convey the severity of your circumstances.

Many people also overlook the need to sign the form properly. Each borrower listed on the mortgage must sign the RMA. Failing to do so may result in your application being marked as incomplete. Make sure that everyone involved in the loan is aware of their responsibility to sign the form; this simple step can save you considerable time and effort down the road.

In addition, some applicants forget to submit supporting documentation. When you send in your application, remember that you need to attach all necessary hardship and income documentation. Not providing these documents can result in delays in processing your application or even lead to denial. It is best practice to keep a checklist of all required documents and verify that everything is included before sending.

Lastly, be cautious about relying on income from non-borrower contributors. If you choose to include this income, it is necessary to provide the appropriate documents, such as a credit authorization form. This oversight can create confusion and hamper your chances of qualifying for the assistance you seek.

By being aware of these common mistakes, you can improve your chances of successfully completing the SLS form. Approach this process with care and thoughtfulness, ensuring that all information is accurate and complete. Properly filling out this form is an essential step in seeking the help you need in challenging financial times.

Documents used along the form

The following is a list of forms and documents frequently associated with the SLS form, particularly in the context of loss mitigation. Each document plays a pivotal role in the process of seeking assistance or modifying mortgage terms. It is important for borrowers to be aware of these documents, as they may facilitate the resolution of their financial difficulties.

- Request for Mortgage Assistance Form (RMA): This essential form must be completed and returned to initiate evaluation for loss mitigation options. It requires a detailed explanation of the financial hardship faced by the borrower, as well as income and expense disclosures.

- Mortgage Assistance Application Checklist: This checklist serves as a guide to help borrowers ensure they have completed all necessary documents and gathered pertinent the information before submission. It outlines steps to avoid foreclosure and the required paperwork for a successful application.

- Income Documentation: This document is necessary to verify the borrower's financial situation. It should include recent pay stubs, tax returns, and any additional proof of income for household members, whether they are borrowers or non-borrower contributors.

- Hardship Documentation: This contains evidence supporting the claims of financial difficulty. Documentation might include medical bills, job loss letters, or any other relevant materials that illustrate the reasons for financial distress.

- IRS Form 4506T or 4506T-EZ: These forms allow SLS to obtain a copy of the borrower’s tax return from the IRS, helping verify claimed income. Completing these forms is vital for those who are self-employed or whose income documentation requires additional verification.

- Information on Avoiding Foreclosure: This document provides valuable insights into various programs and options available to help borrowers facing potential foreclosure. It outlines strategies that may assist in staying in the home or transitioning out with minimal impact.

Understanding these documents is crucial to navigating the loss mitigation process effectively. Proper completion and submission of all required materials can significantly increase the chances of obtaining a suitable resolution for financial hardships faced by borrowers.

Similar forms

The SLS form, primarily focused on assisting borrowers in distress, shares similarities with several other important documents in the realm of debt and mortgage assistance. Below are five such documents, each with a brief explanation of its relationship to the SLS form:

- Request for Mortgage Assistance (RMA) Form: This is directly referenced within the SLS form as it serves as the official application for loss mitigation options. Like the SLS form, it collects detailed financial information and documents the borrower's circumstances to facilitate assistance.

- Hardship Letter: A hardship letter outlines the specific financial difficulties that a borrower is facing. Similar to the information required in the SLS form, it communicates the reason for seeking assistance and supports the request for mortgage relief.

- Bankruptcy Petition: When a borrower files for bankruptcy, they may be shielded from foreclosure. Like the SLS form, which deals with financial hardships, a bankruptcy petition also serves as an official declaration of financial distress aimed at securing relief options.

- Loan Modification Agreement: Once a borrower qualifies for assistance, a Loan Modification Agreement formalizes the new terms for repayment. This document similarly focuses on revising existing loan conditions, paralleling the objectives outlined in the SLS form for resolution and support.

- IRS Form 4506T: This IRS form allows a lender to obtain tax return information, which is often necessary for evaluating a borrower's financial situation. Like the supporting documents required by the SLS form, it plays a critical role in providing the necessary financial background for effective decision-making regarding assistance programs.

Dos and Don'ts

When filling out the SLS form, there are certain important things to remember. Here’s a list of what you should and shouldn’t do:

- Do: Review all instructions carefully before starting. Make sure you understand what is required.

- Do: Sign the Request for Mortgage Assistance (RMA) form. All borrowers must sign it.

- Do: Provide accurate information about your financial situation. This includes income, expenses, and any financial hardship.

- Do: Submit copies of all necessary documentation. Keep the originals for your records.

- Do: Contact SLS if you have questions. They are available to help you.

- Don’t: Wait until the last minute. Submit your application as soon as possible to avoid complications.

- Don’t: Send original documents. Always provide copies of your hardship and income documentation.

- Don’t: Provide incomplete information. Ensure all sections of the form are filled out properly.

- Don’t: Disclose personal information to anyone who is not authorized to help with your case.

- Don’t: Ignore correspondence from SLS. Prompt responses are crucial to your application process.

Misconceptions

Understanding the SLS form can be challenging, leading to several misconceptions. Here are five common misunderstandings and explanations to clarify them.

- Misconception 1: The SLS form is just for people behind on payments.

- Misconception 2: Submitting the SLS form guarantees immediate loan modification.

- Misconception 3: You must provide original documents.

- Misconception 4: You can discuss your situation with SLS without completing the form.

- Misconception 5: If you ignore the SLS form, the foreclosure process will stop.

This is not entirely accurate. While the form is often sent to individuals who have missed mortgage payments, it is also applicable to those seeking assistance before falling behind. Early intervention can provide options to prevent delinquency.

Submitting the form does not ensure loan modification or other assistance. Each application is evaluated, and SLS will determine which options are available based on individual circumstances. Quick responses may influence outcomes, but there are no guarantees.

This is misleading. Copies of all required documentation are acceptable for submission. In fact, it is advised not to send original documents. This helps ensure that necessary paperwork is not lost.

While general inquiries can be made, specific loan assistance often requires the completion of the SLS form. Without it, SLS may not have sufficient information to provide tailored assistance.

This is a critical misunderstanding. Ignoring the form or the communication can lead to escalating foreclosure proceedings. Responding promptly can help keep options open and enable negotiations to prevent foreclosure.

Key takeaways

When filling out and using the SLS form for mortgage assistance, it's crucial to keep several key points in mind:

- Complete the Request for Mortgage Assistance (RMA) form: Ensure all sections are filled out accurately. Each borrower must sign the form, which doesn't require notarization. A clear explanation of your financial hardship, income, and expenses is essential.

- Provide necessary documentation: Include all required hardship and income documents. These documents should be copies, not originals. Writing your loan number on each page helps in identifying your submission.

- Use the correct submission method: You can send your application via mail, secure fax, secure email, or secure web upload. If using email, be aware of the page limit per transmission.

- Act promptly: If you are close to a scheduled foreclosure sale, it's important to reach out immediately. Timely communication can help explore your options and prevent escalation of the situation.

Following these steps carefully can make a significant difference in your mortgage assistance application process.

Browse Other Templates

How to Make an Ig Complaint Army - The form aids in documenting and addressing concerns about deficiencies within the Army.

Bank Signature Cards - Each signer's manual or facsimile signature must be provided.