Fill Out Your Medicaid Income Trust Form

The Medicaid Income Trust form, particularly known as the Qualified Income Trust (QIT), serves a critical role for individuals whose income exceeds the eligibility limit for Medicaid’s long-term care services. When facing the potential high costs of nursing home care or other institutional services, this form offers a pathway for individuals to qualify for assistance by allowing them to place a portion of their income into a dedicated account each month. The process involves creating a written agreement that outlines the trust's terms, establishing a specific account, and regularly depositing income into it. Those in need of a QIT typically have incomes that surpass the standard thresholds for various Medicaid programs, such as the Institutional Care Program (ICP) or the Home and Community-Based Services (HCBS) waivers. Setting up this trust can be done independently or with professional assistance, but it must be structured according to specific legal requirements and receive approval from the state’s Department of Children and Families. Crucially, the agreement must stipulate that the funds are irrevocable, ensuring that any remaining balance is returned to the state upon the beneficiary's death, up to the total amount of Medicaid benefits provided. This careful management of income through the QIT enables those in need to maintain eligibility for vital healthcare services while navigating the complexities of financial and legal obligations.

Medicaid Income Trust Example

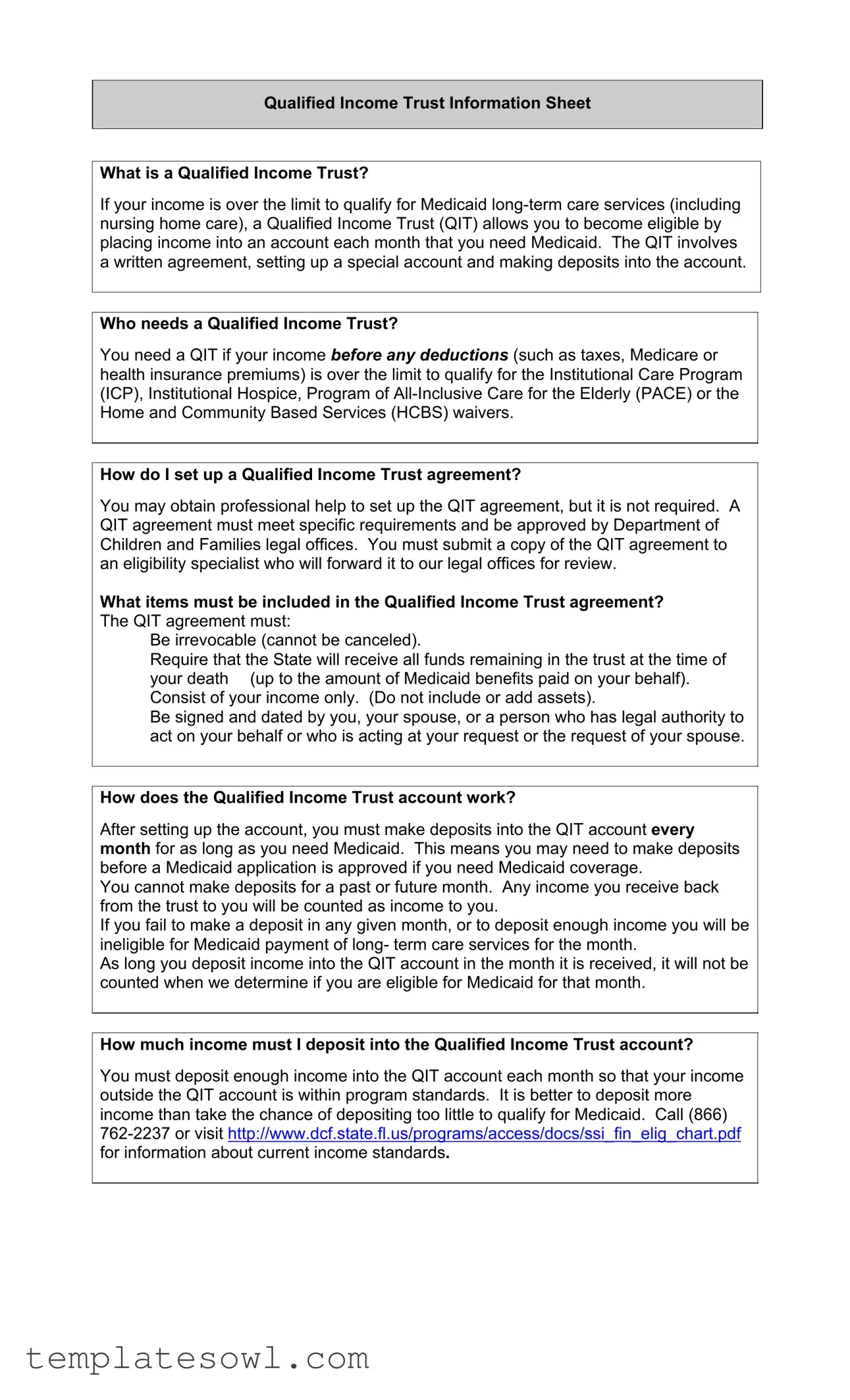

Qualified Income Trust Information Sheet

What is a Qualified Income Trust?

If your income is over the limit to qualify for Medicaid

Who needs a Qualified Income Trust?

You need a QIT if your income before any deductions (such as taxes, Medicare or health insurance premiums) is over the limit to qualify for the Institutional Care Program (ICP), Institutional Hospice, Program of

How do I set up a Qualified Income Trust agreement?

You may obtain professional help to set up the QIT agreement, but it is not required. A QIT agreement must meet specific requirements and be approved by Department of Children and Families legal offices. You must submit a copy of the QIT agreement to an eligibility specialist who will forward it to our legal offices for review.

What items must be included in the Qualified Income Trust agreement? The QIT agreement must:

Be irrevocable (cannot be canceled).

Require that the State will receive all funds remaining in the trust at the time of your death (up to the amount of Medicaid benefits paid on your behalf). Consist of your income only. (Do not include or add assets).

Be signed and dated by you, your spouse, or a person who has legal authority to act on your behalf or who is acting at your request or the request of your spouse.

How does the Qualified Income Trust account work?

After setting up the account, you must make deposits into the QIT account every month for as long as you need Medicaid. This means you may need to make deposits before a Medicaid application is approved if you need Medicaid coverage.

You cannot make deposits for a past or future month. Any income you receive back from the trust to you will be counted as income to you.

If you fail to make a deposit in any given month, or to deposit enough income you will be ineligible for Medicaid payment of long- term care services for the month.

As long you deposit income into the QIT account in the month it is received, it will not be counted when we determine if you are eligible for Medicaid for that month.

How much income must I deposit into the Qualified Income Trust account?

You must deposit enough income into the QIT account each month so that your income outside the QIT account is within program standards. It is better to deposit more income than take the chance of depositing too little to qualify for Medicaid. Call (866)

What happens to the income I deposit in the Qualified Income Trust account?

The income you have in and out of the QIT is used to calculate your patient responsibility. If you do have a patient responsibility, you are responsible for paying that amount. If there is money left in the QIT upon your death, it is paid to the State, up to an amount equal to the total medical assistance paid on your behalf by the state while the trust was in effect.

How to pay funds remaining in the QIT to the State?

The QIT trustee or other individual acting on your behalf should contact the long term care facility to see if any refund for the month of death is due back to the trust. The balance of the QIT at the date of death, plus any refund from the long term care facility is to be paid to the State.

Mail a check payable to the “Agency for Health Care Administration” to: Xerox State Healthcare, LLC

PO Box 12188 Tallahassee, FL

A brief cover letter or note should state that the payment is for a QIT and include your name, Social Security number, and/or Medicaid ID number. Enclose a copy of the QIT bank statement covering the date of death to confirm the check is for the balance. Also, include documentation of any refunds received from the long term care facility. Contact Xerox State Healthcare, LLC at (877)

Form Characteristics

| Fact Title | Description |

|---|---|

| Definition of Qualified Income Trust | A Qualified Income Trust (QIT) enables individuals whose income exceeds the limits for Medicaid long-term care services to qualify by depositing their income into a designated account each month. |

| Eligibility Criteria | Individuals with income above the limits for Medicaid's Institutional Care Program (ICP), Institutional Hospice, PACE, or HCBS waivers must establish a QIT to qualify for services. |

| Agreement Requirements | The QIT agreement must be irrevocable, include only income, and stipulate that remaining funds go to the State upon the individual's death, covering Medicaid expenses incurred. |

| Deposits and Medicaid Eligibility | Monthly deposits into the QIT must be made to maintain Medicaid eligibility. If deposits are insufficient or missed, eligibility for long-term care services becomes compromised. |

| Transfer of Funds Upon Death | Upon the individual's death, any remaining funds in the QIT, along with any refunds from the long-term care facility, must be paid to the State to cover past medical assistance costs. |

Guidelines on Utilizing Medicaid Income Trust

Completing the Medicaid Income Trust form requires careful attention to details specified in the guidelines. Properly filling out this form is essential to ensure eligibility for Medicaid long-term care services. Below are step-by-step instructions to accurately complete the form.

- Obtain the Qualified Income Trust (QIT) Information Sheet from the relevant state department or agency.

- Carefully read the information sheet to understand the requirements for the Qualified Income Trust agreement.

- Prepare the QIT agreement with the following elements:

- Make the agreement irrevocable.

- State that the funds remaining at the time of death will go to the State up to the amount of Medicaid benefits paid.

- Include only your income in the trust agreement; do not add assets.

- Ensure the agreement is signed and dated by you, your spouse, or an authorized representative.

- Set up a special account specifically for the QIT. This account will hold your monthly income deposits.

- Deposit your income into the QIT account monthly for the duration of your need for Medicaid services.

- Verify that you deposit enough income each month so that your income outside the QIT meets Medicaid program standards.

- Submit a copy of the QIT agreement to the assigned eligibility specialist for approval. They will forward it to the legal offices for review.

- After approval, maintain accurate records of all deposits made to the QIT account.

- If necessary, contact the Department of Children and Families for any clarifications or additional information.

Next, be prepared to manage the funds in the QIT account in accordance with Medicaid rules, making sure to meet deposit requirements every month. Proper management will assist in maintaining eligibility for the needed services.

What You Should Know About This Form

What is a Qualified Income Trust?

A Qualified Income Trust (QIT) is a specific type of trust that allows individuals with income exceeding the Medicaid limit to qualify for Medicaid long-term care services, including nursing home care. By placing their income into a QIT each month, individuals can potentially become eligible for benefits. The process includes creating a written agreement and setting up a special account for these deposits.

Who needs a Qualified Income Trust?

If your monthly income, before taxes and deductions, exceeds the allotted limit for programs like the Institutional Care Program (ICP) or the Program of All-Inclusive Care for the Elderly (PACE), you will need a QIT to qualify for Medicaid services. It is crucial to assess your income level accurately to understand if you fall into this category.

How do I set up a Qualified Income Trust agreement?

You can set up a QIT agreement on your own, though seeking professional assistance is also an option. The QIT must follow specific guidelines and get approval from legal offices under the Department of Children and Families. Once you create the agreement, it must be submitted to an eligibility specialist for review before it can take effect.

What items must be included in the Qualified Income Trust agreement?

The QIT agreement needs to be irrevocable, meaning it cannot be canceled. It should specify that all remaining funds will go to the State upon your death, up to the total Medicaid benefits paid. Additionally, only your income should be included; no assets are allowed. Lastly, it must be signed and dated by either you, your spouse, or someone with legal authority acting on your behalf.

How does the Qualified Income Trust account work?

Once the account is established, regular monthly deposits into the QIT are necessary while you require Medicaid. If you receive income during a month, you must deposit that amount into the QIT for it not to count against your eligibility. Missing a deposit could result in losing Medicaid benefits for that month, so it is vital to manage deposits carefully.

Common mistakes

Completing the Medicaid Income Trust form requires careful attention to detail. One common mistake is not including all necessary information required in the Qualified Income Trust (QIT) agreement. Ensure that every item listed as necessary is addressed. Omitting even a single detail can lead to delays or denial of your application.

Another mistake to avoid is failing to make the QIT irrevocable. The trust must be permanent and cannot be canceled. Ensure that the language in the agreement explicitly states this requirement to avoid complications later.

Many individuals also mistakenly include assets in the QIT. The funds deposited must consist of income only, not any other assets. Clearly identifying these funds as income will help maintain compliance with Medicaid regulations.

Some applicants do not sign and date the trust correctly. This step is crucial, and it must be completed by you, your spouse, or someone with legal authority to act on your behalf. Make sure all required parties fulfill this obligation to prevent issues with the trust's validity.

Depositing insufficient funds into the QIT account is another frequent error. It's essential to regularly make deposits that keep your income within program limits. Regularly assess your income to ensure adequate deposits, as failure to do so may jeopardize your Medicaid eligibility.

Not submitting the QIT agreement to an eligibility specialist for approval is a critical oversight. The approval process is necessary, as it ensures that the agreement meets all legal requirements. Always submit this document promptly to avoid any unnecessary delays in your application.

Finally, some people neglect to provide proper documentation when sending payments to the State. It's vital to include a cover letter or note with your QIT payment and all necessary identification information. This final step helps ensure that your payment is processed smoothly and accurately.

Documents used along the form

When navigating the complexities of Medicaid eligibility, especially for long-term care services, several important documents work in conjunction with the Qualified Income Trust (QIT) form. Each of these documents serves a significant role in ensuring compliance with Medicaid regulations while also protecting the interests of individuals seeking assistance. Below is a list of forms and documents that are often utilized alongside the QIT.

- Medicaid Application Form: This is the main application filed with Medicaid to determine eligibility for benefits. It requires comprehensive personal, financial, and medical information.

- Medicaid Authorization Form: This form allows healthcare providers to share necessary medical information with Medicaid. It ensures that Medicaid can review your medical history and determine coverage eligibility.

- Financial Disclosure Form: Detailed financial documentation is required to prove income and assets, including bank statements and tax returns. These documents support the income details provided in the QIT.

- Proof of Income Documentation: Items such as pay stubs, Social Security statements, or pension notices must be submitted to verify income. Accurate proof is crucial for setting up the QIT correctly.

- Trust Account Bank Statement: This demonstrates the deposits made into the QIT account. It's essential for verifying that the deposits were made timely each month as needed for Medicaid eligibility.

- Power of Attorney (POA) Document: If someone is acting on your behalf, a POA document is needed. This legal document designates a specific person to manage your financial and medical decisions.

- Notice of Medicaid Spend Down: This form describes the process by which a recipient must reduce their income or assets to qualify for Medicaid. A clear understanding of this process is essential when utilizing a QIT.

- Patient Responsibility Statement: Once approved for Medicaid, this statement details the amount you are required to pay towards your care based on the income sent to the QIT.

- Final Settlement Documents: Upon the death of the QIT beneficiary, these documents outline the final balances in the trust and detail how funds will be paid to the state following Medicaid's guidelines.

Understanding and organizing these documents is vital for a smoother application and ongoing eligibility for Medicaid services. Working closely with legal or financial advisors can significantly ease the process, leading to more peace of mind during a challenging time.

Similar forms

- Special Needs Trust (SNT): Like a Qualified Income Trust, a Special Needs Trust is designed to maintain eligibility for government benefits. It allows individuals with disabilities to receive income without jeopardizing their access to Medicaid or Supplemental Security Income (SSI).

- Irrevocable Life Insurance Trust (ILIT): An ILIT removes life insurance from the estate, allowing beneficiaries to receive the proceeds free of estate taxes. This is similar to a QIT in that it cannot be altered once established, protecting the funds for specific beneficiaries while avoiding estate tax implications.

- Pooled Trust: Pooled Trusts combine the resources of several beneficiaries to manage funds efficiently. Like a QIT, funds deposited remain protected and help beneficiaries qualify for benefits, but they usually allow for more flexibility regarding distributions.

- Charitable Remainder Trust (CRT): A CRT allows individuals to receive income during their lifetime, with remaining assets directed to charity after death. This echoes the QIT’s structure where income is managed according to specific rules while intent is designated for the remainder.

- Revocable Living Trust: While this type of trust can be modified during the creator's lifetime, it shares similarities with a QIT in providing a structured way to manage assets and determine the distribution after death, preserving the intent and wishes laid out by the individual.

- Medicaid Asset Protection Trust (MAPT): This trust can help protect assets from being counted against Medicaid eligibility. Similar to a QIT, it restricts access to funds for a specified purpose, but it involves a broader range of asset protection while qualifying for benefits.

- Spendthrift Trust: A Spendthrift Trust prevents beneficiaries from using their trust distributions to claim against debts or for creditors, similar to the QIT's effect of safeguarding income in relation to Medicaid eligibility.

- Family Trust: A Family Trust, like a QIT, serves to manage how assets are distributed to beneficiaries, protecting them while ensuring that funds are available for specific needs, such as healthcare or living expenses.

- Educational Trust: This trust is created to provide funds specifically for educational expenses. Like the QIT, it provides a structured way to manage money for a designated purpose, but is focused on ensuring access to education instead of healthcare.

- Retirement Accounts with Payable on Death (POD) designations: These accounts allow for the direct transfer of funds upon death, maintaining the intended allocation of resources. They are similar to a QIT in the way they assure that funds can be utilized as needs dictate, without being counted as part of the estate for Medicaid purposes.

Dos and Don'ts

When filling out the Medicaid Income Trust form, consider the following do's and don'ts:

- Do ensure that the QIT agreement is irrevocable.

- Do deposit your full income into the QIT account each month.

- Do have the QIT agreement signed and dated by the appropriate parties.

- Do submit the completed QIT agreement to an eligibility specialist.

- Do keep records of all deposits and communications regarding the QIT.

- Don't include any assets or properties in the QIT.

- Don't forget to make your deposits on time each month.

- Don't attempt to modify or cancel the trust after it has been established.

- Don't neglect to contact the long-term care facility for any potential refunds.

- Don't hesitate to seek professional assistance if needed.

Misconceptions

Many individuals considering a Qualified Income Trust (QIT) harbor misconceptions about its purpose and requirements. Here are five common misunderstandings:

- Misconception #1: A QIT can be canceled at any time.

- Misconception #2: You can include assets in the trust.

- Misconception #3: You do not need to deposit income each month.

- Misconception #4: The state does not receive funds remaining in the trust.

- Misconception #5: Professional help is mandatory to set up a QIT.

This is not true. A Qualified Income Trust is irrevocable, meaning once established, it cannot be undone. It is essential to understand that this ensures that the trust will adhere to the relevant Medicaid regulations.

Many people mistakenly believe they can add assets to their QIT. However, a QIT must consist solely of income. Assets cannot be included, which is crucial to maintaining eligibility for Medicaid.

This is a critical error. Regular monthly deposits are necessary for maintaining Medicaid eligibility. If a deposit is missed, it jeopardizes your coverage for that month.

Many individuals believe that they can keep any leftover funds. In reality, when an individual passes away, the state will receive all remaining trust funds up to the total amount spent on Medicaid benefits on their behalf.

While it can be beneficial to seek assistance from a professional, it is not a requirement to establish a QIT. It is possible to create the trust independently, as long as all necessary requirements are met and the agreement is approved by the appropriate authorities.

Key takeaways

- A Qualified Income Trust (QIT) allows individuals with income above the Medicaid limit to qualify for long-term care services by depositing excess income into a designated account.

- Eligibility for a QIT is necessary for those whose pre-deduction income exceeds the threshold set for programs such as the Institutional Care Program (ICP) and Home and Community Based Services (HCBS) waivers.

- Setting up a QIT does not require professional assistance, but the trust must comply with specific legal requirements and be approved by the Department of Children and Families.

- A QIT agreement must be irrevocable, meaning it cannot be canceled, and it must stipulate that the state receives any remaining funds upon the individual's death.

- Monthly deposits of income into the QIT account must be made consistently. Failure to do so may result in ineligibility for Medicaid long-term care services.

- To maintain eligibility, individuals should deposit enough income each month to keep their total income within the established program limits.

- Upon the individual's death, any remaining funds in the QIT, along with any applicable refunds from the long-term care facility, are to be paid to the State, covering the total medical assistance provided while the trust was active.

Browse Other Templates

Church Balance Sheet - Clarify purpose statements to justify financial expenditures.

How to Cancel Carefirst Insurance - Use this form responsibly to ensure your health insurance is managed appropriately.

Filing for Custody in Florida - Consider the mental and physical health of each parent.