Fill Out Your Sr 330A Of Wbtr 1 Form

The SR 330A OF WBTR-1 Utilisation Certificate is a vital document in the financial management process for institutions receiving government grants in West Bengal. This form serves as proof that funds disbursed under a government grant have been properly used for their intended purposes. It requires specific details, including the sanction date, total amount sanctioned, and any unspent balances carried forward from previous years. The completion of the form involves a thorough certification that the financial aid has strictly adhered to the stipulations set forth by the Directorate of Technical Education & Training. With sections designated for documenting the exact expenditures and a summary of checks performed to ensure appropriate fund usage, this certificate is crucial for maintaining accountability in public funding. Ultimately, it underscores the recipient’s commitment to transparency and responsible financial stewardship within the context of the sanctioned grants.

Sr 330A Of Wbtr 1 Example

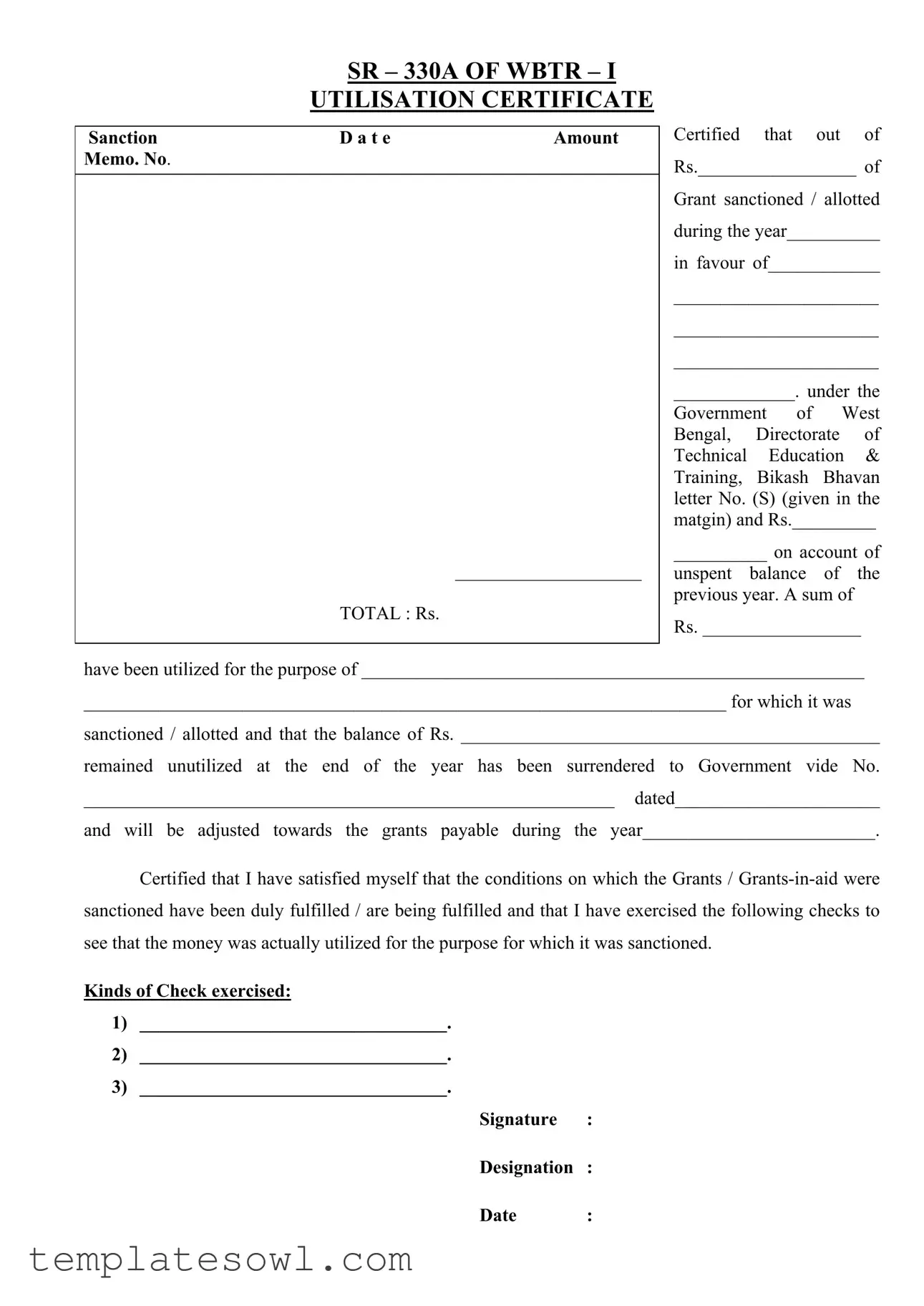

SR – 330A OF WBTR – I

UTILISATION CERTIFICATE

Sanction |

D a t e |

Amount |

Memo. No. |

|

|

____________________

TOTAL : Rs.

Certified that out of

Rs._________________ of

Grant sanctioned / allotted during the year__________

in favour of____________

______________________

______________________

______________________

_____________. under the

Government of West Bengal, Directorate of Technical Education & Training, Bikash Bhavan letter No. (S) (given in the matgin) and Rs._________

__________ on account of

unspent balance of the previous year. A sum of

Rs. _________________

have been utilized for the purpose of ______________________________________________________

_____________________________________________________________________ for which it was

sanctioned / allotted and that the balance of Rs. _____________________________________________

remained unutilized at the end of the year has been surrendered to Government vide No.

_________________________________________________________ dated______________________

and will be adjusted towards the grants payable during the year_________________________.

Certified that I have satisfied myself that the conditions on which the Grants /

sanctioned have been duly fulfilled / are being fulfilled and that I have exercised the following checks to

see that the money was actually utilized for the purpose for which it was sanctioned.

Kinds of Check exercised:

1)_________________________________.

2)_________________________________.

3)_________________________________.

Signature :

Designation :

Date :

Form Characteristics

| Fact Name | Description |

|---|---|

| Purpose of the Form | The SR 330A OF WBTR 1 form certifies the utilization of funds granted by the Government of West Bengal for specific projects under the Directorate of Technical Education & Training. |

| Governing Law | This form is governed by the financial rules and regulations established by the state government of West Bengal, specifically pertaining to financial management of grants. |

| Information Recorded | The form records important details such as the total amount sanctioned, the amount utilized, and the unutilized balance, along with conditions that ensure the grants were correctly utilized. |

| Verification Process | The signer of the form is required to certify that proper checks were exercised to verify the utilization of funds, ensuring accountability and oversight. |

Guidelines on Utilizing Sr 330A Of Wbtr 1

Filling out the Sr 330A Of Wbtr 1 form requires attention to detail and accuracy. You will be documenting financial information and ensuring that all necessary conditions are met. This process is vital for maintaining transparency and proper utilization of funds. Here’s how to complete the form step by step:

- Begin by entering the Sanction Date at the top of the form.

- Write the total amount sanctioned or allotted in the designated section.

- Fill in the Memo Number provided for the grant.

- In the section near the bottom, enter the total sum of the grant sanctioned during the specific year.

- Specify the purpose of the grant by providing detailed information about the organization or entity receiving the funds.

- Indicate the unspent balance of the previous year and the amount utilized for the sanctioned purpose.

- Document the remaining balance and confirm that it has been surrendered to the government by filling in the surrender number and date.

- In the checklist that follows, list at least three checks you exercised to ensure the funds were used appropriately.

- Sign the form where indicated, adding your designation and the date of signing.

By accurately filling out this form, you help ensure that accountability is maintained. Keep a copy for your records and submit the completed form as required. It's essential to be thorough and precise to avoid any potential issues down the line.

What You Should Know About This Form

What is the purpose of the SR 330A Of WBTR 1 form?

The SR 330A Of WBTR 1 form serves as an Utilization Certificate. It is used by organizations or institutions to certify how government grants were spent. The form outlines the total amount sanctioned, the purpose for which the funds were used, and any remaining balance that has been surrendered to the government. This form ensures accountability for the use of public funds.

Who is required to complete the SR 330A Of WBTR 1 form?

What information needs to be included in the form?

What happens if the remaining balance is not surrendered?

How does one verify that the funds were utilized properly?

Is there a deadline for submitting the SR 330A Of WBTR 1 form?

Common mistakes

Filling out the SR 330A Of WBTR 1 form can be a straightforward process, but there are common mistakes that people often make. One of the most frequent errors is leaving important fields blank. In particular, ensuring that the Memo Number and Total Amount sections are completed is essential. Omissions in these areas can lead to delays in processing or, worse, rejection of the form. Every detail matters, so it’s crucial to double-check that nothing is inadvertently skipped.

Another mistake is incorrect data entry. This can include writing amounts in the wrong format, misspelling names, or entering the wrong grant year's details. Such inaccuracies can create confusion and may require additional communication to rectify. It’s advisable to review all entries carefully. Utilizing clear handwriting or typing can minimize the risk of such errors.

A third common issue is improper certification. At the end of the form, there is a section requiring a signature, designation, and date. If any of these components are missing or incorrectly filled out, the form may be deemed incomplete. It’s important to verify that the certification is appropriately completed to avoid complications later on.

Lastly, the failure to provide a detailed explanation of the funds’ utilization is a mistake that should be avoided. Individuals often simply write “utilized for project” without giving specifics. A clear description not only highlights accountability but also aids in future assessments. Providing detailed descriptions lends credibility to the reporting process and helps show that funds were used appropriately.

Documents used along the form

The Sr 330A Of Wbtr 1 form is an important document used to certify the utilization of government grants within the Directorate of Technical Education & Training in West Bengal. Alongside this form, a few other documents and forms are commonly used to ensure proper financial oversight and accountability. Here are some of those key documents:

- Internal Audit Report: This report provides an assessment of the financial processes and controls relating to the use of government funds. It ensures that expenditures comply with budgetary guidelines and highlights any discrepancies that may arise.

- Grant Application Form: This form initiates the request for funding. It outlines the project's objectives, budget, and justifications for the grant, serving as a foundation for any subsequent financial transactions.

- Utilization Statement: This document supplements the Sr 330A form by detailing the specific expenditures made during the grant period. It offers a clearer picture of how the awarded funds were allocated and spent.

- Project Completion Report: Upon completing a project, this report summarizes the outcomes achieved against the initial goals. It provides an overview of both financial and operational aspects of the project, thereby supporting future funding applications.

- Balance Confirmation Letter: This letter serves to confirm any remaining balances of previous grants. It ensures transparency and accountability by documenting unspent funds that are to be returned or reallocated in subsequent financial periods.

These documents work together to ensure that government grants are utilized effectively and in accordance with established guidelines. Understanding how each document functions alongside the Sr 330A Of Wbtr 1 form can aid in promoting good financial practices and accountability in project management.

Similar forms

The SR 330A Of WBTR 1 form serves as a critical document in the process of reporting and certifying the utilization of government grants. Several other documents share similarities in structure and purpose. Here are five of those documents:

- Utilization Certificate (UC): This document affirms the actual amount of grant used by an organization. Like the SR 330A, it includes details regarding the sanctioned amount, the total utilized sums, and any remaining balance which needs to be surrendered or adjusted.

- Statement of Expenditure (SoE): The SoE outlines the expenditures made from the grant funds. Similar to the SR 330A, it demands a clear account of funds allocated, spent, and unspent amounts, providing transparency in financial reporting.

- Project Completion Report (PCR): A PCR details the outcomes of a funded project, including fund utilization. It parallels the SR 330A by requiring confirmation that the purpose of the grant has been fulfilled, often combining financial and narrative components.

- Annual Financial Statement: This statement presents a complete financial summary for the year. It is akin to the SR 330A in that it captures the grants received, utilized, and any remaining balances, offering a comprehensive view of financial health.

- Grant Finalization Report: This document is often submitted at the end of a grant period, summarizing total funds received and utilized. It is similar to the SR 330A as it focuses on the effective use of funds and compliance with the conditions set out in the grant agreement.

These documents work together to ensure that grants are managed effectively and transparently.

Dos and Don'ts

When completing the SR 330A OF WBTR 1 form, attention to detail is crucial. Here are some essential dos and don'ts:

- Do: Use clear and legible handwriting or type the information to ensure readability.

- Do: Fill in all required fields accurately, including the date and grant amounts.

- Do: Double-check the totals for consistency and correctness before submission.

- Do: Ensure all signatures and designations are included as required.

- Don't: Leave any sections blank; incomplete forms can lead to delays.

- Don't: Use abbreviations or unclear terms; clarity is key for reviewers.

- Don't: Submit the form without a thorough review; errors can be costly.

- Don't: Forget to mention any unspent balance clearly to avoid confusion.

Misconceptions

- Misconception 1: The SR 330A form is only for large organizations.

- Misconception 2: It’s unnecessary to include unspent balances.

- Misconception 3: Only financial officers need to fill out the form.

- Misconception 4: The form does not need to reflect the actual purpose of utilization.

- Misconception 5: Submitting the form is a one-time requirement.

- Misconception 6: The checks mentioned in the form are optional.

- Misconception 7: Once submitted, the contents of the form cannot be questioned.

This form can be utilized by smaller institutions as well, not just large organizations. Any educational or training institution receiving grants can complete this form.

On the contrary, detailing unspent balances is essential. The form specifies how much of the allocated grants were not used and indicates that those funds should be surrendered to the government.

While financial officers often handle this form, it’s crucial for any authorized representative who understands the utilization of funds to fill it out. This ensures accuracy and accountability.

This is incorrect. The form must clearly state how the funds were utilized, including specific projects or expenditures that align with the purpose of the grant.

Submitting the SR 330A form is a periodic task. It typically needs to be completed at the end of each fiscal year or grant period, reflecting ongoing financial oversight.

The checks are not optional; they are a critical part of the process. Certifying that funds were utilized correctly requires that appropriate checks were conducted.

This is not true. After submission, the details can be audited or questioned by the relevant authorities to ensure proper compliance and use of funds.

Key takeaways

Filling out the Sr 330A of Wbtr 1 form is an important process. It facilitates transparency in financial matters related to government grants. Here are some key takeaways to keep in mind:

- Ensure Accuracy: All details entered in the form should be precise and accurate, especially the Grant amount and dates.

- Completion of Required Fields: Every section that requires information must be completed to prevent processing delays.

- Utilization Purpose: Clearly state how the funds were utilized. Specificity helps in maintaining clarity and justifying the expenses.

- Unutilized Balance: If there are unutilized funds, they must be reported and surrendered correctly, adhering to government guidelines.

- Documentation: Keep copies of all documents associated with the grant for future reference or audits.

- Signature and Designation: Ensure the signature is from an authorized person, and the designation is accurately mentioned for accountability.

- Meeting Deadlines: Submit the form before the deadline to avoid penalties or issues with future grants.

- Preserve Records: Maintain records of all submitted forms and any correspondence for accountability and future reference.

Approaching this task with diligence and care will help ensure compliance and proper fund utilization. It contributes to a smooth operational process within the established structures.

Browse Other Templates

Mcdhh Interpreter Request - State the start time to ensure availability of the interpreter.

Cas 5 - It requires identification details such as surname, first name, and middle initial of the applicant.

What Is an Hvac System - Check the rated BTU input for the boiler and its condition.