Fill Out Your West Virginia Cd 3 Form

The West Virginia CD-3 form serves as a crucial tool for taxpayers seeking to settle outstanding tax liabilities with the state. It is designed for instances where there is uncertainty regarding the taxpayer's obligation or the ability of the state to collect the full amount owed. This form not only presents the taxpayer's offer to compromise their total liability but also outlines the terms and conditions that must be adhered to upon acceptance. The taxpayer must provide detailed information about their financial situation, including the types of taxes owed and the periods those taxes cover. Furthermore, the CD-3 form requires an initial payment along with potential monthly installments, while also detailing that interest will accrue on any outstanding balance. A significant stipulation of this offer is that all prior payments and credits against the liability will be retained by the state. Additionally, taxpayers are expected to comply with ongoing state tax laws for five years after acceptance. To support their offer, taxpayers must attach a financial statement and a justification for their request. The essence of the CD-3 form lies in its functionality to facilitate negotiations between the taxpayer and the state, ultimately aiming for a resolution that is beneficial to both parties.

West Virginia Cd 3 Example

|

West Virginia State Tax Department |

|

|||

|

Offer In Compromise |

|

|

|

|

|

Form |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Names and Address of Taxpayer |

|

|

Taxpayer Representative |

|

|

|

|

|

Name: |

|

|

|

|

|

Address |

|

|

|

|

|

Phone |

|

|

Social Security or Tax Identification Number |

|

||||

|

|

|

|||

|

|

|

|

|

|

To: State Tax Commissioner |

|

Date |

Amount of Offer |

|

Total Liability |

|

|

|

$ |

|

$ |

|

|

|

|

|

|

|

|

|

|

|

|

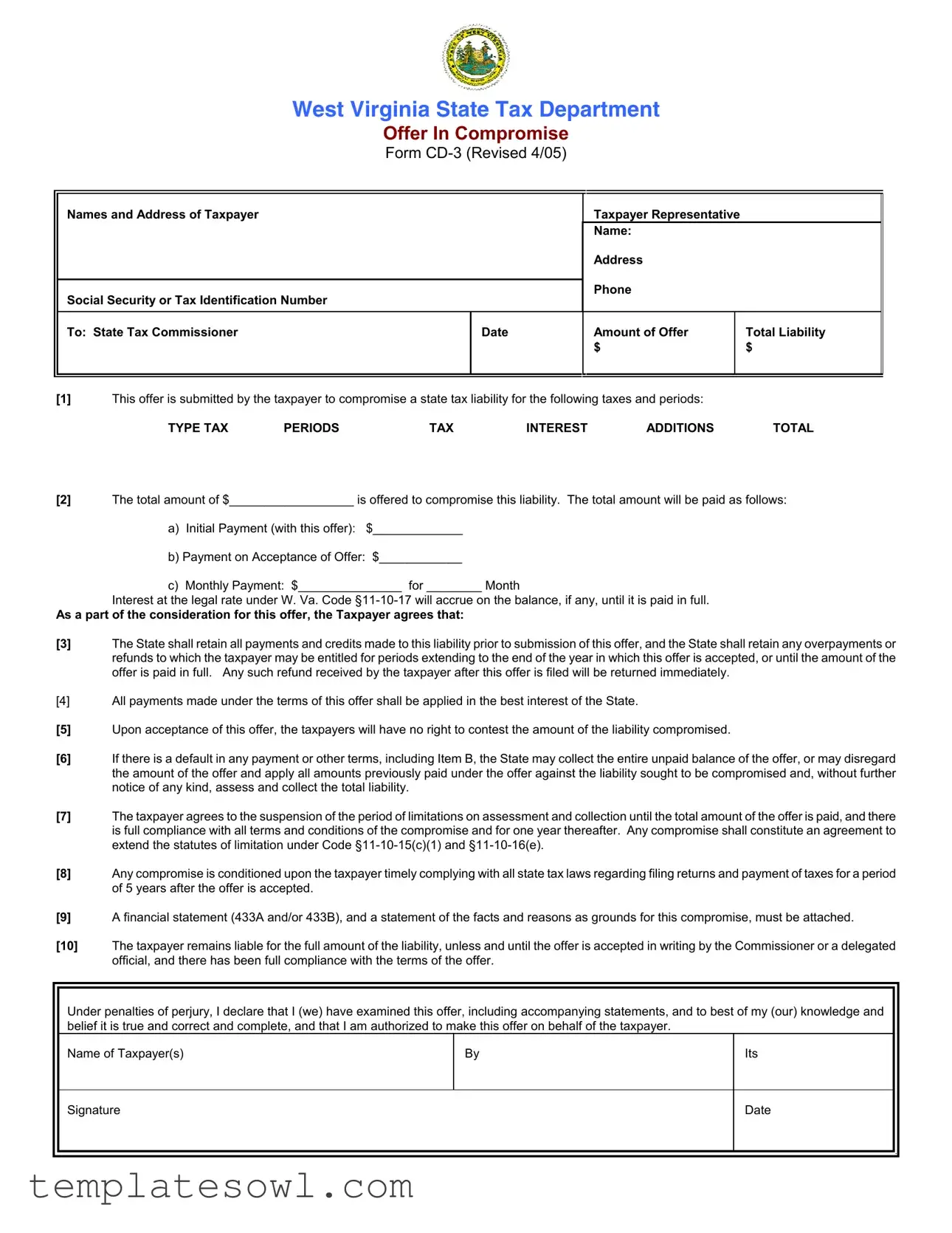

[1]This offer is submitted by the taxpayer to compromise a state tax liability for the following taxes and periods:

TYPE TAX |

PERIODS |

TAX |

INTEREST |

ADDITIONS |

TOTAL |

[2]The total amount of $__________________ is offered to compromise this liability. The total amount will be paid as follows:

a)Initial Payment (with this offer): $_____________

b)Payment on Acceptance of Offer: $____________

c)Monthly Payment: $_______________ for ________ Month

Interest at the legal rate under W. Va. Code

As a part of the consideration for this offer, the Taxpayer agrees that:

[3]The State shall retain all payments and credits made to this liability prior to submission of this offer, and the State shall retain any overpayments or refunds to which the taxpayer may be entitled for periods extending to the end of the year in which this offer is accepted, or until the amount of the offer is paid in full. Any such refund received by the taxpayer after this offer is filed will be returned immediately.

[4]All payments made under the terms of this offer shall be applied in the best interest of the State.

[5]Upon acceptance of this offer, the taxpayers will have no right to contest the amount of the liability compromised.

[6]If there is a default in any payment or other terms, including Item B, the State may collect the entire unpaid balance of the offer, or may disregard the amount of the offer and apply all amounts previously paid under the offer against the liability sought to be compromised and, without further notice of any kind, assess and collect the total liability.

[7]The taxpayer agrees to the suspension of the period of limitations on assessment and collection until the total amount of the offer is paid, and there is full compliance with all terms and conditions of the compromise and for one year thereafter. Any compromise shall constitute an agreement to extend the statutes of limitation under Code

[8]Any compromise is conditioned upon the taxpayer timely complying with all state tax laws regarding filing returns and payment of taxes for a period of 5 years after the offer is accepted.

[9]A financial statement (433A and/or 433B), and a statement of the facts and reasons as grounds for this compromise, must be attached.

[10]The taxpayer remains liable for the full amount of the liability, unless and until the offer is accepted in writing by the Commissioner or a delegated official, and there has been full compliance with the terms of the offer.

Under penalties of perjury, I declare that I (we) have examined this offer, including accompanying statements, and to best of my (our) knowledge and belief it is true and correct and complete, and that I am authorized to make this offer on behalf of the taxpayer.

Name of Taxpayer(s)

By

Its

Signature

Date

OFFERS IN COMPROMISE - INSTRUCTIONS

Authority

W. Va. Code

Reason for Compromise

We are allowed to compromise a liability for one or both of the following two (2) reasons: (1) doubt as to whether the taxpayer owes the liability; (2) doubt that we can collect the full amount of the liability. This form and instructions is only used in cases of doubt as to collectibility.

Policy

We will accept an offer in compromise when it is unlikely that we can collect the tax liability in full, and the amount offered reasonably reflects the amount we can collect. An offer in compromise is a legitimate alternative to declaring a case as currently not collectible or to a

The success of the compromise will be assured only if taxpayers make adequate compromise proposals consistent with their ability to pay the State. Taxpayers are expected to provide reasonable documentation to verify their ability to pay. The goal is a compromise which is in the best interest of both the taxpayer and the State. Where an offer in compromise appears to be a workable solution, the employee assigned the case will discuss the compromise with the taxpayer and, when necessary, assist in preparing the required forms. The taxpayer will be responsible for making the first offer for compromise.

Practical Consideration

It is the taxpayer's responsibility to show us why it would be in our best interest to accept your proposal. When we consider your offer we ask the following questions: (1) Could we collect the amount owed through liquidation of your assets or through an installment agreement? (2) Could we collect more from your assets and future income than is offered? (3) Would collection in the future result in more payment than is offered? (4) Would the public believe that the acceptance of your offer was a reasonable action?

The fact that you have no assets or income at this time from which the State could collect the liability does not mean that the State should simply accept any offer because it is all we can collect now. It would generally be better for us to reject a nominal amount and wait to see what collection potential would arise during the remainder of our

Additional Consideration

We believe that you benefit if we accept your offer because you can manage your finances without the burden of a tax liability. Therefore, we may require either: (1) A written agreement that will require you to pay a percentage of future earnings; and/or (2) A written agreement to give up present or future tax refunds.

Tax Compliance

(1)We will not accept your offer if you have not filed all tax returns. (2) We will also require that the taxpayer comply with all future filing and payment requirements. The terms of the offer require future compliance for a period of five (5) years.

Collection and Payments

The submission of an offer does not automatically suspend collection. If it appears the offer was filed to delay collection of the tax or that delay would hinder our ability to collect the tax, we will continue collection efforts. If you have agreed to make installment payments before you made the offer, those payments should continue.

Special Instructions for Offer in Compromise Form

(1)The Offer in Compromise form must be used to submit an offer. The form must be filed with the Compliance Division. If you have been working with a specific employee on your case, file the offer with that employee.

(2)Your full name, address and taxpayer identification number(s) must be entered at the top of the Offer form. If this is a joint liability (husband and wife) and both wish to make an offer, both names must be shown. If you are individually liable for a liability and are also jointly liable for another liability, and only one person is submitting an offer, only one offer must be submitted. If you are individually liable for one liability and jointly liable for another and both joint parties are submitting an offer, two (2) Offers must be submitted, one (1) for separate liability and one (1) for the joint liability.

(3)You must list all liabilities to be compromised in item (1). The types of tax, the periods, and the amounts must be specifically identified.

(4)The total amount you offer must be entered in item (2). The amount must not include any amount which has already been paid or collected on the liability. The amount submitted with the offer is entered in 2(a); the amount is to be paid on acceptance of the offer is entered in (2) (b) and any amount to be paid in installments, is entered in 2(c) in item 2. You should pay the amount of the offer in the shortest time possible, or we will reject your offer. Under no circumstances should the payment extend beyond two (2) years. Interest is due at the legal rate from the date of acceptance to the date of full payment.

(5)You must state in detail in item (9) why the State should accept your offer. Attach additional pages as necessary. Describes in detail why you believe the State cannot collect more than offered from your assets and your present and future income.

(6)The taxpayer(s) must sign and date the offer. If a person other than the taxpayer signs the offer, a power of attorney must be submitted with the offer.

(7)Form

What You Are Agreeing To

Please read the Offer in Compromise Form carefully so that you understand that you are agreeing to:

(1)The period for collection is suspended while the offer is pending, while any amount offered remains unpaid, and for one (1) year after all terms and conditions of the offer are fulfilled.

(2)You won't contest or appeal the amount of the liability if your offer is accepted.

(3)You give up of overpayments (refunds) for all tax periods through the year the offer is accepted, and until the amount of the offer is paid in full.

(4)The collection of the entire tax liability, if you do not comply with all the terms of the offer, i.e. payment, future compliance.

Form Characteristics

| Fact Name | Description |

|---|---|

| Form Purpose | The West Virginia CD-3 form is used by taxpayers to propose a settlement for state tax liabilities due to doubt about their collectibility. |

| Governing Law | This form falls under W. Va. Code §11-10-5q(c), which allows the State Tax Commissioner to compromise tax liabilities. |

| Key Requirements | Taxpayers must attach a financial statement (Form 433A and/or 433B) and provide a detailed explanation of why the compromise is justified. |

| Payment Terms | The offer must specify an initial payment, amount due upon acceptance, and any monthly payments over a defined period. |

| Compliance Obligations | Taxpayers must comply with all state tax laws for five years following the acceptance of the offer to maintain the compromise agreement. |

| Consequences of Default | If a taxpayer defaults on payments, the State may collect the entire remaining balance or disregard the offer entirely. |

Guidelines on Utilizing West Virginia Cd 3

Once you gather the necessary documents and information, you'll be ready to fill out the West Virginia Offer in Compromise Form CD-3. Completing this form accurately is crucial to ensure your offer is considered promptly. Follow these steps carefully.

- Fill in Your Personal Information: Start by entering the taxpayer's name, address, and contact information at the top of the form. If any representative is involved, include their name as well.

- Provide Identification Numbers: Enter your Social Security Number or Tax Identification Number where indicated.

- Address the Offer: Clearly state the amount of offer, total liability, and include the date. Specify the taxes and periods related to the liability.

- Detail Payment Structure: In Section (2), provide the total amount you are offering to compromise the liability. Break it down into the initial payment, payment upon acceptance, and monthly payment amounts.

- List all Liabilities: Mention each specific liability to be compromised, clearly indicating the type of tax, periods involved, and amounts.

- Explain Your Reasons: In Section (9), detail why you believe the State should accept your offer. Attach additional pages if necessary.

- Sign and Date: Ensure that either the taxpayer or an authorized representative signs the form. If someone else is signing, include a power of attorney.

- Attach Required Documents: Include Forms 433-A and/or 433-B, along with supporting documentation that verifies your financial status.

- Submit the Form: File the completed form and all attachments with the Compliance Division or the designated employee handling your case.

After submission, you will await a response from the State Tax Commissioner. It's essential to maintain compliance with all future tax obligations for five years following the acceptance of your offer. This will ensure that your compromise remains valid and beneficial.

What You Should Know About This Form

What is the West Virginia CD-3 form used for?

The West Virginia CD-3 form is the Offer In Compromise form used by taxpayers to propose a settlement of their state tax liability. This form allows taxpayers to offer a specific amount to resolve their unpaid taxes, penalties, and interest that may be difficult to collect in full. The state will review the offer and decide whether to accept it based on the taxpayer's financial situation and the likelihood of collecting the full amount owed.

Who should file the CD-3 form?

The CD-3 form should be filed by any taxpayer who believes they cannot pay their full state tax liability. This may apply to individuals or businesses experiencing financial difficulties, such as low income, high debts, or other extenuating circumstances that affect their ability to pay taxes. It is crucial that all tax returns are filed before submitting this form, as noncompliance with filing obligations may result in rejection of the offer.

What are the key components of the CD-3 form?

Key components of the CD-3 form include the taxpayer's information, details regarding the tax liability being compromised, the total amount of the offer, and a payment structure (including an initial payment and installment plan, if applicable). Taxpayers must also submit a financial statement (Form 433-A and/or 433-B) and a written explanation of why the offer is reasonable. Accepted offers require future compliance with all tax laws for five years.

What happens if my offer is accepted?

If the state accepts your offer, you must adhere to all the terms outlined in the agreement. This includes not contesting the accepted amount of tax liability, complying with future tax laws, and making all required payments within the specified timeframe. Additionally, any future overpayments will be retained by the state until your agreed-upon amount is paid in full.

What are the consequences of defaulting on my agreement?

Defaulting on any payment or other terms can lead to significant consequences. The state may collect the remaining balance of the offer immediately or disregard the offer and apply any previously made payments to the total liability owed. Furthermore, you may lose the benefit of the compromise, and the state can initiate collection actions without further notification.

Common mistakes

When filling out the West Virginia Offer in Compromise Form CD-3, many individuals unknowingly make mistakes that could jeopardize their chances of successfully compromising their tax liabilities. Here are six common mistakes to watch out for:

First, it's essential to clearly identify all the tax liabilities you wish to compromise. Many people fail to list each type of tax, the relevant periods, and the amounts accurately. This oversight can lead to confusion and possibly result in the rejection of the offer. Ensuring that every tax type and period is documented correctly is crucial for a smooth process.

Another common error is related to the total offer amount. Some taxpayers incorrectly include amounts already paid or assume prior payments should be counted toward the compromise. The total offered must strictly reflect what you are proposing, and it should not combine any amounts already collected by the state. Understand the distinction between what has been paid and what you are currently proposing.

Additionally, submitting the form without the required attachments is a frequent mistake. Taxpayers must include financial statements, specifically Form 433-A or 433-B, along with a detailed explanation of why the state should accept the offer. Providing clear, well-supported documentation helps convey your financial situation and strengthens your case.

Timing is also crucial when submitting the offer. Some individuals submit offers that extend payment arrangements beyond the stipulated two-year limit, which can lead to outright rejection. Be sure to structure any installment payments to comply with the timeline guideline set forth.

Another common oversight occurs when taxpayers fail to sign and date the form. If someone other than the taxpayer is signing the form, a power of attorney must be included. Leaving out this information could lead to delays. It is best to double-check all signatures and related documentation for completeness.

Lastly, many applicants do not take the time to clearly explain in detail why the State should accept their offer. Simply stating that you cannot pay your full tax liability is often not enough. A detailed explanation, attached to Item 9 of the form, along with supporting evidence, will significantly enhance the credibility of your offer.

By taking care to avoid these common mistakes when filling out the West Virginia CD-3 form, you can improve your chances for a successful compromise and a more manageable financial situation moving forward.

Documents used along the form

The West Virginia CD-3 form is part of a crucial process for individuals looking to settle their tax liabilities through an Offer in Compromise. This form is often accompanied by several other important documents and forms that aid in submitting a comprehensive and accurate proposal. Below is a list of relevant forms and documents commonly used alongside the West Virginia CD-3 form, each with a brief description.

- Form 433-A: This is a Collection Information Statement for individuals. It provides detailed information about the taxpayer’s income, expenses, assets, and liabilities to help the State Tax Department evaluate the Offer in Compromise.

- Form 433-B: This Collection Information Statement is designed for businesses. Just like Form 433-A, it collects necessary financial details that help assess the business's ability to meet tax obligations.

- Cover Letter: A cover letter explains the purpose of the Offer in Compromise submission. It outlines the taxpayer's situation, summarizes the offer proposal, and clarifies supporting documents included.

- Financial Documentation: This may include bank statements, pay stubs, property deeds, and other relevant financial records that confirm the information provided in Forms 433-A and 433-B.

- Statement of Facts: A narrative document detailing the specific circumstances that led to the tax liability. It supports the Offer in Compromise by explaining why the taxpayer believes the compromise is justified.

- Power of Attorney (if applicable): If a representative submits the Offer in Compromise on behalf of the taxpayer, a power of attorney must be included. This document authorizes the representative to act on behalf of the taxpayer in tax matters.

- Tax Returns: Copies of recent tax returns may be required to demonstrate compliance with tax laws and provide insight into the taxpayer’s financial status.

Including these additional documents helps provide clarity and strengthens the application when submitting the Offer in Compromise. Each form collectively ensures that the proposal is comprehensive and increases the likelihood of acceptance by the State Tax Department.

Similar forms

- IRS Form 656 - This form is used for submitting an Offer in Compromise to the Internal Revenue Service (IRS) to settle federal tax debts. Similar to the West Virginia CD-3, it allows taxpayers to propose a settlement amount based on their ability to pay and the likelihood of the IRS collecting the full tax liability.

- IRS Form 433-A - This form collects financial information about an individual taxpayer’s assets and income. Like the financial statement required with the CD-3, it helps assess the taxpayer's ability to pay and supports the offer being made.

- IRS Form 433-B - Specifically for businesses, this form gathers crucial financial data to evaluate a company's capacity to pay its tax debts. It is similar to the CD-3's requirement for a financial statement to establish the taxpayer's financial situation.

- State Offer in Compromise Forms - Other states have their own forms for tax compromise offers, closely mirroring West Virginia's CD-3. These forms typically require details about the taxpayer’s financial situation and the proposed offer amount.

- Installment Agreement Request (IRS Form 9465) - This form allows taxpayers to request a payment plan for their federal tax debts. It serves a similar purpose as a compromise offer in that it seeks manageable payment terms based on the taxpayer’s financial situation.

- Delinquent Tax Return Filing Forms - These state and federal forms are submitted to resolve tax debts from returns that have not been filed. Like the CD-3, filing these forms is often a prerequisite to negotiating any settlement or payment plan for tax liabilities.

- Financial Hardship Letters - A taxpayer may submit a letter to request temporary relief or compromise due to financial hardship. This type of correspondence is akin to the rationale provided in the CD-3 form to justify a reduced tax payment.

- Request for Collection Due Process Hearing (IRS Form 12153) - This form allows taxpayers to appeal IRS collection actions. Comparably, taxpayers may appeal decisions made after submitting a CD-3 if they believe the outcome is unjust, maintaining their right to challenge tax liabilities.

Dos and Don'ts

When filling out the West Virginia CD-3 form, it is crucial to approach the process with care and attention to detail. Here are some essential do's and don'ts to keep in mind:

- Do provide your full name, address, and taxpayer identification number accurately at the top of the form.

- Do specify all liabilities you wish to compromise, including tax types, periods, and amounts in item (1).

- Do attach a financial statement (Form 433-A and/or 433-B) and any supporting documents that justify your request.

- Do ensure your offer amount does not include any payments previously made on the liability.

- Don't leave out any requested information or documents, as missing details can lead to a rejection.

- Don't submit your offer if you have not filed all tax returns, as compliance is mandatory before acceptance.

Misconceptions

When it comes to understanding the West Virginia Offer in Compromise Form CD-3, many taxpayers hold misconceptions that can hinder their efforts to navigate tax liabilities. Here are six common misconceptions and the truths behind them:

- The offer guarantees acceptance. Many believe that submitting an Offer in Compromise (OIC) will automatically lead to acceptance. However, the state evaluates each offer on a case-by-case basis, considering factors such as collectibility and the taxpayer's financial situation.

- All tax liabilities are eligible for compromise. Not all tax debts can be settled through an OIC. The state only accepts offers based on doubt as to collectibility, meaning there must be uncertainty about whether the taxpayer can fully pay the owed amount.

- Submitting the form stops all collection activities. Some taxpayers think filing the CD-3 form will halt collection efforts immediately. This is not the case. If the state suspects the OIC is intended to delay payment, they may continue with collection actions.

- Future compliance is not a requirement. It’s a common belief that once an OIC is accepted, there are no further obligations. In reality, taxpayers must comply with all state tax laws for five years following acceptance of the offer.

- You can offer any amount you choose. Taxpayers often think they can propose any figure they want. However, the amount offered must be realistic, reflecting what the taxpayer can pay. The state expects a reasonable proposal based on the taxpayer’s financial capabilities.

- Financial statements aren’t necessary. Some assume they can submit an offer without detailed financial documentation. In fact, taxpayers must include a financial statement and a clear explanation of why the compromise should be granted, providing essential insight into their current financial state.

Understanding these misconceptions can make a significant difference in how taxpayers approach the West Virginia CD-3 form. Knowledge of the process can lead to more effective strategies and a higher likelihood of successful resolution of tax liabilities.

Key takeaways

Understanding the West Virginia CD-3 Offer in Compromise form is crucial for effectively managing state tax liabilities. Here are some key takeaways to consider:

- Purpose of the Form: The CD-3 form is specifically designed for taxpayers seeking to compromise a state tax liability due to doubts about either the existence of the liability or the ability to collect the full amount.

- Initial Payment Requirement: Upon submitting the offer, an initial payment must be included. Ensure that this amount aligns with your financial capacity.

- Comprehensive Documentation: Attach necessary financial statements (like Forms 433A and 433B) along with a detailed explanation of why the compromise is justified.

- Future Compliance: Taxpayers must continue complying with tax laws for five years following the acceptance of the offer. Failure to do so can result in the State's right to collect the full amount due.

- Retention of Payments: All payments made toward the liability prior to the offer will be retained by the State, and any overpayments or tax refunds may also be kept until the offer is resolved.

- Consequences of Default: If any payment terms are not met, the State may demand the entire unpaid balance immediately without further notice.

- Collection Attempts: Submitting the CD-3 offer does not stop collection efforts; it's imperative to stay current on any existing payment commitments until the offer is accepted.

- Signature Requirement: The form must be signed by the taxpayer(s), or a power of attorney must be included if someone else is signing on their behalf.

Submit the CD-3 form to the Compliance Division promptly, and ensure all entries are complete. Properly following these guidelines can facilitate a more favorable outcome for your tax situation.

Browse Other Templates

Texas Tax Relief Bill - Seek assistance if you have questions about filling out the application correctly.

Canon IP100 Setup Guide,Canon IP100 User Manual,Canon IP100 Quick Reference,Canon IP100 Troubleshooting Guide,Canon PIXMA IP100 Instructions,Canon IP100 Helpful Hints,Canon IP100 Operational Guide,Canon IP100 Support Handbook,Canon IP100 Care and Mai - Canon provides reliability information but does not guarantee complete accuracy.