Fill Out Your Rbc Co Applicant Form

The RBC Co-Applicant Request Form is essential for individuals looking to expand their financial opportunities through shared credit card accounts. This form allows a primary cardholder to request the addition of a co-applicant to their existing RBC credit card account, such as the Cash Back Mastercard or Visa Classic. Applicants will need to provide personal details, including names, addresses, and relationship to the primary cardholder. This form outlines important terms regarding interest rates for purchases and cash advances, emphasizing the significance of making timely payments to avoid higher rates. Notably, there are no annual fees associated with these credit cards, but various other charges may apply, such as cash advance fees and over-limit fees. The document stipulates that both the primary cardholder and co-applicant share responsibility for any amounts owed on the account. Joint disclosure options are available, allowing one address to receive all regulatory documents, or individual addresses can be used to send separate copies. Ultimately, this form not only facilitates credit expansion but also encourages a shared financial commitment between the primary cardholder and co-applicant.

Rbc Co Applicant Example

RBC® Cash Back Mastercard‡, Visa‡ Classic Student,

RBC Rewards® Visa Gold, Visa Classic and RBC Rewards+® Visa

(subject to change) |

03798 (05/2022) |

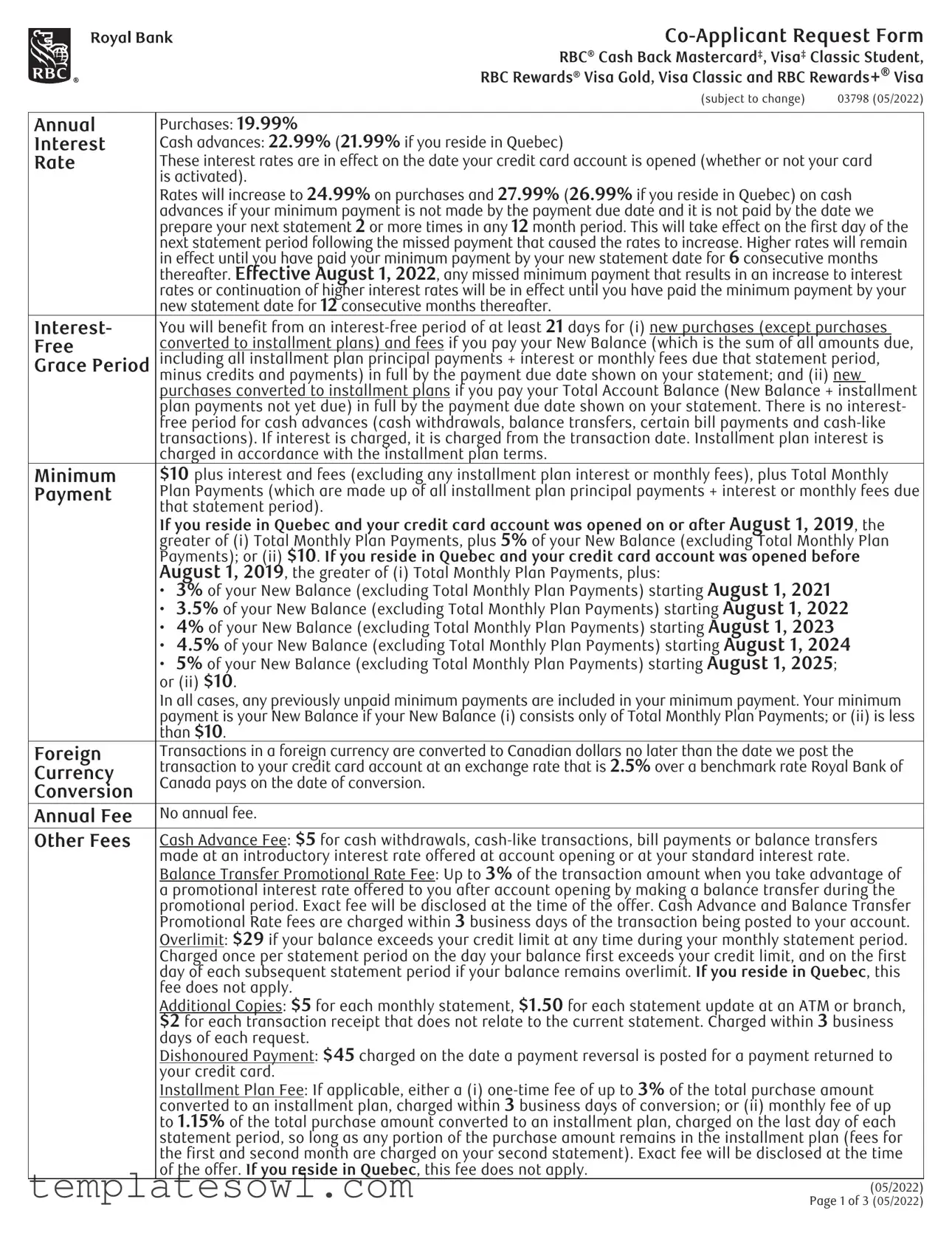

Annual |

Purchases: 19.99% |

|

Interest |

Cash advances: 22.99% (21.99% if you reside in Quebec) |

|

Rate |

These interest rates are in effect on the date your credit card account is opened (whether or not your card |

|

|

is activated). |

|

|

Rates will increase to 24.99% on purchases and 27.99% (26.99% if you reside in Quebec) on cash |

|

|

advances if your minimum payment is not made by the payment due date and it is not paid by the date we |

|

|

prepare your next statement 2 or more times in any 12 month period. This will take effect on the first day of the |

|

|

next statement period following the missed payment that caused the rates to increase. Higher rates will remain |

|

|

in effect until you have paid your minimum payment by your new statement date for 6 consecutive months |

|

|

thereafter. Effective August 1, 2022, any missed minimum payment that results in an increase to interest |

|

|

rates or continuation of higher interest rates will be in effect until you have paid the minimum payment by your |

|

|

new statement date for 12 consecutive months thereafter. |

|

Interest- |

You will benefit from an |

|

Free |

converted to installment plans) and fees if you pay your New Balance (which is the sum of all amounts due, |

|

Grace Period |

including all installment plan principal payments + interest or monthly fees due that statement period, |

|

|

minus credits and payments) in full by the payment due date shown on your statement; and (ii) new |

|

|

purchases converted to installment plans if you pay your Total Account Balance (New Balance + installment |

|

|

plan payments not yet due) in full by the payment due date shown on your statement. There is no interest- |

|

|

free period for cash advances (cash withdrawals, balance transfers, certain bill payments and |

|

|

transactions). If interest is charged, it is charged from the transaction date. Installment plan interest is |

|

|

charged in accordance with the installment plan terms. |

|

Minimum |

$10 plus interest and fees (excluding any installment plan interest or monthly fees), plus Total Monthly |

|

Payment |

Plan Payments (which are made up of all installment plan principal payments + interest or monthly fees due |

|

|

that statement period). |

|

|

If you reside in Quebec and your credit card account was opened on or after August 1, 2019, the |

|

|

greater of (i) Total Monthly Plan Payments, plus 5% of your New Balance (excluding Total Monthly Plan |

|

|

Payments); or (ii) $10. If you reside in Quebec and your credit card account was opened before |

|

|

August 1, 2019, the greater of (i) Total Monthly Plan Payments, plus: |

|

|

• 3% of your New Balance (excluding Total Monthly Plan Payments) starting August 1, 2021 |

|

|

• 3.5% of your New Balance (excluding Total Monthly Plan Payments) starting August 1, 2022 |

|

|

• 4% of your New Balance (excluding Total Monthly Plan Payments) starting August 1, 2023 |

|

|

• 4.5% of your New Balance (excluding Total Monthly Plan Payments) starting August 1, 2024 |

|

|

• 5% of your New Balance (excluding Total Monthly Plan Payments) starting August 1, 2025; |

|

|

or (ii) $10. |

|

|

In all cases, any previously unpaid minimum payments are included in your minimum payment. Your minimum |

|

|

payment is your New Balance if your New Balance (i) consists only of Total Monthly Plan Payments; or (ii) is less |

|

|

than $10. |

|

Foreign |

Transactions in a foreign currency are converted to Canadian dollars no later than the date we post the |

|

Currency |

transaction to your credit card account at an exchange rate that is 2.5% over a benchmark rate Royal Bank of |

|

Canada pays on the date of conversion. |

||

Conversion |

||

|

||

Annual Fee |

No annual fee. |

|

Other Fees |

Cash Advance Fee: $5 for cash withdrawals, |

|

|

made at an introductory interest rate offered at account opening or at your standard interest rate. |

|

|

Balance Transfer Promotional Rate Fee: Up to 3% of the transaction amount when you take advantage of |

|

|

a promotional interest rate offered to you after account opening by making a balance transfer during the |

|

|

promotional period. Exact fee will be disclosed at the time of the offer. Cash Advance and Balance Transfer |

|

|

Promotional Rate fees are charged within 3 business days of the transaction being posted to your account. |

|

|

Overlimit: $29 if your balance exceeds your credit limit at any time during your monthly statement period. |

|

|

Charged once per statement period on the day your balance first exceeds your credit limit, and on the first |

|

|

day of each subsequent statement period if your balance remains overlimit. If you reside in Quebec, this |

|

|

fee does not apply. |

|

|

Additional Copies: $5 for each monthly statement, $1.50 for each statement update at an ATM or branch, |

|

|

$2 for each transaction receipt that does not relate to the current statement. Charged within 3 business |

|

|

days of each request. |

|

|

Dishonoured Payment: $45 charged on the date a payment reversal is posted for a payment returned to |

|

|

your credit card. |

|

|

Installment Plan Fee: If applicable, either a (i) |

|

|

converted to an installment plan, charged within 3 business days of conversion; or (ii) monthly fee of up |

|

|

to 1.15% of the total purchase amount converted to an installment plan, charged on the last day of each |

|

|

statement period, so long as any portion of the purchase amount remains in the installment plan (fees for |

|

|

the first and second month are charged on your second statement). Exact fee will be disclosed at the time |

|

|

of the offer. If you reside in Quebec, this fee does not apply. |

|

|

(05/2022) |

|

|

Page 1 of 3 (05/2022) |

RBC® Cash Back Mastercard‡, Visa‡ Classic Student,

RBC Rewards® Visa Gold, Visa Classic and RBC Rewards+® Visa

(subject to change) |

03798 (05/2022) |

PRIMARY CARDHOLDER INFORMATION

PRIMARY CARDHOLDER NAME

CREDIT CARD NUMBER (REQUIRED)

FIRST NAME/INITIAL |

LAST NAME |

4 5 1 9

CLIENT CARD NUMBER (IF APPLICABLE)

We are required to give you regulatory disclosure documents (for example, your initial disclosure statement or your monthly statements) including a copy of the RBC Royal Bank® Credit Card Agreement. We will send each of you your own separate copy of these documents unless both of you consent to receiving joint disclosure. Joint disclosure means these documents will be sent to one address.

We each want to receive separate disclosure documents at the address for each borrower that appears in your records.

We want to receive joint disclosure documents at the address for the Primary Cardholder. We do not want to receive separate disclosure documents for each borrower.

MR. |

MS. |

DR. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

MRS. |

MISS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

FIRST NAME |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

INITIAL |

|

|

LAST NAME |

||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

HOME ADDRESS / APT. NO. / STREET NUMBER (if different from primary cardholder) (valid civic address required – P.O. Box, Rural Route, or General Delivery are not acceptable) CITY / TOWN |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PROVINCE / TERRITORY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

POSTAL CODE |

|

|

|

|

|

|

|

TELEPHONE NUMBER (IF DIFFERENT FROM PRIMARY CARDHOLDER) |

||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SOCIAL INSURANCE NUMBER∞ (OPTIONAL) |

|

|

|

OCCUPATION (REQUIRED) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||

4 |

5 |

|

1 |

9 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

M |

M |

D |

D |

|

Y |

|

Y |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

RBC ROYAL BANK CLIENT CARD NUMBER (IF APPLICABLE) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

DATE OF BIRTH (REQUIRED) |

|

|

|

|

RELATIONSHIP TO PRIMARY CARDHOLDER |

|||||||||||||||||||||||||||||||||||||||||||||||||||

IMPORTANT – PRIMARY CARDHOLDER AND

RBC aims to ensure our products and services are right for our clients; however we are not always able to do so when our clients use our

The Primary Cardholder on the RBC Royal Bank® credit card account (the Account) requests that we (Royal Bank of Canada) issue a credit card of the same type as currently issued on the Account to the

¡All the information that you have supplied in this Request Form is true and complete.

¡If you have chosen joint disclosure above, then both of you acknowledge that we may consider the Primary Cardholder as having the authority and being your personal representative to receive the RBC Royal Bank Credit Card Agreement (Agreement) on the

¡If the

¡The

¡The

¡You are each fully responsible for all amounts owing under the Account, irrespective of which one of you incurred, or which credit card was used to incur any particular charge. This also means that the

Your Account must be in good standing at the time the request is received, and the

You understand that this request is subject to credit approval and that we may refuse to issue a credit card to the

Yes, please add the additional cardholder as an Authorized User if the

|

X |

|

|

|

X |

|

|

|

|

Primary Cardholder Signature (REQUIRED) |

|

|

|

Date |

|||

|

|

|

|

|

|

|

|

|

SEND THE FORM TO US FOR PROCESSING BY MAIL: RBC ROYAL BANK C/O ADMINISTRATION DEPARTMENT, P.O. BOX 8400, STN TERMINAL, VANCOUVER, BC V6B 9Z9

(05/2022)

Page 2 of 3 (05/2022)

Important! Please read these terms, which are part of this request form.

RESPECTING YOUR PRIVACY IS IMPORTANT TO US

Periodically we provide you with information about products and services we feel would interest you. However, if you prefer not to receive such information, please let us know by calling

COLLECTING YOUR PERSONAL INFORMATION

We collect financial and other information about you from time to time such as:

•information establishing your identity (for example: name, address, phone number, date of birth, etc.) and your personal background;

•information about your transactions or other dealings with and through us;

•information you provide in an application for any of our products and services;

•information about your use of our products and services; and

•information about financial behaviour such as your payment history and credit worthiness.

We collect and confirm this information during the course of our relationship. We obtain this information from a variety of sources, including from you; from your use of our products and services; from service arrangements you make with or through us; from credit reporting agencies, other financial or lending institutions, or insurers; from registries; from fraud detection and prevention agencies, service providers, or regulatory or governmental bodies; from references you provide to us; and from other sources, as is necessary for the provision of our products and services.

You acknowledge receipt of notice that from time to time reports about you may be obtained by us from credit reporting agencies.

USING YOUR PERSONAL INFORMATION

This information may be used from time to time for the following purposes:

•to verify your identity and investigate your personal background;

•to open and operate your account(s) and provide you with products and services you may request;

•to maintain up to date records;

•to manage our risks and operations, and detect and prevent fraud or suppress financial abuse;

•to better understand your financial situation;

•to determine your eligibility for products, services, programs and promotions;

•to manage and administer loyalty programs and promotions;

•to help us better understand the current and future needs of our clients;

•to communicate to you any benefit, feature and other information about products and services you have with us;

•to facilitate the operation of payment networks including to process transactions and resolve disputes;

•to help us better manage our business and your relationship with us;

•to create aggregated and anonymous information, statistics, and reports and to generate data insights, analysis, and predictive models; and

•as required or permitted by law.

We may also use this information as described in “Other Uses and Disclosures of Your Personal Information” below.

DISCLOSING YOUR PERSONAL INFORMATION

We make this information available to our employees, agents and service providers, who require access for the purposes described above. Our employees, agents and service providers are required to maintain the confidentiality of this information.

In the event our service provider is located outside Canada, the service provider is bound by, and this information may be disclosed in accordance with, the laws of the jurisdiction in which the service provider is located.

We may share this information with other organizations (such as other financial or lending institutions, or insurance companies), fraud detection and prevention agencies, service providers, or regulatory or governmental bodies to prevent, detect or suppress financial abuse, fraud or other criminal activity, protect our assets and interests, defend or settle claims, manage risks and resolve disputes.

We share this information with the operators and participants of payment networks to process payments and other transactions, manage risks, detect and prevent fraud, maintain up to date records, resolve disputes and administer loyalty programs, promotional activities or other activities related to your Credit Card or Account.

We share your credit, financial and other related information with credit reporting agencies for the purpose of maintaining the accuracy and integrity of the credit reporting system. Credit reporting agencies may share this information with others.

We share this information with your consent or where required in order to facilitate the provision or administration of a product or service that you have requested.

We collect and share this information with RBC companies (i) to manage our risks and operations and those of RBC companies, (ii) to comply with valid requests for information about you from regulators, government agencies, public bodies or other entities who have a right to issue such requests, and (iii) to let RBC companies know your choices under “Other Uses and Disclosures of Your Personal Information” below for the purpose of knowing and honouring your choices.

We share this information where permitted or required by law, such as to comply with valid requests for information about you from regulators, government agencies, public bodies or other entities who have a right to issue such requests, or to collect a debt owed to us. We may share this information in connection with the sale of all or part of our business or assets.

If we have your social insurance number, we may use it for tax related purposes if you hold a product generating income and share it with the appropriate government agencies, and we may also share it with credit reporting agencies as an aid to identify you.

OTHER USES AND DISCLOSURES OF YOUR PERSONAL INFORMATION

•We may use and disclose this information to promote our products and services, and promote products and services of RBC companies or third parties we select, which may be of interest to you. We may communicate with you through various channels using the contact information you have provided.

•We may also, where not prohibited by law, share this information with RBC companies for the purpose of referring you to them or promoting to you products and services which may be of interest to you. We and RBC companies may communicate with you through various channels using the contact information you have provided. You acknowledge that as a result of such sharing they may advise us of those products or services provided.

•If you also deal with RBC companies, we may, where not prohibited by law, consolidate this information with information they have about you to allow us and any of them to manage your relationship with RBC companies and our business.

You understand that we and RBC companies are separate, affiliated corporations. RBC companies include our affiliates which are engaged in the business of providing any one or more of the following services to the public: deposits, loans and other personal financial services; credit, charge and payment card services; trust and custodial services; securities and brokerage services; and insurance services.

You may choose not to have this information shared or used for these other purposes described above under “Other Uses and Disclosures of Your Personal Information” by contacting us as set out below. In this event: (i) you will not be refused credit or other services just for making this choice; (ii) we will respect your choices; and (iii) we will share your information with RBC companies for the purpose of knowing and honouring your choices.

If you are applying for a

YOUR RIGHT TO ACCESS YOUR PERSONAL INFORMATION

You may obtain access to your personal information we hold about you at any time and review its content and accuracy, and have it amended as appropriate; however, access may be restricted as permitted or required by law. To request access to your personal information, to ask questions about our privacy policies, or to request that your personal information not be used for any or all of the purposes outlined in “Other Uses or Disclosures of Your Personal Information”, or to ask that your social insurance number not be shared with a credit reporting agency as an identifier, you may do so now or at any time in the future by:

•contacting your branch; or

•calling us

OUR PRIVACY POLICIES

You may obtain more information about our privacy policies by asking for a copy of our “Financial fraud prevention and privacy protection” brochure, by calling us at the toll free number shown above or by visiting our website at www.rbc.com/ privacysecurity.

While we make a considerable effort to avoid any discrepancies between our marketing materials and the RBC Royal Bank Credit Card Agreement you will receive with your card, in the event there is a discrepancy, the Credit Card Agreement will prevail.

®/ ™ Trademark(s) of Royal Bank of Canada. RBC and Royal Bank are registered trademarks of Royal Bank of Canada.

‡ All other trademarks are the property of their respective owner(s).

∞ Optional but recommended. By including this information we will be able to process your request form more quickly and accurately. See above for our use of your Social Insurance Number.

Page 3 of 3 (05/2022)

Form Characteristics

| Fact Name | Details |

|---|---|

| Form Name | Co-Applicant Request Form for various RBC credit cards. |

| Version Date | Form version is dated May 2022 (03798 / 05/2022). |

| Applicable Credit Cards | Includes RBC® Cash Back Mastercard‡, Visa‡ Classic Student, RBC Rewards® Visa Gold, Visa Classic, and RBC Rewards+® Visa. |

| Interest Rates | Annual purchases at 19.99%; cash advances at 22.99% (21.99% in Quebec). |

| Missed Payments | Rates can increase to 24.99% for purchases and 27.99% for cash advances after missed payments. |

| Minimum Payment Requirement | Minimum payment varies based on balance; $10 if only Total Monthly Plan Payments exist. |

| Foreign Transactions | Foreign transactions incur a 2.5% currency conversion fee. |

| Additional Fees | Cash advance fee is $5; overlimit fee is $29 (if applicable). |

| Privacy Policies | Personal information usage and sharing policy is detailed, respecting your privacy. |

Guidelines on Utilizing Rbc Co Applicant

Once you've gathered your information and decided to complete the RBC Co-Applicant Form, it’s time to dive in. This form allows a co-applicant to be added to an existing credit card account. Whether that’s your spouse, partner, or someone else, it's essential to fill it out accurately to ensure a smooth application process. Here’s how to do it step-by-step.

- Gather your information: Make sure you have all necessary details at hand. This includes information for both the primary cardholder and the co-applicant.

- Fill in primary cardholder information: Enter the primary cardholder’s full name and credit card number. This is crucial to link the new co-applicant with the correct account.

- Co-Applicant Information: Input the co-applicant’s details. This includes their first name, last name, home address, city, province/territory, postal code, and telephone number. Make sure the address is valid.

- Date of Birth: Enter the date of birth for the co-applicant. This information is required to verify their identity.

- Social Insurance Number: Providing the co-applicant’s Social Insurance Number is optional, but it can help in processing the application more quickly.

- Occupation: Fill in the co-applicant's occupation. This information is typically required for credit assessment purposes.

- Relationship to primary cardholder: Indicate the nature of the relationship between the primary cardholder and the co-applicant (e.g., spouse, partner).

- Select disclosure preference: Choose whether you want to receive separate disclosure documents or joint disclosure with documents sent to the primary cardholder's address.

- Signatures: Both the primary cardholder and the co-applicant must sign and date the form to confirm agreement to the terms.

- Mail the form: Send the completed form to RBC for processing at the address specified in the form.

After you submit the form, expect the processing of your request to take around three to four weeks. Stay alert for any follow-up communications from RBC regarding the status of the application.

What You Should Know About This Form

1. What is the RBC Co-Applicant Request Form used for?

The RBC Co-Applicant Request Form is used when a primary cardholder wants to add another individual as a co-applicant for a credit card. This allows the co-applicant to obtain a credit card that shares the same account as the primary cardholder. It is important for both parties to understand their responsibilities and liabilities regarding the account.

2. Who can be a co-applicant for an RBC credit card?

A co-applicant must be a resident of Canada and have reached the age of majority in their province or territory of residence. It's important to note that only one co-applicant can be added to an account at a time. Both the primary cardholder and the co-applicant need to agree to the terms outlined in the form before proceeding.

3. What information is required on the form?

The form requires both the primary cardholder's and co-applicant's personal information. This includes names, addresses, telephone numbers, date of birth, and occupation. The co-applicant may also provide their social insurance number, though this is optional. An important part of the form is ensuring that all information provided is accurate and complete.

4. What are the responsibilities of the co-applicant?

By signing the form and utilizing the credit card, the co-applicant agrees to take full responsibility for any charges incurred on the account. This means that the co-applicant is financially accountable for any balance owed, regardless of who made the charges. Each party will also have access to the account information and transactions.

5. How long does it take to process this request?

Once the RBC Co-Applicant Request Form is submitted, you can expect the approval and delivery of the new RBC credit card to take about three to four weeks. It's crucial to ensure that the request is completed and submitted correctly to avoid any delays in processing.

6. What if the co-applicant does not qualify for the credit card?

If the co-applicant does not meet the qualification criteria, the primary cardholder may request to add the individual as an Authorized User instead. This option provides the individual access to the account without the same level of financial responsibility and liability as a co-applicant.

7. Can we choose joint disclosure of account information?

Yes, both the primary cardholder and the co-applicant have the option to choose joint disclosure of account information. This means that all regulatory documents, such as monthly statements and credit card agreements, will be sent to one address. Alternatively, separate disclosures can be requested, allowing each individual to receive their own documentation at their respective addresses. This choice should be indicated on the form.

Common mistakes

When completing the RBC Co-Applicant Request Form, individuals often overlook essential details that can lead to delays or complications in the application process. One common mistake is failing to provide complete information. Each section of the form must be filled out thoroughly. Omissions can result in the application being returned or denied, requiring unnecessary rework.

Another frequent error is incorrectly filling out the personal information. This includes information such as the co-applicant’s name, date of birth, and address. Accuracy is vital; any discrepancies between what is provided and what is on file with credit bureaus may raise red flags, hindering the approval process.

Many applicants do not pay close attention to the required signature fields. Both the primary cardholder and the co-applicant must sign the form. Without both signatures, the application may be considered incomplete, resulting in further delays.

Individuals sometimes neglect to check their contact information, particularly the phone number and email address. If the information is outdated or incorrect, it can obstruct communication regarding the application, potentially causing missed notifications about its status.

Misunderstanding the joint disclosure option can also create problems. If both parties wish to receive separate statements, they must indicate this clearly. If joint disclosure is chosen without proper consent, further complications can arise with information access and privacy standards.

Additionally, many applicants fail to verify income and occupation details. These are crucial factors in assessing creditworthiness. Providing incorrect or vague information can lead to setbacks, as financial institutions count on this information to gauge the risk involved in issuing credit.

Another mistake involves not being aware of the residency requirements. The co-applicant must be a resident of Canada and of legal age in their province or territory. Failing to satisfy these conditions could lead to an outright denial of the application.

Some applicants overlook the necessity of including optional information, such as the Social Insurance Number. While it is not mandatory, providing this can expedite the processing of the request. Omitting it may lead to delays due to additional verification processes.

Moreover, forgetting to keep a copy of the submitted application can create confusion regarding what was included. Retaining a copy allows both parties to revisit the details should any questions arise during processing, thus facilitating smoother communication with the bank.

Finally, many do not carefully review the terms and conditions associated with the application. It is essential to understand the responsibilities and obligations tied to the credit card. Ignoring these details can lead to misunderstandings about fees, payments, and interest rates, which can significantly impact financial planning.

Documents used along the form

When applying for a credit card, such as the RBC® Cash Back Mastercard or other RBC card options, certain forms and documents accompany the Co-Applicant Request Form. Understanding these documents can facilitate a smoother application process and clarify responsibilities and rights.

- RBC Royal Bank Credit Card Agreement: This is a crucial document outlining the terms and conditions associated with your credit card, including interest rates and fees. Each user will receive a copy to ensure clarity on the cardholder's management practices.

- Credit Report Authorization Form: This form allows the bank to assess the creditworthiness of the co-applicant. It typically requires the co-applicant's consent to access their credit history from reporting agencies.

- Identification Verification Documents: Generally required, these documents serve to confirm the identity of both the primary cardholder and the co-applicant. They may include government-issued photo ID, such as a driver's license or passport.

- Income Verification Documents: This document may consist of recent pay stubs or tax returns. Such documentation assists the bank in evaluating the co-applicant's financial capacity to manage credit obligations.

- Joint Disclosure Consent Form: If both parties agree to receive joint disclosure documents, this form outlines their choice. It commonly addresses how information about the account will be shared and indicates preferences for communication.

- Authorized User Agreement: This optional document can be used if the co-applicant does not qualify for a credit card. It outlines the rights and responsibilities of an authorized user on the credit account.

- Debt Responsibility Disclosure: This document informs both cardholders of their responsibilities for any outstanding amounts and clarifies that both are liable for the total balance incurred on the account.

Having a clear understanding of these accompanying documents is essential for both the primary cardholder and co-applicant. This awareness helps in making informed decisions while navigating the landscape of shared financial responsibility. The partnership formed through such agreements can foster a supportive financial environment, provided both parties stay informed and engaged.

Similar forms

- Credit Card Application Form: Like the Co-Applicant Request Form, this document also collects necessary personal information from both primary and secondary applicants to establish eligibility for a credit card. It requires signatures to process the application.

- Authorized User Request Form: This form allows a primary cardholder to add someone as an authorized user. Similar to the Co-Applicant form, it involves the collection of personal information and outlines the responsibilities of each party.

- Credit Card Agreement: This document details the terms and conditions associated with a credit card account. It is provided after the completion of forms like the Co-Applicant Request form and must be acknowledged by both parties.

- Account Disclosure Statement: Just as the Co-Applicant Request Form seeks to clarify terms, this document provides detailed information about fees, interest rates, and disclosure practices related to the credit card account.

- New Credit Card Terms and Conditions Notification: Upon acceptance of a credit card application, this similar document informs the applicants of any updates or changes in terms, much like the Co-Applicant form outlines responsibilities.

- Loan Request Form: This document requests a loan and collects personal information from applicants. It serves a similar purpose to the Co-Applicant Request form by determining eligibility for financial products, including credit cards.

Dos and Don'ts

When filling out the RBC Co-Applicant form, it’s important to follow specific guidelines to ensure your application is processed smoothly. Here’s a list of ten do’s and don’ts to keep in mind.

- Do read all instructions carefully before beginning to fill out the form.

- Do provide complete and accurate information for both the primary cardholder and co-applicant.

- Do check that all signatures are present—both the primary cardholder and co-applicant must sign the form.

- Do ensure the contact information listed is current and correct to avoid delays in processing.

- Do keep a copy of the completed form for your records.

- Don't skip any sections of the form, as incomplete applications may be rejected.

- Don't use a P.O. Box for the address; a valid civic address is required.

- Don't provide false or misleading information, as this can lead to denial of your application.

- Don't forget to review the terms and conditions before submitting; it’s crucial to understand your obligations.

- Don't submit the form if you know your account is not in good standing.

Misconceptions

Misunderstanding the RBC Co-Applicant Form can lead to confusion and unexpected issues. Let's clarify some common misconceptions:

- Everyone Qualifies Automatically: Not everyone will qualify for a co-applicant credit card. Approval is subject to credit review and specific eligibility criteria.

- Co-Applicants Share Responsibility Equally: While both the primary cardholder and the co-applicant are responsible for the account, it does not mean responsibilities are equally shared. The extent of liability may vary based on who incurred the charges.

- Joint Disclosure is Mandatory: Many believe joint disclosure of documents is required, but both parties can request individual copies of disclosures if they prefer.

- Co-Applicant Receives No Documentation: Contrary to popular belief, the co-applicant will receive important documentation, such as the credit card agreement, indicating their responsibility.

- Higher Interest Rates are Imposed Immediately: Some think that interest rates increase immediately if a minimum payment is missed. In reality, rates only increase after multiple missed payments over a specified time.

- There are No Fees for Cash Advances: It's a misconception that cash advances incur no fees. There are specific charges outlined for cash withdrawals and balance transfers.

- Information is Not Shared Between Applicants: Many assume that personal information remains confidential. However, both parties can access transaction details and account information.

- Only One Co-Applicant is Allowed: While it’s true that only one co-applicant is allowed per account, applicants may also consider adding authorized users later.

- Authorization Means Financial Independence: Just because a co-applicant has authority to use the card doesn't mean they are financially independent; they are still accountable for charges made on the account.

- Social Insurance Number is Mandatory: Although providing a Social Insurance Number can expedite processing, it is optional, not mandatory.

By dispelling these myths, individuals can navigate the co-applicant process with greater confidence and clarity.

Key takeaways

Filling out and using the RBC Co-Applicant form for credit cards is an important process. Here are key takeaways to keep in mind:

- Understand Eligibility: The co-applicant must be a resident of Canada and of legal age in their province or territory of residence.

- Accurate Information Required: Ensure all provided details are true and complete. Incomplete or inaccurate information can delay processing.

- Joint Disclosure Option: Decide whether you want separate disclosure documents or joint ones, which will be sent to the primary cardholder's address.

- Interest Rates: Be aware of the interest rates associated with your cards, including higher rates for missed payments.

- Minimum Payment Obligations: Understand that both the primary cardholder and co-applicant are responsible for all charges made on the account.

- Personal Information Use: Know how your personal information is collected, shared, and used. This includes credit checks and promotional offers.

- Timeframe for Approval: Allow three to four weeks for the processing and delivery of the credit card after submission.

- Authorized User Option: If the co-applicant does not qualify, the primary cardholder has the opportunity to add them as an authorized user, which offers limited responsibilities.

By following these key points, you can navigate the RBC Co-Applicant form more effectively and understand the implications of your application.

Browse Other Templates

Sinai Hospital Medical Records Phone Number - A list of all Memorial Hermann facilities is available on the release form for reference.

Annexure E Indian Passport - This affidavit can also be executed at Indian Missions abroad.