Fill Out Your Lincoln Request Distribution Form

The Lincoln Request Distribution form plays a crucial role in helping individuals manage their retirement assets effectively. It is primarily designed to facilitate the process of transferring funds from one retirement account to another company. Users can leverage this form for standard distribution requests, ensuring their funds are managed according to regulatory guidelines and minimizing potential tax liabilities. Important distribution methods highlighted include rollovers, contract exchanges, plan-to-plan transfers, and permissive service credit transfers, each with specific criteria and requirements. However, it is critical to note that this form should not be used for hardship withdrawals, required minimum distributions, or death claims, among other exceptions. By understanding the nuances of the Lincoln Request Distribution form, individuals can secure their financial futures while making informed decisions about their retirement funds. For those needing assistance, resources and support are readily available through the Lincoln Customer Contact Center and online platforms.

Lincoln Request Distribution Example

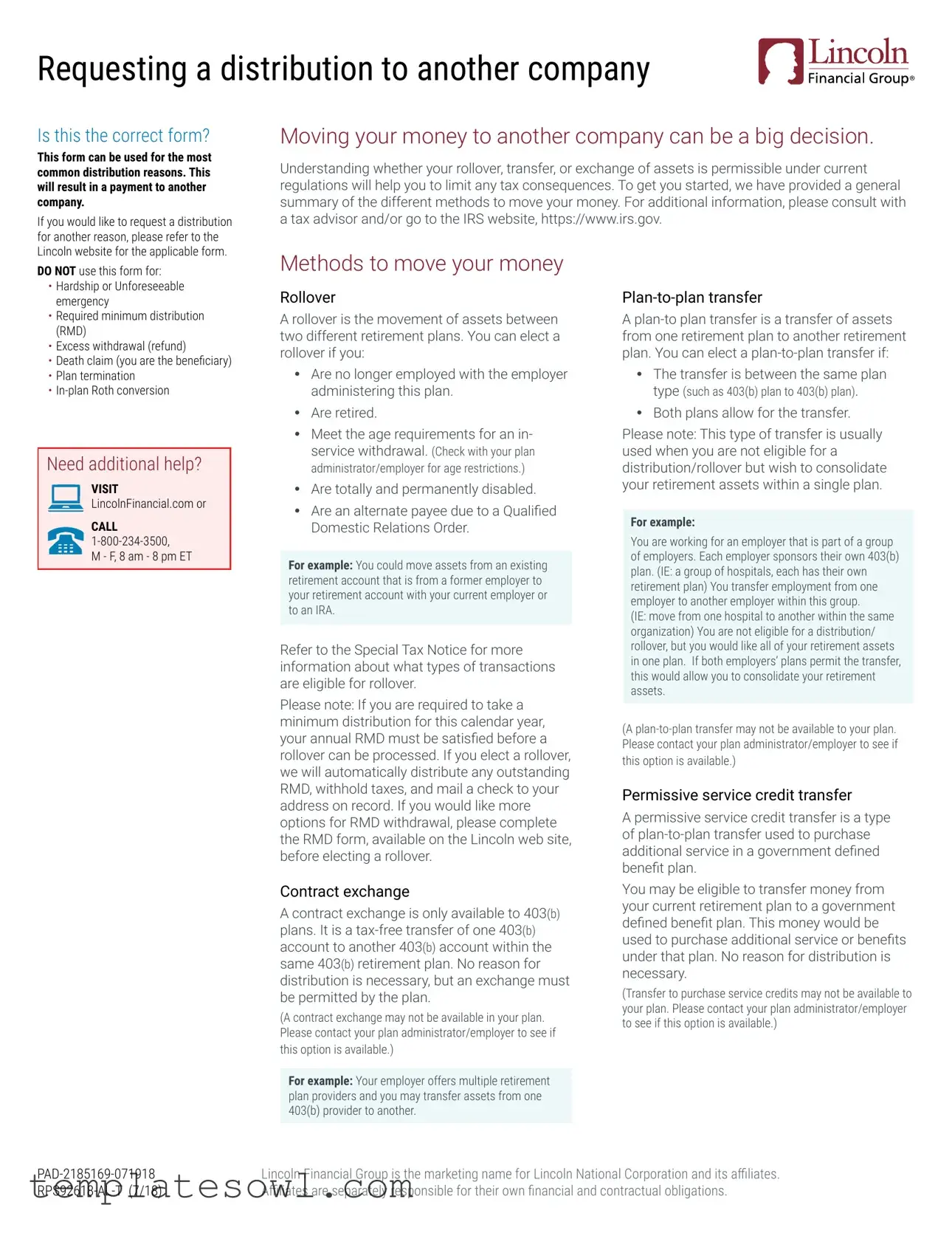

Requesting a distribution to another company

Is this the correct form?

This form can be used for the most common distribution reasons. This will result in a payment to another company.

If you would like to request a distribution for another reason, please refer to the

Moving your money to another company can be a big decision.

Understanding whether your rollover, transfer, or exchange of assets is permissible under current regulations will help you to limit any tax consequences. To get you started, we have provided a general summary of the different methods to move your money. For additional information, please consult with a tax advisor and/or go to the IRS website, https://www.irs.gov.

Lincoln website for the applicable form. DO NOT use this form for:

•Hardship or Unforeseeable emergency

•Required minimum distribution (RMD)

•Excess withdrawal (refund)

•Death claim (you are the beneficiary)

•Plan termination

•

Need additional help?

VISIT

LincolnFinancial.com or

CALL

M - F, 8 am - 8 pm ET

Methods to move your money

Rollover

A rollover is the movement of assets between two different retirement plans. You can elect a rollover if you:

yy Are no longer employed with the employer administering this plan.

yy Are retired.

yy Meet the age requirements for an in- service withdrawal. (Check with your plan administrator/employer for age restrictions.)

yy Are totally and permanently disabled.

yy Are an alternate payee due to a Qualified Domestic Relations Order.

For example: You could move assets from an existing retirement account that is from a former employer to your retirement account with your current employer or to an IRA.

Refer to the Special Tax Notice for more information about what types of transactions are eligible for rollover.

Please note: If you are required to take a minimum distribution for this calendar year, your annual RMD must be satisfied before a rollover can be processed. If you elect a rollover, we will automatically distribute any outstanding RMD, withhold taxes, and mail a check to your address on record. If you would like more options for RMD withdrawal, please complete the RMD form, available on the Lincoln web site, before electing a rollover.

Contract exchange

A contract exchange is only available to 403(b) plans. It is a

(A contract exchange may not be available in your plan. Please contact your plan administrator/employer to see if

this option is available.)

For example: Your employer offers multiple retirement plan providers and you may transfer assets from one 403(b) provider to another.

A

yy The transfer is between the same plan type (such as 403(b) plan to 403(b) plan).

yy Both plans allow for the transfer.

Please note: This type of transfer is usually used when you are not eligible for a distribution/rollover but wish to consolidate your retirement assets within a single plan.

For example:

You are working for an employer that is part of a group of employers. Each employer sponsors their own 403(b) plan. (IE: a group of hospitals, each has their own retirement plan) You transfer employment from one employer to another employer within this group.

(IE: move from one hospital to another within the same organization) You are not eligible for a distribution/ rollover, but you would like all of your retirement assets in one plan. If both employers’ plans permit the transfer, this would allow you to consolidate your retirement assets.

(A

this option is available.)

Permissive service credit transfer

A permissive service credit transfer is a type of

You may be eligible to transfer money from your current retirement plan to a government defined benefit plan. This money would be used to purchase additional service or benefits under that plan. No reason for distribution is necessary.

(Transfer to purchase service credits may not be available to your plan. Please contact your plan administrator/employer to see if this option is available.)

Lincoln Financial Group is the marketing name for Lincoln National Corporation and its affiliates. |

|

Affiliates are separately responsible for their own financial and contractual obligations. |

This page is intentionally left blank.

Request a distribution to another company

If you have questions or need assistance completing this form, call the Lincoln Customer Contact Center at

Is this the correct form?

This form can be used for the most common distribution reasons. This will result in a payment to another company.

If you would like to request a distribution for another reason, please refer to the Lincoln website for the applicable form.

DO NOT use this form for:

• Hardship or Unforeseeable |

emergency |

• Required minimum distribution |

(RMD) |

• Excess withdrawal (refund) |

1Tell us about yourself.

Name (first, MI, last, suffix) |

|

|

|

|

|

SSN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

- |

|

- |

|

|

|

|

|

Street address |

|

|

|

|

|

Plan ID (refer to your statement) |

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

State |

Zip |

|

Mobile |

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

- |

|

- |

|

|

|

|||

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

Phone |

|

|

|

|

|

|

|

||

• Death claim (you are the beneficiary) |

• Plan termination |

• |

Marital status: Please provide your martial status in order to ensure timely

processing of your distribution.

Marital status

I do not have a living spouse. I have a living spouse.

Employment status (choose one)

I retired on (mm/dd/yyyy)

/

/

.

- |

- |

Date of birth (mm/dd/yyyy)

/ |

|

/ |

Restrictions may apply depending on your plan provisions. Please contact

your plan administrator/employer to discuss what options are available.

If you are totally and

permanently disabled:

permanently disabled:

A letter from the Social Security Administration is required.

A letter from the Social Security Administration is required.

For Qualified Domestic Relations Orders: A copy of the court order, divorce, or legal separation is required.

If you have Roth and/or after tax money, please verify that your receiving

company will accept your rollover.

When requesting a rollover of

for payment of federal and state income tax, if applicable, at the time you prepare your personal tax filing. You may wish to discuss your personal tax liability with a qualified tax advisor.

Receiving company information: If your receiving company information is incomplete or inaccurate, we will issue the check to the receiving company but mail it to your address. You will be responsible for mailing the check to the receiving company to complete the transaction.

I am no longer working for the employer that administers this plan as of

(mm/dd/yyyy) |

|

/ |

|

/ |

|

. |

I am currently employed with the employer that administers this plan. (Restrictions may apply.)  I am totally and permanently disabled.

I am totally and permanently disabled.

I am not an employee. (You are the alternate payee due to a Qualified Domestic Relations Order.)

2How should we move your funds to another company?

Please refer to “Requesting a distribution to another company” included with this form.

I would like to distribute my money in the form of a (choose one)

Rollover

If you have after tax contributions and you elect a rollover, Lincoln will automatically include your after tax contributions unless you tell us otherwise by checking this box: Do not include my after tax contributions in this rollover.

Contract exchange (Restrictions may apply.)

Permissive service credit transfer (Restrictions may apply.)

Type of receiving plan/account (choose one)

401(k) 403(b) 401(a) 457(b) governmental

Individual Retirement Account (IRA) (Traditional, SEP, SIMPLE, etc.)

Roth IRA  Defined benefit plan

Defined benefit plan

Provide information about the receiving company. |

|

|

Receiving company name (payable to) |

Account number |

|

|

|

|

|

|

|

Street address |

City, State, Zip |

|

|

|

|

|

|

|

Lincoln Financial Group is the marketing name for Lincoln National Corporation and its affiliates. |

|

|

Affiliates are separately responsible for their own financial and contractual obligations. |

Page 1 of 6 |

Request a distribution to another company

3How much should we send?

Amounts will be distributed from your available vested balance and may be limited to certain contribution types. The total amount you receive may be less than the amount requested, depending on your available balance and tax withholding.

Restrictions may apply to options (where noted) on this form depending on your plan.

Please contact your plan administrator/ employer to discuss what options are available.

Amount options (choose one)

Send 100% of my account balance to another If applicable, your distribution will automatically include the

company as described in Step 2. (Skip to Step 6.) Lincoln Secured Retirement IncomeSM investment option. This |

|||

|

|

|

may result in an excess withdrawal. An excess withdrawal may |

Send part of my account balance in the |

reduce your income base. Please let us know if you want to |

||

amount of $ |

|

to another |

exclude it from your distribution. |

|

|

||

company as |

|

|

I do not want to include the Secured Retirement IncomeSM |

described in Step 2 and leave the |

|||

remainder in my account. (Dollar amount must be |

option in my distribution. |

||

|

|||

provided. Skip to Step 6.) (Restrictions may apply.)

Direct Deposit: If your bank account information is illegible or incomplete,

Lincoln will issue a check and mail to your address on file.

Please note: We cannot direct deposit to reloadable bank cards.

If you direct deposit to a checking account: A voided

check or a verification of deposit from your financial institution is required.

check or a verification of deposit from your financial institution is required.

If you direct deposit to a savings account: A verification of deposit from your financial institution is required.

The amount you receive:

The total amount you receive from this distribution will be reduced by the total amount of taxes withheld. Depending on your available balance, you may adjust your requested distribution amount to account for additional taxes that may be assessed as part of your tax liability.

Federal tax withholding election: If you do not provide a rate, or if you

provide a federal tax withholding rate that is less than 20%, we are still required to withhold the applicable minimum.

Please note: Your distribution may be subject to an additional 10% early distribution penalty tax. This penalty tax will be assessed when you file your tax returns as part of your tax liability and is not automatically included in your tax withholding for this distribution.

Send me a partial cash payment of

$and send the remainder of my account balance to another company as described in Step 2. (Dollar amount must be

provided. Continue to Step 4.)

4How would you like to receive your payment?

Only complete this section if you are receiving a partial cash payment.

I would like my payment to be sent as a (choose one)

Direct deposit to my personal bank account as described here:

Name as it appears on your account |

Bank transit/ABA number |

|

|

|

|

|

|

|

Financial institution |

Account number |

|

|

|

|

|

|

|

Type of account: Checking  Savings

Savings

Check, mailed to my address on file.

5How do taxes impact your partial cash payment?

Only complete this section if you are receiving a partial cash payment.

Lincoln will withhold taxes from your distribution at the rates detailed below and automatically send the withholding to the IRS on your behalf. Please refer to the Special Tax Notice for more information.

Taxes withheld from your distribution will include:

yy Federal tax (if applicable)

20% mandatory withholding applies to distributions that are eligible for rollover.

Indicate here if you would like to withhold federal taxes at a higher rate than the mandatory 20%:

Withhold federal taxes at the rate of (minimum 20%) |

|

%. |

|

yy State tax (if applicable) |

|

|

|

State tax is automatically calculated and based on your residence on file. |

|

||

Questions? Visit LincolnFinancial.com or call |

Page 2 of 6 |

||

Request a distribution to another company

Did you know?

If you move this year: Please update your address to receive your tax documents for use when you file your income taxes.

To update your address: If you are an active employee, contact your employer; if you are no longer employed, call Lincoln.

6Sign and date this form.

For New York residents only: Any person who knowingly and with intent to defraud any insurance company or other person files an application for insurance or statement of claim containing any materially false information, or conceals for the purpose of misleading, information concerning any fact material thereto, commits a fraudulent insurance act, which is a crime and shall also be subject to civil penalty not to exceed five thousand dollars and the stated value of the claim for each such violation.

By signing below, I certify that:

yy I have read and understand the Important Fraud Notice and Important Information sections on the last page of this form.

yy I have received the Special Tax Notice, and if applicable, I waive the required

yy I am responsible for meeting the federal tax law requirements to qualify for this distribution. yy My answers on this form and any documents I have attached are true and accurate.

yy If there are not enough funds in my retirement account for the amount requested, Lincoln will process the withdrawal from the amount available.

yy If applicable to this plan, I have received the Qualified Joint and Survivor Annuity (QJSA) notice; waive the 30 day review period and normal QJSA form of payment; and instead; elect to receive this distribution as detailed on this form.

Your signature |

Today’s date (mm/dd/yyyy) |

/

/

If spousal consent is required and if your plan administrator does not sign

here as a witness to your spouse’s signature, you must have a notary sign, seal, and date where noted to the right.

7Your spouse’s signature may be required.

In some instances, your spouse may be required to sign this form. Please call your plan administrator/ employer to determine if this is required for your plan. This section is not needed for distributions due to Qualified Domestic Relations Order.

By signing below, I certify that I am the spouse of the individual named above and that:

yy If applicable to this plan, I have received the QJSA notice, consent to my spouse’s election to waive the normal QJSA form of payment, and consent to my spouse’s election to an immediate distribution as detailed on this form.

Spouse’s signature (if required) |

|

|

|

|

|

|

|

Today’s date (mm/dd/yyyy) |

||||

|

|

|

|

|

|

|

|

|

/ |

|

/ |

|

|

|

|

|

|

|

|

|

|

|

|

||

Plan administrator’s signature or notary’s signature |

|

|

|

|

|

|

|

Today’s date (mm/dd/yyyy) |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

/ |

|

/ |

|

Notary seal |

Notary’s commission expires (mm/dd/yyyy) |

|||||||||||

|

|

|

/ |

|

/ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Continue to the next page for additional instructions. |

|

|

|

|

Questions? Visit LincolnFinancial.com or call |

Page 3 of 6 |

Request a distribution to another company

Did you remember to:

Print, sign and date this form?

Print, sign and date this form?

Attach any necessary documents?

Attach any necessary documents?

If faxing, include both the front and back of ALL pages of the form?

If faxing, include both the front and back of ALL pages of the form?

Questions?

VISIT

LincolnFinancial.com or

CALL

M - F, 8 am - 8 pm ET

Current, former, or

Your employer’s Human Resources department.

What you can expect:

yy Log in to your account at LincolnFinancial.com to verify when funds are removed from your retirement account.

yy For ACH deposits, it takes up to two business days to see your payment posted to your bank account once the funds have left your retirement account.

yy For checks, your payment will arrive depending on the United States Postal Service delivery schedule. This generally takes

Plan administrator/employer use only.

I authorize Lincoln to proceed with the elections made on this form.

Plan administrator’s name

Plan administrator’s signature |

Today’s date (mm/dd/yyyy) |

/

/

Continue to the next page for additional instructions.

Continue to the next page for additional instructions.

|

|

|

Questions? Visit LincolnFinancial.com or call |

Page 4 of 6 |

Request a distribution to another company

Participant information: If participant information is incomplete, Lincoln

will use the information currently on file.

Authorization: Lincoln will process this request based on TPA authorization only. Lincoln will not screen for plan administrator/ employer’s signature or QDRO orders.

TPA distribution fees are established at plan setup, deducted automatically at the time of withdrawal, and included in the aggregated monthly fee sent to the TPA. For recurring distribution payments, the fee will be assessed only for the initial withdrawal.

Plan administrator or TPA return all documents to:

•FAX

Lincoln Retirement Services Company, LLC

Lincoln Retirement Services Company, LLC

P.O. Box 7876

Fort Wayne, IN

•EXPRESS MAIL

Lincoln Retirement Services Company, LLC

1300 South Clinton St. Fort Wayne, IN

IMPORTANT INFORMATION

There are restrictions on the amount that can be withdrawn from the Lincoln Fixed Account/Lincoln Stable Value Account/ Lincoln Stable Value Separate Account in a

Lincoln Financial Group® affiliates, their distributors, and their respective employees, representatives, and/or insurance agents do not provide tax, accounting, or legal advice. Clients should consult their own independent advisor as to any tax, accounting or legal statements made herein. We recommend that you consult a tax advisor regarding the distribution rules as they pertain to your personal circumstances.

Third party administrator (TPA) use only.

Complete the following information:

yy If the employee is no longer working, provide the date of severance

|

(mm/dd/yyyy) |

|

/ |

|

/ |

|

|

. |

|

|

|

|

|

|

|

|

yy |

Is the employee 100% vested? |

Yes |

No |

|

|

|

||||||||||

|

If no, please provide the vested percentage: |

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|||||||||||||

|

|

|

%. |

|||||||||||||

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

%. |

|||||||||||||

yy |

If applicable, please provide the amount to separate into the alternate payee account for a Qualified |

|||||||||||||||

|

Domestic Relations Order (QDRO) |

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

. |

|

|

|

|

|

||||||

yy |

If applicable, please provide the QDRO fee $ |

|

|

|

|

|

|

|

||||||||

|

|

. |

|

|

|

|

||||||||||

This fee will be applied to the (choose one): |

Participant |

Alternate payee |

|||||

I authorize Lincoln to proceed with the elections made on this form. |

|||||||

TPA’s name |

|

|

Phone |

|

|

|

|

|

|

|

|

- |

|

- |

|

|

|

|

|

|

|||

TPA’s authorization code |

|

|

Contact name |

||||

IMPORTANT FRAUD NOTICE

Residents of all states except Alabama, Arkansas, Colorado, District of Columbia, Florida, Kentucky, Louisiana, Maine, Maryland, New Jersey, New Mexico, New York, Ohio, Oklahoma, Pennsylvania, Rhode Island, Tennessee, Vermont, Virginia and Washington, please note: Any person who knowingly, and with intent to defraud any insurance company or other person, files or submits an application or statement of claim containing any materially false or deceptive information, or conceals, for the purpose of misleading, information concerning any fact material thereto, commits a fraudulent insurance act, which is a crime and may subject such person to criminal and civil penalties.

For Arkansas, Colorado, Kentucky, Maine, New Mexico, Ohio, Rhode Island, Tennessee residents only: Any person who, knowingly and with intent to injure, defraud or deceive any insurance company or other person, files an application for insurance or statement of claim containing any materially false information or conceals, for the purpose of misleading, information concerning any fact material thereto commits a fraudulent insurance act, which is a crime and may subject such person to criminal and civil penalties, fines, imprisonment, or a denial of insurance benefits.

For Alabama and Louisiana residents only: Any person who knowingly presents a false or fraudulent claim for payment of a loss or benefit or who knowingly presents false information in an application for insurance is guilty of a crime and may be subject to restitution fines or confinement in prison, or any combination thereof.

For District of Columbia residents only: WARNING: It is a crime to provide false or misleading information to an insurer for the purpose of defrauding the insurer or any other person. Penalties include imprisonment and/or fines. In addition, an insurer may deny insurance benefits if false information materially related to a claim was provided by the applicant.

For Florida and New Jersey residents only: Any person who knowingly and with intent to injure, defraud, or deceive any insurer files a statement of claim or an application containing any false, incomplete, or misleading information is guilty of a felony of the third degree.

For Maryland residents only: Any person who knowingly or willfully presents a false or fraudulent claim for payment of a loss or benefit or who knowingly or willfully presents false information in an application for insurance is guilty of a crime and may be subject to fines and confinement in prison.

For Oklahoma and Pennsylvania residents only: Any person who knowingly and with intent to defraud any insurance company or other person files an application for insurance or statement of claim containing any materially false information or conceals for the purpose of misleading, information concerning any fact material thereto commits a fraudulent insurance act, which is a crime and subjects such person to criminal and civil penalties.

For Vermont residents only: Any person who knowingly presents a false statement in an application for insurance may be guilty of a criminal offense and subject to penalties under state law.

For Washington residents only: It is a crime to knowingly provide false, incomplete, or misleading information to an insurance company for the purpose of defrauding the company. Penalties include imprisonment, fines, and denial of insurance benefits.

|

|

|

Questions? Visit LincolnFinancial.com or call |

Page 5 of 6 |

This page is intentionally left blank.

Special tax notice regarding plan payment from

Your rollover options

You are receiving this notice because all or a portion of a payment you are receiving from an

This notice describes the rollover rules that apply to payments that are from a “designated Roth account” (an account for

Rules that apply to most payments from a plan are described in the “General Information About Rollovers” section. Special rules that only apply in certain circumstances are described in the “Special Rules and Options” section.

GENERAL INFORMATION ABOUT

ROLLOVERS

How can a rollover affect my taxes?

You will be taxed on a payment from a

Designated Roth account

If the payment from the Plan is not a qualified distribution and you do not do a rollover to a Roth IRA or a designated Roth account in an employer plan, you will be taxed on the earnings in the payment. If you are under age 59½, a 10% additional income tax on the early distributions will also apply to the earnings (unless an exception applies). However, if you do a rollover, you will not have to pay taxes currently on the earnings and you will not have to pay taxes later on payments that are qualified distributions.

If the payment from the Plan is a qualified distribution, you will not be taxed on any part of the payment even if you do not do a rollover. If you do a rollover, you will not be taxed on the amount you roll over and any earnings on the amount you roll over will not be taxed if paid later in a qualified distribution.

A qualified distribution from a designated Roth account in the Plan is a payment made after you are age 59½ (or after your death or disability) and after you have had a designated Roth account in the Plan for at least 5 years. In applying the

What types of retirement accounts and plans may accept my rollover?

You may roll over the payment to either an IRA (an individual retirement account or individual retirement annuity) or an employer plan (a tax- qualified plan, section 403(b) plan, or governmental section 457(b) plan) that will accept the rollover. The rules of the IRA or employer plan that holds the rollover will determine your investment options, fees, and rights to payment from the IRA or employer plan (for example, no spousal consent rules apply to IRAs and IRAs may not provide loans). Further, the amount rolled over will become subject to the tax rules that apply to the IRA or employer plan.

Designated Roth account

You may roll over the payment from a designated Roth account to either a Roth IRA (a Roth individual retirement account or Roth individual retirement annuity) or a designated Roth account in an employer plan (a

yy If you do a rollover to a Roth IRA, all of your Roth IRAs will be considered for purposes of determining whether you have satisfied the

for later Roth IRA payments that are not qualified distributions). yy Eligible rollover distributions from a Roth IRA can only be rolled

over to another Roth IRA.

How do I do a rollover?

There are two ways to do a rollover. You can either do a direct rollover or a

If you do a direct rollover, the Plan will make the payment directly to your IRA or an employer plan. You should contact the IRA sponsor or

Lincoln Financial Group is the marketing name for Lincoln National Corporation and its affiliates. |

|

|

RPS33691 (10/18) |

Affiliates are separately responsible for their own financial and contractual obligations. |

Page 1 of 7 |

Special tax notice regarding plan payment from

the administrator of the employer plan for information on how to do a direct rollover.

If you do not do a direct rollover, you may still do a rollover by making a deposit into an IRA or eligible employer plan that will accept it. Generally, you will have 60 days after you receive the payment to make the deposit. If you do not do a direct rollover, the Plan is required to withhold 20% of the payment for federal income taxes (up to the amount of cash and property received other than employer stock). This means that, in order to roll over the entire payment in a

yy Corrective distributions of contributions that exceed tax law limitations

yy Loans treated as deemed distributions (for example, loans in default due to missed payments before your employment ends)

yy Cost of life insurance paid by the Plan

yy Payments of certain automatic enrollment contributions requested to be withdrawn within 90 days of the first contribution

yy Amounts treated as distributed because of a prohibited allocation of S corporation stock under an ESOP (also, there will generally be adverse tax consequences if you roll over a distribution of S corporation stock to an IRA)

The Plan administrator or the payor can tell you what portion of a payment is eligible for rollover.

Designated Roth account

If you do a direct rollover, the Plan will make the payment directly to your Roth IRA or designated Roth account in an employer plan. You should contact the Roth IRA sponsor or the administrator of the employer plan for information on how to do a direct rollover.

If you do not do a direct rollover, you may still do a rollover by making a deposit (generally within 60 days) into a Roth IRA, whether the payment is a qualified or nonqualified distribution. In addition, you can do a rollover by making a deposit within 60 days into a designated Roth account in an employer plan if the payment is a nonqualified distribution and the rollover does not exceed the amount of the earnings in the payment. You cannot do a

If you do a direct rollover of only a portion of the amount paid from the Plan and a portion is paid to you at the same time, the portion directly rolled over consists first of earnings.

If you do not do a direct rollover and the payment is not a qualified distribution, the Plan is required to withhold 20% of the earnings for federal income taxes (up to the amount of cash and property received other than employer stock). This means that, in order to roll over the entire payment in a

How much may I roll over?

The following rules are the same for both

If you wish to do a rollover, you may roll over all or part of the amount eligible for rollover. Any payment from the Plan is eligible for rollover, except:

yy Certain payments spread over a period of at least 10 years or over your life or life expectancy (or the lives or joint life expectancy of you and your beneficiary)

yy Required minimum distributions after age 70½ (or after death) yy Hardship distributions

yy ESOP dividends

If I don’t do a rollover, will I have to pay the 10% additional income tax on early distributions?

If you are under age 59½, you will have to pay the 10% additional income tax on early distributions for any payment from the Plan (including amounts withheld for income tax) that you do not roll over, unless one of the exceptions listed below applies. This tax applies to the part of the distribution that you must include in income and is in addition to the regular income tax on the payment not rolled over.

Designated Roth account

If the payment is not a qualified distribution and you are under age 59½, you will have to pay the 10% additional income tax on early distributions with respect to the earnings allocated to the payment that you do not roll over (including amounts withheld for income tax), unless one of the exceptions listed below applies. This tax is in addition to the regular income tax on the earnings not rolled over.

Both

The 10% additional income tax does not apply to the following payments from the Plan:

yy Payments made after you separate from service if you will be at least age 55 in the year of the separation

yy Payments that start after you separate from service if paid at least annually in equal or close to equal amounts over your life or life expectancy (or the lives or joint life expectancy of you and your beneficiary)

yy Payments from a governmental retirement plan made after you separate from service if you are a qualified public safety employee and you will be at least age 50 in the year of the separation. The term “qualified public safety employee” means public safety employees of a state, political subdivision of a state; and specified federal law enforcement officers, federal customs and border protection officers, federal firefighters and air traffic controllers

yy Payments made due to disability yy Payments after your death

yy Payments of ESOP dividends

yy Corrective distributions of contributions that exceed tax law limitations

yy Cost of life insurance paid by the Plan

yy Payments made directly to the government to satisfy a federal tax levy

|

|

|

RPS33691 (10/18) |

Questions? Visit LincolnFinancial.com or call |

Page 2 of 7 |

Form Characteristics

| Fact Name | Description |

|---|---|

| Purpose | This form is designed for individuals requesting a distribution to another company, primarily for common reasons like rollovers or plan-to-plan transfers. |

| Restrictions | This form should not be used for hardship distributions, required minimum distributions (RMDs), or death claims, among others. |

| Methods of Distribution | Options include rollovers, plan-to-plan transfers, contract exchanges, and permissive service credit transfers, depending on eligibility and plan type. |

| Governing Law | This form is subject to federal regulations regarding retirement accounts, along with any applicable state laws, depending on the recipient's location. |

Guidelines on Utilizing Lincoln Request Distribution

Completing the Lincoln Request Distribution form is essential for initiating a payment to another company from your retirement plan. Each section of the form collects specific information to ensure the transaction is processed smoothly. Follow these detailed steps to fill out the form accurately.

- Provide your personal details: Fill in your name, Social Security Number (SSN), street address, city, state, zip code, mobile number, email address, and phone number. Indicate your marital status and employment status, and enter your date of birth.

- Select how you want to move your funds: Choose from the options available: Rollover, Contract exchange, Plan-to-plan transfer, or Permissive service credit transfer. Specify the type of receiving plan/account such as 401(k), 403(b), or IRA.

- Fill in the receiving company information: Include the name of the company that will receive the funds, the account number, and the complete street address, including the city, state, and zip code.

- Specify the amount to send: Choose whether to send 100% of your account balance or a specific dollar amount. If opting for partial distribution, provide the exact amount.

- Decide how to receive your payment: For partial cash payments, indicate whether you prefer direct deposit or a check mailed to your address. If choosing direct deposit, include your bank account details.

- Determine tax withholdings: If receiving partial cash, indicate your federal and state tax withholding preferences. If you choose to withhold federal taxes at a higher rate, specify that rate.

- Sign and date the form: Confirm your understanding of the important notices and certify the accuracy of the provided information by signing and dating the form.

- Verify spousal consent if required: If applicable, ensure your spouse signs the form consenting to the distribution, and have a notary sign if needed.

Following these steps will help ensure your distribution request is submitted correctly. Make sure to double-check all entries for accuracy before sending the form. This attention to detail can help avoid potential delays in your request.

What You Should Know About This Form

What is the purpose of the Lincoln Request Distribution form?

The Lincoln Request Distribution form is designed for individuals who want to request a distribution of their retirement funds to another company. This form is particularly useful for the most common reasons for distribution, such as rollovers, plan-to-plan transfers, or contract exchanges. It's important to ensure that you are using the correct form for your specific needs, as other forms exist for different circumstances.

Can I use this form for any type of distribution request?

No, this form should not be used for certain specific distribution requests. Some situations that require a different form include hardship or unforeseeable emergencies, required minimum distributions (RMD), excess withdrawals, death claims, plan terminations, and in-plan Roth conversions. Always check with your plan administrator if you're unsure which form to use.

What methods are available for moving my retirement funds?

There are several methods for transferring your retirement funds, depending on your situation:

- Rollover: This is when you move assets from one retirement plan to another, usually upon leaving an employer or retiring.

- Contract exchange: Applicable only to 403(b) plans, allowing for tax-free transfers within the same plan.

- Plan-to-plan transfer: This involves transferring assets from one plan to another of the same type without a distribution event.

- Permissive service credit transfer: A transfer to purchase additional service or benefits in a government-defined benefit plan.

What should I do if my receiving company information is incorrect?

If the information for your receiving company is incomplete or incorrect, Lincoln will issue a check made out to that company but will send it to your address instead. You will then be responsible for ensuring that the check is mailed to the receiving company to complete the transaction. It’s crucial to double-check this information before submitting the form.

How will taxes affect my distribution?

Do I need to consult anyone before submitting this form?

What if I need more assistance with the form?

Are there any restrictions I should be aware of?

Common mistakes

Completing the Lincoln Request Distribution form is crucial, yet many individuals make common mistakes that can delay their distribution or complicate the process. One frequent error is using the form incorrectly. This form is specifically for requesting distributions to another company, and it should only be used for the most common distribution reasons. If the distribution is due to a hardship or a death claim, for example, this form is not appropriate. Always confirm that you are using the correct documentation to avoid unnecessary complications.

Inaccuracies in personal information is another issue. Individuals often fail to provide complete and correct details about themselves, such as their Social Security Number and address. Incomplete information can lead to confusion and possible denial of the request. Always double-check that all personal information is accurate and fully filled out.

Some people neglect to clarify their marital status, which is crucial for processing the request. This form requires explicit indication of whether you have a living spouse, as this information can affect the handling of your distribution. Failing to specify this can lead to delays in processing.

Not understanding the type of distribution being requested is also a common pitfall. Individuals may select the wrong option, such as rollover or plan-to-plan transfer, without fully understanding the differences. Each option has specific requirements and implications. It is essential to read through the definitions and options carefully before making a selection.

Another mistake is providing incomplete or inaccurate receiving company information. If the details for the company you're transferring your funds to are incorrect, the check will be issued improperly, leading to delays. Ensure that the company name and address are correct and formatted properly to facilitate smooth transactions.

Many people overlook the tax implications that come with distributions. Not providing the correct federal tax withholding rate or disregarding potential penalties can lead to unexpected tax burdens later. Make sure to understand how distributions are taxed and consult a tax advisor if needed to avoid these issues.

Furthermore, failing to provide required documentation can significantly affect the approval process. For example, if totally and permanently disabled, a letter from the Social Security Administration is mandatory. Similarly, a Qualified Domestic Relations Order requires a court document. Be sure to gather and include all needed documents with your form.

Finally, signing and dating the form is sometimes rushed or forgotten. All parties involved must ensure that the form is signed correctly to validate the request. Without a signature, processing will be halted, leading to unnecessary delays. Take a moment to confirm that everything is completed before submission.

Documents used along the form

The Lincoln Request Distribution form is an important document for initiating the distribution of funds to another company. In addition to this form, there are several other documents that may be needed to facilitate your requests related to retirement plans. Below is a list of commonly used forms that may accompany the Lincoln Request Distribution form.

- Rollover Request Form: This form is used specifically to request the rollover of retirement assets from one account to another. It provides the necessary information regarding the current plan and the receiving account.

- Required Minimum Distribution (RMD) Form: Individuals who reach a certain age must take minimum distributions from their retirement accounts. This form is required to request those distributions in compliance with IRS regulations.

- Plan-to-Plan Transfer Form: This document allows participants to transfer retirement assets from one plan to another. It requires information about both plans to process the transfer smoothly.

- Contract Exchange Request: Used only for 403(b) plans, this form allows for the tax-free transfer of funds between two 403(b) accounts. Approval from the plan administrator is often needed.

- Qualified Domestic Relations Order (QDRO): This order from a court outlines how retirement plan benefits are to be divided following a divorce. A copy of this document is required when dividing benefits.

- Spousal Consent Form: In some cases, the plan may require a spouse's signature to consent to a distribution. This form confirms that the spouse is aware of and agrees to the distribution request.

- Permissive Service Credit Transfer Form: This form pertains to transferring funds into a government defined benefit plan for the purpose of purchasing additional service credits.

- Withdrawal Request Form: This form is needed for members who wish to withdraw funds from their retirement account directly, differing from a rollover or transfer.

- Address Change Form: If you have moved, updating your address ensures that tax documents and correspondence reach you. This form is critical for maintaining accurate records.

- Tax Withholding Election Form: This form allows you to specify how much federal and state tax, if any, should be withheld from your distribution, ensuring compliance with tax regulations.

Familiarizing yourself with these forms can help streamlining your transaction process related to your retirement funds. If you have any questions regarding these documents or need assistance, a representative is available to help you.

Similar forms

The Lincoln Request Distribution form is a crucial document for anyone looking to move funds from one retirement account to another. It has similarities to other specific forms used in similar contexts. Here’s a breakdown of six documents that share features or purposes with the Lincoln Request Distribution form:

- Rollover Request Form: Like the Lincoln Request Distribution form, this form is used when transferring funds from one retirement account to another. It facilitates the movement of assets, ensuring that the rollover is done in a tax-efficient manner.

- Plan-to-Plan Transfer Form: This document is very similar to the Lincoln form as it also allows for the transfer of retirement assets from one plan to another. Both forms are designed to help individuals consolidate their retirement savings, thereby simplifying their financial management.

- Contract Exchange Form: Used specifically for 403(b) plans, this form allows for the tax-free transfer of funds from one 403(b) account to another. Similar to the Lincoln Request Distribution, the focus is on facilitating distributions without tax penalties when moving within the same plan type.

- Permissive Service Credit Transfer Form: This type of transfer is used to move funds for the purpose of purchasing additional service credits in certain defined benefit plans. Like the Lincoln form, it handles specific types of transfers without requiring a reason for distribution, simplifying the process.

- Withdrawal Request Form: While focusing more on immediate cash distributions rather than transfers, this form still encompasses the general process of requesting funds. It shares the need for personal and account information to ensure the right funds are released.

- Required Minimum Distribution (RMD) Form: Though different in the type of transaction, both forms require detailed personal and tax information to calculate distribution amounts. The RMD form specifically addresses required withdrawals, reflecting similar concerns regarding tax implications as seen in the Lincoln Request Distribution form.

Dos and Don'ts

When filling out the Lincoln Request Distribution form, there are important guidelines to follow. Here’s a straightforward list of things to do and avoid:

- Do verify you are using the correct form for your specific distribution purpose.

- Do provide accurate personal information, including your name, SSN, and contact details.

- Do check if you need to include additional documentation, such as divorce decrees or disability letters, if applicable.

- Do specify the correct receiving company and ensure that all information is complete and accurate.

Misconceptions

Understanding the Lincoln Request Distribution form is crucial for individuals looking to manage their retirement assets effectively. However, several misconceptions often arise regarding this process. Here are ten common misconceptions:

- This form can be used for any type of distribution. The Lincoln Request Distribution form is specifically for the most common distribution scenarios. It should not be used for hardship withdrawals, required minimum distributions, or in-plan Roth conversions.

- All retirement plans allow for direct rollovers. Not every retirement plan permits direct rollovers. It is essential to check with your plan administrator to understand the specific provisions of your plan.

- You can send funds to any account or institution. The receiving account must be eligible to accept rollovers. Double-check that the account type you specify can indeed receive the funds.

- You can ignore tax implications of a rollover. Tax consequences cannot be overlooked. A rollover could potentially trigger tax liabilities, especially if you are moving pre-tax funds to a Roth IRA.

- You must fill out every section of the form. While it’s advisable to provide complete information, only certain sections need to be filled according to your specific circumstances. For instance, not every individual will receive a partial cash payment.

- A signature is not necessary for distributions. You must sign the form to confirm the information you provided is accurate and that you understand the implications of your request.

- Federal tax withholding is optional. Federal tax withholding is required on certain distributions. Failure to account for this can lead to unexpected tax liabilities.

- Transfers to different types of accounts are always allowed. You cannot assume that you can transfer funds to any type of retirement account. Each type of account has its own rules, and not all transfers are permissible.

- The form guarantees that your request will be processed promptly. Even with a complete form, the processing time may vary based on several factors, including plan provisions and tax implications.

- Once submitted, you cannot change your mind. While withdrawing a distribution is a significant decision, contacting your plan administrator after submission may allow for modifications in some cases.

By addressing these misconceptions, individuals can better navigate the complexities of their retirement distributions. Being informed is a vital step in managing retirement accounts aptly.

Key takeaways

Understanding the Lincoln Request Distribution form is crucial for a smooth asset transfer. Here are key points to consider:

- Confirm its purpose: This form is specifically for requesting distributions to another company. Ensure you are using the correct form for your situation.

- Know what it cannot be used for: Do not use this form for hardship distributions, required minimum distributions (RMDs), excess withdrawals, death claims, plan terminations, or in-plan Roth conversions.

- Different distribution methods: Familiarize yourself with various methods to move your money, such as rollovers, contract exchanges, plan-to-plan transfers, and permissive service credit transfers. Each has specific conditions and eligibility.

- Accurate information is key: Ensure that all provided details about yourself and the receiving company are complete and accurate to avoid delays in processing.

- Be aware of tax implications: Understand that taxes will be withheld from your distribution. Consider consulting a tax advisor for tailored advice regarding your tax liabilities and options.

- Seek assistance if needed: If you have questions or require help with the form, contact Lincoln’s Customer Contact Center at 1-800-234-3500 or reach out to your retirement plan representative.

Browse Other Templates

Healthypaws Login - The claims team is available to assist with inquiries.

End Stage Renal Disease Enrollment Form,ESRD Medicare Application,Medicare Kidney Disease Certification,Chronic Kidney Disease Registration Document,Renal Disease Patient Entitlement Form,ESRD Patient Medical Evidence Report,Kidney Transplant Eligibi - Completion must occur within 45 days of starting dialysis treatment.