Fill Out Your Michigan 165 Form

The Michigan 165 form, officially known as the 2021 Sales, Use, and Withholding Taxes Annual Return (Form 5081), is a critical document for businesses navigating their tax obligations within the state. Designed to ensure compliance with state tax laws, it covers three primary tax categories: sales tax, use tax, and withholding tax. Businesses must accurately report total gross sales, calculate taxable balances, and account for allowable deductions. To fill out this form correctly, taxpayers are required to provide their business information, including taxpayer identification numbers and addresses, as well as detailed sales figures and tax amounts owed. It’s also essential to distinguish between different types of revenues, such as those from rentals or telecommunications services. Timely submission by the February 28 deadline prevents penalties and late fees. Additionally, the form offers clear guidelines on claiming exemptions, refunds, and credits, making it easier for businesses to manage their tax responsibilities effectively. For most taxpayers, filing electronically is encouraged, streamlining the process and reducing potential errors. Understanding how to properly utilize the Michigan 165 form is key to keeping your business compliant and avoiding unnecessary complications with the state treasury.

Michigan 165 Example

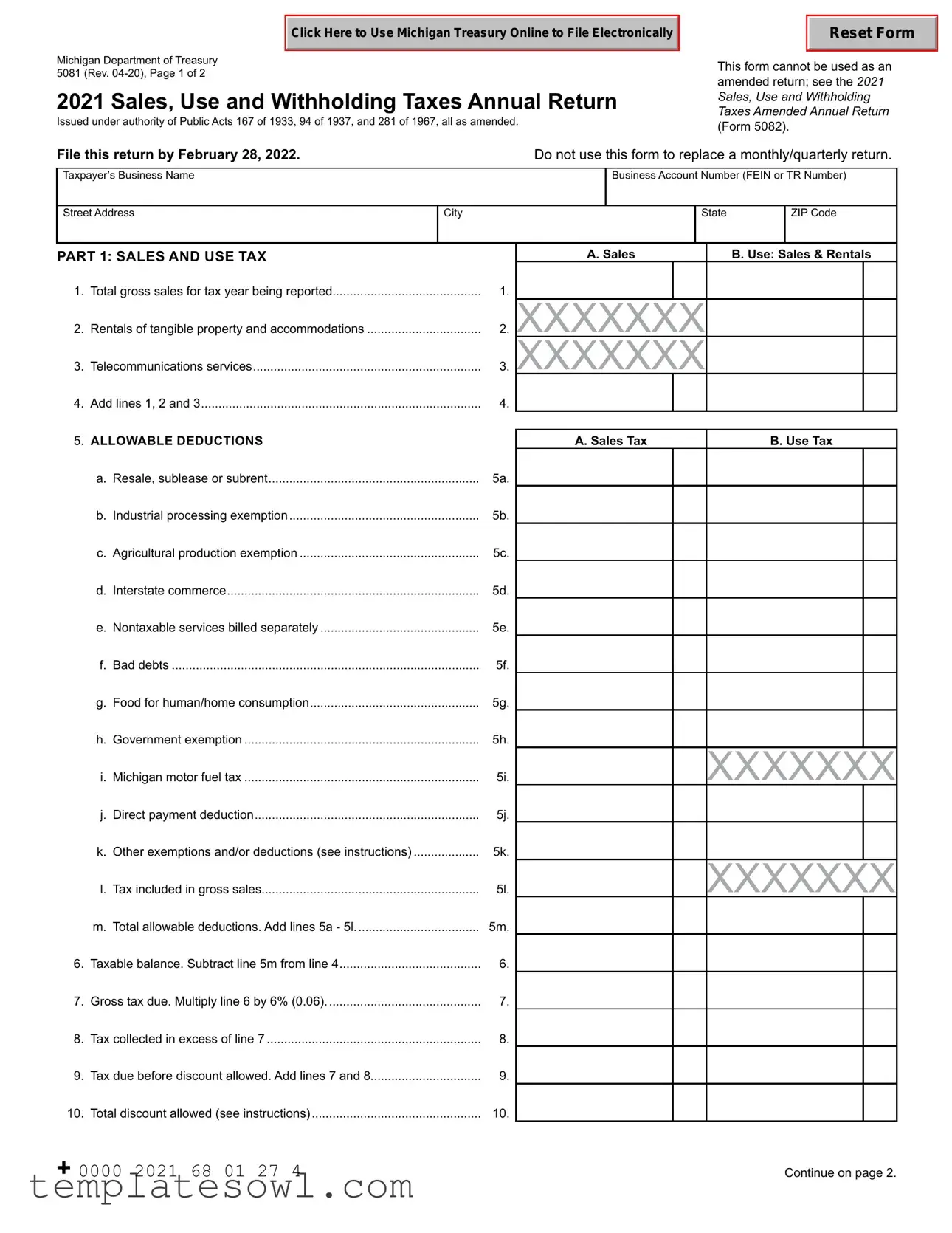

Click Here to Use Michigan Treasury Online to File Electronically

Michigan Department of Treasury

5081 (Rev.

2021 Sales, Use and Withholding Taxes Annual Return

Issued under authority of Public Acts 167 of 1933, 94 of 1937, and 281 of 1967, all as amended.

Reset Form

This form cannot be used as an amended return; see the 2021

Sales, Use and Withholding

Taxes Amended Annual Return (Form 5082).

File this return by February 28, 2022. |

Do not use this form to replace a monthly/quarterly return. |

Taxpayer’s Business Name

Business Account Number (FEIN or TR Number)

Street Address

City

State

ZIP Code

PART 1: SALES AND USE TAX

1.Total gross sales for tax year being reported...........................................

2.Rentals of tangible property and accommodations .................................

3.Telecommunications services..................................................................

4.Add lines 1, 2 and 3.................................................................................

A. Sales |

B. Use: Sales & Rentals |

1.

2. XXXXXXX

3. XXXXXXX

4.

5.ALLOWABLE DEDUCTIONS

|

a. Resale, sublease or subrent |

5a. |

|

b. Industrial processing exemption |

5b. |

|

c. Agricultural production exemption |

5c. |

|

d. Interstate commerce |

5d. |

|

e. Nontaxable services billed separately |

5e. |

|

f. Bad debts |

5f. |

|

g. Food for human/home consumption |

5g. |

|

h. Government exemption |

5h. |

|

i. Michigan motor fuel tax |

5i. |

|

j. Direct payment deduction |

5j. |

|

k. Other exemptions and/or deductions (see instructions) |

5k. |

|

l. Tax included in gross sales |

5l. |

|

m. Total allowable deductions. Add lines 5a - 5l |

5m. |

6. |

Taxable balance. Subtract line 5m from line 4 |

6. |

7. |

Gross tax due. Multiply line 6 by 6% (0.06) |

7. |

8. |

Tax collected in excess of line 7 |

8. |

9. |

Tax due before discount allowed. Add lines 7 and 8 |

9. |

10. |

Total discount allowed (see instructions) |

10. |

A. Sales Tax |

B. Use Tax |

XXXXXXX

XXXXXXX

+ 0000 2021 68 01 27 4 |

Continue on page 2. |

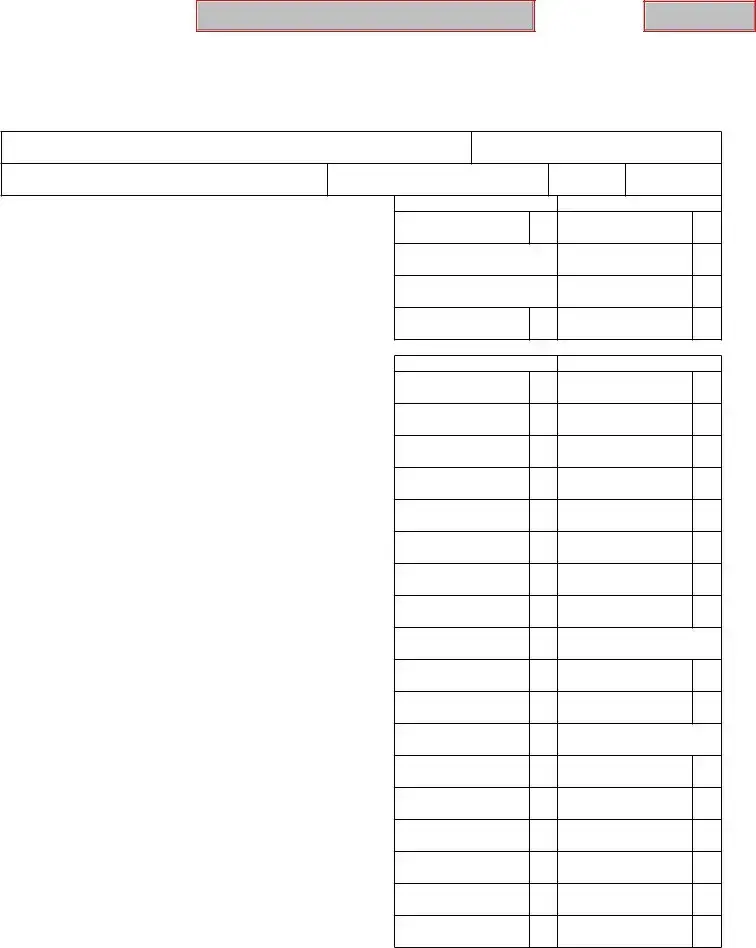

2021 Form 5081, Page 2 of 2 |

|

|

|

|

|

|||

Taxpayer’s Business Name |

|

Business Account Number |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

A. Sales Tax |

|

B. Use Tax |

||

11. |

Total tax due. Subtract line 10 from line 9 |

|

11. |

|

|

|

|

|

12. |

.....................Tax payments and credits in current year (after discounts) |

12. |

|

|

|

|

|

|

PART 2: USE TAX ON ITEMS PURCHASED FOR BUSINESS OR PERSONAL USE |

|

|

|

|||||

|

|

|

||||||

13. |

Purchases for which no tax was paid or inventory purchased or withdrawn for business or personal use.... |

13. |

|

|

||||

14. |

.....................................................................Total use tax on purchases due. Multiply Line 13 by 6% (0.06) |

|

|

14. |

|

|

||

15. |

..........................................................................Use tax paid on purchases and withdrawals in current year |

|

|

15. |

|

|

||

PART 3: WITHHOLDING TAX |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

16. |

Gross Michigan payroll, pension and other taxable compensation |

|

|

16. |

|

|

||

17. |

Total number of |

|

17. |

|

|

|

|

|

18. |

........................................................................Total Michigan income tax withheld per |

|

|

18. |

|

|

||

19. |

..............................................................Total Michigan income tax withholding paid during current tax year |

|

|

19. |

|

|

||

PART 4: SUMMARY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

20. |

Total sales, use and withholding tax due. Add lines 11A, 11B, 14 and 18 |

|

|

20. |

|

|

||

21. |

.....................................................Total sales, use and withholding tax paid. Add lines 12A, 12B, 15 and 19 |

|

|

21. |

|

|

||

22. |

...........................................If line 21 is greater than line 20, enter the difference here. If not, skip to line 25 |

|

|

|||||

23. |

............................................................................Amount of line 22 to be credited forward to a future period |

|

|

23. |

|

|

||

24. |

REFUND. Subtract line 23 from line 22 |

|

|

|

|

24. |

|

|

25. |

If line 21 is less than 20, enter balance due |

|

|

|

|

25. |

|

|

26. |

.................................................................................Penalty for late filing or late payment (see instructions) |

|

|

26. |

|

|

||

27. |

Interest for late payment (see instructions) |

|

|

|

|

27. |

|

|

28. |

TOTAL PAYMENT DUE. Add lines 25, 26 and 27 |

|

|

|

|

28. |

|

|

PART 5: SIGNATURE (All information below is required.)

Taxpayer Certification. I declare under penalty of perjury that the information in this |

Preparer Certification. I declare under penalty of perjury that this |

|||||

return and attachments is true and complete to the best of my knowledge. |

return is based on all information of which I have any knowledge. |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Preparer’s Signature |

|

|

|

By checking this box, I authorize Treasury to discuss my return with my preparer. |

|

|

||

|

|

|

|

|||

|

|

|

|

|

||

|

|

|

|

|

|

|

Signature of Taxpayer or Official Representative (must be Owner, Officer, Member, |

Preparer’s Business Address |

|

||||

Manager, or Partner) |

|

|

|

|

||

|

|

|

|

|

|

|

Print Taxpayer or Official Representative’s Name |

|

Date |

|

|

||

|

|

|

|

|

|

|

Title |

Telephone |

Number |

Preparer’s Identification Number |

Preparer’s Telephone Number |

||

|

|

|

|

|

|

|

File and pay this return for free on Michigan Treasury Online at mto.treasury.michigan.gov.

Alternatively, make check payable to “State of Michigan.” Write the account number, “SUW Annual” and tax year on the check. Send the return and payment due to: Michigan Department of Treasury, P.O. Box 30401, Lansing, MI

+ 0000 2021 68 02 27 2

2021 Form 5081, Page 3

Instructions for 2021 Sales, Use and

Withholding Taxes Annual Return (Form 5081)

Form 5081 is available for submission electronically using Michigan Treasury Online (MTO) at mto.treasury.michigan.gov or by using approved tax preparation software. Most taxpayers will have the option to file the Annual EZ form, reducing the amount of fields needed to complete. Go to MTO to see if you qualify.

NOTE: The address field on this form is required to be completed but will not be used to replace an existing valid address for the purpose of correspondence or refunds. Update address and other registration information using MTO at mto.treasury.michigan.gov or mail a Notice of Change or Discontinuance (Form 163).

IMPORTANT: This is a return for sales tax, use tax and/ or withholding tax. If the taxpayer inserts a zero on or leaves blank any line reporting sales tax, use tax or withholding tax, the taxpayer is certifying that no tax is owed for that tax type. Only enter figures for taxes the business is registered and/or liable for. If it is determined that tax is owed the taxpayer will be liable for the deficiency as well as penalty and interest.

PART 1: SALES AND USE TAX

Lines 1 through 3: For information about determining whether a person has nexus with Michigan, see Revenue Administrative Bulletins (RABs)

16.Please also visit www.michigan.gov/remotesellers for guidance, including FAQs.

Line 1A: SALES TAX - Total Gross Sales for the Tax

Year: This line should be used by sellers with nexus to report sales of tangible personal property where ownership transfers in Michigan. This includes sellers with nexus through physical presence or economic presence (remote sales).

Enter total sales, including cash, credit and installment transactions, of tangible personal property. Include any costs incurred before ownership of the property is transferred to the buyer, including installation, shipping, handling, and delivery charges. Dealers do not reduce sales reported here by any

Providers of nontaxable services (that do not involve the sale or lease of tangible personal property) should not report those sales.

Line 1B: USE TAX - Total Sales for the Tax Year: This line should be used by:

•Sellers with nexus to report sales of tangible personal property sourced to Michigan, for which ownership transfers outside Michigan, or

•Remote sellers without nexus who voluntarily collect Michigan tax.

Enter total sales, including cash, credit, and installment transactions, of tangible personal property.

Line 2B: USE TAX - Rentals of Tangible Personal Property and Accommodations.

•Lessors of tangible personal property: Lessors that have made a valid election under MCL 205.95(4) and MAC R 205.132(1) should report receipts from rentals of that tangible personal property under the election.

•Persons providing accommodations: This includes but is not limited to total hotel, motel, and vacation home rentals, and assessments imposed under the Convention and Tourism Act, the Convention Facility Development Act, the Regional Tourism Marketing Act, and the Community Convention or Tourism Marketing Act.

Line 3B: USE TAX - Telecommunications Services. Enter gross income from telecommunications services.

Line

Line 5a: Resale, Sublease or Subrent. Enter resale, sublease or subrent exemption claims.

Line 5b: Industrial Processing Exemption. The sale or lease of tangible personal property ultimately used in industrial processing by an industrial processor is exempt. Industrial processing is the activity of converting or conditioning tangible personal property by changing its form, composition, quality, combination, or character. In general, all of the following must be met:

•Property must be used in producing a product for ultimate sale at retail,

•Property must be sold or leased to an industrial processor, including a person that performs industrial processing on behalf of another industrial processor or performs industrial processing on property that will be incorporated into a product for ultimate sale at retail, and

•Activity starts when property begins moving from raw materials storage to begin industrial processing and ends when finished goods first come to rest in finished goods inventory.

If property is used for both an exempt and a taxable purpose, the property is only exempt to the extent that it is used for an exempt purpose. In such cases, the exemption is limited to the percentage of exempt use to total use determined by a reasonable formula or method approved (but not required to be

Line 5c: Agricultural Production Exemption. Property must be directly or indirectly used in agricultural production. Generally, the following

(i) Tangible personal property sold or leased to a person

2021 Form 5081, Page 4

engaged in a business enterprise that uses or consumes the property for either:

•Tilling, planting, draining, caring for, maintaining, or harvesting things of the soil, or

•Breeding, raising, or caring for livestock, poultry, or horticultural products.

(ii)To the extent that the property is affixed to and made a structural part of real estate for others and used for an exempt purpose in (i), tangible personal property sold to a contractor that is one of the following:

•Agricultural land tile

•Subsurface irrigation pipe

•Portable grain bins

•Grain drying equipment and its fuel or energy source However, the following sales from (i) or (ii) are not exempt:

•Food, fuel, clothing, or similar property for personal living or human consumption, or

•Property permanently affixed to and becoming a structural part of real estate unless it is agricultural land tile, subsurface irrigation pipe, a portable grain bin, or grain drying equipment. Certain property that can be disassembled and reassembled may be exempt.

Some specific types of exempt property and exempt uses of property are clarified in the statute. If property is used for both an exempt and a taxable purpose, the property is only exempt to the extent that it is used for an exempt purpose. In such cases, the exemption is limited to the percentage of exempt use to total use determined by a reasonable formula or method approved (but not required to be

Line 5d: Interstate Commerce. Enter sales made in interstate commerce. To claim such a deduction, the property must be delivered by the business to the

Line 5e: Nontaxable Services Billed Separately. Enter charges for nontaxable services billed separately, such as repair or maintenance, if these charges were included in gross receipts on line 1. Costs, such as delivery or installation charges, that are incurred before the completion of the transfer of ownership of taxable property are included in the tax base and may not be subtracted.

Line 5f: Bad Debts. Bad debts may be eligible for a deduction if the following criteria are met:

•The debts are charged off as uncollectible on business books and records at the time the debts become worthless

•The debts are deducted on the return for the period during which the bad debts are written off as uncollectible

•The debts are or would be eligible to be deducted for federal income tax purposes.

A bad debt deduction may be claimed by a

Line 5g: Food for Human/Home Consumption. Enter the total of retail sales of

Line 5h: Government Exemption. Direct sales to the United States government or the state of Michigan or its political subdivisions are exempt.

Line 5i: Michigan Motor Fuel Tax. Motor fuel retailers may deduct the Michigan motor fuel taxes that were included in gross sales on line 1 and paid to the State or the distributor.

Line 5j: Direct Payment Deduction. Enter sales made to purchasers that claimed direct pay exemption from sales and use taxes. With the exemption claim, the purchaser must include the following statement: “Authorized to pay use tax on purchases of tangible personal property directly to the State of Michigan under Account Number [listing either the Federal Employer Identification Number or the Michigan Treasury Registration Number]. If using Michigan Sales and Use Tax Certificate of Exemption (Form 3372), check the box in Section 3 for “Other” and include the above statement as the explanation. MCL 205.98.

Line 5k: Other Exemptions and/or Deductions. Identify exemptions or deductions not covered in items 5a through 5j on this line. Examples of exemptions or deductions are:

•Allowable

Taxes paid to Secretary of State are not reported here. Instead, they are reported on the Vehicle Dealer Supplemental Schedule (Form 5086,

•Credit for the core charge attributable to a recycling fee, deposit, or disposal fee for a motor vehicle or recreational vehicle part or battery if the recycling fee, deposit, or disposal fee is separately stated on the invoice, bill of sale, or similar document given to the purchaser.

•Direct sales, not for resale, to certain nonprofit agencies, churches, schools, hospitals, and homes for the care of children and the aged, to the extent the property is used to carry out the nonprofit purpose of the organization. For sales to certain nonprofit agencies, the exemption is limited based on the sales price of property used to raise funds or obtain resources. All sales must be paid for directly from the funds of the exempt organization to qualify.

•Assessments imposed under the Convention and Tourism Act, the Convention Facility Development Act, the

2021 Form 5081, Page 5

Regional Tourism Marketing Act, or the Community Convention or Tourism Marketing Act. Hotels and motels may deduct the assessments included in gross sales and rentals if use tax on the assessments was not charged to the customers.

•Credits allowed to customers for sales tax originally paid on merchandise voluntarily returned, provided the return is made within the time period for returns stated in the taxpayer’s refund policy or 180 days after the initial sale, whichever is earlier. Repossessions are not allowable deductions.

•Sales to contractors of materials which will become part of a finished structure for a qualified exempt nonprofit hospital, qualified exempt nonprofit housing entity or church sanctuary, or materials to be affixed to and made a structural part of real estate located in another state. The purchaser will provide a Michigan Sales and Use Tax Contractor Eligibility Statement (Form 3520). See RAB

•Vehicle sales to

•Qualified nonprofit organizations with aggregate sales in the calendar year of less than $25,000 may exempt the first $10,000 of sales for fundraising purposes. Separately, veterans organizations exempt under IRC 501(c)(19) may exempt sales for the purpose of raising funds for the benefit of an active duty service member or veteran, up to $25,000 per event.

Line 5l: Tax Included in Gross Sales. Complete this line only if you have tax included in your gross sales. Subtract line 5m from line 4, then divide by 17.6667 and enter the amount.

Line 8: If more tax was collected than the amount on line 7, enter the difference.

Line 10: Total Discount Allowed for Timely Payments.

•Annual filers: Enter $72 if the tax due on line 9 is $108 or more. If tax due is less than $108, calculate the discount by multiplying line 9 by 2/3 (0.6667).

•Accelerated/Monthly/Quarterly filers: Enter total discounts allowed for the year.

Line 12: Enter total payments plus credits from 2021 Fuel Supplier and Wholesaler Prepaid Sales Tax Schedule (Form 5083), 2021 Fuel Retailer Supplemental Schedule (Form 5085), and 2021 Vehicle Dealer Supplemental Schedule (Form 5086), if applicable, made for the current tax year.

Note: all prepaid sales tax schedules are

PART 2: USE TAX ON ITEMS PURCHASED FOR BUSINESS OR PERSONAL USE

Line 13: Unless a specific exemption applies enter purchases for which no sales or use tax was paid, including property withdrawn for business or personal use. See Michigan Use Tax Act, 1937 PA 94, for information on various exemptions. For questions contact Michigan Department of

Treasury at

PART 3: WITHHOLDING TAX

Line 17: Enter the number of your

Line 18: Enter the total Michigan income tax withheld for the return year.

Line 19: Enter the total Michigan income tax withholding previously paid for the return year. (Do not include penalty and interest.)

PART 4: SUMMARY

Line 24: Enter the amount of overpayment from line 22 to be refunded. Refunds will not be made in amounts of less than $1.

Line 25: If line 21 (tax paid) is less than line 20 (tax due), enter the additional tax due. Pay any amount greater than or equal to $1.

Line 28: Total Payment Due. Add lines 25, 26 and 27. Make check payable to “State of Michigan.” Write the account number, “SUW Annual” and the tax year on the check. Do not pay if the amount due is less than $1.

How to Compute Penalty and Interest

If the return is filed after February 28 and no tax is due, compute penalty at $10 per day up to a maximum of $400. If the return is filed with additional tax due, include penalty and interest with the payment. Penalty is 5% of the tax due and increases by an additional 5% per month or fraction thereof, after the second month, to a maximum of 25%. Interest is charged daily using the average prime rate, plus 1 percent.

Refer to www.michigan.gov/taxes for current interest rate information or help in calculating late payment fees.

PART 5: SIGNATURE

REMINDER: Taxpayers must sign and date returns. Preparers must provide a Preparer Taxpayer Identification Number (PTIN), FEIN or Social Security Number (SSN), as well as a business name, business address and phone number.

Annual Return Reporting

All taxpayers are encouraged to file the annual return electronically using Michigan Treasury Online (MTO). Visit mto.treasury.michigan.gov for more information. Taxpayers with 250 or more employees must file their withholding return electronically. Do not include wage statements with your mailed annual return.

1099 and Wage Statement Reporting

Due Date. State copies of wage statements are due to the Department of Treasury on or before January 31. Late filing is subject to penalty as provided by the Revenue Act. Pursuant to the Income Tax Act of 1967, Treasury is unable to grant an extension of this filing.

2021 Form 5081, Page 6

1099 Reporting: Forms with Withholding. Taxpayers who withheld Michigan income tax on a 1099 form (1099- MISC,

1099 Reporting: Forms without Withholding. Michigan participates in the combined federal/state 1099 filing program. Taxpayers who electronically filed 1099 forms using the IRS Filing Information Returns Electronically (FIRE) system should not send copies to Treasury. Taxpayers who did not electronically file 1099 forms through the IRS FIRE system should only send copies of the

Filing Options. All taxpayers are encouraged to file state copies of wage statements electronically using Michigan Treasury Online (MTO). On MTO, you can submit wage statements for a particular business you have connected to via Tax Services or you can utilize Guest Services to send a copy of the IRS EFW2 file for one or multiple businesses.

For all MTO upload options, you will receive a confirmation of your submission. Visit mto.treasury.michigan.gov for more information. Alternatively, taxpayers can mail wage statements to: Michigan Department of Treasury Lansing, MI 48930. Do not include a copy of the annual return with wage statement mailing.

Magnetic Media. Treasury offers Magnetic Media filing to all taxpayers reporting wage statements to Michigan. You can send Magnetic Media by mail or electronically through MTO. Taxpayers with 250 or more employees must use MTO to electronically submit wage statements. For more information, refer to Transmittal for Magnetic Media Reporting of

Tax Assistance

For assistance, call

Form Characteristics

| Fact Name | Details |

|---|---|

| Form Identification | This is the 2021 Sales, Use, and Withholding Taxes Annual Return, known as Form 5081. |

| Governing Laws | The form is issued under Public Acts 167 of 1933, 94 of 1937, and 281 of 1967. |

| Filing Deadline | The return must be filed by February 28, 2022, without an option for amendments on this form. |

| Filing Method | You can file electronically through Michigan Treasury Online or use approved tax preparation software. |

| Exemption Documentation | Businesses must maintain proper documentation for any exemptions claimed on the return. |

| Tax Types | The form addresses sales tax, use tax, and withholding tax for Michigan-based businesses. |

| Amended Returns | This form cannot be used for amended returns; a separate form, Form 5082, is required for that purpose. |

| Discount for Timely Payment | A discount is available for timely tax payments, helping to reduce overall tax liability. |

| Signature Requirement | All taxpayers must sign and date the return. A preparer must also include their identification number and contact details. |

Guidelines on Utilizing Michigan 165

Once you have gathered all necessary information, you're ready to fill out the Michigan 165 form. This process requires attention to detail to ensure that the information reported is accurate, as it affects your tax obligations. The following steps outline how to successfully complete the form.

- Begin by entering your Taxpayer’s Business Name at the top of the form.

- Provide your Business Account Number, which can be either your FEIN or TR Number.

- Fill in your Street Address, City, State, and ZIP Code in the designated fields.

- Move on to PART 1: Sales and Use Tax. Report the Total gross sales for the tax year on line 1.

- Enter the amounts for Rentals of tangible property and Telecommunications services on lines 2 and 3, respectively.

- Add lines 1, 2, and 3 and write the total on line 4.

- Complete ALLOWABLE DEDUCTIONS by entering the applicable amounts on lines 5a to 5l and calculate the Total allowable deductions (line 5m) by summing the entries on lines 5a through 5l.

- Calculate the Taxable balance by subtracting line 5m from line 4 (line 6).

- Multiply the taxable balance (line 6) by 6% and enter the result on line 7 as Gross tax due.

- If you've collected more tax than what's on line 7, enter that excess on line 8.

- Add lines 7 and 8 for the Tax due before discount on line 9.

- Determine any discounts allowed and enter that amount on line 10. Remember to follow the specific instructions provided for calculation.

- Calculate the Total tax due by subtracting line 10 from line 9 and report it on line 11.

- For the next section, PART 2, enter any purchases for which no tax was paid on line 13, and then compute the Total use tax due for these purchases on line 14.

- Proceed to PART 3 for withholding tax information. Report your Gross Michigan payroll on line 16 and the total number of W-2 and 1099 forms on line 17.

- Input the Total Michigan income tax withheld on line 18 and any withholding paid during the tax year on line 19.

- In PART 4, calculate the Total sales, use and withholding tax due by adding the relevant totals (line 20).

- Report any overpayments on line 22, and move to line 23 if any amount is to be credited forward.

- If applicable, fill in the REFUND amount on line 24, and the balance due on line 25 if needed.

- Calculate any late penalties and interest on lines 26 and 27.

- Sum the amounts on lines 25, 26, and 27 for the TOTAL PAYMENT DUE on line 28.

- Lastly, complete the SIGNATURE section. Ensure that all required signatures are clear and that any preparer information is included.

After completing the form, review all entries carefully for any errors or omissions before submitting. Ensure timely filing and payment to avoid any penalties. This process lays the groundwork for fulfilling your responsibilities regarding sales, use, and withholding taxes in Michigan.

What You Should Know About This Form

What is the Michigan 165 form?

The Michigan 165 form, also known as Form 5081, is used for reporting sales, use, and withholding taxes for the tax year. Every year, businesses must file this annual return to report taxable sales, use tax due on purchases made without paying sales tax, and withholding tax collected from employees. The form must be submitted by February 28 of the following year.

Who needs to file the Michigan 165 form?

If your business sells tangible personal property or provides taxable services in Michigan, you are required to file the Michigan 165 form. This includes retailers, wholesalers, and service providers who collect sales tax. Additionally, businesses that withhold Michigan income tax from employees’ wages also need to include these figures on this form. If your business has a gross sales threshold or meets specific payroll criteria, you must file this return.

What information is required to complete the Michigan 165 form?

To complete the Michigan 165 form, you will need to provide your business name, account number, and address. Additionally, report your total gross sales, deductions for nontaxable sales, and compute the taxable balance. You also need to report any use tax due on items purchased for business or personal use, and include your withholding tax figures. Remember, adequate records to support your deductions and exemptions must be maintained.

What happens if I don’t file the Michigan 165 form on time?

Failing to file the Michigan 165 form by the deadline can result in penalties and interest on the taxes owed. If you do not owe any tax, a penalty of $10 per day can accrue up to a maximum of $400. If there are taxes due, a penalty of 5% of the owed amount is charged, increasing by 5% for each month late, up to 25%. Interest is also applied daily based on the current average prime rate plus 1 percent.

How can I file the Michigan 165 form?

The Michigan 165 form can be filed electronically using Michigan Treasury Online (MTO) at mto.treasury.michigan.gov. This method is free and convenient. If you prefer to file by mail, you can print the form, complete it, and mail it along with your payment to the Michigan Department of Treasury. Ensure that you write your account number, “SUW Annual,” and the tax year on the check to avoid processing delays.

Common mistakes

Filling out the Michigan 165 form can be a complex task, and mistakes can lead to delays or penalties. One common error is neglecting to enter the correct taxpayer identification information. It's crucial to provide either the Federal Employer Identification Number (FEIN) or the Michigan Treasury Registration Number (TR Number). Incomplete or incorrect information in this section can result in processing delays.

Another frequent mistake involves the calculations on the form. Taxpayers often miscalculate their total gross sales or allowable deductions. For example, when reporting total sales, all transactions, including cash and credit sales, must be included. If tax cannot be substantiated through proper documentation, it could lead to discrepancies and adjustments in future tax assessments.

Additionally, many individuals fail to recognize the importance of reporting both sales tax and use tax accurately. This misunderstanding can lead to incorrect entries on relevant lines of the form. Leaving a line blank or inserting a zero without appropriate justification signals that no tax is owed, which may not reflect the actual tax situation. Taxpayers must check that they only report figures for taxes for which they are registered or liable.

Finally, some tax preparers overlook the signature section. It's essential for both the taxpayer and the preparer to sign the return and include their identification numbers. Skipping this step will result in the return not being processed correctly, potentially leading to further complications with tax obligations. Double-checking every section, especially the signature area, helps ensure that the form is complete and can be filed without issues.

Documents used along the form

The Michigan 165 form, more formally known as the 2021 Sales, Use and Withholding Taxes Annual Return (Form 5081), serves as a crucial document for businesses reporting their sales, use, and withholding tax obligations in the state of Michigan. To ensure comprehensive tax compliance, several other forms and documents may accompany the Michigan 165 form during submission. Below are a few noteworthy examples.

- Michigan Sales and Use Tax Certificate of Exemption (Form 3372): This document allows purchasers to claim exemption from sales tax for certain transactions, certifying the reason for the exemption. Businesses must retain this form for their records to substantiate any exempt sales.

- 2021 Sales, Use and Withholding Taxes Amended Annual Return (Form 5082): This form is used when a taxpayer needs to amend a previously filed Michigan 165 form. It helps correct any inaccuracies in previous filings, ensuring that the tax records are accurate.

- Notice of Change or Discontinuance (Form 163): This document is essential for notifying the Michigan Department of Treasury about changes in business registration information, such as changes in address or ownership. It can help ensure that tax correspondence is sent to the correct location.

- W-2 and 1099 Forms: These forms report the wages paid to employees and non-employee compensation, respectively. They summarize income and taxes withheld, providing the state with essential information necessary for tax collection and compliance review.

- Vehicle Dealer Supplemental Schedule (Form 5086): This is specifically for vehicle dealers and reports sales tax information related to vehicle sales. It helps calculate and report any special deductions applicable to vehicle transactions.

By submitting these accompanying documents, taxpayers can better navigate their obligations under Michigan's taxation laws. This holistic approach not only aids in ensuring compliance but also minimizes the risk of penalties and interest for errors or omissions during tax reporting.

Similar forms

- Form 5082: This is the amended version of the Michigan 165 form, used to correct errors in the original tax return. Similar to the Michigan 165, it addresses sales, use, and withholding taxes, but specifically for adjustments instead of initial reporting.

- Form 3372: This form serves as the Sales and Use Tax Certificate of Exemption. Both forms deal with tax responsibilities, but Form 3372 allows purchasers to claim exemptions, thereby affecting the calculations presented in the Michigan 165.

- Form 163: The Notice of Change or Discontinuance is used to update registration information. While the Michigan 165 focuses on tax returns, Form 163 is essential for maintaining accurate taxpayer records, ensuring that the information aligns with what is declared on tax forms.

- Form 5040: The Michigan Corporate Income Tax (CIT) Annual Return is related as it represents corporate tax filing, similar to how the Michigan 165 encompasses various tax types, including sales and withholding taxes for businesses.

- Form 1099: This is used to report various types of income other than wages. While the Michigan 165 summarizes tax liabilities, Form 1099 details income that may influence those liabilities, especially regarding withholding taxes.

- Form W-2: This form provides information about employee wages and taxes withheld. Similar to the Michigan 165, it contributes to the reporting of withholding tax for employees, crucial for accurate tax filings.

- Form 5086: The Vehicle Dealer Supplemental Schedule allows motor vehicle dealers to report sales tax collected on vehicle sales. Like the Michigan 165, it addresses tax liabilities but focuses specifically on vehicle transactions.

- Form 5083: The Fuel Supplier and Wholesaler Prepaid Sales Tax Schedule relates to fuel sales tax reporting. Similar to the Michigan 165, it deals with taxes due, though it focuses on the fuel sector.

- Form 5050: The Michigan Treasury Online (MTO) Account Registration form is necessary for online tax filings. While the Michigan 165 is a return form, Form 5050 establishes the account needed to facilitate that return electronically.

Dos and Don'ts

When completing the Michigan 165 form, it’s crucial to handle the process carefully to avoid complications. Here are some important dos and don’ts to keep in mind:

- Do file the form electronically if possible. This simplifies the process and reduces errors.

- Don't use the 165 form as an amended return. If you need to amend, use the specific Amended Annual Return form (Form 5082).

- Do ensure that all business information, like the account number and address, is accurate and complete.

- Don't leave any fields blank. If a tax type doesn’t apply, write “0” instead of leaving it empty.

- Do keep proper records to substantiate deductions claimed, such as receipts or exemption certificates.

- Don't forget to claim any allowable discounts for timely payments, as this can reduce your total tax due.

- Do verify that you are registered for the appropriate tax types before reporting sales, use, or withholding taxes.

- Don't file late. Penalties and interest can accumulate quickly, so be sure to submit by the deadline.

- Do sign and date the form. Both the taxpayer and the preparer must provide their information clearly.

Following these steps can help ensure a smoother filing experience and prevent issues with the Michigan Department of Treasury.

Misconceptions

- It's just for sales tax. Many people believe the Michigan 165 form is only for sales tax. In reality, it encompasses not just sales tax but also use tax and withholding tax, making it a comprehensive annual return for various tax types.

- You can amend it for corrections. There's a misconception that this form can serve as an amended return. However, the Michigan 165 form cannot be used for amendments. Instead, one must file a separate amended return using the 2021 Sales, Use and Withholding Taxes Amended Annual Return (Form 5082).

- Filing late incurs no penalties. Another common myth is that filing the return late won't affect payment. This is incorrect. If filed after the deadline, penalties and interest may apply based on the amount due, particularly if additional tax is owed.

- All information can be submitted online. While electronic filing is encouraged, some taxpayers mistakenly think they can do everything online without restrictions. Certain taxpayers, specifically those with 250 or more employees, are mandated to file withholding returns electronically. The submission process has specific requirements that shouldn’t be overlooked.

Key takeaways

Key Takeaways About the Michigan 165 Form

- This form is also known as the 2021 Sales, Use and Withholding Taxes Annual Return.

- The deadline for filing is February 28, 2022. Make sure to submit it on time to avoid penalties.

- You cannot use this form to amend previous returns; use Form 5082 for amendments.

- Ensure that your business name and account number (FEIN or TR Number) are accurately filled in at the top of the form.

- Gather total gross sales for the year being reported, including sales of tangible personal property.

- Identify any allowable deductions such as bad debts, resale claims, and agricultural production exemptions.

- The form allows electronic filing through the Michigan Treasury Online (MTO) system, making it easier for taxpayers.

- Include all necessary signatures on the form. Incomplete forms may lead to delays or rejections in processing.

- Be aware of potential penalties for late filing or payment; calculating these accurately is important to avoid surprises.

- If taxes were collected in excess of what is owed, you can report that on the form as well.

Browse Other Templates

What Does Osha Look for When Inspecting a Workplace - The checklist promotes a systematic review of training programs related to personal protective equipment and tools.

Illinois Department of Financial and Professional Regulation - Insurance must cover minimum liability requirements.