Fill Out Your Independent Form

The Independent Review is a crucial aspect of maintaining a compliant and effective Anti-Money Laundering (AML) Compliance Program for Money Services Businesses (MSBs). This process typically occurs at a frequency set during the establishment of the Compliance Program, with MoneyGram’s approval required. If your business does not have a specific Independent Review form, templates provided in the documentation should be utilized to guide the reviewer. It is vital to understand that federal AML regulations mandate this review to ensure ongoing compliance. The review must be carried out by individuals who possess a solid understanding of AML requirements and, importantly, cannot be a designated Compliance Officer or anyone reporting directly to them. After the review is completed, the signed Independent Review form should be carefully retained with other compliance documents for a minimum of five years. This ensures that your business can prove its compliance efforts during any potential audits or investigations. A comprehensive review addresses various critical components, including risk assessments of the business's location and services offered, the establishment of a rigorous Compliance Program, employee training protocols, and detailed transaction processes. Each of these elements works in tandem to safeguard your business from the risks associated with money laundering and financial crimes.

Independent Example

Section 4 : Independent Review

MoneyGram

INDEPENDENT REVIEW

When you established your Compliance Program and with MoneyGram's approval, you indicated how often you would have an Independent Review of your AML Compliance Program.

In the event that you do not have your own Independent Review form, the following pages of this section

contains an Independent Review template that you should have the reviewer use as a guide and complete

accordingly.

As a reminder:

•An Independent Review of your MSB is required by Federal AML Regulations.

•The Independent Review will be conducted by a person or persons who are knowledgeable about the AML requirements that apply to MSBs.

•The Agent's Independent Review cannot be conducted by your designated Compliance Officer, anyone that reports to your Compliance Officer, or any MoneyGram representative.

What do I do with the completed Independent Review Form?

Once the Independent Review Form has been completed and signed by the reviewer, please keep/file/store it with your Compliance related documents for at least 5 years.

Please make extra copies of the blank Independent Review Form and

do not use your last blank one.

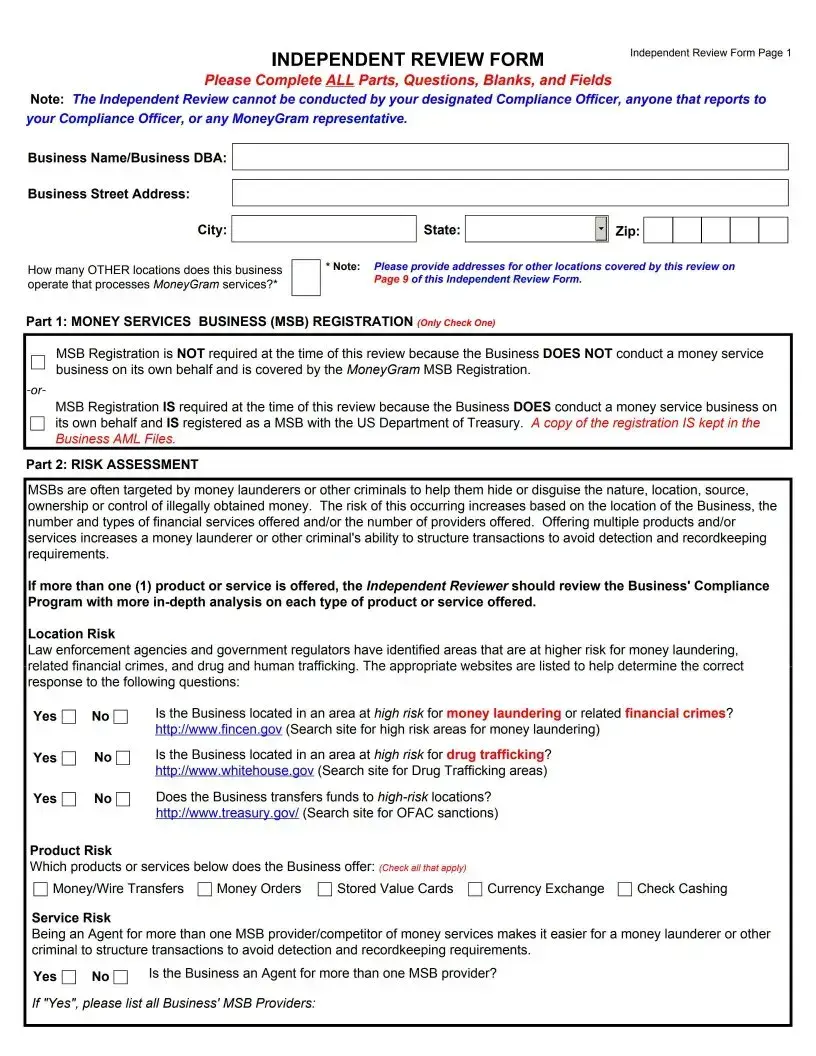

INDEPENDENT REVIEW FORM

Independent Review Form Page 1

Please Complete ALL Parts, Questions, Blanks, and Fields

Note: The Independent Review cannot be conducted by your designated Compliance Officer, anyone that reports to your Compliance Officer, or any MoneyGram representative.

How many OTHER locations does this business |

Note: Please provide addresses for other locations covered by this review on |

operate that processes MoneyGram services?* |

Page 9 of this Independent Review Form. |

|

Part 1: MONEY SERVICES BUSINESS (MSB) REGISTRATION (Only Check One)

MSB Registration is NOT required at the time of this review because the Business DOES NOT conduct a money service business on its own behalf and is covered by the MoneyGram MSB Registration.

MSB Registration IS required at the time of this review because the Business DOES conduct a money service business on

Оits own behalf and IS registered as a MSB with the US Department of Treasury. A copy of the registration IS kept in the Business AML Files.

Part 2: RISK ASSESSMENT

MSBs are often targeted by money launderers or other criminals to help them hide or disguise the nature, location, source, ownership or control of illegally obtained money. The risk of this occurring increases based on the location of the Business, the number and types of financial services offered and/or the number of providers offered. Offering multiple products and/or services increases a money launderer or other criminal's ability to structure transactions to avoid detection and recordkeeping requirements.

If more than one (1) product or service is offered, the Independent Reviewer should review the Business' Compliance Program with more

Location Risk

Law enforcement agencies and government regulators have identified areas that are at higher risk for money laundering, related financial crimes, and drug and human trafficking. The appropriate websites are listed to help determine the correct response to the following questions:

Yes |

NoD |

Is the Business located in an area at high risk for money laundering or related financial crimes? |

|

|

htto://www.fincen.aov (Search site for hiqh risk areas for monev launderinq) |

Yes |

NoD |

Is the Business located in an area at high risk for drug trafficking? |

|

|

htto://www.whitehouse.qov (Search site for Druq Traffickinq areas) |

Yes |

NoD |

Does the Business transfers funds to |

|

|

htto://www.treasurv.qov/ (Search site for OFAC sanctions) |

Product Risk

Which products or services below does the Business offer: (Check all that apply)

ОMoney/Wire Transfers Q Money Orders Q Stored Value Cards Q Currency Exchange Q Check Cashing

Service Risk

Being an Agent for more than one MSB provider/competitor of money services makes it easier for a money launderer or other criminal to structure transactions to avoid detection and recordkeeping requirements.

Yes О No О Is the Business an Agent for more than one MSB provider?

If "Yes", please list all Business' MSB Providers:

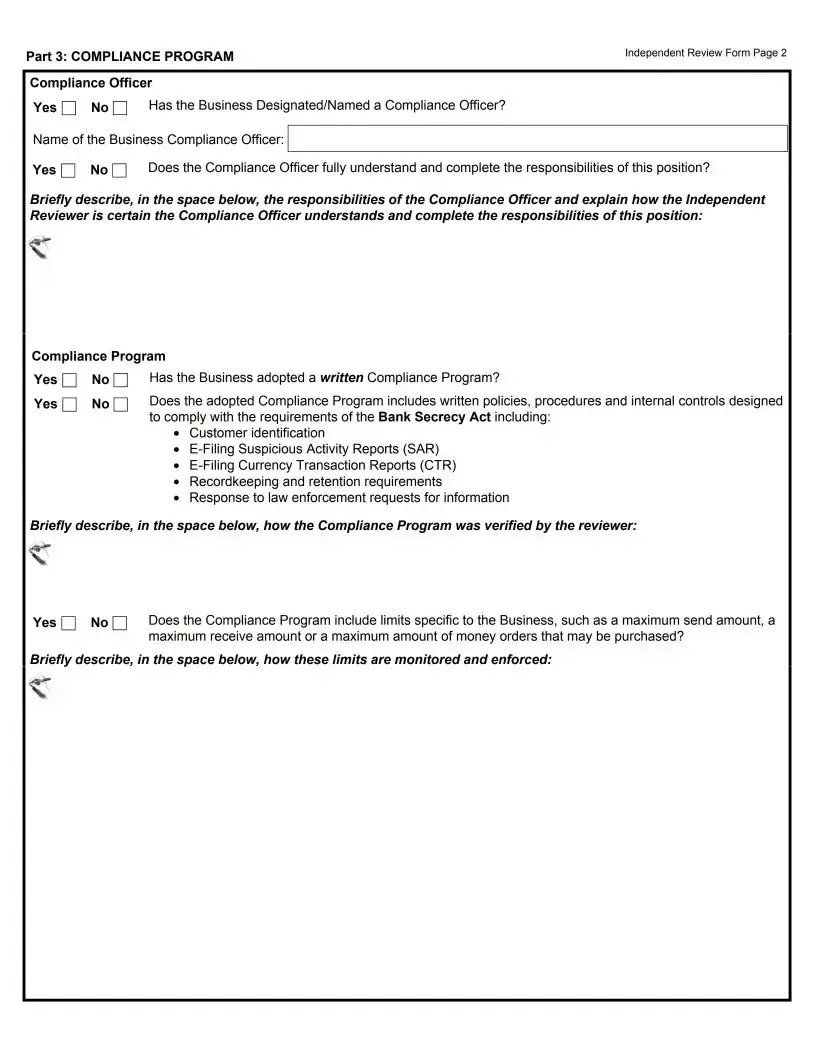

Part 3: COMPLIANCE PROGRAM |

Independent Review Form Page 2 |

Compliance Officer

Yes |

No О Has the Business Designated/Named a Compliance Officer? |

Name of the Business Compliance Officer:

Yes П No О Does the Compliance Officer fully understand and complete the responsibilities of this position?

Briefly describe, in the space below, the responsibilities of the Compliance Officer and explain how the Independent Reviewer is certain the Compliance Officer understands and complete the responsibilities of this position:

Compliance Program

Yes О No П |

Has the Business adopted a written Compliance Program? |

||

Yes |

No |

Does the adopted Compliance Program includes written policies, procedures and internal controls designed |

|

|

|

to comply with the requirements of the Bank Secrecy Act including: |

|

|

|

• |

Customer identification |

|

|

• |

|

|

|

• |

|

|

|

• Recordkeeping and retention requirements |

|

|

|

• |

Response to law enforcement requests for information |

Briefly describe, in the space below, how the Compliance Program was verified by the reviewer:

Yes |

No О Does the Compliance Program include limits specific to the Business, such as a maximum send amount, a |

|

maximum receive amount or a maximum amount of money orders that may be purchased? |

Briefly describe, in the space below, how these limits are monitored and enforced:

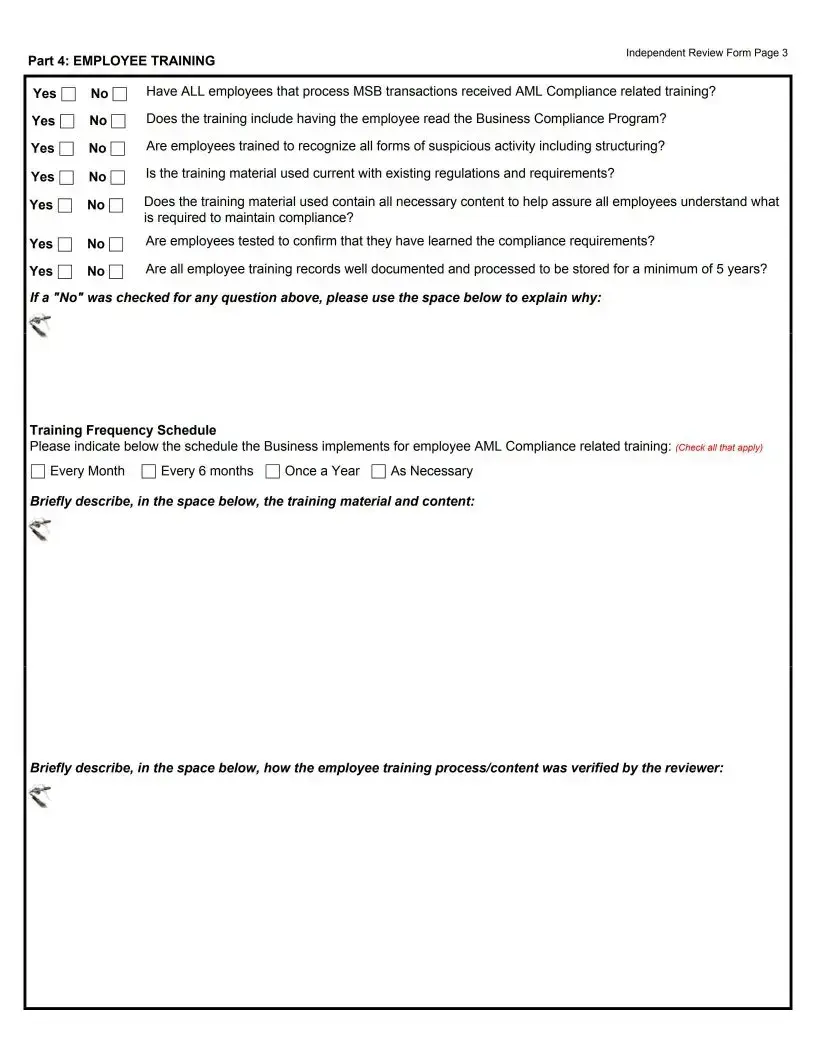

Part 4: |

|

Independent Review Form Page 3 |

EMPLOYEE TRAINING |

||

Yes |

NoD |

Have ALL employees that process MSB transactions received AML Compliance related training? |

Yes |

NoD |

Does the training include having the employee read the Business Compliance Program? |

Yes |

No |

Are employees trained to recognize all forms of suspicious activity including structuring? |

Yes |

No |

Is the training material used current with existing regulations and requirements? |

Yes |

No |

Does the training material used contain all necessary content to help assure all employees understand what |

|

|

is required to maintain compliance? |

Yes |

No |

Are employees tested to confirm that they have learned the compliance requirements? |

Yes |

No |

Are all employee training records well documented and processed to be stored for a minimum of 5 years? |

If a "No" was checked for any question above, please use the space below to explain why:

Training Frequency Schedule

Please indicate below the schedule the Business implements for employee AML Compliance related training: (Check all that apply)

Every Month |

Every 6 months |

Once a Year О As Necessary |

Briefly describe, in the space below, the training material and content:

Briefly describe, in the space below, how the employee training process/content was verified by the reviewer:

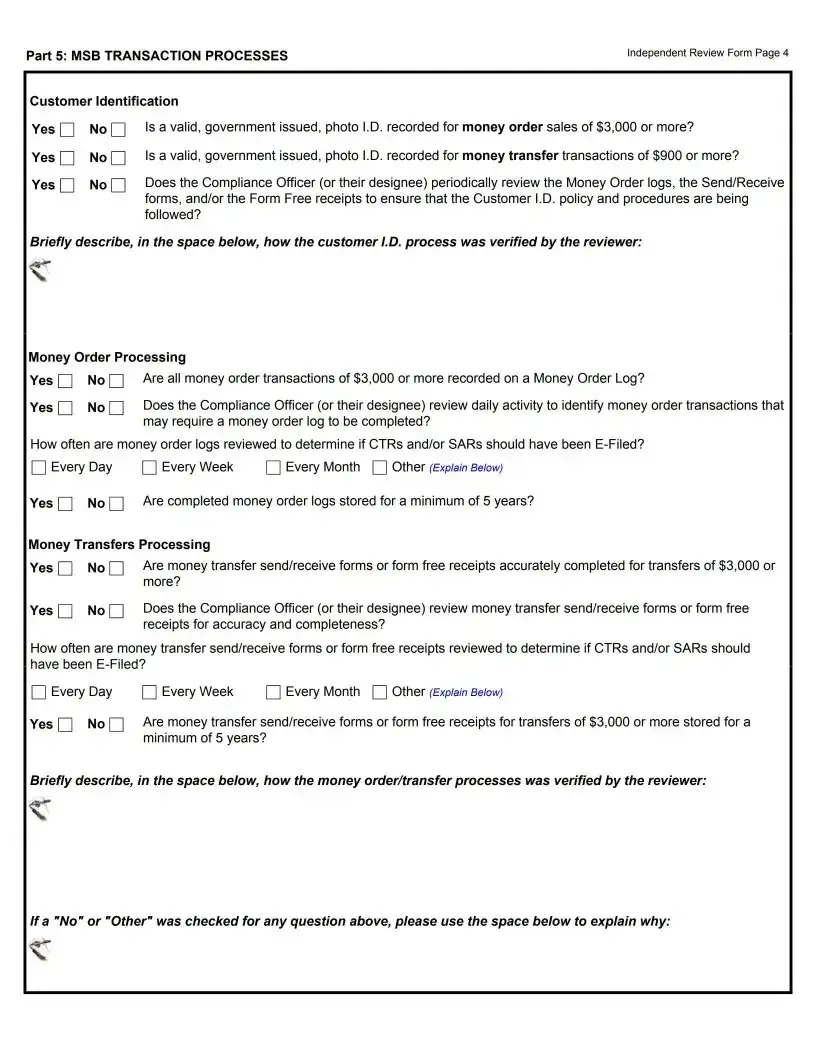

Part 5: MSB TRANSACTION PROCESSES |

Independent Review Form Page 4 |

Customer Identification

Yes |

NoD |

Is a valid, government issued, photo I.D. recorded for money order sales of $3,000 or more? |

Yes |

No О |

Is a valid, government issued, photo I.D. recorded for money transfer transactions of $900 or more? |

Yes |

No |

Does the Compliance Officer (or their designee) periodically review the Money Order logs, the Send/Receive |

|

|

forms, and/or the Form Free receipts to ensure that the Customer I.D. policy and procedures are being |

|

|

followed? |

Briefly describe, in the space below, how the customer I.D. process was verified by the reviewer:

Money Order Processing

Yes |

No О Are all money order transactions of $3,000 or more recorded on a Money Order Log? |

|

Yes |

No |

Does the Compliance Officer (or their designee) review daily activity to identify money order transactions that |

|

|

may require a money order log to be completed? |

How often are money order logs reviewed to determine if CTRs and/or SARs should have been

Ц Every Day |

Q Every Week |

Q Every Month Q Other (Explain Below) |

|

Yes |

No О |

Are completed money order logs stored for a minimum of 5 years? |

|

Money Transfers Processing |

|

||

Yes |

No |

Are money transfer send/receive forms or form free receipts accurately completed for transfers of $3,000 or |

|

|

|

more? |

|

Yes |

No О |

Does the Compliance Officer (or their designee) review money transfer send/receive forms or form free |

|

|

|

receipts for accuracy and completeness? |

|

How often are money transfer send/receive forms or form free receipts reviewed to determine if CTRs and/or SARs should have been

О Every Day |

Every Week |

Q Every Month Ц Other (Explain Below) |

|

Yes |

No П |

Are money transfer send/receive forms or form free receipts for transfers of $3,000 or more stored for a |

|

|

|

minimum of 5 years? |

|

Briefly describe, in the space below, how the money order/transfer processes was verified by the reviewer:

V

If a "No" or "Other" was checked for any question above, please use the space below to explain why:

V

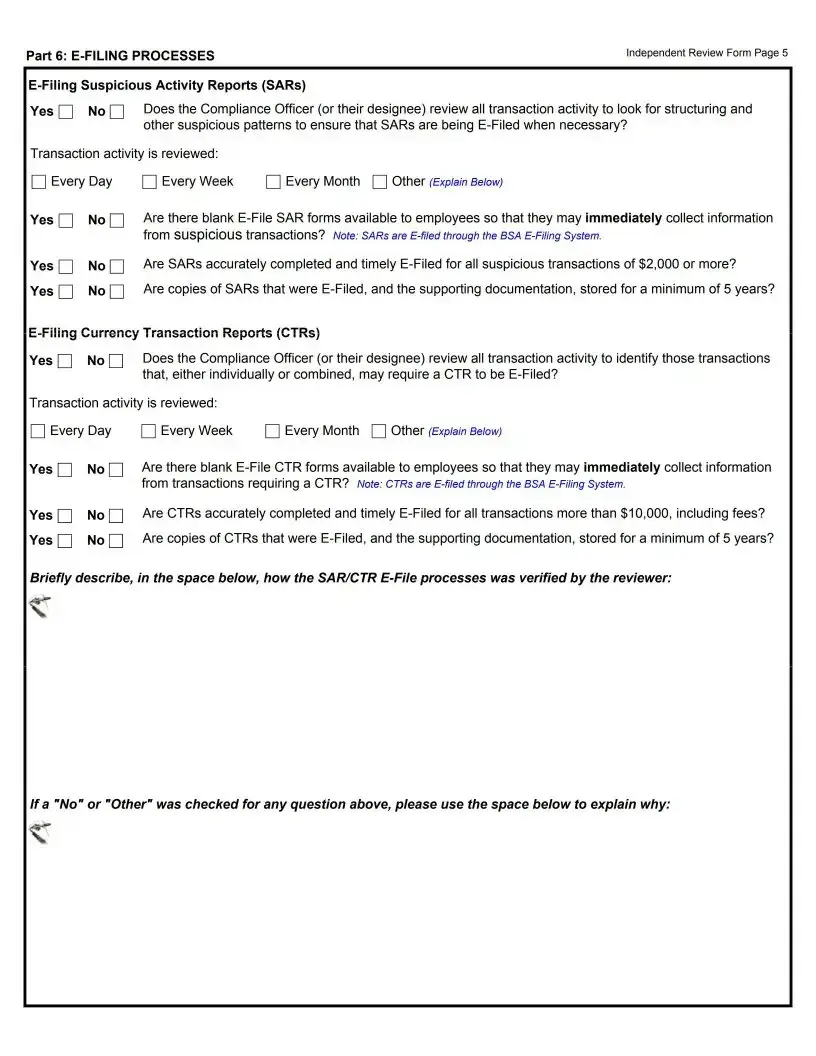

Part 6: |

Independent Review Form Page 5 |

Yes |

No |

Does the Compliance Officer (or their designee) review all transaction activity to look for structuring and |

|

|

other suspicious patterns to ensure that SARs are being |

Transaction activity is reviewed:

Ц Every Day |

Q Every Week |

Q Every Month Q Other (Explain Below) |

|

Yes |

No О |

Are there blank |

|

|

|

from suspicious transactions? Note: SARs are |

|

Yes |

No О |

Are SARs accurately completed and timely |

|

Yes |

No |

Are copies of SARs that were |

|

Yes |

No О |

Does the Compliance Officer (or their designee) review all transaction activity to identify those transactions |

|

|

|

that, either individually or combined, may require a CTR to be |

|

Transaction activity is reviewed:

О Every Day |

Every Week |

Q Every Month Q Other (Explain Below) |

|

Yes П No О |

Are there blank |

||

|

|

from transactions requiring a CTR? Note: CTRs are |

|

Yes |

No О |

Are CTRs accurately completed and timely |

|

Yes |

No О |

Are copies of CTRs that were |

|

Briefly describe, in the space below, how the SAR/CTR

If a "No" or "Other" was checked for any question above, please use the space below to explain why:

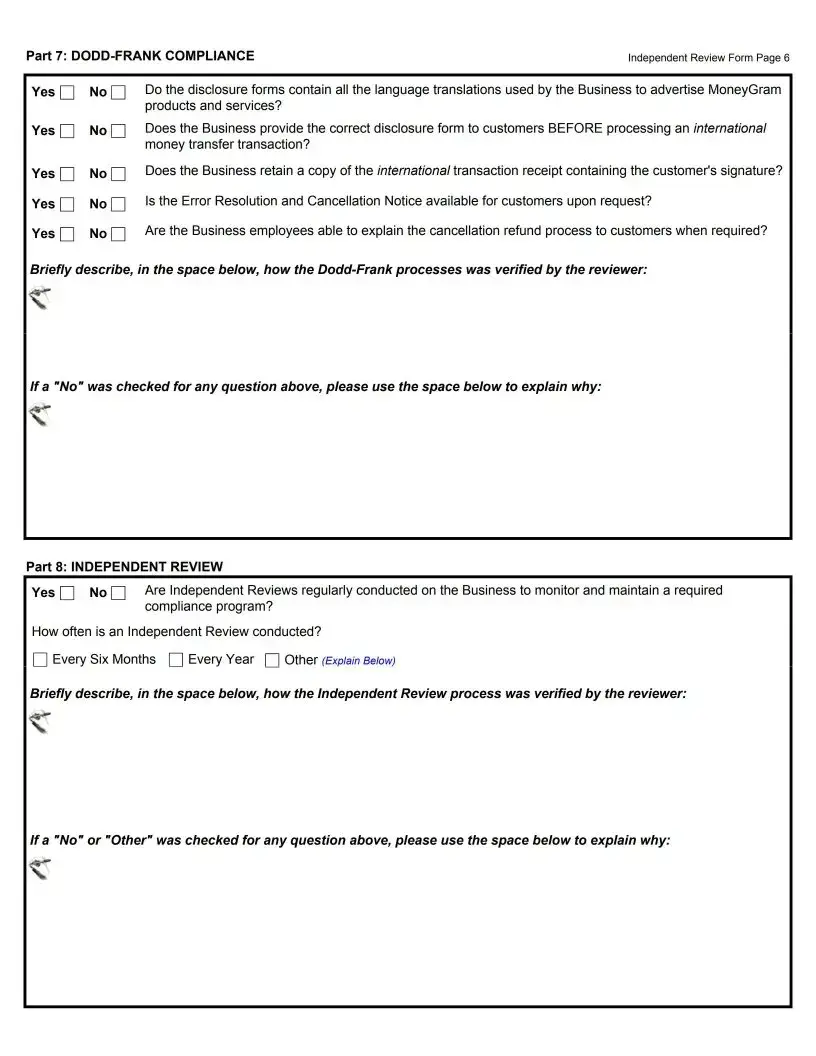

Part 7: |

Independent Review Form Page 6 |

||

Yes |

No |

Do the disclosure forms contain all the language translations used by the Business to advertise MoneyGram |

|

|

|

products and services? |

|

Yes |

No |

Does the Business provide the correct disclosure form to customers BEFORE processing an international |

|

|

|

money transfer transaction? |

|

Yes |

No |

Does the Business retain a copy of the international transaction receipt containing the customer's signature? |

|

Yes |

No |

Is the Error Resolution and Cancellation Notice available for customers upon request? |

|

Yes |

No |

Are the Business employees able to explain the cancellation refund process to customers when required? |

|

Briefly describe, in the space below, how the

If a "No" was checked for any question above, please use the space below to explain why:

V

Part 8: INDEPENDENT REVIEW___________________________________________________________________

Yes |

No |

Are Independent Reviews regularly conducted on the Business to monitor and maintain a required |

|

|

compliance program? |

How often is an Independent Review conducted?

Every Six Months Every Year Other (Explain Below)

Briefly describe, in the space below, how the Independent Review process was verified by the reviewer:

c

If a "No" or "Other" was checked for any question above, please use the space below to explain why:

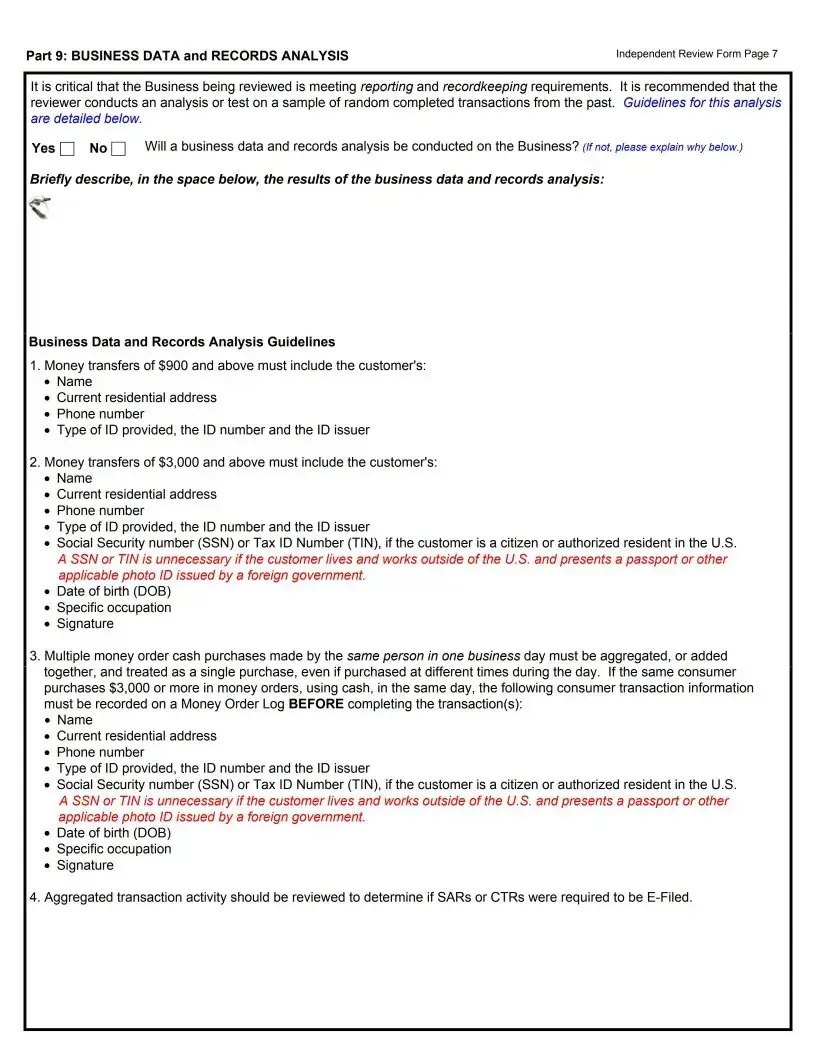

Part 9: BUSINESS DATA and RECORDS ANALYSIS |

Independent Review Form Page 7 |

It is critical that the Business being reviewed is meeting reporting and recordkeeping requirements. It is recommended that the reviewer conducts an analysis or test on a sample of random completed transactions from the past. Guidelines for this analysis

are detailed below.

Yes |

No О Will a business data and records analysis be conducted on the Business? (if not, please explain why below.) |

Briefly describe, in the space below, the results of the business data and records analysis:

Business Data and Records Analysis Guidelines

1.Money transfers of $900 and above must include the customer's:

•Name

•Current residential address

•Phone number

•Type of ID provided, the ID number and the ID issuer

2.Money transfers of $3,000 and above must include the customer's:

•Name

•Current residential address

•Phone number

•Type of ID provided, the ID number and the ID issuer

•Social Security number (SSN) or Tax ID Number (TIN), if the customer is a citizen or authorized resident in the U.S. A SSN or TIN is unnecessary if the customer lives and works outside of the U.S. and presents a passport or other applicable photo ID issued by a foreign government.

•Date of birth (DOB)

•Specific occupation

•Signature

3.Multiple money order cash purchases made by the same person in one business day must be aggregated, or added together, and treated as a single purchase, even if purchased at different times during the day. If the same consumer purchases $3,000 or more in money orders, using cash, in the same day, the following consumer transaction information must be recorded on a Money Order Log BEFORE completing the transaction(s):

•Name

•Current residential address

•Phone number

•Type of ID provided, the ID number and the ID issuer

•Social Security number (SSN) or Tax ID Number (TIN), if the customer is a citizen or authorized resident in the U.S.

ASSN or TIN is unnecessary if the customer lives and works outside of the U.S. and presents a passport or other applicable photo ID issued by a foreign government.

•Date of birth (DOB)

•Specific occupation

•Signature

4.Aggregated transaction activity should be reviewed to determine if SARs or CTRs were required to be

Independent Review Form Page 8

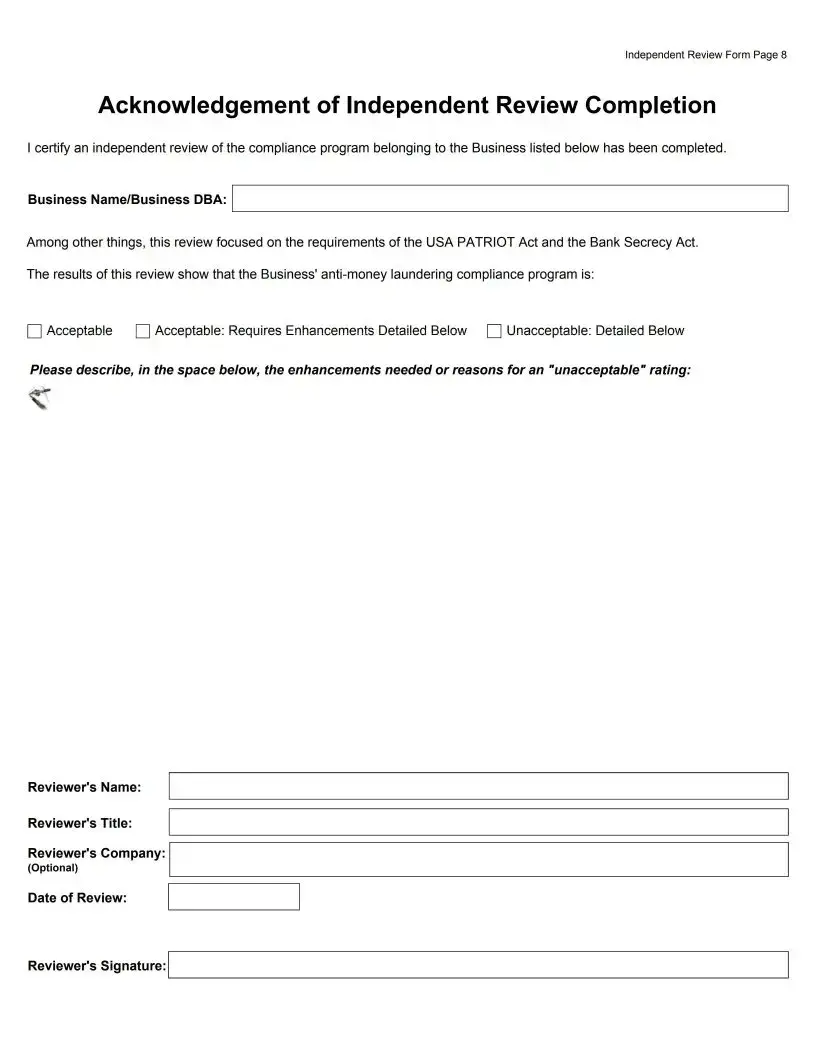

Acknowledgement of Independent Review Completion

I certify an independent review of the compliance program belonging to the Business listed below has been completed.

Business Name/Business DBA:

Among other things, this review focused on the requirements of the USA PATRIOT Act and the Bank Secrecy Act.

The results of this review show that the Business'

ОAcceptable О Acceptable: Requires Enhancements Detailed Below О Unacceptable: Detailed Below

Please describe, in the space below, the enhancements needed or reasons for an "unacceptable" rating:

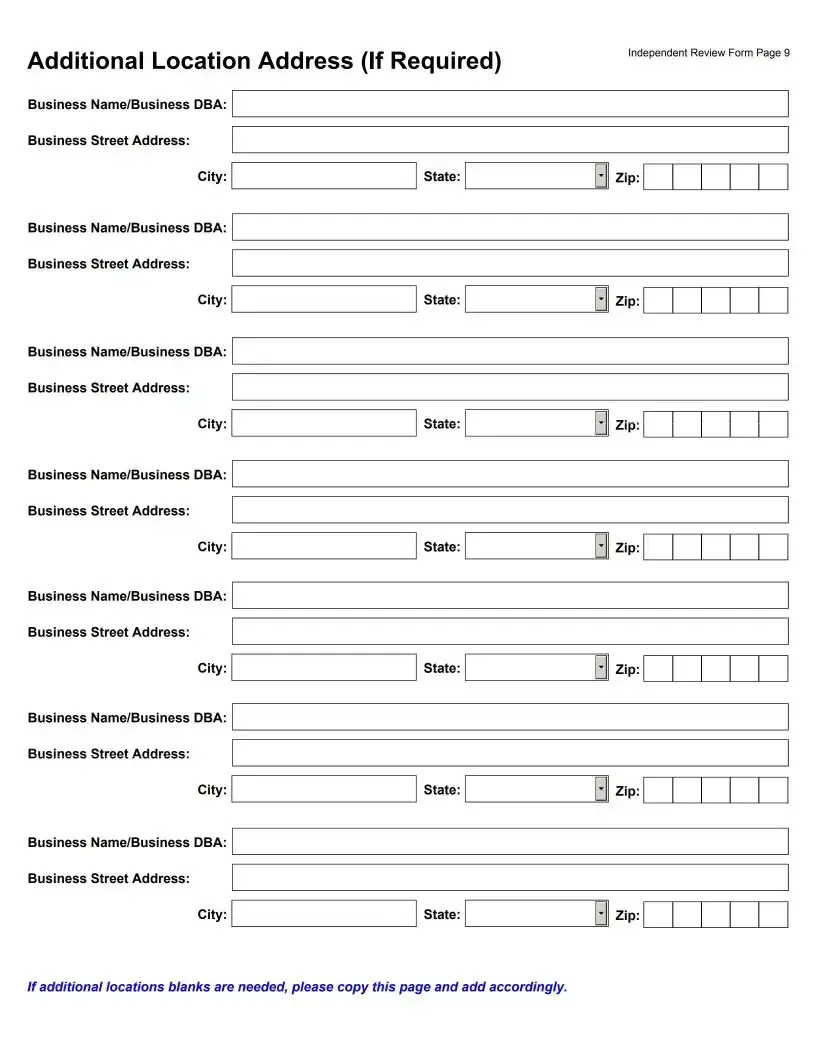

Additional Location Address (If Required)

Independent Review Form Page 9

If additional locations blanks are needed, please copy this page and add accordingly.

Form Characteristics

| Fact Name | Fact Description |

|---|---|

| Purpose of Independent Review | The Independent Review assesses the effectiveness of an AML Compliance Program as per federal regulations. |

| Reviewer Qualifications | The review must be conducted by an individual knowledgeable about AML requirements, excluding the Compliance Officer and direct reports. |

| Document Retention | Completed Independent Review forms must be stored for a minimum of 5 years with compliance documents. |

| Business Registration | Businesses either require MSB registration or are covered under MoneyGram's MSB registration. |

| Risk Assessment Requirement | The review must include a thorough risk assessment based on business location and services offered. |

| Training Verification | All employees involved in MSB transactions must receive AML compliance training and such training must be well documented. |

| Customer Identification Procedures | Valid government-issued photo identification is required for significant transaction amounts ($3,000 for money orders, $900 for transfers). |

| Logs Review | The Compliance Officer or designee must periodically review transaction logs to ensure compliance with identity verification policies. |

| Regulatory Compliance | The Independent Review includes verification that the Compliance Program meets the Bank Secrecy Act requirements. |

Guidelines on Utilizing Independent

Filling out the Independent Review Form requires careful attention to each section to ensure compliance with federal regulations tied to anti-money laundering efforts. Understanding what is needed can make the process smoother and more efficient, benefiting both the reviewer and the business involved. The form is systematically structured to collect necessary information, so following each step is essential for accuracy.

- Start by entering your Business Name/Business DBA in the designated field.

- Fill in the Business Street Address, along with City, State, and Zip Code.

- Indicate the number of OTHER locations that the business operates to process MoneyGram services, if applicable.

- Proceed to Part 1: MONEY SERVICES BUSINESS (MSB) REGISTRATION and check one box indicating whether registration is required at the time of the review.

- Move on to Part 2: RISK ASSESSMENT. Answer the questions regarding location risk by checking Yes or No for each of the three questions.

- For Product Risk, check all the services your business offers from the list provided.

- Answer the question regarding whether the business is an agent for more than one MSB provider and provide a list if applicable.

- Under Part 3: COMPLIANCE PROGRAM, answer questions about the designated Compliance Officer and their understanding of the role.

- Confirm whether the business has adopted a written Compliance Program and respond to questions about its content.

- Detail how the reviewer verified the Compliance Program and provide information about limits specific to the business.

- Check whether all employees involved in MSB transactions have received the necessary training and answer additional questions on training adequacy.

- In Part 4: EMPLOYEE TRAINING, indicate the frequency of AML Compliance training and describe the material used.

- Under Part 5: MSB TRANSACTION PROCESSES, answer questions regarding customer identification for money order sales and money transfer transactions.

- Complete additional questions concerning money order and money transfer processing along with how these processes were verified by the reviewer.

- Finally, review all inputs to ensure correctness before completion of the form.

Once completed, the form should be signed by the reviewer. Store it with your compliance documentation and retain it for at least five years, along with making extra copies of the blank Independent Review Form for future use.

What You Should Know About This Form

What is the purpose of the Independent Review?

The Independent Review is designed to evaluate a Money Services Business (MSB)'s compliance with federal Anti-Money Laundering (AML) regulations. By assessing the compliance program and related practices, the review helps ensure that businesses effectively mitigate risks associated with money laundering and other financial crimes. It provides an external assessment, validating that the business follows required procedures and maintains robust controls to prevent illicit activities.

Who can conduct the Independent Review?

The Independent Review must be conducted by individuals who possess knowledge of AML requirements that apply specifically to MSBs. Importantly, the designated Compliance Officer, their direct reports, or any representative from MoneyGram are prohibited from performing this review. This independence is essential to eliminate any potential bias and uphold the integrity of the compliance assessment.

How should the completed Independent Review Form be handled?

Once the Independent Review Form is finalized and signed by the reviewer, it is crucial to store this document alongside other compliance-related documents for a period of at least five years. Maintaining copies of the completed form is necessary, and businesses should create duplicates of the blank forms to ensure they never run out. Proper record-keeping is essential for regulatory compliance and organizational accountability.

What factors are evaluated in the Risk Assessment section of the Independent Review?

In the Risk Assessment section, multiple factors are reviewed to gauge the potential for money laundering. These include the location of the business, products or services offered, and the business's role as an agent for multiple MSB providers. The presence of a higher risk environment, as evidenced by crime rates or geographical proximity to high-risk areas, is significantly influential in determining the overall risk profile and appropriate compliance measures that need to be implemented.

What components should a Compliance Program include?

A comprehensive Compliance Program should have written policies, procedures, and internal controls that comply with the Bank Secrecy Act. Key areas it should address include customer identification, reporting of suspicious activities, recordkeeping, and how law enforcement requests for information are handled. Additionally, there should be clear protocols laid out for monitoring limits on transactions and ensuring that all employees are adequately trained in the compliance processes.

How often should employee training occur under the Independent Review?

Employee training related to AML compliance should take place regularly, as stipulated by the business’s training frequency schedule. This may be conducted monthly, biannually, annually, or as necessary, depending on the business's specific policies and the evolving regulatory landscape. Consistent training helps ensure that all personnel remain informed and understand how to recognize and report suspicious activities.

What documentation is required for transaction processes in the Independent Review?

Documentation for transaction processes must clearly outline procedures for customer identification, money order processing, and money transfers. For example, valid government-issued photo identification should be recorded for specific transaction thresholds. The Compliance Officer or their designee must periodically review transaction logs and forms to confirm adherence to established guidelines. All related logs and records must be maintained for at least five years for compliance verification.

Common mistakes

Completing the Independent Review Form is a crucial step for ensuring compliance with AML regulations, yet many individuals make common mistakes that can lead to significant issues later on. One prevalent mistake is neglecting to fill out all required parts. Every question and field on the form must be addressed. Leaving sections blank or providing incomplete information raises red flags during compliance audits and can lead to penalties. When filling out the form, take the time to provide thorough responses for each part, ensuring that nothing is overlooked.

Another common error is choosing the incorrect MSB registration option. Respondents must accurately determine whether their business conducts an MSB on its own behalf or falls under the MoneyGram MSB registration. Misidentifying the type of registration can result in improper compliance processes, which may expose the business to legal risks. Carefully review the definitions provided in the form before making this critical decision to avoid any potential pitfalls.

People often forget to consider the depth of risk assessment needed. Section 2 emphasizes assessing location and product risks associated with money laundering and related financial crimes. Failing to conduct a thorough risk assessment may lead the reviewer to miss important vulnerabilities within the business. Conducting a detailed evaluation of all services offered and their associated risks is essential. A comprehensive understanding of these risks will not only strengthen your compliance program but also enhance the overall integrity of your business operations.

Many users also skip over the importance of training records and compliance program verification. Properly documenting employee training and confirming that all staff members understand compliance requirements is essential. In Section 3, the reviewer is asked to describe how the compliance program was verified. Failing to provide this information can suggest that the program lacks rigor and oversight. Make sure to maintain detailed records of training materials, schedules, and employee acknowledgment to demonstrate adherence to AML requirements.

Lastly, a significant oversight involves the retention of the Independent Review Form. Many underestimate the importance of keeping these records for the mandated period of five years. Not storing these documents appropriately can cause issues during an audit or review. Ensure that completed forms are filed securely alongside other compliance-related documentation. This not only satisfies regulatory requirements but also fosters a culture of accountability and transparency within your organization.

Documents used along the form

When managing your Compliance Program, several additional forms and documents can complement the Independent Review Form. These documents serve specific purposes and help ensure that your compliance efforts are thorough and accountable. Below are some commonly used documents associated with the Independent Review process.

- Anti-Money Laundering (AML) Compliance Program: This document outlines the policies, procedures, and internal controls that a business implements to prevent and detect money laundering activities. It is a crucial part of your compliance framework and must be tailored to the specific risks associated with your operations.

- Risk Assessment Document: This document assesses the risks of money laundering and related financial crimes that your business might face. It identifies risk factors based on the nature of your services and location, helping guide your compliance strategies and responses.

- Employee Training Records: These records are essential for documenting that employees have received training on AML regulations and the business's compliance policies. They help ensure that all staff members understand their roles in maintaining compliance and can be critical during audits.

- Suspicious Activity Report (SAR): If there are any transactions or patterns that raise concern, a SAR must be filed with regulatory authorities. This document provides an essential means for reporting suspicious activities and plays a significant role in the broader AML framework.

- Currency Transaction Report (CTR): This report is required for specific cash transactions exceeding a certain threshold. It captures detailed information about the transaction and the parties involved, ensuring that businesses remain compliant with the Bank Secrecy Act.

It’s vital to keep all these documents organized and accessible. By doing so, you enhance your ability to respond effectively to audits or inquiries while promoting a robust compliance culture within your organization.

Similar forms

- Compliance Program Plan: Similar to the Independent Review Form, a Compliance Program Plan outlines the processes and controls a business has in place to ensure adherence to regulatory requirements. Both documents are used to demonstrate a commitment to compliance.

- Risk Assessment Document: The Risk Assessment Document identifies potential risks a business may face, similar to how the Independent Review assesses risk factors related to money laundering and compliance issues.

- Employee Training Manual: Just like the Independent Review Form verifies employee training processes, an Employee Training Manual details the training requirements and responsibilities, ensuring that all employees are knowledgeable about compliance standards.

- Annual Compliance Report: Similar in nature, an Annual Compliance Report summarizes a business's compliance efforts over the previous year, including the outcomes of independent reviews and any identified areas for improvement.

- Audit Report: An Audit Report, like the Independent Review, evaluates compliance with regulations and procedures but typically involves more formal oversight and may cover additional operational areas beyond just AML compliance.

- SAR (Suspicious Activity Report): Just as an Independent Review Form assesses how suspicious activities are handled, a SAR is a specific report filed by a business when it detects suspicious transactions, indicating compliance with AML regulations.

- CTR (Currency Transaction Report): While the Independent Review checks the processes for currency transactions, a CTR documents specific transactions over a threshold amount, ensuring compliance with reporting requirements.

- AML Policy Document: An AML Policy Document outlines the company's policies for preventing money laundering, similar to how the Independent Review Form ensures that these policies are implemented and understood by employees.

- Due Diligence Checklist: Like the Independent Review, a Due Diligence Checklist ensures that proper procedures are followed when onboarding new customers to mitigate risks associated with money laundering.

- Compliance History Record: A Compliance History Record tracks a business's compliance activities, similar to the Independent Review Form which keeps a record of the independent review process and findings over time.

Dos and Don'ts

Things You Should Do When Filling Out the Independent Review Form:

- Complete all parts, questions, blanks, and fields of the form.

- Ensure that the reviewer is knowledgeable about AML requirements.

- Verify the compliance officer’s responsibilities are clearly understood.

- Include a valid government-issued photo I.D. for required transactions.

- Maintain a record of the Independent Review Form for at least 5 years.

Things You Shouldn't Do When Filling Out the Independent Review Form:

- Do not conduct the Independent Review yourself if you are the Compliance Officer.

- Do not leave any sections of the form incomplete.

- Avoid using the last blank Independent Review Form; make copies instead.

- Don't forget to provide addresses for all other locations if applicable.

- Never overlook the importance of employee training regarding compliance.

Misconceptions

Misconceptions about the Independent Review form may lead to confusion regarding compliance requirements. The following lists eight common misconceptions and clarifies each:

- Independent Review is optional. This is false. An Independent Review of an MSB is required by Federal AML Regulations to ensure compliance with anti-money laundering laws.

- The Compliance Officer can conduct the Independent Review. This is incorrect. The Independent Review must be conducted by someone other than the Compliance Officer or anyone reporting to them to maintain objectivity.

- Only a MoneyGram representative can perform the Independent Review. This is misleading. The review should be conducted by a qualified individual who is knowledgeable about AML requirements, but not affiliated with MoneyGram.

- Completed Independent Review Forms do not need to be stored. This is untrue. The completed forms must be retained with compliance documents for at least 5 years as part of record-keeping requirements.

- Any form can be substituted for the Independent Review Form. This is incorrect. The designated Independent Review Form provided should be used to ensure all necessary information is captured.

- A single review suffices indefinitely. This is false. The frequency of Independent Reviews should be determined as part of the Compliance Program, and they should occur regularly, as established with MoneyGram's approval.

- Any employee can be the Independent Reviewer. This is misleading. The Independent Reviewer must possess knowledge of AML requirements, and cannot be an employee connected to compliance oversight.

- It’s acceptable to use the last blank Independent Review Form. This is untrue. Businesses should always maintain extra copies to ensure continuity in the review process and compliance efforts.

Being aware of these misconceptions can help ensure that businesses comply appropriately with their AML obligations.

Key takeaways

Here are some important points to remember when filling out and using the Independent Review Form:

- Independent Review Requirement: An Independent Review is a mandatory step for your AML Compliance Program. This review must be conducted by a knowledgeable party who is not your Compliance Officer or anyone reporting to them.

- Documentation Storage: After the Independent Review Form is completed and signed, store it with your compliance documents for at least five years. Ensure you also make extra copies of the blank form to have on hand.

- Completeness is Key: Fill out all parts, questions, blanks, and fields of the form. Missing information can lead to compliance issues or delays in your review process.

- Consider All Locations: If your business operates multiple locations, provide addresses for each on the form. The reviewer needs to assess risks associated with all of them.

- Employee Training Documentation: Ensure all employee training related to AML compliance is well documented. The training records must be kept for a minimum of five years.

Browse Other Templates

Tractor Inspection Checklist - Completing the checklist promotes a culture of safety and accountability among operators.

Ucc Transcripts - Include your student ID or Social Security number for identification purposes.