Fill Out Your Inventory Tax 50 246 Form

The Inventory Tax 50-246 form, officially known as the Dealer’s Motor Vehicle Inventory Tax Statement, is a crucial document for motor vehicle dealers in Texas. This form must be submitted each month to report sales and calculate the inventory tax owed on motor vehicles sold in the previous month. Dealers are required to file a separate form for each business location. Accompanying this submission is a payment equivalent to the unit property tax assessed on these vehicles. The form also includes an election option for eligible dealers who wish to file renditions under a different tax code, allowing for potential alternative reporting, provided specific criteria are met. Information captured in the form includes the dealer's details, vehicle sale data, and unit property tax calculations. Timely filing is essential, with deadlines set for the 10th of each month to avoid penalties. Non-compliance can result in fines, including a minimum penalty of $500 per month for late submissions. The form must be filed directly with the county tax assessor-collector and the appraisal district, not the Texas Comptroller of Public Accounts. Understanding the nuances of this reporting requirement is vital for dealers to avoid unnecessary penalties and ensure compliance with state tax regulations.

Inventory Tax 50 246 Example

Texas Comptroller of Public Accounts |

Form |

|

|

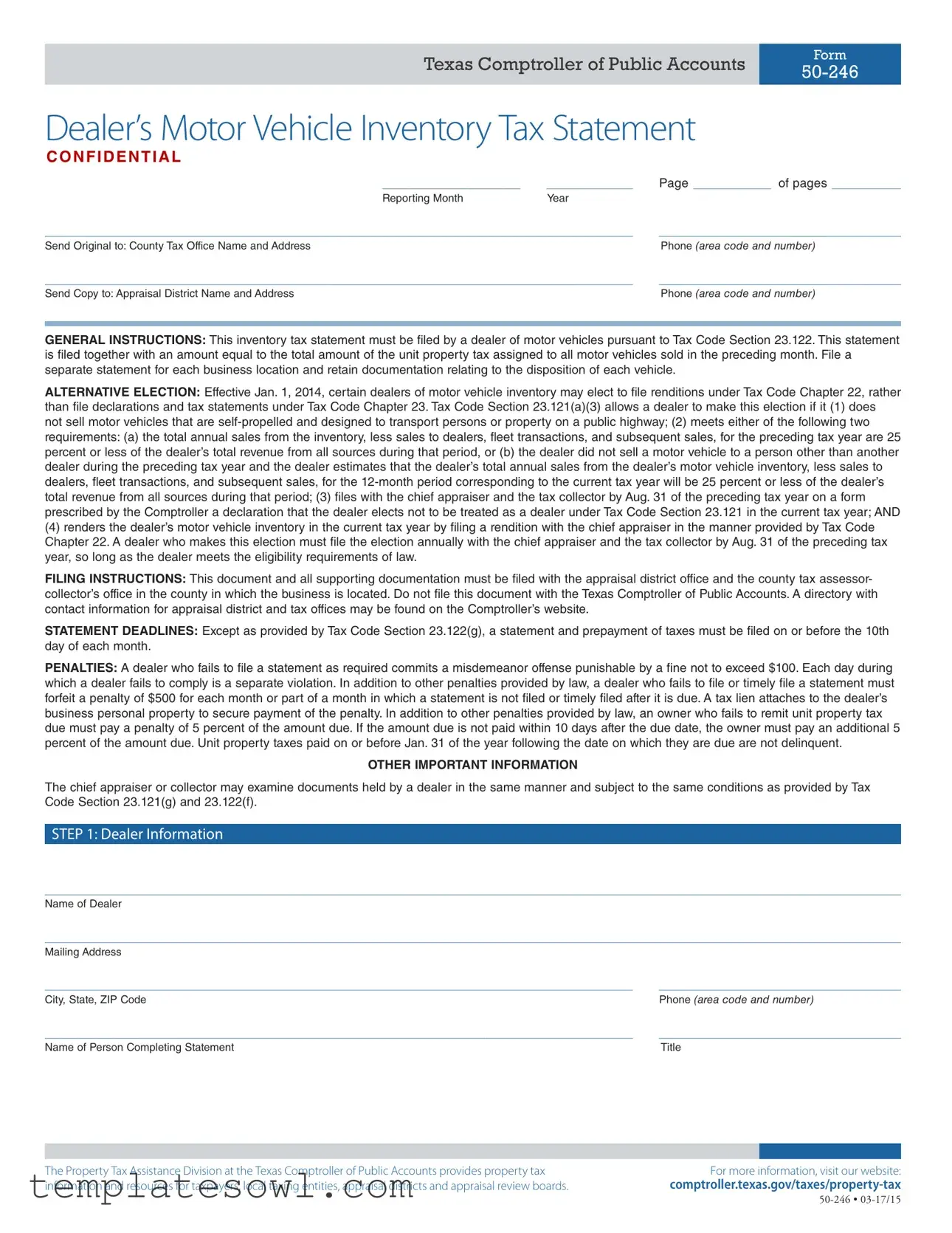

Dealer’s Motor Vehicle Inventory Tax Statement

CONFIDENT IAL

________________ |

__________ |

Page _________ of pages ________ |

Reporting Month |

Year |

|

____________________________________________________________________ |

____________________________ |

|

Send Original to: County Tax Office Name and Address |

|

Phone (area code and number) |

____________________________________________________________________ |

____________________________ |

|

Send Copy to: Appraisal District Name and Address |

|

Phone (area code and number) |

GENERAL INSTRUCTIONS: This inventory tax statement must be filed by a dealer of motor vehicles pursuant to Tax Code Section 23.122. This statement is filed together with an amount equal to the total amount of the unit property tax assigned to all motor vehicles sold in the preceding month. File a separate statement for each business location and retain documentation relating to the disposition of each vehicle.

ALTERNATIVE ELECTION: Effective Jan. 1, 2014, certain dealers of motor vehicle inventory may elect to file renditions under Tax Code Chapter 22, rather than file declarations and tax statements under Tax Code Chapter 23. Tax Code Section 23.121(a)(3) allows a dealer to make this election if it (1) does not sell motor vehicles that are

(4)renders the dealer’s motor vehicle inventory in the current tax year by filing a rendition with the chief appraiser in the manner provided by Tax Code Chapter 22. A dealer who makes this election must file the election annually with the chief appraiser and the tax collector by Aug. 31 of the preceding tax year, so long as the dealer meets the eligibility requirements of law.

FILING INSTRUCTIONS: This document and all supporting documentation must be filed with the appraisal district office and the county tax assessor- collector’s office in the county in which the business is located. Do not file this document with the Texas Comptroller of Public Accounts. A directory with contact information for appraisal district and tax offices may be found on the Comptroller’s website.

STATEMENT DEADLINES: Except as provided by Tax Code Section 23.122(g), a statement and prepayment of taxes must be filed on or before the 10th day of each month.

PENALTIES: A dealer who fails to file a statement as required commits a misdemeanor offense punishable by a fine not to exceed $100. Each day during which a dealer fails to comply is a separate violation. In addition to other penalties provided by law, a dealer who fails to file or timely file a statement must forfeit a penalty of $500 for each month or part of a month in which a statement is not filed or timely filed after it is due. A tax lien attaches to the dealer’s business personal property to secure payment of the penalty. In addition to other penalties provided by law, an owner who fails to remit unit property tax due must pay a penalty of 5 percent of the amount due. If the amount due is not paid within 10 days after the due date, the owner must pay an additional 5 percent of the amount due. Unit property taxes paid on or before Jan. 31 of the year following the date on which they are due are not delinquent.

OTHER IMPORTANT INFORMATION

The chief appraiser or collector may examine documents held by a dealer in the same manner and subject to the same conditions as provided by Tax Code Section 23.121(g) and 23.122(f).

STEP 1: Dealer Information

___________________________________________________________________________________________________

Name of Dealer

___________________________________________________________________________________________________

Mailing Address

____________________________________________________________________ |

____________________________ |

City, State, ZIP Code |

Phone (area code and number) |

____________________________________________________________________ |

____________________________ |

Name of Person Completing Statement |

Title |

The Property Tax Assistance Division at the Texas Comptroller of Public Accounts provides property tax |

For more information, visit our website: |

information and resources for taxpayers, local taxing entities, appraisal districts and appraisal review boards. |

Texas Comptroller of Public Accounts |

Form |

|

|

STEP 2: Business’ Name and Physical Address of Business Location

Provide the appraisal district account number if available or attach tax bill or copy of appraisal or tax office correspondence concerning your account.

___________________________________________________________________________________________________

Name of Business

___________________________________________________________________________________________________

Address, City, State, ZIP Code

____________________________________________________________________ |

____________________________ |

Account Number |

Business Start Date, if Not in Business on Jan. 1 |

____________________________________________________________________ |

|

General Distinguishing Number (GDN) |

|

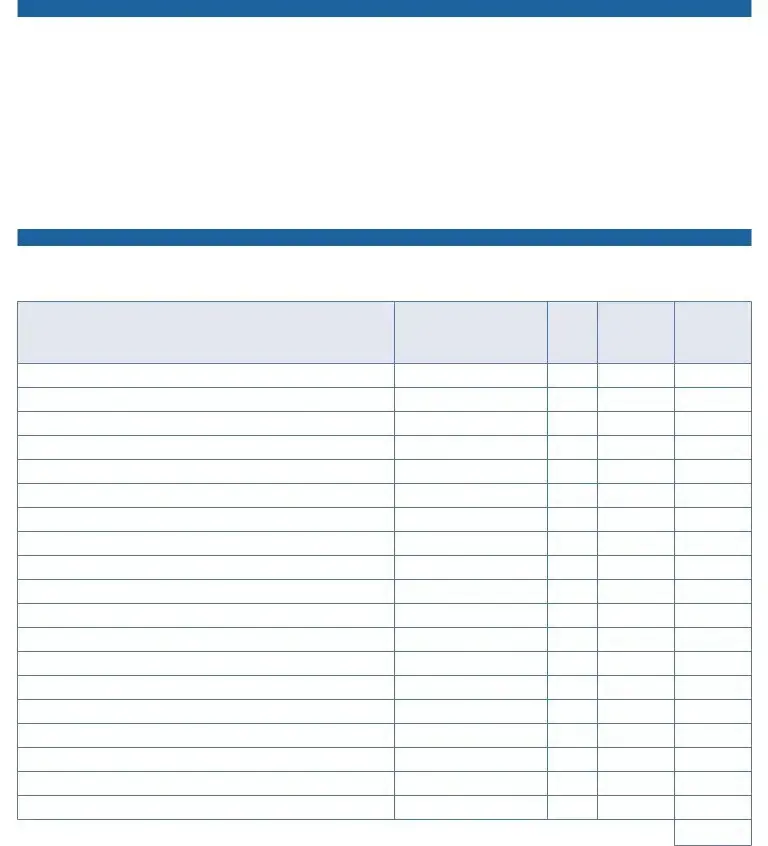

STEP 3: Vehicle Inventory Information

Provide the following information about each motor vehicle sale during the reporting month. Continue on additional sheets if necessary. In lieu of filling out the information in this step, you may attach separate documentation setting forth the information required. All such information must be separately identified in a manner that conforms to the column headers used in the table below. See last page for additional instructions and footnotes.

Description of Vehicle Sold

Date of |

Model |

|

Vehicle |

Sale |

Year |

Make |

Identification Number |

|

|

|

|

Purchaser’s

Name

Type of

Sale1

Sales Price2

Unit Property

Tax3

Total Unit Property Tax4

________________________________________________

Unit Property Tax Factor

For more information, visit our website: |

Page 2 |

|

|

Texas Comptroller of Public Accounts |

Form |

|

|

STEP 4: Total Units Sold and Total Sales

Number of units sold for reporting month:

______________________ |

______________________ |

______________________ |

_____________________ |

|||

Motor Vehicle Inventory |

Fleet Transactions |

Dealer Sales |

|

Subsequent Sales |

||

Sales amounts for reporting month: |

|

|

|

|

||

$_____________________ |

$_____________________ |

$_____________________ |

$ ____________________ |

|||

Motor Vehicle Inventory |

Fleet Transactions |

Dealer Sales |

|

Subsequent Sales |

||

|

|

|

|

|

|

|

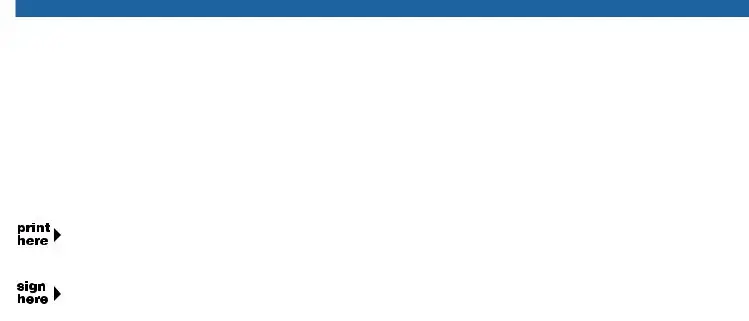

STEP 5: Signature and Date |

|

|

|

|

||

Signature required on last page only. |

|

|

|

|

||

|

________________________________ |

|||||

|

|

__________________________________________________________ |

||||

|

||||||

|

|

Print Name |

|

|

Title |

|

|

________________________________ |

|||||

|

|

_________________________________________________________ |

||||

|

||||||

|

|

Authorized Signature |

|

|

Date |

|

If you make a false statement on this report, you could be found guilty of a Class A misdemeanor or a state jail felony under Penal Code Section 37.10

For more information, visit our website: |

Page 3 |

|

|

Texas Comptroller of Public Accounts |

Form |

|

|

Additional Instructions

Step 3: Information on each vehicle sold during the reporting month. Complete the information on each motor vehicle sold, including the date of sale, model year, model make, vehicle identification number, purchaser’s name, type of sale, sales price and unit property tax. The footnotes include:

1Type of Sale: Place one of the following codes by each sale reported:

MV – motor vehicle inventory – sales of motor vehi- cles. A motor vehicle is a fully

FL – fleet transactions – motor vehicles included in the sale of five or more motor vehicles from inventory to the same person within one calendar year.

DL – dealer sales – sales of vehicles to another Texas dealer or dealer who is legally recognized in another state as a motor vehicle dealer.

SS – subsequent sales –

2Sales Price: Total amount of money paid or to be paid for the purchase of a motor vehicle as set forth as sales price in the form entitled Application for Texas Certificate of Title promulgated by the Texas Department of Motor Vehicles. In a transaction that does not involve the use of that form, the term means an amount of money that is equivalent, or substantially equivalent, to the amount that would appear as sales price on the Application for Texas Certificate of Title if that form were involved.

3Unit Property Tax: To compute, multiply the sales price by the unit property tax factor. Contact either the county tax

4Total unit property tax for reporting month: Enter the total amount of unit property tax from the “Total for this page only” box on previous page(s). This is the total amount of unit property tax that will be submitted with the statement to the collector.

For more information, visit our website: |

Page 4 |

|

|

Form Characteristics

| Fact Name | Details |

|---|---|

| Purpose of Form | This form is used by motor vehicle dealers in Texas to report monthly inventory taxes. |

| Governing Law | Tax Code Section 23.122 mandates the filing of this form. |

| Filing Frequency | Dealers must file this statement by the 10th of each month. |

| Penalties for Non-compliance | A dealer can incur fines up to $1,100 if they fail to file in a timely manner. |

| Alternative Filing Option | Dealers may choose an alternative method under Tax Code Chapter 22 effective January 1, 2014. |

| Sales Reporting Requirement | This form requires details about all motor vehicle sales for the reporting month. |

| Documentation Retention | Dealers must keep records related to the disposition of each vehicle sold. |

| Tax Lien Risks | A tax lien can attach to a dealer's business property for unpaid penalties. |

Guidelines on Utilizing Inventory Tax 50 246

Completing the Inventory Tax 50-246 form requires careful attention to detail to ensure that all the necessary information is accurately provided. This form must be submitted along with the corresponding tax amount by the specified filing deadlines. Here are the straightforward steps to follow to fill out the Inventory Tax 50-246 form correctly.

- Dealer Information: Fill in your name, mailing address, city, state, ZIP code, and phone number. Include the name and title of the person completing the statement.

- Business Information: Enter the name and physical address of your business location. If available, provide the appraisal district account number. Also, include your business start date if you were not operational on January 1st.

- Vehicle Inventory Information: List information for each motor vehicle sold during the reporting month. Include details such as the vehicle's description, sale date, model year, make, identification number, purchaser's name, type of sale, sales price, and unit property tax. If space is limited, you may attach separate documentation that conforms to the required format.

- Total Units Sold and Total Sales: Record the number of units sold for the reporting month, separating them into categories such as motor vehicle inventory, fleet transactions, dealer sales, and subsequent sales. Next, enter the total sales amounts for each category.

- Signature and Date: Sign and date the form on the last page. Ensure the name and title are printed legibly.

After completing the form, ensure that you have all necessary documentation ready for submission. It’s important to file the original with the county tax office and send a copy to the appraisal district. Make sure to check the deadlines to avoid penalties. If you have questions while filling out the form, consider reaching out to the appropriate tax office or appraisal district for assistance.

What You Should Know About This Form

What is the purpose of the Inventory Tax Form 50-246?

The Inventory Tax Form 50-246 is used by motor vehicle dealers in Texas to report and pay property taxes on their inventory of motor vehicles. This form must be filed monthly, detailing the motor vehicles sold during the previous month, to comply with Texas tax laws.

Who is required to file Form 50-246?

Any dealer selling motor vehicles in Texas must file Form 50-246. This includes those who maintain an inventory of vehicles that are sold either to consumers, other dealers, or as fleet transactions. A separate form must be filed for each business location operated by the dealer.

What are the deadlines for filing this form?

Dealers must file their Inventory Tax Form 50-246 and the corresponding payment by the 10th day of each month. This ensures that the report and payment for the previous month’s vehicle sales are submitted in a timely manner.

What happens if a dealer fails to file the form on time?

Failure to file the form on time can result in various penalties. A dealer might face a misdemeanor offense and a fine up to $100. Additionally, the dealer incurs a $500 penalty for each month that the statement is late, alongside a potential tax lien on their business property.

Can a dealer choose not to file Form 50-246?

Yes, under certain conditions, a dealer may elect to file under Tax Code Chapter 22 instead of using Form 50-246. This option is available for dealers who meet specific criteria related to their sales volume and inventory type. They must file a declaration by August 31 of the preceding tax year to make this election.

What information is required when completing Form 50-246?

Dealers must provide detailed information about each motor vehicle sold during the reporting month. This includes the date of sale, model year, make of the vehicle, identification number, purchaser’s name, sales price, and associated unit property tax. Supporting documentation must accompany the form if needed.

Where should the completed form and payments be submitted?

The completed Form 50-246 and all supporting documents must be filed with the appraisal district office and the county tax assessor-collector’s office for the county where the business operates. It is crucial not to send these documents to the Texas Comptroller of Public Accounts.

What is the potential penalty for inaccurate reporting on Form 50-246?

If a dealer submits false information on the form, they could face serious legal consequences. This could include being charged with a Class A misdemeanor or even a state jail felony, highlighting the importance of accurate reporting.

Common mistakes

Completing the Inventory Tax Form 50-246, the Dealer’s Motor Vehicle Inventory Tax Statement, can be a straightforward process with proper attention. However, mistakes can easily occur. One common error is failing to report all motor vehicle sales for the month. Dealers might overlook a vehicle sale or miscategorize it, leading to an incomplete reporting of sales figures. Accurate documentation of each motor vehicle sold is crucial, and each detail matters.

Another mistake frequently observed involves not filing the form with the appropriate offices. Dealers must send the original to the County Tax Office and a copy to the Appraisal District. Neglecting this step can result in penalties that could have been easily avoided. Filing with the wrong office delays processing and creates confusion, so clarity on submission directives is essential.

Inaccuracies in data entry, particularly in vehicle identification numbers or sales prices, can also cause significant issues. Double-checking these details helps prevent needless complications. Incorrect figures can lead to discrepancies during audits, and this may ultimately require extensive corrections and explanations down the line.

Additionally, some dealers misinterpret the filing deadline. The form must be submitted on or before the 10th day of every month. Missing this deadline could lead to various penalties, including fines or loss of good standing with tax authorities. Setting reminders and keeping a calendar of deadlines can be a beneficial strategy.

Another pitfall lies in the misunderstanding of the unit property tax calculation. Dealers may inadvertently use outdated or incorrect unit property tax factors. It is crucial to verify these figures with the county tax assessor-collector or the appraisal district to ensure compliance with current regulations. This simple step can prevent costly mistakes.

Lastly, some dealers might not retain proper documentation related to the sale of vehicles. All relevant records must be kept for audit purposes and future reference. Without these, it may be challenging to justify claims made in the submission, leading to potential disputes or penalties. Organized record-keeping can ease the stress of compliance and facilitate smoother processing of the form.

Documents used along the form

When filing the Inventory Tax 50-246 form in Texas, there are several other forms and documents that may be necessary to accompany the submission. Each of these documents plays a vital role in ensuring compliance with tax regulations and maintaining accurate records of vehicle sales and inventory management. Below is a list of commonly used forms and documents.

- Form 50-175: Texas Property Tax Exemption Application - This document is used by entities seeking an exemption from property taxes. Dealers may need this if they qualify under specific exemption categories related to motor vehicle inventory.

- Form 50-153: Business Personal Property Rendition - Dealers may use this form for reporting their business personal property to the appraisal district. It helps in assessing the value of inventory not directly covered by the Inventory Tax 50-246.

- Sales Tax Permit - This permit allows dealers to collect sales tax on vehicle sales. It's crucial for ensuring that all sales taxes are properly accounted for and remitted to the state.

- Texas Motor Vehicle Dealer's License - Holding this license is essential for any entity wishing to engage in the sale of motor vehicles in Texas. It attests to the business's legality and compliance with state regulations.

- Monthly Sales Reports - These reports provide a detailed account of all vehicle sales made during the month. They are useful for tracking performance and ensuring accurate reporting on the Inventory Tax form.

- Vehicle Title Documentation - This paperwork is fundamental to verifying ownership and sales eligibility of the vehicles being sold. It must be maintained and accessible for each vehicle in inventory.

- Federal Employer Identification Number (EIN) - An EIN is required for tax reporting purposes and helps in managing federal taxes associated with the dealer's business income.

- Insurance Documentation - Proof of insurance is necessary to protect the dealer’s inventory from damage or loss, fulfilling legal and operational responsibilities.

- Appraisal District Correspondence - Any communications with the local appraisal district regarding vehicle assessments or questions should be documented and retained.

- Vehicle Inventory List - Maintaining a current list of all vehicles in inventory helps streamline the reporting process and provides crucial data for potential audits.

Each of these forms and documents supports a comprehensive approach to vehicle inventory taxation. By ensuring the correct papers are prepared and submitted alongside the Inventory Tax 50-246 form, dealerships can minimize potential issues with compliance and streamline their business operations.

Similar forms

The Inventory Tax 50-246 form shares similarities with several other tax-related documents. Here are six forms that are comparable, along with a brief explanation of each:

- Sales Tax Permit Application - Dealers must complete this application to collect sales tax on vehicle sales, much like the Inventory Tax 50-246 requires reporting sales and paying taxes on motor vehicle inventory.

- Franchise Tax Report - Similar in that both require businesses to report financial activity, the Franchise Tax Report serves to assess taxes based on the revenue generated by businesses in Texas.

- Property Tax Rendition Form - Like the 50-246 form, this document reports a business's property holdings to the local appraisal district for tax assessment. Both forms ensure compliance with state tax laws.

- Business Personal Property Declaration - Businesses use this to declare personal property and provide valuation for tax purposes, similar to how the Inventory Tax 50-246 details motor vehicle inventory.

- Owner’s Affidavit for Personal Property - This affidavit serves to affirm ownership and valuation of personal property, much like the declaration of ownership and valuation required on the Inventory Tax 50-246 form.

- Monthly Tax Return for Motor Vehicle Dealers - Dealers submit this return to report their monthly sales, similar to the frequency and nature of sales reporting on the Inventory Tax 50-246.

Dos and Don'ts

Filling out the Inventory Tax 50-246 form requires careful attention to detail to ensure compliance with Texas tax laws. The following list outlines essential practices to follow and avoid when completing this form.

- Do verify your dealer information: Ensure that the name, mailing address, and contact details are accurate.

- Do attach supporting documentation: If applicable, provide any necessary paperwork regarding vehicle sales or tax information.

- Do submit on time: Remember that statements and tax prepayments are due by the 10th of each month.

- Do maintain copies: Keep copies of all submitted documents for your records and future reference.

- Don't leave sections blank: Every required field must be filled out to prevent delays or penalties.

- Don't submit late: Failing to file on time could result in fines and complications with your tax status.

- Don't forget to sign the form: The signature is essential for validation and completeness.

- Don't misrepresent information: Accurate reporting is crucial, as false statements may lead to legal repercussions.

Misconceptions

- Misconception: Only large dealerships need to file Form 50-246.

- Misconception: The Inventory Tax is a one-time fee.

- Misconception: Filing Form 50-246 is optional.

- Misconception: Only new vehicles are subject to this tax.

- Misconception: Late filings don't carry significant consequences.

- Misconception: Dealers can file the form anytime during the month.

- Misconception: There’s no need to keep records once the form is filed.

- Misconception: Once the election under Tax Code Chapter 22 is filed, it does not need to be resubmitted.

- Misconception: The form can be filed with the Texas Comptroller of Public Accounts.

This form must be submitted by all motor vehicle dealers, regardless of the size of their operation.

The Inventory Tax must be filed and paid monthly, on or before the 10th day of each month.

Filing this form is mandatory for dealers of motor vehicles as per Texas Tax Code Section 23.122.

All motor vehicles sold by dealers, including used vehicles, are included in this inventory tax.

Filing late can lead to severe penalties, including fines of up to $500 per month.

The filing deadline is strict; it must be submitted by the 10th day of each month.

Dealers must retain documentation related to the disposition of each vehicle sold.

Dealers who make this election must file it annually as long as the eligibility criteria are met.

This form must be submitted to the county tax assessor-collector and the appraisal district office, not the Comptroller.

Key takeaways

The Inventory Tax 50-246 form is essential for motor vehicle dealers in Texas. Here are key takeaways to help you navigate the filing process effectively:

- Required Filings: Dealers must complete this form to report motor vehicle inventory taxes due each month.

- Separate Statements: If operating at multiple business locations, each site requires a separate Inventory Tax 50-246 form.

- Filing Deadlines: Submit the statement and payment by the 10th day of every month to avoid penalties.

- Penalties for Noncompliance: Failing to file on time can result in fines, including a $500 penalty for each month late.

- Alternative Filing Option: Certain dealers may choose to file under Chapter 22 of the Tax Code instead, provided they meet specific qualifications.

- Document Requirements: Keep detailed records of vehicle sales and submit relevant documentation along with the form.

- Unit Property Tax Factor: Calculate the tax owed by multiplying the sales price by the unit property tax factor provided by the appraisal district.

- Signature Requirement: Ensure that the form is signed by an authorized representative before submission.

- Contact Information: Reference the Texas Comptroller’s website for directory information on appraisal districts and tax offices.

- Potential for Audits: Be aware that appraisal district officials may examine documents from your records to verify compliance.

Browse Other Templates

What Does Equal Housing Opportunity Mean - A deposit is required and explained clearly within the form.

Irp Ohio - Fill in the registrant’s Zip Code accurately for correspondence purposes.

Parents Plus Loan Application - Eligibility for a Parent Plus Loan is based on a credit check by the Department of Education.