Fill Out Your Ga St 3 Tax Form

The GA ST-3 Tax form serves a crucial role for businesses and individuals in Georgia who engage in taxable sales and use transactions. This form is specifically designed for reporting sales and use tax activities for the specified reporting period, which in this case is only applicable for sales made during March 2017. The deadline for submission is April 20, 2017. Taxpayers are required to input their Sales and Use Tax Number, along with their identification details, in the designated fields. It's essential for those operating within the City of Atlanta to accurately report their sales data in Part B, particularly lines 3 through 5. A significant aspect of the form involves correctly sourcing sales—meaning determining the jurisdiction in which a sale has occurred. Generally, this includes all sales of goods where the property is delivered within the county or for services performed in that jurisdiction. This sourcing is governed by Georgia state law and also includes specific exemptions for certain categories of sales. For convenience, the form provides options for electronic filing through the Georgia Tax Center, where users can find additional resources, including instructional videos and FAQs. The ST-3 form is divided into multiple sections, covering aspects such as tax summaries, sales distribution, use tax, and vendor compensation calculations, making it comprehensive in handling the complexities associated with sales and use tax reporting.

Ga St 3 Tax Example

Sales and Use Tax Return

**ATTENTION**

Effective date: This Form

Sourcing: Generally, sales sourced to a jurisdiction include all sales of property in which the property is delivered to the purchaser in the jurisdiction and sales of services that are performed in the jurisdiction. Please refer to O.C.G.A. §

Electronic filing: To file and pay electronically, please visit the Georgia Tax Center at https://gtc.dor.ga.gov. Additional information, instructional videos, and frequently asked questions about electronic filing can be found at

General Instructions:

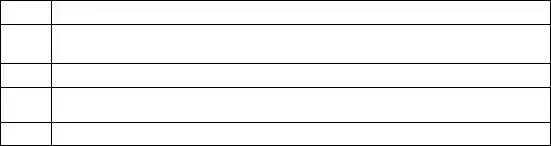

Record the Sales and Use Tax Number (STN), name, and address of the registered taxpayer. The Period Ending should be the end date (mm/dd/yy) of the reporting period. Check the Amended Return box if you are amending a previously filed return for the same period. Check the No Tax Due box if there were no taxable sales during this period. If there has been no sales and use tax activity during the period, do not complete this form. Please check the No Sales/Use Tax Activity box on Page 5, and complete and submit the payment voucher (Form

Part A - Tax Summary

LINE

1Record Total State Sales (all sales sourced to the State of Georgia) including leases and rentals.

2Record Total Exempt State Sales including leases and rentals. Include all sales that are exempt from state sales tax, even if such sales are subject to local sales tax.

3Subtract Exempt State Sales (Line 2) from Total State Sales (Line 1) and record Taxable State Sales. Complete Part B and Part C.

4Record the Total SALES Tax Amount (from Part B, Line 21).

5Record the Total USE Tax Amount (from Part B, Line 26).

6Record the TSPLOST tax (from Part C, Line 50).

7Record the

8Record Total Sales/Use Tax Collected for reporting period from taxpayer accounting records.

9Record the sum of Lines 4 – 7. (Add Line 4 + Line 5 + Line 6 + Line 7)

10Subtract Total Sales/Use Tax amount (Line 9) from Total Tax Collected (Line 8) amount and record the Excess Tax amount. Include the Excess tax amount in the appropriate sales/use category for vendor’s compensation.

11Record the Total Vendor’s Compensation (from Part D, Line 5).

12Record previous prepaid estimated tax, if applicable. Please reference your annual prepaid estimated tax letter.

13Record current prepaid estimated tax if applicable. Please reference your annual

Page 2

prepaid estimated tax letter.

14Add Lines 9 and 10, subtract Lines 11 and 12, and add Line 13 for the Total Amount Due.

Part B - Sales Tax Distribution Table

Do not report Transportation Local Option (TSPLOST) sales and use tax in Part B. Transportation Local Option (TSPLOST) sales and use tax will be reported in Part C.

LINE

1Record the Taxable State Sales (total sales sourced to the State of Georgia LESS sales of energy to manufacturers and all other tax exempt sales). Multiply this amount by the rate indicated on the Part B Sales Tax Distribution Table and record the Sales Tax Amount for the State.

2Record ONLY total sales sourced to the State of Georgia of energy sold to manufacturers. Multiply this amount by the rate indicated on the Part B Sales Tax Distribution Table and record the Sales Tax Amount.

3Record taxable

4Record ONLY sales of motor vehicles subject to sales tax and sourced to the City of Atlanta. These sales are also required to be included in county sales below (044 Dekalb County and/or 060 Fulton County). Multiply this amount by the rate indicated on the Part B Sales Tax Distribution Table and record the Sales Tax Amount.

5Record ONLY Taxable Sales of energy sold to manufacturers that are sourced to the City of Atlanta. These sales are also required to be included in county sales of energy to manufacturers below (044E Dekalb County and/or 060E Fulton County). Multiply this amount by the rate indicated on the Part B Sales Tax Distribution Table and record the Sales Tax Amount.

6Record Taxable Sales for Clayton County (Total sales sourced to Clayton County LESS sales of jet fuel, sales of motor vehicles subject to sales tax, sales of energy to manufacturers, and all other tax exempt sales). Multiply this amount by the rate indicated on the Part B Sales Tax Distribution Table and record the Sales Tax Amount.

7Record ONLY Taxable Sales of jet fuel sourced to Clayton County. Multiply this amount by the rate indicated on the Part B Sales Tax Distribution Table and record Sales Tax Amount.

8Record ONLY sales of motor vehicles subject to sales tax and sourced to Clayton County. Multiply this amount by the rate indicated on the Part B Sales Tax Distribution Table and record Sales Tax Amount.

9Record ONLY Taxable Sales of energy sold to manufacturers in Clayton County. Multiply this amount by the rate indicated on the Part B Sales Tax Distribution Table and record the Sales Tax Amount.

10Record Taxable Sales for Muscogee County (total sales sourced to Muscogee County LESS sales of motor vehicles subject to sales tax, sales of energy to manufacturers, and all other tax exempt sales). Multiply this amount by the rate indicated on the Part B Sales Tax Distribution Table and record the Sales Tax Amount.

Page 3

11Record ONLY sales of motor vehicles subject to sales tax and sourced to Muscogee County. Multiply this amount by the rate indicated on the Part B Sales Tax Distribution Table and record Sales Tax Amount.

12Record ONLY Taxable Sales of energy sold to manufacturers that are sourced to

Muscogee County. Multiply this amount by the rate indicated on the Part B Sales Tax Distribution Table and record the Sales Tax Amount.

Example: Taxpayer has $50,000 in total taxable sales for Cobb County which includes $10,000 in energy sold to a manufacturer. On Line 13 (or next available Line item in Part B or related addendum) list Cobb County (jurisdiction code 033), record $40,000 in total sales to Cobb County ($50,000 less $10,000 energy sales to a manufacturer), multiply this amount by the applicable tax rate for Cobb County and record the Sales Tax Amount. On Line 14 (or next available line) list Cobb County (jurisdiction code 033E), record total sales of energy to manufacturers of $10,000, multiply this amount by the applicable tax rate for Cobb County (for energy sold to manufacturers), and record the Sales Tax Amount.

Line |

Jurisdiction |

Jurisdiction |

Taxable |

Tax |

Sales Tax Amount |

|

|

Code |

Sales |

Rate |

|

13. |

Cobb |

033 |

40,000 |

2% |

800 |

|

|

|

|

|

|

14. |

Cobb |

033E |

10,000 |

1.00% |

100 |

|

|

|

|

|

|

Additional addendum pages (Form

20If additional addendum pages were completed, record the total Sales Tax Amount from all forms.

21Record the sum of Lines

Part B – Use Tax Distribution Table

LINE

Page 4

Code Reason

01Georgia Use – item purchased

02 |

Georgia Withdrawal from Inventory. |

03

04 |

Examples of taxable transactions, Jurisdiction of Use, and Reason Codes include:

A contractor purchases an item for $600.00 in a Georgia county where the total Sales Tax rate is 6% and uses the item to fulfill a contract in a jurisdiction where the total sales tax rate is 8%. The contractor owes additional Use Tax of 2% and should record local use tax due of $12.00 ($600.00 x .02). The Use tax Reason Code is 01.

A Georgia furniture manufacturer withdraws a table worth $700.00 from inventory to use in the business’s break room. The manufacturer owes state and local use tax based on the fair market value of the table, at the rate in effect in the jurisdiction where the withdrawal from inventory occurs. The manufacturer should calculate the use tax due by multiplying the combined state and local use tax rate by $700.00 and recording the resulting use tax. The use tax Reason Code is 02.

A Georgia resident or Georgia business purchases an item for $800.00 via the internet or by catalog, and the seller does not charge Sales Tax. The purchaser owes Use Tax based on the rate in effect in the jurisdiction where the purchaser takes possession of the item. The purchaser should calculate State Use Tax by multiplying the applicable State Use Tax rate by $800, and recording the resulting State Use Tax due with the use tax Reason Code 03. The purchaser should calculate the Local Use Tax due by multiplying the applicable Local Use Tax rate by $800.00 and recording the resulting Local Use Tax due with the Use Tax Reason Code 04.

A Georgia resident or Georgia business purchases a $900.00 item outside of Georgia, pays the other state’s 5% state sales tax at the time of purchase and returns to Georgia with the item. The purchaser will receive credit against Georgia’s 4% state use tax due and thus owes no additional state use tax. The purchaser owes local use tax at the rate in effect in the jurisdiction where the purchaser lives or where the business is located. The purchaser should calculate the local use tax due by multiplying the applicable local use tax rate by $900.00 and recording the resulting local use tax due. The Use tax Reason Code is 04.

Additional addendum pages, (Form

25Record the Addendum Page Total.

26Record the sum of Lines

Page 5

Part C – TSPLOST Sales & Use Tax

LINE

47

48

TSPLOST Sales and Use Tax – This section should ONLY be completed by individuals or businesses who have taxable sales sourced to or owe use tax to the jurisdictions listed in Part C (TSPLOST Sales & Use Tax).

Column A: TSPLOST Taxable Sales - Record Taxable Sales by county (Total County Sales LESS sales of energy to manufacturers and all other tax exempt sales).

Record the sum of taxable sales Lines

Column B: TSPLOST Use Tax - Record TSPLOST use tax amount due. Use tax is due if applicable TSPLOST Sales Tax was not paid on an item purchased or leased and that item has been placed into “use” within one of the listed jurisdictions.

49Record the sum of use tax Lines

50Record the sum of Lines 48 through 49 as total TSPLOST and record this amount on Part A, Line 6.

Part D – Vendor’s Compensation Calculation

LINE

1Record Total Sales and Use Tax on

.03) Vendor’s Compensation and record result.

2Record Total Sales and Use Tax on

3Record

4

5

Record State and Local Sales/Use Tax due on

Total above Vendor’s Compensation amounts for Total Vendor’s Compensation and record this amount on Part A, Line 11.

Part E – Bad Debt Reporting

LINE

1Record bad debt losses incurred on taxable Georgia sales.

2Record recoveries on Georgia bad debt that were previously written off.

Page 6

Part F – Certification and Signature

The return must be completed and signed in order to be considered timely filed.

Additional Instructions

Amended Returns

An amended return must be submitted on an

Master Accounts

Any dealer with four or more locations is required to report on a consolidated Sales and Use Tax form

Penalty and Interest on Delinquent Returns

Returns and payments are considered timely if postmarked by the due date of the return (the 20th day following the close of the reporting period). Taxpayers will be billed penalty and interest for all returns and payments filed after this date.

Penalty is calculated separately for the state and all local taxes in aggregate. A penalty of 5% (.05) of the tax due or five dollars ($5.00), whichever is greater, for the state and for the local taxes will be billed after the return is processed. This penalty will be billed for each month, or fraction of a month, when the return is delinquent. The penalty amount will be 25% (.25) or

For all periods beginning before July 1, 2016, interest is computed at 1% per month. For periods beginning on or after July 1, 2016, the annual interest rate will be the bank prime loan rate published on or after January 1 of each calendar year plus 3%. Interest will accrue on the tax amount owed from the date of the tax is due until the rate is paid.

Vendor’s Compensation is only given when both the payment and return are submitted timely. Taxpayers who are mandated to file electronically will not receive vendor’s compensation if a paper return and/or payment is submitted.

Mailing Instructions

Mail the return to the following address:

State of Georgia, Department of Revenue

PO BOX 105408

Atlanta, GA

Additional forms and information may be obtained from: Department of Revenue website/Forms, http://dor.georgia.gov

If you need additional assistance, please contact Taxpayer Service at

Print Blank Form |

|

|

|

|

|

|

|

|

Form

Georgia Department of Revenue

Sales and Use Tax Return

PO Box 105408

Atlanta, Georgia

Sales & Use #

-

-

/

/

Name:

Address:

Address:

City:State: Zip:

County of Business:

Clear

Page 1

Check/Money Order

No Sales/Use Activity

No Tax Due

/ |

|

Amended Return |

DEPARTMENT USE ONLY

Part A Tax Summary

1. Total State Sales |

|

|

|

|

|

||

2. Total Exempt State Sales |

|

||

|

|||

3. Taxable State Sales |

|

|

|

4. |

Total Sales Tax (from Part B, Line 21) |

+ |

|

5. |

Total Use Tax (from Part B, Line 26) |

+ |

|

6. |

Total TSPLOST Tax (from Part C, Line 50) |

+ |

|

7. |

+ |

|

|

8. |

Total Tax Collected (from accounting records) |

|

|

|

|

||

9. |

Total Sales/Use Tax (Ln 4 + Ln 5+ Ln 6 + Ln 7) |

|

|

10. |

Excess Tax (Subtract Line 9 from Line 8) |

+ |

|

11. |

Total Vendor’s Compensation (from Part D, Line 5) |

- |

|

12. |

Previous Prepaid Amount |

- |

|

13. |

Current Prepaid Amount |

+ |

|

14. Total Amount Due..................................................................................................................................

Print Blank Form

Form

Georgia Department of Revenue

Sales and Use Tax Return

PO Box 105408

Atlanta, Georgia

Clear

Page 2

|

Part B Sales Tax Distribution Table |

|

PERIOD ENDING |

|

|

|

/ |

|

|

|

|

/ |

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

JURISDICTION |

TAXABLE SALES |

|

TAX RATE |

SALES TAX AMOUNT |

|

|||||||||||||||

1. |

|

|

|

|

|

CODE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

State |

|

000 |

|

|

|

|

|

|

4% |

|

|

|

|

|

|

|

|

|

|

|

||||||

|

2. State (Energy to Manufacturers) |

|

|

000E |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

0% |

|

|

|

|

|

|

|

|

|

|

|

||||||||

3. |

|

City of Atlanta |

|

999 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

1.5% |

|

|

|

|

|

|

|

|

|

|

|

||||||||

4. |

|

City of Atlanta (Motor Vehicle) |

|

|

999R |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

0.5% |

|

|

|

|

|

|

|

|

|

|

|

||||||||

5. |

City of Atlanta (Energy to Manufacturers) |

|

999E |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

0% |

|

|

|

|

|

|

|

|

|

|

|

||||||||||

6. |

Clayton |

031 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

4% |

|

|

|

|

|

|

|

|

|

|

|

||||||||||

7. |

Clayton (Jet Fuel) |

|

|

031JF |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

2% |

|

|

|

|

|

|

|

|

|

|

|

|||||||||

8. |

Clayton (Motor Vehicle) |

|

|

031R |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

3% |

|

|

|

|

|

|

|

|

|

|

|

|||||||||

9. |

Clayton (Energy to Manufacturers) |

|

|

031E |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

1% |

|

|

|

|

|

|

|

|

|

|

|

|||||||||

10. Muscogee |

|

106 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

3% |

|

|

|

|

|

|

|

|

|

|

|

|||||||||

11. Muscogee (Motor Vehicle) |

|

|

106R |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

2% |

|

|

|

|

|

|

|

|

|

|

|

|||||||||

12. Muscogee (Energy to Manufacturers) |

|

|

106E |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

1% |

|

|

|

|

|

|

|

|

|

|

|

|||||||||

13. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

14. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

15. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

16. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

17. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

18. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

19. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

20. |

|

|

|

ADDENDUM PAGE TOTALS (if applicable) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

21. |

|

|

|

|

TOTAL SALES TAX (Record on Part A, Line 4) |

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Part B Use Tax Distribution Table |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

JURISDICTION OF |

JURISDICTION OF |

USE TAX |

|

|

|

|

STATE AND LOCAL |

|

|||||||||||||||

|

|

|

|

USE CODE |

REASON CODE |

|

|

|

|

USE TAX AMOUNT |

|

||||||||||||||||

22. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

23. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

24. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

25. |

|

|

|

ADDENDUM PAGE TOTALS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

26. |

|

TOTAL USE TAX (Record on Part A, Line 5) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Print Blank Form

Form

Georgia Department of Revenue

Sales and Use Tax Return

PO Box 105408

Atlanta, Georgia

Clear

Page 3

PART C TSPLOST Sales & Use Tax

|

Jurisdiction |

Code |

A. TSPLOST |

B. TSPLOST |

|

Name |

Taxable Sales Amt |

Use Tax Amt |

|

|

|

|

|

|

1 |

Appling |

001 |

|

|

|

|

|

|

|

2 |

Bleckley |

012 |

|

|

|

|

|

|

|

3 |

Burke |

017 |

|

|

|

|

|

|

|

4 |

Candler |

021 |

|

|

|

|

|

|

|

5 |

Chattahoochee |

026 |

|

|

|

|

|

|

|

6 |

Clay |

030 |

|

|

7 |

Columbia |

036 |

|

|

|

|

|

|

|

8 |

Crisp |

040 |

|

|

|

|

|

|

|

9 |

Dodge |

045 |

|

|

10 |

Dooly |

046 |

|

|

11 |

|

|

|

|

Emanuel |

053 |

|

|

|

12 |

|

|

|

|

Evans |

054 |

|

|

|

13 |

|

|

|

|

Glascock |

062 |

|

|

|

14 |

|

|

|

|

Hancock |

070 |

|

|

|

15 |

|

|

|

|

Harris |

072 |

|

|

|

16 |

|

|

|

|

Jeff Davis |

080 |

|

|

|

17 |

|

|

|

|

Jefferson |

081 |

|

|

|

18 |

|

|

|

|

Jenkins |

082 |

|

|

|

19 |

|

|

|

|

Johnson |

083 |

|

|

|

20 |

|

|

|

|

Laurens |

087 |

|

|

|

21 |

|

|

|

|

Lincoln |

090 |

|

|

|

|

|

|

|

|

22 |

Macon |

094 |

|

|

|

|

|

|

|

23 |

Marion |

096 |

|

|

|

|

|

|

|

|

Jurisdiction |

Code |

A. TSPLOST |

B. TSPLOST |

|

Name |

Taxable Sales Amt |

Use Tax Amt |

|

|

|

|||

|

|

|

|

|

24 |

McDuffie |

097 |

|

|

|

|

|

|

|

25 |

Montgomery |

103 |

|

|

|

|

|

|

|

26 |

Muscogee |

106 |

|

|

|

|

|

|

|

27 |

Quitman |

118 |

|

|

|

|

|

|

|

28 |

Randolph |

120 |

|

|

|

|

|

|

|

29 |

Richmond |

121 |

|

|

30 |

Schley |

123 |

|

|

|

|

|

|

|

31 |

Stewart |

128 |

|

|

|

|

|

|

|

32 |

Sumter |

129 |

|

|

33 |

Talbot |

130 |

|

|

|

|

|

|

|

34 |

Taliaferro |

131 |

|

|

|

|

|

|

|

35 |

Tattnall |

132 |

|

|

|

|

|

|

|

36 |

Taylor |

133 |

|

|

|

|

|

|

|

37 |

Telfair |

134 |

|

|

|

|

|

|

|

38 |

Toombs |

138 |

|

|

|

|

|

|

|

39 |

Treutlen |

140 |

|

|

|

|

|

|

|

40 |

Warren |

149 |

|

|

|

|

|

|

|

41 |

Washington |

150 |

|

|

|

|

|

|

|

42 |

Wayne |

151 |

|

|

|

|

|

|

|

43 |

Webster |

152 |

|

|

|

|

|

|

|

44 |

Wheeler |

153 |

|

|

|

|

|

|

|

45 |

Wilcox |

156 |

|

|

|

|

|

|

|

46 |

Wilkes |

157 |

|

|

|

|

|

|

|

TSPLOST Taxable Sales (Add Column A Lines 1 through 46)

48TSPLOST Sales Tax (Multiply Line 47 by 0.01)

49TSPLOST Use Tax (Add Column B Lines 1 through 46)

50Total TSPLOST Tax (Add Line 48 & Line 49, also enter on Part A Line 6)

Print Blank Form

Form

Georgia Department of Revenue

Sales and Use Tax Return

PO Box 105408

Atlanta, Georgia

Clear

Page 4

Part D Vendor’s Compensation Calculation

TAX AMOUNTS RATE VENDOR’S COMPENSATION

1. State and Local

2. State and Local

3.

4. State and Local

5. TOTAL VENDOR’S COMPENSATION(Record on Part A, Line 11)

3%

.5%

3%

3%

Part E Bad Debt Reporting

1. Bad Debt

2. Bad Debt Recovered ..........................................................................................................

Part F Certification and Signature

I certify that this return, including any accompanying schedules or statements, has been examined by me and is to the best of my knowledge and belief a true and complete return made in good faith for the period stated. This_____________ day of ___________________________, ________.

Return prepared by: |

Phone Number |

Title |

Email Address |

Signature

This return must be filed and paid by the 20th of the month following the period for which the tax is due in order to avoid loss of vendor’s compensation and the application of penalty and interest. Businesses must file a timely return for each period even though no tax is due. Do not remit cash in the mail.

Form Characteristics

| Fact Name | Detail |

|---|---|

| Effective Date | This form is applicable only for sales made during March 2017, with a due date of April 20, 2017. |

| Sourcing Rules | Sales sourced to Georgia include property delivered to purchasers within the state and services performed in the jurisdiction, as per O.C.G.A. § 48-8-77. |

| Amended Returns | Taxpayers can check the amended return box if they are updating a previously submitted return for the same period. |

| No Tax Due Notification | If there were no taxable sales during the reporting period, taxpayers should check the "No Tax Due" box instead of completing the entire form. |

| Electronic Filing | Taxpayers are encouraged to file and pay electronically through the Georgia Tax Center, with further resources available online. |

| Vendor's Compensation | Taxpayers can record their vendor's compensation based on the sales and use tax collected, with specific percentages dependent on the total tax amount. |

| Use Tax Obligation | If sales tax is unpaid on an item used in Georgia, the use tax must be reported using the relevant jurisdiction of use code. |

| Transportation Local Option | This tax should not be reported in Part B; it has a dedicated section in Part C for TSPLOST sales and use tax reporting. |

| Additional Forms | For detailed situations or additional sales, taxpayers may need to include addendum pages, which are available on the Georgia Department of Revenue’s website. |

Guidelines on Utilizing Ga St 3 Tax

To ensure you successfully file the Georgia ST-3 Tax Form, meticulous attention to detail is required. The completion process involves several key steps, each of which contributes to accurately reporting your sales and use tax obligations for the appropriate period. It's crucial to gather your sales records, ensure you have the necessary documentation, and approach this process with the understanding that any errors could lead to penalties or misreporting. Proceed carefully through the following steps to complete the form correctly.

- Begin by entering your Sales and Use Tax Number (STN) as well as the name and address of the registered taxpayer.

- Enter the period ending date (mm/dd/yy) that corresponds to the reporting period.

- If you are amending a previously filed return, check the box for Amended Return.

- If there were no taxable sales during this period, check the No Tax Due box.

- If there was no sales and use tax activity, complete the No Sales/Use Tax Activity box on Page 5 and submit the payment voucher (Form PV-ST). Do not complete the ST-3 form in this case.

For Part A - Tax Summary, follow these instructions:

- Record the Total State Sales (all sales sourced to the State of Georgia), including leases and rentals.

- Record Total Exempt State Sales (including leases and rentals), ensuring to include exempt sales subject to local sales tax.

- Subtract the amount in Line 2 from Line 1 to record your Taxable State Sales.

- Transfer the Total SALES Tax Amount from Part B, Line 21.

- Transfer the Total USE Tax Amount from Part B, Line 26.

- Record the TSPLOST tax from Part C, Line 50.

- Record the Pre-paid Local Sales/Use Tax for on-road motor fuel from Form ST-3 Motor Fuel.

- Record Total Sales/Use Tax Collected for the reporting period from your accounting records.

- Add Lines 4 through 7 to calculate the total tax amount and record this sum.

- Calculate the Excess Tax amount by subtracting the Total Sales/Use Tax amount (Line 9) from Total Tax Collected (Line 8) and record it.

- Record Total Vendor’s Compensation from Part D, Line 5.

- Record previous prepaid estimated tax, if applicable, based on your annual prepaid estimated tax letter.

- Record current prepaid estimated tax, if applicable, also referencing your annual prepaid estimated tax letter.

- Calculate the Total Amount Due by adding Lines 9 and 10 and then subtracting Lines 11 and 12 before adding Line 13.

Proceed to fill out Part B - Sales Tax Distribution Table:

- Record Taxable State Sales and multiply by the applicable tax rate from the Part B table for the Sales Tax Amount.

- Record sales of energy sold to manufacturers and calculate the Sales Tax Amount.

- Record taxable non-motor vehicle sales for the City of Atlanta and calculate the Sales Tax Amount.

- Record motor vehicle sales in the City of Atlanta and calculate the Sales Tax Amount.

- Document taxable sales of energy sold to manufacturers sourced to the City of Atlanta and calculate the Sales Tax Amount.

- Continue recording taxable sales for Clayton County, including jet fuel and other sales, using the appropriate calculations.

- Similarly, report taxable sales for Muscogee County and any other counties as necessary, providing accurate jurisdiction and tax rate information.

- For any additional pages, sum up the Sales Tax Amount from all completed forms.

- Finally, record the total from Lines 1-20 as the Total Sales Tax and carry this over to Part A, Line 4.

Complete Part B - Use Tax Distribution Table and Part C - TSPLOST Sales & Use Tax by following the similar structure of inputting the required data and ensuring it is consistent. Always double-check your totals and review while preparing for submission.

Once all parts are completed, ensure everything is accurate and submit the form electronically through the Georgia Tax Center if applicable. This step not only eases the filing process but also ensures prompt payment options are available. Prompt filing is crucial, as deadlines can lead to penalties or interest on late payments.

What You Should Know About This Form

What is the GA ST 3 Tax form?

The GA ST 3 Tax form, also known as the Sales and Use Tax Return, is used by taxpayers in Georgia to report sales and use tax for a specific period. This form captures details such as total sales, exemptions, and tax liability. It ensures compliance with state tax regulations and provides information necessary to calculate the correct sales and use tax owed to jurisdictions within Georgia.

When is the GA ST 3 Tax form due?

The GA ST 3 Tax form is due on April 20 for sales made during the reporting period. For instance, if you are reporting sales for March 2017, the completed form must be submitted by April 20, 2017. Timely submission helps avoid penalties and interest on unpaid taxes.

Who needs to file the GA ST 3 Tax form?

All businesses making taxable sales in Georgia are required to file the GA ST 3 Tax form, regardless of their size. Specific requirements may differ depending on the location of sales, especially for those with sales sourced to the City of Atlanta or other jurisdictions with unique tax obligations. If a business had no taxable sales during the reporting period, a different form indicating no activity should be filed.

What type of transactions are reported on the GA ST 3 Tax form?

This form requires taxpayers to report all sales sourced to Georgia, including sales of tangible personal property and certain services. Additional reporting is necessary for exempt sales, fuel sales, and specific local taxes such as TSPLOST. Each entry must clearly indicate which types of transactions are being reported to ensure accuracy.

How can I file the GA ST 3 Tax form electronically?

Taxpayers can file the GA ST 3 Tax form electronically through the Georgia Tax Center. To do this, visit https://gtc.dor.ga.gov. The Georgia Department of Revenue also provides additional resources, including instructional videos and FAQs about the electronic filing process, which can simplify your filing experience.

What if I need to amend my GA ST 3 Tax form?

If you discover an error on your previously submitted GA ST 3 Tax form, you can amend your return by checking the "Amended Return" box on the form. This notifies the Georgia Department of Revenue to review the changes and calculate any potential adjustments to your tax liability. Be sure to include all relevant details when completing the amended return.

What is the Vendor's Compensation on the GA ST 3 Tax form?

Vendor's Compensation is a percentage that allows businesses to retain a portion of the sales and use tax they collect to compensate for the cost of collecting the tax. The compensation varies depending on the total sales and use tax amount collected. It is calculated on different thresholds outlined in Part D of the form and should be included in the overall tax calculation.

What if I had no sales or use tax activity during the reporting period?

If there were no sales or use tax activities during the reporting period, taxpayers do not need to complete the GA ST 3 Tax form. Instead, they should check the "No Sales/Use Tax Activity" box provided on Page 5 and submit a payment voucher (Form PV-ST Sales and Use Tax Voucher) only.

Where can I find additional resources or help regarding the GA ST 3 Tax form?

Additional instructions, resources, and forms are available on the Georgia Department of Revenue’s website at http://dor.georgia.gov/georgia-tax-center-info. This site offers valuable information, including addendum pages if more space is needed for reporting. For any questions, contacting the Department of Revenue directly may also provide clarity and assistance.

Common mistakes

Filling out the Georgia ST-3 Tax form can be a daunting task. Many people make mistakes that can lead to errors in their tax reporting. One common error is failing to accurately record the Sales and Use Tax Number (STN). This number is essential for identifying the taxpayer. Leaving it blank or entering it incorrectly can complicate matters and delay processing.

Another mistake is not checking the appropriate boxes on the form. For example, if there were no taxable sales during the reporting period, the taxpayer must check the “No Tax Due” box. Ignoring this step can lead to unnecessary confusion and could result in the form being returned for corrections.

It's important to pay close attention to the calculations involved. Many individuals forget to subtract exempt sales from total sales, which could lead to incorrect Taxable State Sales figures. This mistake could have a significant impact on the total tax due. Double-checking these numbers can avoid potential penalties.

People often overlook the requirement to complete additional pages if their sales are spread across several counties. Each county requires its own entry, and failing to accurately report sales for all applicable jurisdictions can result in an incomplete return. It's critical to diligently record taxable sales by county and ensure each entry is totaled correctly.

Lastly, some taxpayers fail to submit the right voucher when there’s no activity reported. Instead of completing the ST-3 form, they should check the “No Sales/Use Tax Activity” box and submit the payment voucher alone. This ensures that the return is processed correctly and can save time and effort later on.

Documents used along the form

The Georgia Sales and Use Tax Form (ST-3) is essential for reporting sales and use tax in the state. Alongside the ST-3 form, several additional documents are commonly used to manage tax responsibilities effectively. Below is a list of these forms and documents, providing a brief description of each.

- Form PV-ST Sales and Use Tax Voucher: This voucher is submitted when no sales and use tax is due, or for periods of no sales activity. It allows taxpayers to confirm their reporting status.

- Form ST-3 Motor Fuel: Used to report prepaid local sales/use tax for on-road motor fuel, this form provides details on fuel taxation separate from regular sales and use tax reporting.

- Form ST-3 Addendum Sales: When additional taxable sales data exceeds the standard form lines, this addendum captures further entries, ensuring accurate reporting of all taxation items across various jurisdictions.

- Form ST-3 Addendum Use: Similar to the sales addendum, this document tracks state and local use tax amounts. It is used when the original form doesn't offer enough space for comprehensive reporting.

- Off-Road Fuel Worksheet: This worksheet is not filed with the ST-3 but helps calculate state and local sales/use tax due on off-road motor fuel. It is kept for the taxpayer’s records.

- Annual Prepaid Estimated Tax Letter: This letter outlines expected tax payments for the coming year. Taxpayers can refer to it when reporting current and past prepaid estimated taxes.

- Georgia Tax Center Registration: This online platform provides an avenue for electronic filing and payment, accompanied by instructional materials and FAQs to aid taxpayers in completing their forms correctly.

- Tax Exemption Certificates: These certificates may be utilized to document sales exempt from state sales tax. Business owners keep these on file to validate their tax-exempt sales.

- Sales Tax Rate Chart: This chart provides jurisdiction codes and corresponding tax rates. It assists taxpayers in determining the appropriate tax amounts for different areas when filing their returns.

- Audit Documentation: Records maintained to support claims made on the ST-3 form, including invoices and sales receipts, can be reviewed during an audit. Proper documentation helps ensure compliance with state tax laws.

Using these forms and documents in conjunction with the Ga ST 3 Tax form can help ensure correct reporting and compliance with Georgia sales and use tax regulations. Each document serves a specific purpose, aiding taxpayers in navigating their tax obligations more effectively.

Similar forms

- Form 1040 (U.S. Individual Income Tax Return): Like the Ga ST-3 form, this document requires taxpayers to report income and deductions, providing a total that impacts the amount of tax owed or refunded. It includes various sections to summarize financial activities over the year, similar to the tax summaries required by the Ga ST-3.

- Form 941 (Employer's Quarterly Federal Tax Return): This form is used to report employment taxes withheld from employee wages. Both forms require careful calculation and reporting of tax liabilities within specified periods, emphasizing accuracy in financial data.

- Form 1065 (U.S. Return of Partnership Income): Partners must report their income, deductions, and credits, paralleling the Ga ST-3’s focus on summarizing sales made in the state, showing how both documents aim to detail financial transactions for tax purposes.

- Sales Tax Return (various states): Similar to the Ga ST-3, different states have their own sales tax return forms that require reporting total sales, exempt sales, and taxable sales, thereby ensuring compliance with local tax laws.

- Form W-2 (Wage and Tax Statement): Employers must report wages paid to employees and the taxes withheld from those wages. Both forms share the goal of accurately reflecting financial figures over a specific timeframe for tax assessment.

- Form 1065-B (U.S. Return of Income for Electing Large Partnerships): Just as the Ga ST-3 mandates a breakdown of specific sales data, this form requires entities to detail income and deductions across multiple partners, maintaining transparency and accountability in reporting.

- Form 990 (Return of Organization Exempt From Income Tax): Non-profits must file this form to report their financial activities. Similar to the Ga ST-3, it necessitates a detailed overview of revenue, expenses, and tax-exempt status, focusing on financial accountability.

Dos and Don'ts

- Do gather all necessary records before starting the form. This includes your Sales and Use Tax Number, addresses, and sales data for the reporting period.

- Do accurately complete all relevant sections of the form. Ensure that you carefully subtract exempt sales from total sales to determine taxable sales.

- Do check the appropriate boxes as required. Indicate if you are filing an amended return or if there is no tax due to avoid any confusion in processing.

- Do file electronically if possible. Using the Georgia Tax Center can simplify the process and provide immediate confirmation of your submission.

- Don't forget to include all sales sourced to Georgia, including any applicable exemptions. Missing sales can lead to inaccurate reporting.

- Don't neglect to file if you had no sales activity. Instead of submitting the ST-3 form, just check the "No Sales/Use Tax Activity" box and submit the payment voucher.

- Don't ignore the deadlines. Make sure to file your return by April 20, 2017, to avoid any penalties.

- Don't mix different types of sales in your reporting. Ensure that taxable and exempt sales are reported separately, especially when dealing with energy sales to manufacturers.

Misconceptions

Misunderstandings can create confusion when it comes to tax forms. Here are some common misconceptions about the Georgia ST-3 Tax form.

- Only businesses need to file the ST-3. Many individuals fail to recognize that they, too, may have tax obligations related to sales and use tax. Consumers who make taxable purchases from out-of-state vendors could also owe use tax.

- There are no taxes to report if there were no sales during the period. This is not true. If there were no taxable sales, it’s essential to check the "No Tax Due" box. Filling out the form correctly is still important.

- The ST-3 can be filed any time before the deadline. While this might seem convenient, it’s crucial to keep track of the due date. Late submissions can result in penalties and interest.

- All sales are subject to tax under the ST-3. Not every sale requires tax to be collected. Many exemptions exist, such as sales to certain industries or types of goods. Understanding these exemptions is vital for accurately completing the form.

- Electronic filing is optional. Although paper filing is allowed, electronic filing is often encouraged. It’s typically faster and reduces the chances of errors.

- Tax collected during the year is the only amount to report. It is important to report all tax collected, including any changes made later, such as adjustments or refunds. This ensures accurate reporting and compliance.

Addressing these misconceptions can lead to better compliance and smoother tax reporting. Keeping informed helps everyone navigate the complexities of tax responsibilities.

Key takeaways

Effective for sales made during March 2017, the Ga St 3 Tax form is due on April 20, 2017.

Taxpayers with sales sourced to the City of Atlanta must complete Part B, specifically Lines 3 through 5.

Sales sourced to a jurisdiction typically include property delivered to the purchaser or services performed within that jurisdiction.

To file electronically, taxpayers are encouraged to visit the Georgia Tax Center online.

The form requires accurate recording of the Sales and Use Tax Number, taxpayer details, as well as the reporting period's end date.

If there were no taxable sales during the period, individuals should check the No Tax Due box instead of completing the form.

Part A provides a tax summary, including calculations for state taxable sales, exempt sales, and various tax amounts.

Part B is essential for distributing the state tax, particularly highlighting sales taxable for different counties.

Use tax is applicable when sales tax was not paid on an item and it is used within Georgia.

Vendor's compensation calculations in Part D cap the sum of tax activity, providing refunds for bad debt in Part E.

Browse Other Templates

Skyzone Applications - Provide your current contact information.

Nys Household Credit - Using the correct mailing address and format can prevent lost payments.

Vit Tax - The motor vehicle inventory tax is calculated based on sales price and unit property tax factors.